Business

Engineering

Finance

Investing

Power Generation

Global Operations

Heating

Water Management

Waste Management

Capital Goods

Specialty Chemicals

Cooling

Boiler Manufacturing

Turnkey Projects

Waste Heat Recovery

Air Pollution Control

(1/17)

About:

Thermax is an engineering and capital goods firm based in Pune.

It operates globally through 34 international & 22 domestic offices & 14 manufacturing facilities, of which 10 are in 🇮🇳 & 4 are overseas. Thermax is present in

over 90 countries.

About:

Thermax is an engineering and capital goods firm based in Pune.

It operates globally through 34 international & 22 domestic offices & 14 manufacturing facilities, of which 10 are in 🇮🇳 & 4 are overseas. Thermax is present in

over 90 countries.

(2/17)

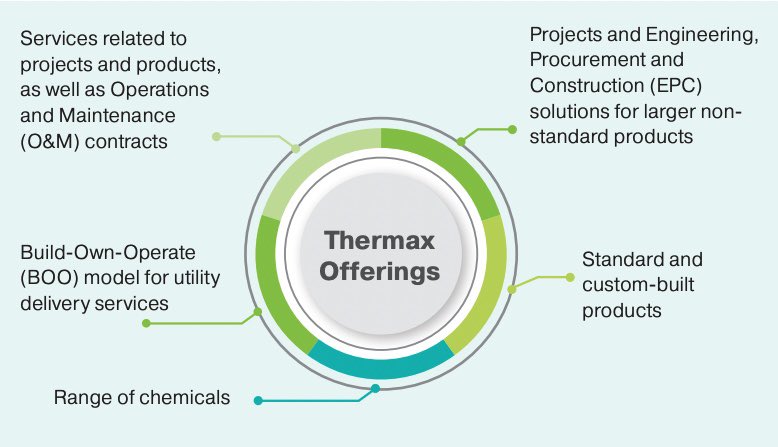

Its business portfolio includes products for heating, cooling, water & waste management & specialty chemicals. It also builds & commissions large boilers for steam & power gen, turnkey power plants, waste heat recovery systems & air pollution control projects.

Its business portfolio includes products for heating, cooling, water & waste management & specialty chemicals. It also builds & commissions large boilers for steam & power gen, turnkey power plants, waste heat recovery systems & air pollution control projects.

(3/17)

Why in focus?

Thermax has benefitted from clients’ increasing focus on energy efficiency and carbon footprint reduction. It is investing in green tech and expanding its product portfolio. The shift towards renewables is ideally suited for the company’s product offerings.

Why in focus?

Thermax has benefitted from clients’ increasing focus on energy efficiency and carbon footprint reduction. It is investing in green tech and expanding its product portfolio. The shift towards renewables is ideally suited for the company’s product offerings.

(4/17)

Top sectors contributing to Thermaxs’ order book:

• Power

• Transportation

• Refinery

• Petrochemical

• Metal

• Steel

• Chemical

• Cement

Top sectors contributing to Thermaxs’ order book:

• Power

• Transportation

• Refinery

• Petrochemical

• Metal

• Steel

• Chemical

• Cement

(5/17)

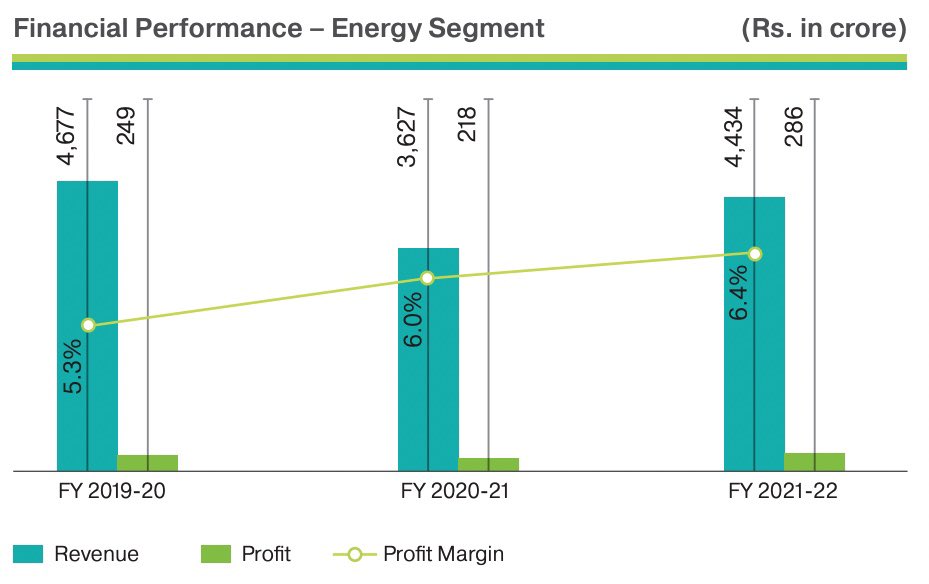

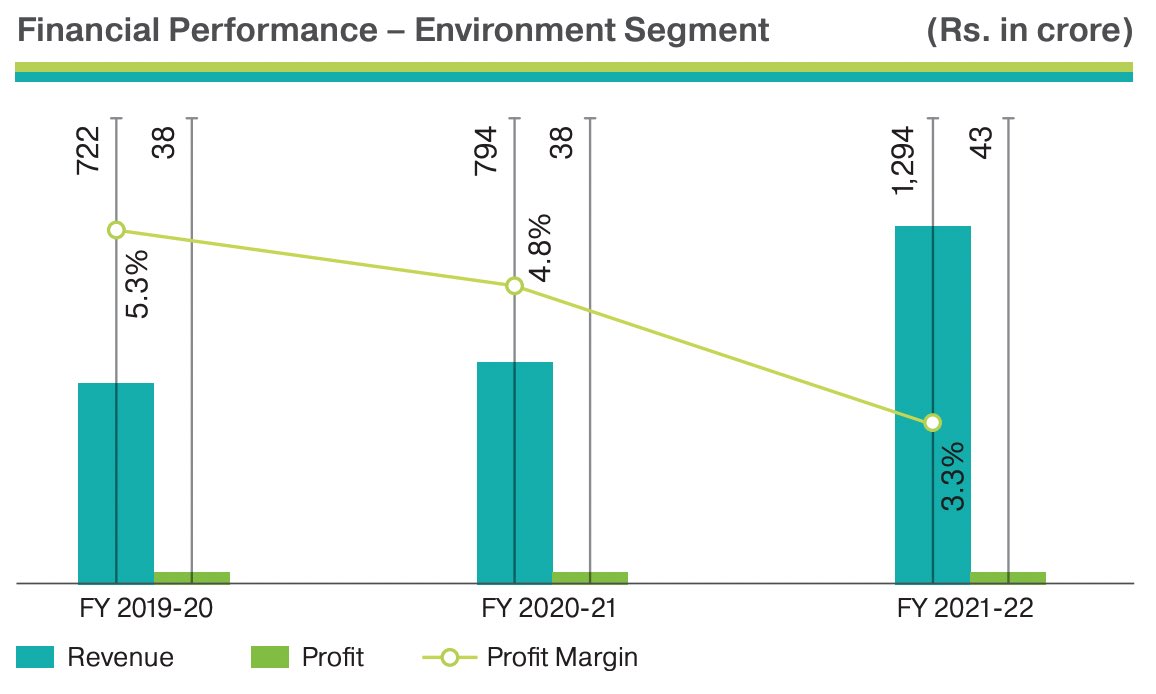

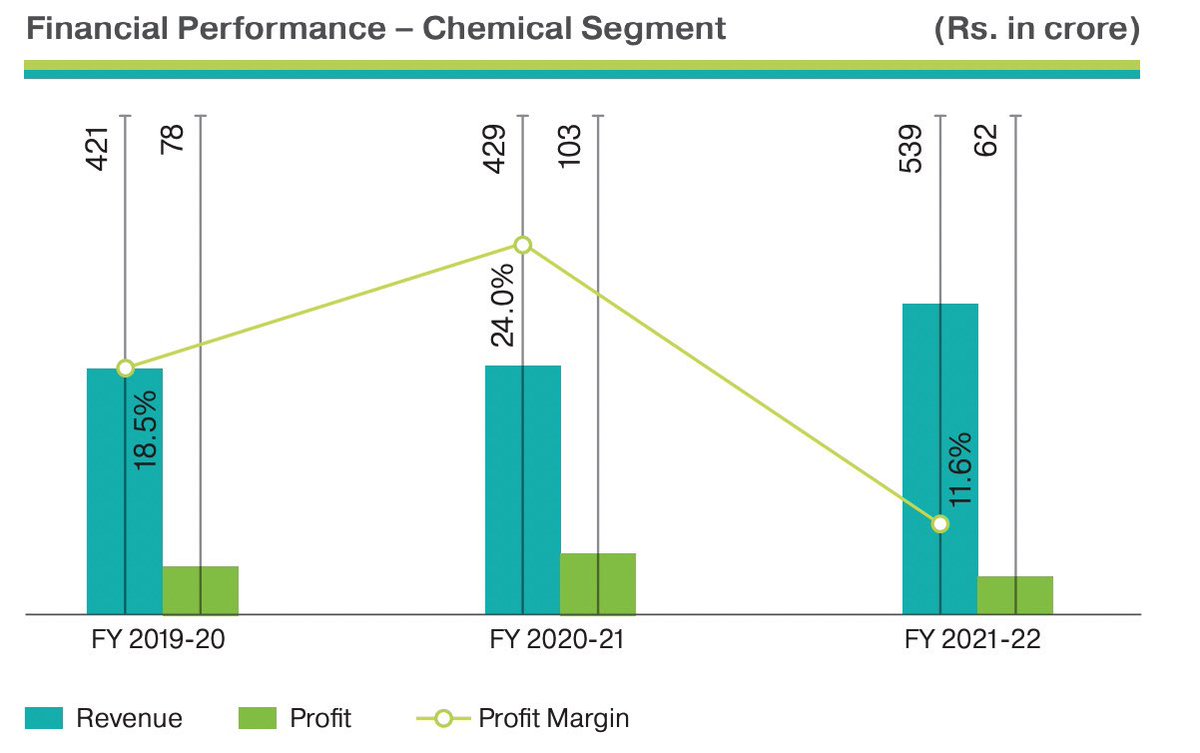

It’s key business segment and their respective growth drivers:

• Energy (71% of Revenue)

• Environment (21% of Revenue)

• Chemical (9% of Revenue)

It’s key business segment and their respective growth drivers:

• Energy (71% of Revenue)

• Environment (21% of Revenue)

• Chemical (9% of Revenue)

(6/17)

• Energy Segment - Drivers

Energy transition & climate change are major priorities of govt globally

Gradual shift from capex to opex based models

In FY22-23, as a part of govt borrowing, sovereign green bonds are to be launched in order to fund green infrastructure

• Energy Segment - Drivers

Energy transition & climate change are major priorities of govt globally

Gradual shift from capex to opex based models

In FY22-23, as a part of govt borrowing, sovereign green bonds are to be launched in order to fund green infrastructure

(7/17)

Environment Segment - Drivers

• Lack of access to water

• Stringent regulatory norms for water and effluent treatment

• Market demand for modularised/ plug-and-play water and wastewater treatment products

• Shift from coal to biomass or agro-based fuels

Environment Segment - Drivers

• Lack of access to water

• Stringent regulatory norms for water and effluent treatment

• Market demand for modularised/ plug-and-play water and wastewater treatment products

• Shift from coal to biomass or agro-based fuels

(8/17)

Chemical Segment - Drivers

• Investments in the petrochemical sector are leading to opportunities for monoethylene glycol (MEG) and catalyst resins

• Increasing emphasis and govt push towards recycling of water

• Rise in demand for RO, multi effect evaporator (MEE)

Chemical Segment - Drivers

• Investments in the petrochemical sector are leading to opportunities for monoethylene glycol (MEG) and catalyst resins

• Increasing emphasis and govt push towards recycling of water

• Rise in demand for RO, multi effect evaporator (MEE)

(9/17)

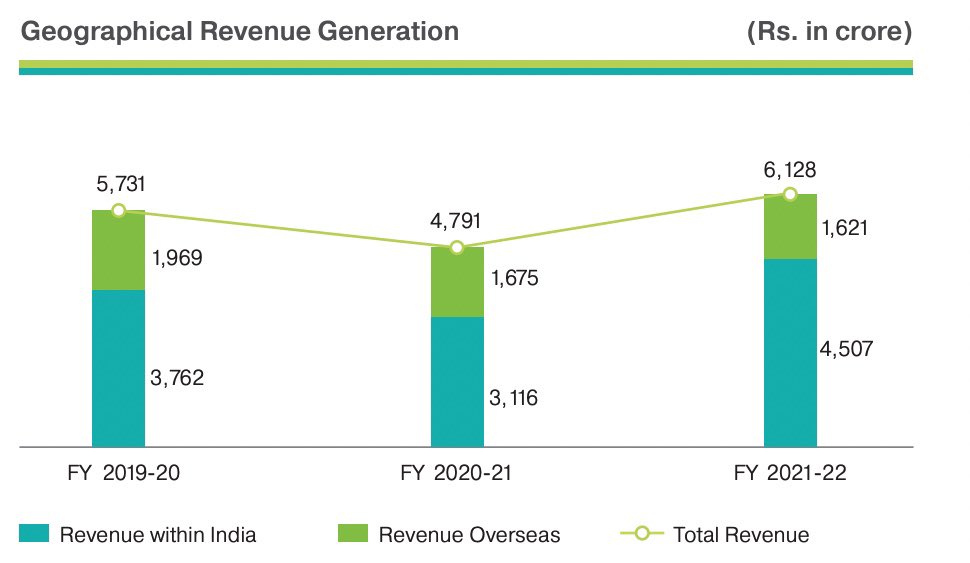

• Focus on Internationalisation:

Currently overseas segment accounts for 20% of overall bookings.

It is establishing itself as a global player in the air pollution control domain.

It’s topline growth in chemical was driven by US, Europe and South East Asian Markets.

• Focus on Internationalisation:

Currently overseas segment accounts for 20% of overall bookings.

It is establishing itself as a global player in the air pollution control domain.

It’s topline growth in chemical was driven by US, Europe and South East Asian Markets.

(10/17)

• Robust financial risk profile:

It has net debt-free balance sheet and large estimated networth of over ₹3,400 cr.

Debt protection metrics are robust on account of limited debt

(₹400 core as on March 31, 2022) and healthy cash accrual.

• Robust financial risk profile:

It has net debt-free balance sheet and large estimated networth of over ₹3,400 cr.

Debt protection metrics are robust on account of limited debt

(₹400 core as on March 31, 2022) and healthy cash accrual.

(11/17)

It is a leading player in several of its product segments, such as vapour absorption chillers, low & medium capacity boilers & electrostatic precipitators

Thermax is also steadily increasing its global footprint with 20% of the revenue coming from the overseas market.

It is a leading player in several of its product segments, such as vapour absorption chillers, low & medium capacity boilers & electrostatic precipitators

Thermax is also steadily increasing its global footprint with 20% of the revenue coming from the overseas market.

(12/17)

Prudent WC management:

NWCC has been 50-70 days, due to prudent collection & inventory mgmt.

Receivables have remained less than 120 days in the past due to careful selection of projects and tight control on collections. This has also led to low dependence on WC debt.

Prudent WC management:

NWCC has been 50-70 days, due to prudent collection & inventory mgmt.

Receivables have remained less than 120 days in the past due to careful selection of projects and tight control on collections. This has also led to low dependence on WC debt.

(13/17)

Weaknesses:

Cyclicality:

A weak demand environment and investment climate has led to a slump in orders in many of the end-user segments as companies have increasingly shelved expansion plans. This led to stagnation in order book in the last two fiscals.

Weaknesses:

Cyclicality:

A weak demand environment and investment climate has led to a slump in orders in many of the end-user segments as companies have increasingly shelved expansion plans. This led to stagnation in order book in the last two fiscals.

(14/17)

Modest profitability:

The company faces intense competition in business segments such as low-capacity boilers and packaged-water treatment plants. Hence, operating margin has largely remained 7-9% in the past. Margin is also vulnerable to

fluctuations in input prices.

Modest profitability:

The company faces intense competition in business segments such as low-capacity boilers and packaged-water treatment plants. Hence, operating margin has largely remained 7-9% in the past. Margin is also vulnerable to

fluctuations in input prices.

(15/17)

Performance FY22 vs FY21

• Revenue: ₹6,128cr vs ₹4,719cr

• Consolidated Order booking :

₹9,410cr vs ₹4,784cr

• International Orders : ₹1,878cr vs ₹1,318 cr

Performance FY22 vs FY21

• Revenue: ₹6,128cr vs ₹4,719cr

• Consolidated Order booking :

₹9,410cr vs ₹4,784cr

• International Orders : ₹1,878cr vs ₹1,318 cr

(16/17)

Key Ratios on YOY basis

• Debtors turnover: 3.88 vs 3.49

• Inventory turnover: 7.80 vs 6.87

• Interest Coverage: 21.26 vs 34.37

• Current Ratio: 1.17 vs 1.51

• RoCE: 9.4% vs 10.20%

• RoNW: 6.7% vs 4.90%

Key Ratios on YOY basis

• Debtors turnover: 3.88 vs 3.49

• Inventory turnover: 7.80 vs 6.87

• Interest Coverage: 21.26 vs 34.37

• Current Ratio: 1.17 vs 1.51

• RoCE: 9.4% vs 10.20%

• RoNW: 6.7% vs 4.90%

(17/17)

Will the global recession woes affect Thermax’s growth prospects?

@caniravkaria @kuttrapali26 @Anshi_________ @PAlearner

Will the global recession woes affect Thermax’s growth prospects?

@caniravkaria @kuttrapali26 @Anshi_________ @PAlearner

Loading suggestions...