Microsoft reported their full year 2022 numbers last week.

Time to have a brief refresher!

A Thread: 👇

Time to have a brief refresher!

A Thread: 👇

If you are new to Microsoft, just know that this is a company with a wide moat.

It's well diversified and operates in 3 segments:

1. (32%) Productivity & Business Processes

2. (38%) Intelligent Cloud

3. (30%) More Personal Computing

Some of their iconic products are below 👇

It's well diversified and operates in 3 segments:

1. (32%) Productivity & Business Processes

2. (38%) Intelligent Cloud

3. (30%) More Personal Computing

Some of their iconic products are below 👇

Microsoft is also a proud member of a very exclusive club of Trillion dollar companies because it currently has a market cap of 2.04 Trillion.

This isn't much different compared to last year, because the $MSFT share price has been flat since then.

This isn't much different compared to last year, because the $MSFT share price has been flat since then.

But as we know, a stock is not the same as the business side of things.

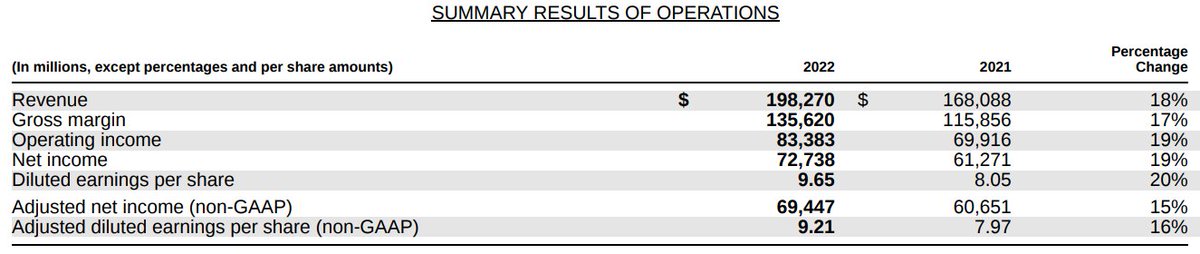

So here's the good news, $MSFT has been firing on all cylinders!

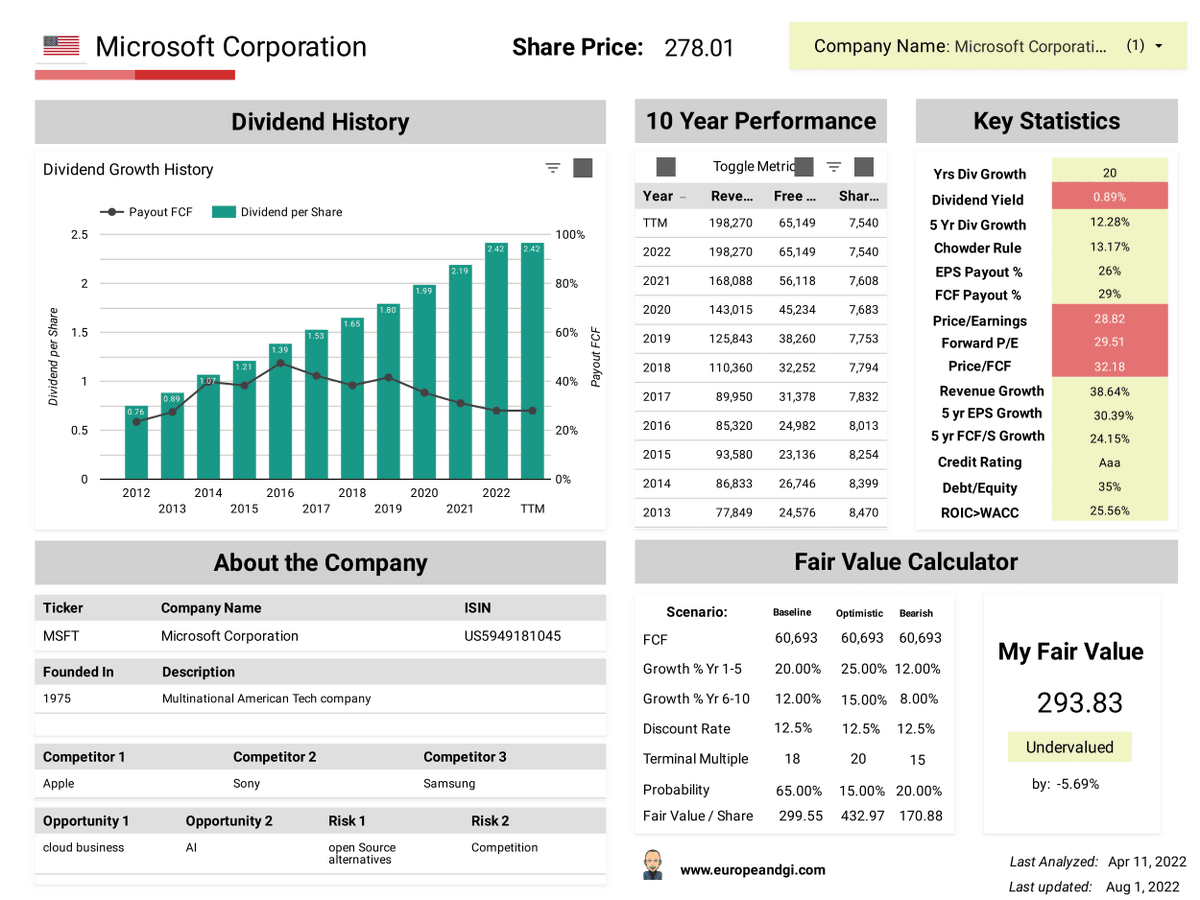

Their sales grew by a whopping 18% to 198 Bln and their Earnings per Share to 9.21 by 16% 💪

So here's the good news, $MSFT has been firing on all cylinders!

Their sales grew by a whopping 18% to 198 Bln and their Earnings per Share to 9.21 by 16% 💪

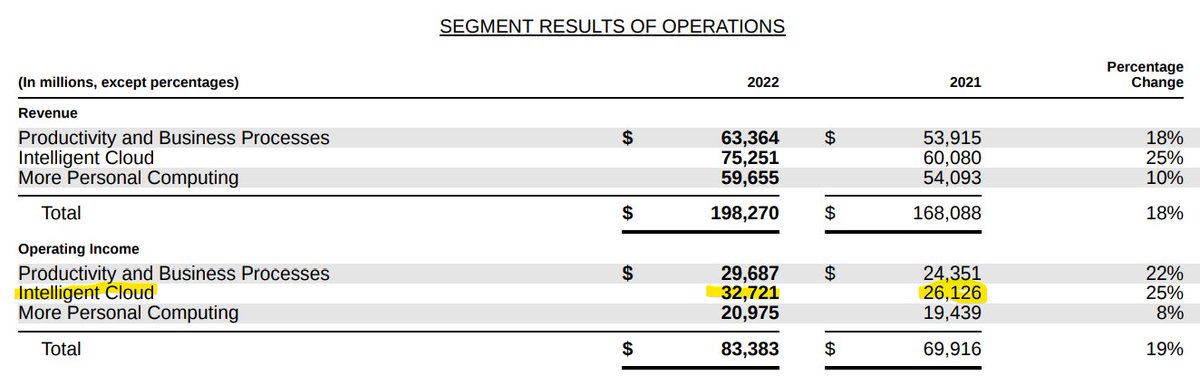

The most impressive to me continues to be the intelligent cloud. It grew by another 25% and it's really leading the pack right now.

The main growth driver is Azure and other cloud services which grew by 45% 🚀

In 2017 this was still the smallest segment with 27.4 Bln

The main growth driver is Azure and other cloud services which grew by 45% 🚀

In 2017 this was still the smallest segment with 27.4 Bln

So let's look a bit more into their financial performance.

Balance Sheet:

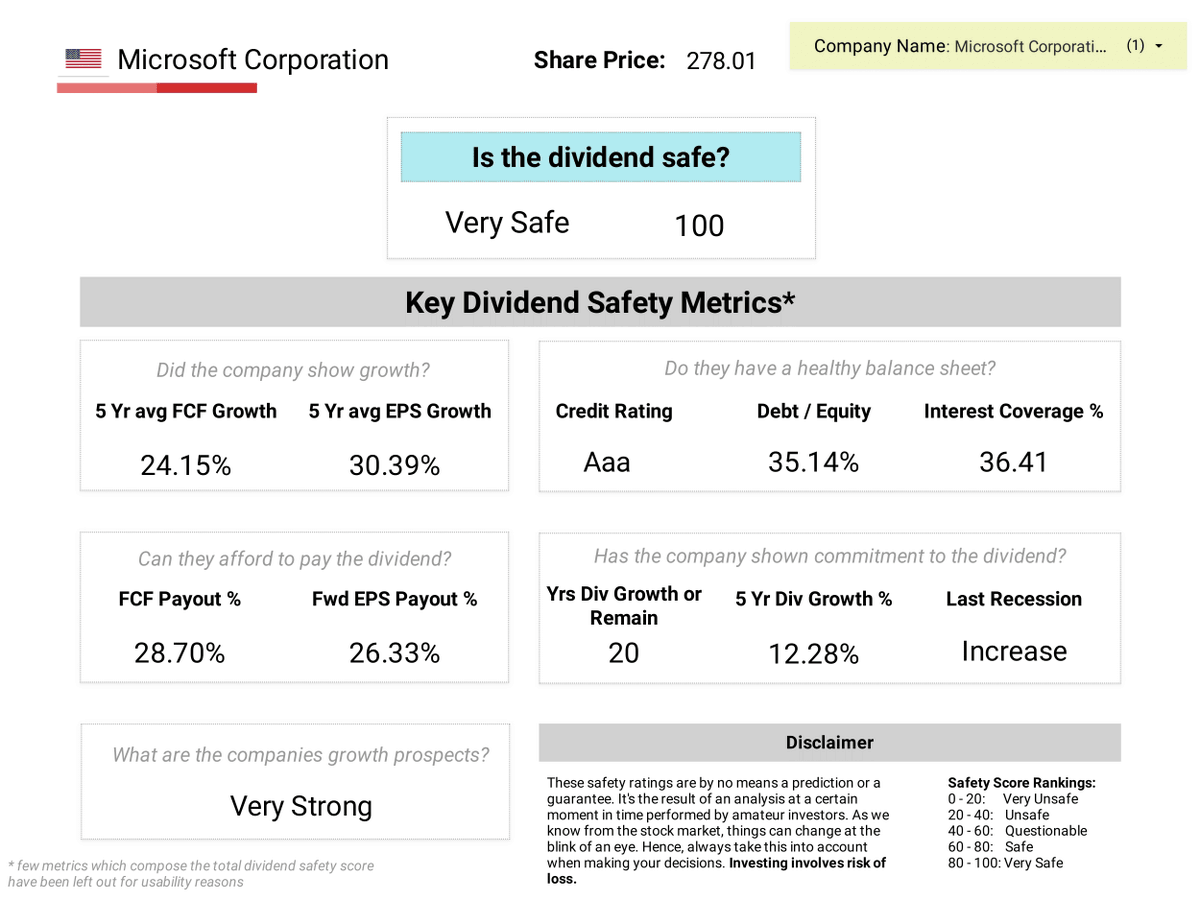

$MSFT has an AAA credit rating and it's one of the strongest balance sheets in the world.

Their Long-Term debt is 47 Bln and they could pay it off entirely by their 104 Bln cash position.

Balance Sheet:

$MSFT has an AAA credit rating and it's one of the strongest balance sheets in the world.

Their Long-Term debt is 47 Bln and they could pay it off entirely by their 104 Bln cash position.

Hence, a 28% debt/equity ratio should come as no surprise!

In fact, there are only 2 other companies with an AAA balance sheet:

📱 Apple

💊 Johnson & Johnson

I would dare to say that $MSFT is still outshining them and for that reason, it deserves an AAAA rating

In fact, there are only 2 other companies with an AAA balance sheet:

📱 Apple

💊 Johnson & Johnson

I would dare to say that $MSFT is still outshining them and for that reason, it deserves an AAAA rating

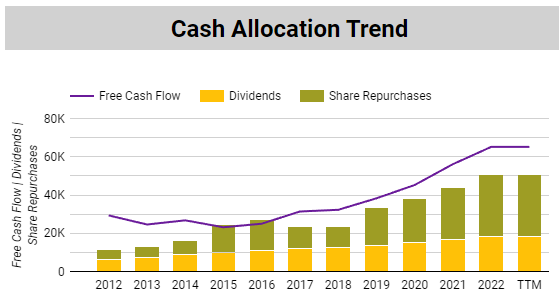

Cash Flow:

$MSFT set again a new record💪:

+ 89 Bln in Cash from Operations (76.7 Bln)

- 23.9 Bln in CAPEX (20.6 Bln)

= 65.1 Bln in FCF

CAPEX / FCF = 36,7%. -> this is in line with the last years and it means that they are heavily investing to remain competitive.

(= last year)

$MSFT set again a new record💪:

+ 89 Bln in Cash from Operations (76.7 Bln)

- 23.9 Bln in CAPEX (20.6 Bln)

= 65.1 Bln in FCF

CAPEX / FCF = 36,7%. -> this is in line with the last years and it means that they are heavily investing to remain competitive.

(= last year)

So what did it do with the Free Cash Flow?

👉 It paid out 18.1 Bln in dividends

👉 It repurchased 32.7 Bln of shares

This means that it didn't spend all its free cash flow to reward shareholders.

However, it did finalize the Nuance acquisition for 18.8 Bln.

👉 It paid out 18.1 Bln in dividends

👉 It repurchased 32.7 Bln of shares

This means that it didn't spend all its free cash flow to reward shareholders.

However, it did finalize the Nuance acquisition for 18.8 Bln.

Ah, and I almost forgot to mention that they bought Activision Blizzard for 68.7 Bln.

This deal should be paid for next year and as you can see, they can almost entirely pay it from their Free Cash Flow in a single year!

That's what balance sheet optionality really is about!

This deal should be paid for next year and as you can see, they can almost entirely pay it from their Free Cash Flow in a single year!

That's what balance sheet optionality really is about!

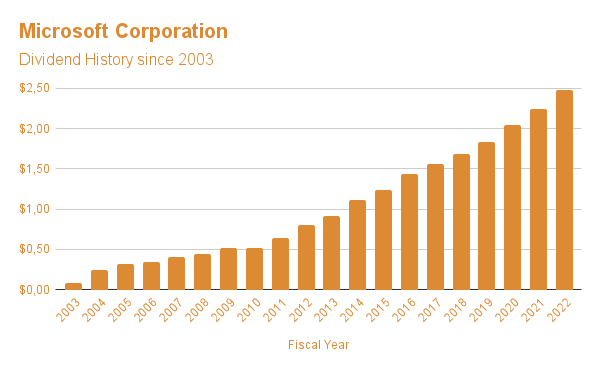

So let's talk dividends right now.

Who says a growth stock can't be a dividend stock?

I truly believe that dividends and growth can go hand-in-hand and Microsoft is a good example of that.

The company started paying a dividend in 2003 and it has grown ever since

Who says a growth stock can't be a dividend stock?

I truly believe that dividends and growth can go hand-in-hand and Microsoft is a good example of that.

The company started paying a dividend in 2003 and it has grown ever since

This leads to amazing dividend statistics:

👉 20 years of growth

👉 5-year CAGR of 12,28%

👉 29% FCF payout

BUT:

0,89% yield 😟

Good news: we should learn about their next dividend hike in a few weeks from now 💪

In my opinion, this is a dividend King in the making.

👉 20 years of growth

👉 5-year CAGR of 12,28%

👉 29% FCF payout

BUT:

0,89% yield 😟

Good news: we should learn about their next dividend hike in a few weeks from now 💪

In my opinion, this is a dividend King in the making.

But yeah, what about the low yield then?

It's true that a dividend yield below 1% isn't attractive to me. It would simply take too many years for it to become meaningful.

However, sometimes there's a case for it, especially if you have many high-yielders in your portfolio.

It's true that a dividend yield below 1% isn't attractive to me. It would simply take too many years for it to become meaningful.

However, sometimes there's a case for it, especially if you have many high-yielders in your portfolio.

Look, I bought $MSFT somewhere in the low 40's and later averaged up in the 80s.

My main thesis for buying was the cloud as a secular growth trend and I knew that Satya Nadella came from that unit.

So couple that with an attractive valuation and the case was made.

My main thesis for buying was the cloud as a secular growth trend and I knew that Satya Nadella came from that unit.

So couple that with an attractive valuation and the case was made.

But it wasn't easy as the future was very uncertain!

Many tell me that it was a golden opportunity and that they are waiting for something similar.

But hindsight is 20/20, because, at the time, many people thought $MSFT was dead.

Tbh, it felt a little bit like $INTC right now.

Many tell me that it was a golden opportunity and that they are waiting for something similar.

But hindsight is 20/20, because, at the time, many people thought $MSFT was dead.

Tbh, it felt a little bit like $INTC right now.

Hence, it is probably easier to buy $MSFT at the current price, because we know it's driven by success.

But what if there is a sudden headwind and the price drops by 50%.

Would you buy aggressively then?

This is why investing is so difficult.

You CAN"T borrow conviction!

But what if there is a sudden headwind and the price drops by 50%.

Would you buy aggressively then?

This is why investing is so difficult.

You CAN"T borrow conviction!

But what you can do is study their business and the fundamentals of the company.

After that, write down your "one-liner" of why you would want to own their stock. This is your thesis!

Try then to estimate what you think the company is worth and give it a 20% margin of safety.

After that, write down your "one-liner" of why you would want to own their stock. This is your thesis!

Try then to estimate what you think the company is worth and give it a 20% margin of safety.

As an example,

"I believe that $MSFT is uniquely positioned to support the DIGITALIZATION OF EVERYTHING.

This applies as well to businesses as to direct consumers.

I believe that the secular growth trend is just half underway and that we still have at least a decade to go."

"I believe that $MSFT is uniquely positioned to support the DIGITALIZATION OF EVERYTHING.

This applies as well to businesses as to direct consumers.

I believe that the secular growth trend is just half underway and that we still have at least a decade to go."

Based on this, I've made my fair value estimate for Microsoft.

My assumptions are the following:

👉 a 60 Bln FCF baseline (now 65 Bln)

👉 20% growth in the first 5 years

👉 12% in the next 5 years

👉 12.5% discount rate

👉 Terminal Multiple of 18

This is aggressive though!

My assumptions are the following:

👉 a 60 Bln FCF baseline (now 65 Bln)

👉 20% growth in the first 5 years

👉 12% in the next 5 years

👉 12.5% discount rate

👉 Terminal Multiple of 18

This is aggressive though!

As you can see, the Fair Value price is ~295 USD

I might be wrong of course, that's why we take another 20% margin of safety. This would give it a BUY price of 236 USD.

Please note that I'm also taking a 12.5% discount rate instead of a 10%

This all makes it more conservative.

I might be wrong of course, that's why we take another 20% margin of safety. This would give it a BUY price of 236 USD.

Please note that I'm also taking a 12.5% discount rate instead of a 10%

This all makes it more conservative.

As you can see, estimating the fair value of a business is to some extent a form of art.

The moment it's just becoming a formula to you probably means that you should spend more time on studying the business.

Every assumption matters!

The moment it's just becoming a formula to you probably means that you should spend more time on studying the business.

Every assumption matters!

That's what you really should know and you shouldn't simply copy what financial influencers say or do. Neither from me!

As an example, I love my audience, because they often challenge me on my assumptions

And that's what's making me stronger as an investor as well 🙏

Ref: $TXN

As an example, I love my audience, because they often challenge me on my assumptions

And that's what's making me stronger as an investor as well 🙏

Ref: $TXN

Last but not least, every company comes with risks, also $MSFT!

Hence, I foresee the following 3 main risks for them:

👉 Cyberattacks having adverse effects on trust

👉 A recession could lower consumer spending on their products

👉 Losing market share (i.e. gSuite vs Office)

Hence, I foresee the following 3 main risks for them:

👉 Cyberattacks having adverse effects on trust

👉 A recession could lower consumer spending on their products

👉 Losing market share (i.e. gSuite vs Office)

So to sum it up.

I'm very bullish on the future for Microsoft. It's been a great turnaround story and Satya Nadella deserves a statue.

It's currently my 2nd largest portfolio position with 7% in size.

I would probably further nibble in below 236 USD.

I'm very bullish on the future for Microsoft. It's been a great turnaround story and Satya Nadella deserves a statue.

It's currently my 2nd largest portfolio position with 7% in size.

I would probably further nibble in below 236 USD.

That's it from my side!

If you enjoyed this thread:

1. Follow me @European_DGI for more of these

2. RT the tweet below to share this thread with your audience

Last but not least, consider buying me a coffee in case you would like to support me further: buymeacoffee.com

If you enjoyed this thread:

1. Follow me @European_DGI for more of these

2. RT the tweet below to share this thread with your audience

Last but not least, consider buying me a coffee in case you would like to support me further: buymeacoffee.com

Loading suggestions...