Benjamin Graham is outdated!

That's what many growth investors think.

I disagree.

Spent the last 3 months slowly reading through Security Analysis by Graham and Dodd.

It's a gem.

Here's 18 powerful lessons I took home that can be applied to modern day investing:

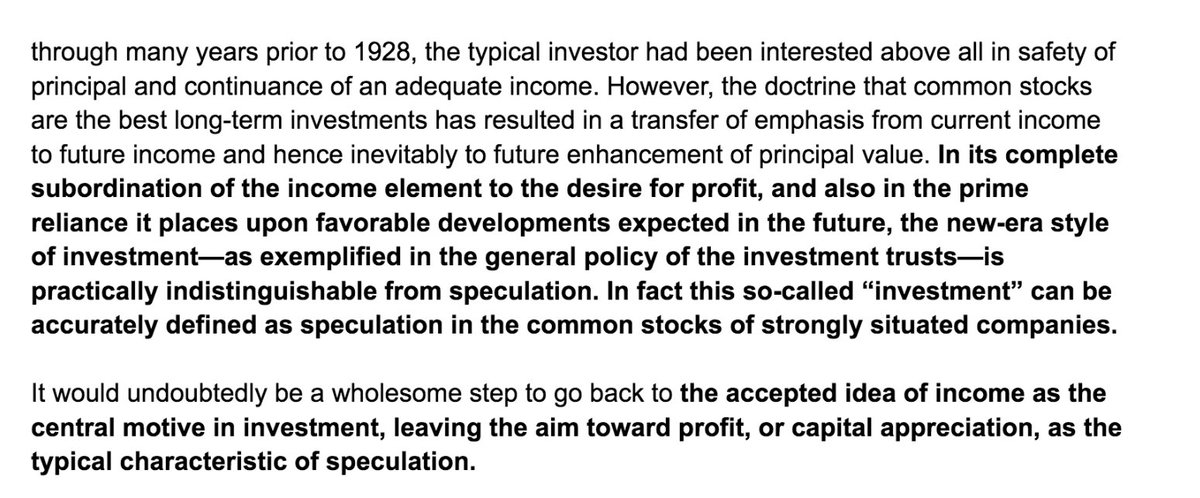

That's what many growth investors think.

I disagree.

Spent the last 3 months slowly reading through Security Analysis by Graham and Dodd.

It's a gem.

Here's 18 powerful lessons I took home that can be applied to modern day investing:

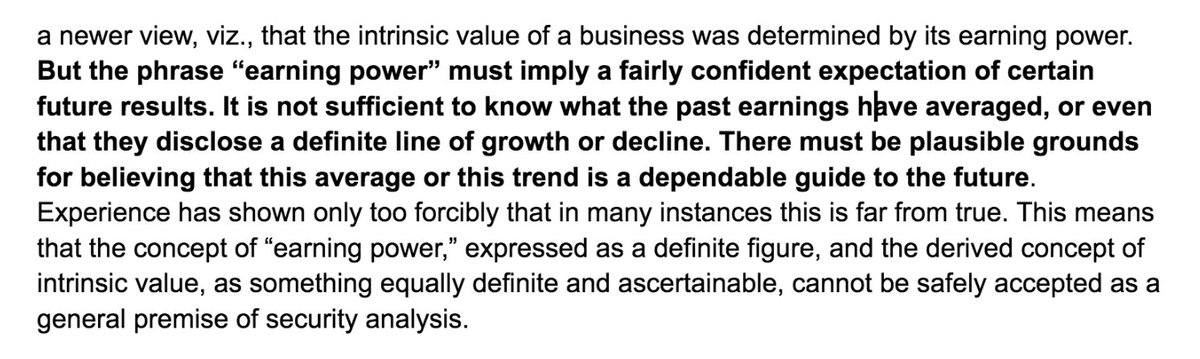

1. Intrinsic value is not a fixed number.

Don't get tied down by a number you see on a spreadsheet.

It's usually a range and defined by assumptions, which are fluid and subject to change.

Don't get tied down by a number you see on a spreadsheet.

It's usually a range and defined by assumptions, which are fluid and subject to change.

2. For valuation and proper value to be determined, there must be stability in earnings.

Not just in the numbers of the past...

But also in the business model and how it will perform in future.

This makes high growth disruptive companies hard to value and do DCFs on.

Not just in the numbers of the past...

But also in the business model and how it will perform in future.

This makes high growth disruptive companies hard to value and do DCFs on.

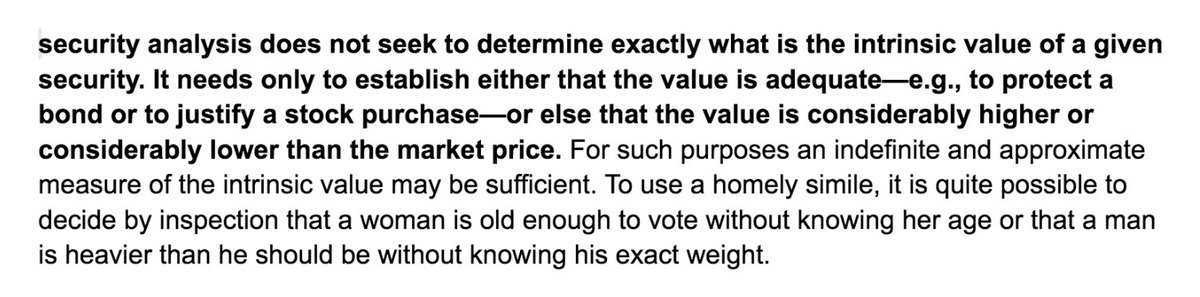

3. How then do you use security analysis on high growth companies?

Good news! you don't need to find an exact value for the stock.

As long as the conservative assumptions made give you a number that is way below the market price...

That is still a smart investment.

Good news! you don't need to find an exact value for the stock.

As long as the conservative assumptions made give you a number that is way below the market price...

That is still a smart investment.

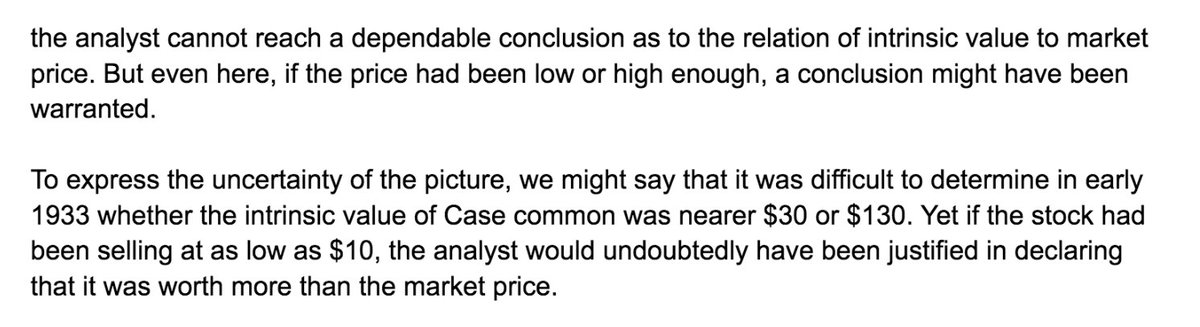

4. Once again, you don't need to know the specific value.

You just need to know that it's a good deal at the current price that Mr Market is serving up to you!

Like Buffett says...

"the best investment ideas should hit you over the head with a baseball bat"

You just need to know that it's a good deal at the current price that Mr Market is serving up to you!

Like Buffett says...

"the best investment ideas should hit you over the head with a baseball bat"

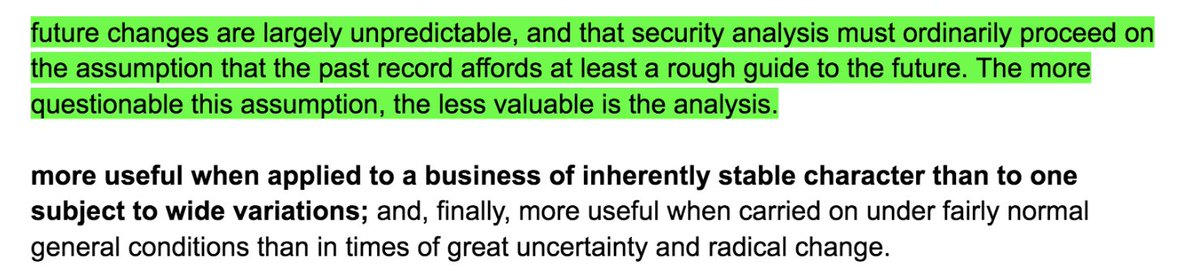

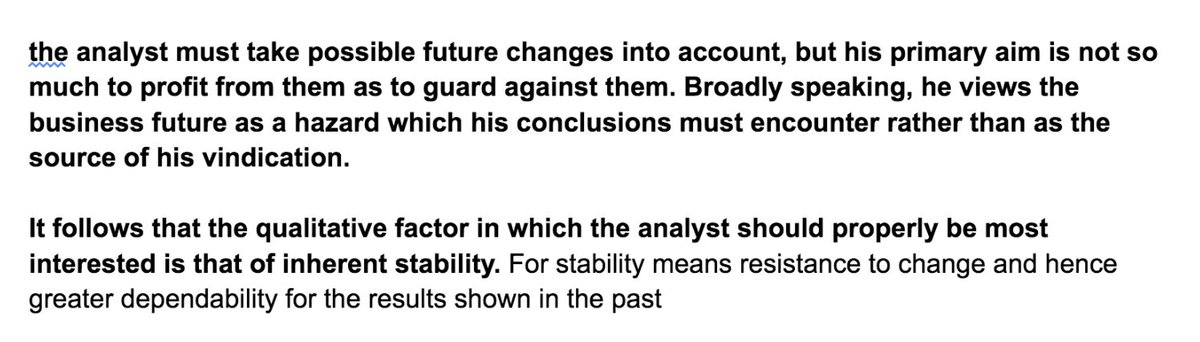

5. The past is ONLY equal to the future when the company has a stable character

The less stable the business model...

The less valuable any DCFs would be.

This doesn't mean you should ignore valuation.

It just means you should be careful about the assumptions you input.

The less stable the business model...

The less valuable any DCFs would be.

This doesn't mean you should ignore valuation.

It just means you should be careful about the assumptions you input.

6. Be careful of stocks that are less recognized by the market

There are always gems in undervalued securities.

But the market may take a longer time to realize the value given the information obscurity.

I believe this is less of a issue in today's internet age.

There are always gems in undervalued securities.

But the market may take a longer time to realize the value given the information obscurity.

I believe this is less of a issue in today's internet age.

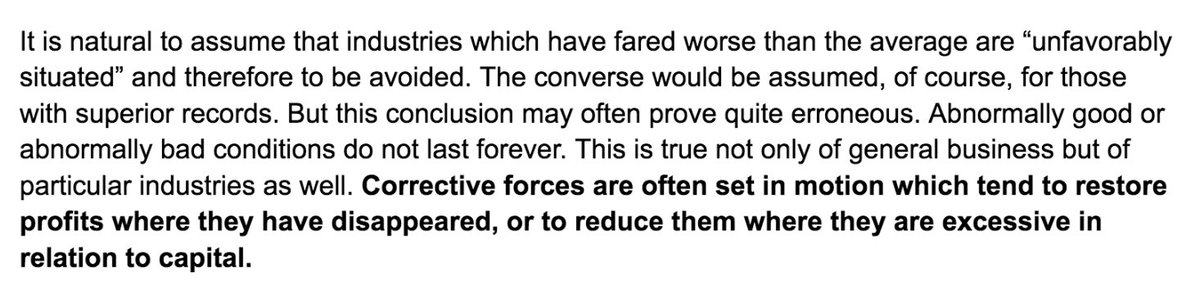

7. Mean reversion happens to most companies

Not all. There are exceptions and anomalies for sure.

But most companies revert to the mean.

Also a good reminder NOT to buy a stock just because of the industry.

Reminds me of Buffett's lessons on shooting down the wright brothers.

Not all. There are exceptions and anomalies for sure.

But most companies revert to the mean.

Also a good reminder NOT to buy a stock just because of the industry.

Reminds me of Buffett's lessons on shooting down the wright brothers.

8. Investor vs Analyst

The investor makes decisions based on the facts and value of the asset.

The speculator makes decisios based on future expectations and other participants' behaviours.

Similar to the keynesian beauty contest analogy we read about in most investing books.

The investor makes decisions based on the facts and value of the asset.

The speculator makes decisios based on future expectations and other participants' behaviours.

Similar to the keynesian beauty contest analogy we read about in most investing books.

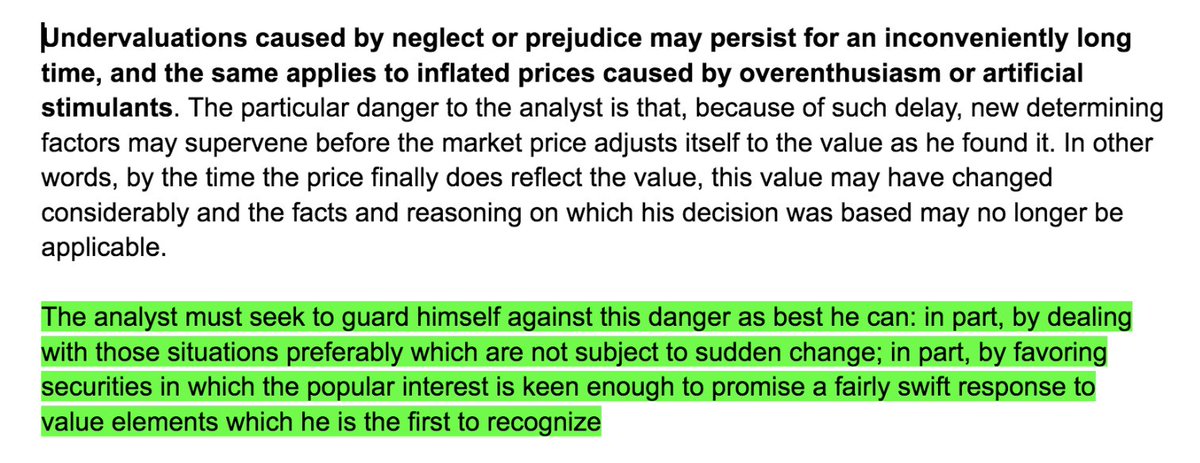

9. Change is something you factor in NOT to profit from, but to guard against.

This is where the line between value and growth is drawn in the sand.

But there is wisdom in this statement.

One should buy a stock that would still do well even if the assumed changes don't happen.

This is where the line between value and growth is drawn in the sand.

But there is wisdom in this statement.

One should buy a stock that would still do well even if the assumed changes don't happen.

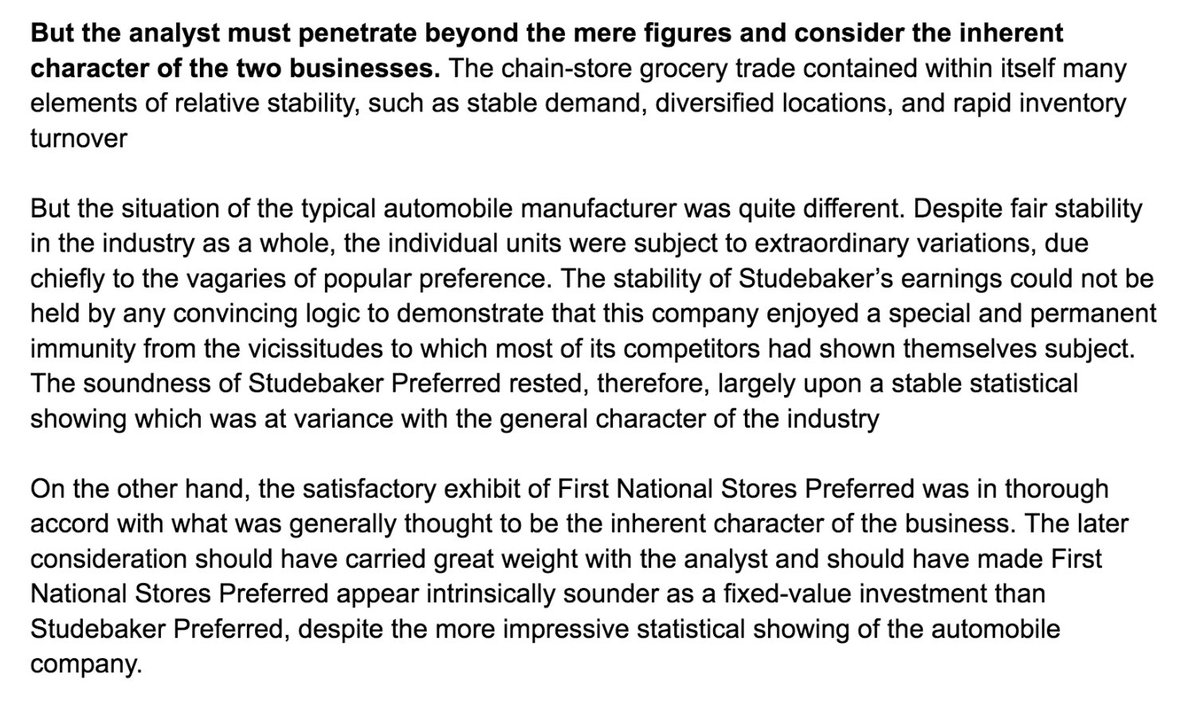

10. Look for business stability not just in numbers, but also in the business quality and traits

Don't fall into the trap of stability just by zooming into trends that seem consistent.

instead ask yourself:

"will the nature of the customers needs and wants change drastically?"

Don't fall into the trap of stability just by zooming into trends that seem consistent.

instead ask yourself:

"will the nature of the customers needs and wants change drastically?"

11. Focus on what the asset can generate, not how much it can be sold for in future

In this example, Graham was referring to dividends and income.

But the essence is the same.

When you look at an asset for what it can generate for you, you start thinking like an owner

In this example, Graham was referring to dividends and income.

But the essence is the same.

When you look at an asset for what it can generate for you, you start thinking like an owner

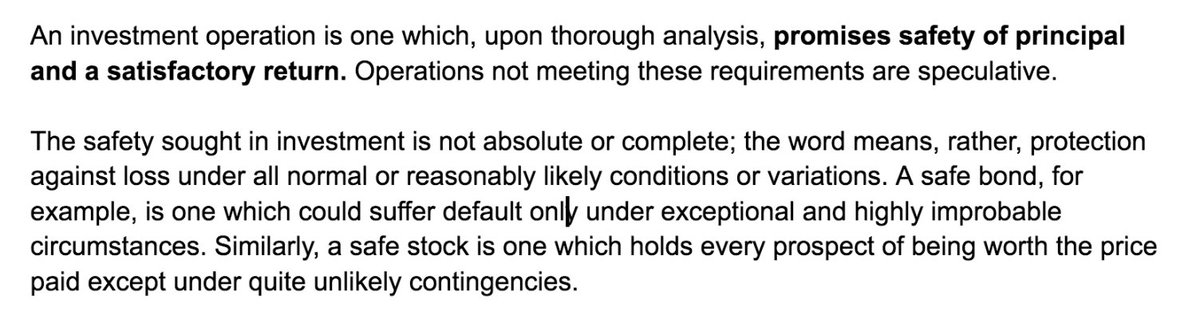

12. Definition of what it means to be a good investor.

a. Safety of principal

b. Satisfactory return

The nature of the asset you invest in doesn't make it safer than others i.e. bonds vs stocks.

It's always about price you pay.

a. Safety of principal

b. Satisfactory return

The nature of the asset you invest in doesn't make it safer than others i.e. bonds vs stocks.

It's always about price you pay.

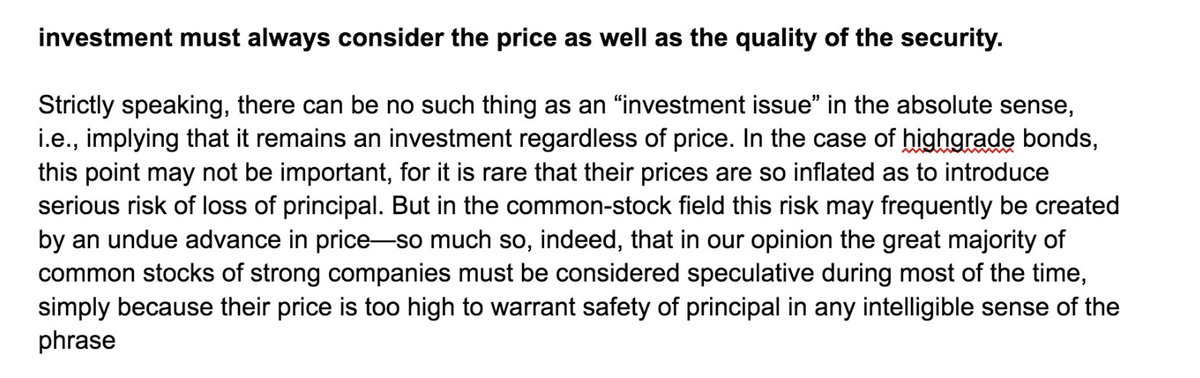

13. Price is your due diligence

It's not just about buying good things.

It's about buying things well.

It's not just about buying good things.

It's about buying things well.

14. Even good stocks can be silly investments if you pay too high a price for it

Once again shows you the wisdom of Graham and Dodd.

I's NEVER just a binary decision of quality vs numbers.

You must always consider both in your investment decision.

Once again shows you the wisdom of Graham and Dodd.

I's NEVER just a binary decision of quality vs numbers.

You must always consider both in your investment decision.

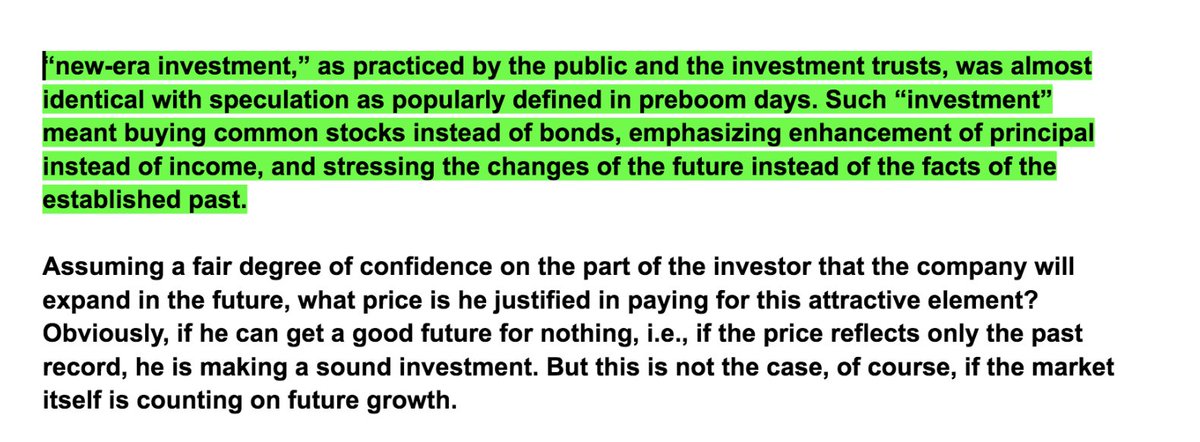

15. Know that when you pay a high price for a business, you are paying for future growth.

Nothing wrong with that if you are willing to hold long.

But you have the be aware what you are paying for.

Good investing should be viewed as buying a private business in the real world.

Nothing wrong with that if you are willing to hold long.

But you have the be aware what you are paying for.

Good investing should be viewed as buying a private business in the real world.

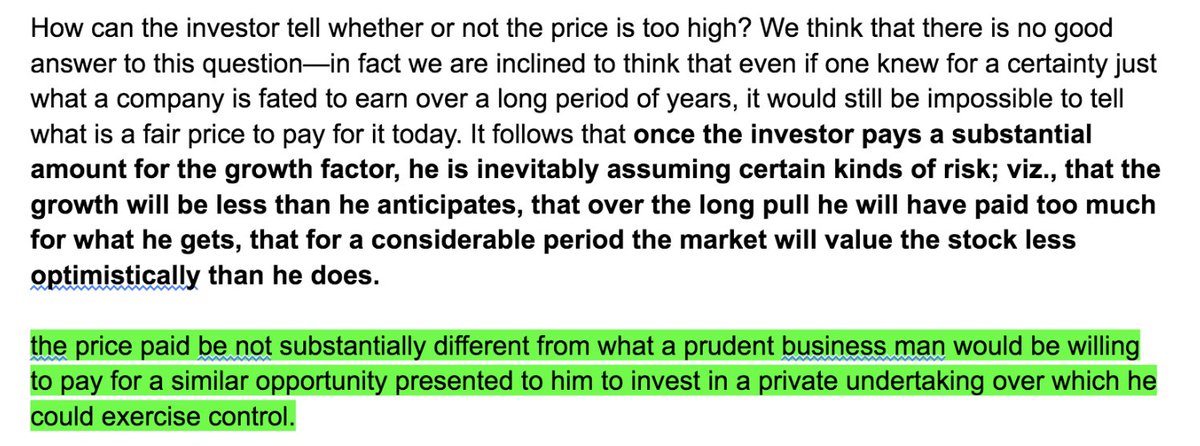

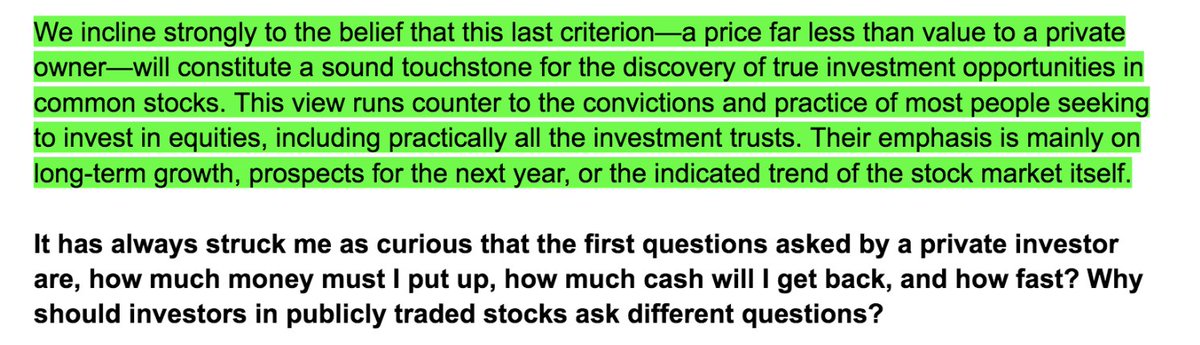

16. Questions to help you think like a private business buyer:

How much money must I put up?

How much cash will I get back, and how fast?

Graham then asks...

"Why should investors in publicly traded stocks ask different questions?"

Good to chew on this.

How much money must I put up?

How much cash will I get back, and how fast?

Graham then asks...

"Why should investors in publicly traded stocks ask different questions?"

Good to chew on this.

17. You have to make a judgment call in your valuations

This, to me, is what makes Graham a fucking wise guy.

All the criticisms about Graham being old school is untrue.

He mentioned - you have to also consider recent changes in the business.

And decide which to prioritize.

This, to me, is what makes Graham a fucking wise guy.

All the criticisms about Graham being old school is untrue.

He mentioned - you have to also consider recent changes in the business.

And decide which to prioritize.

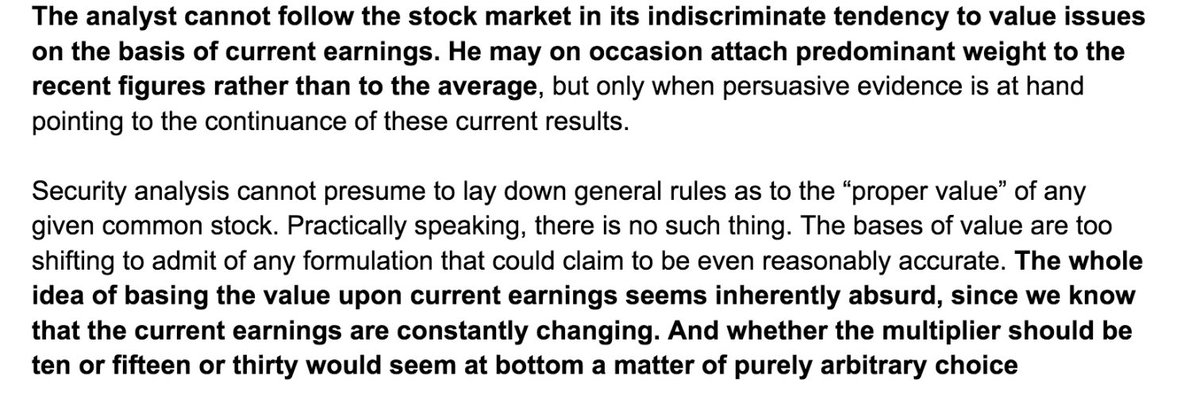

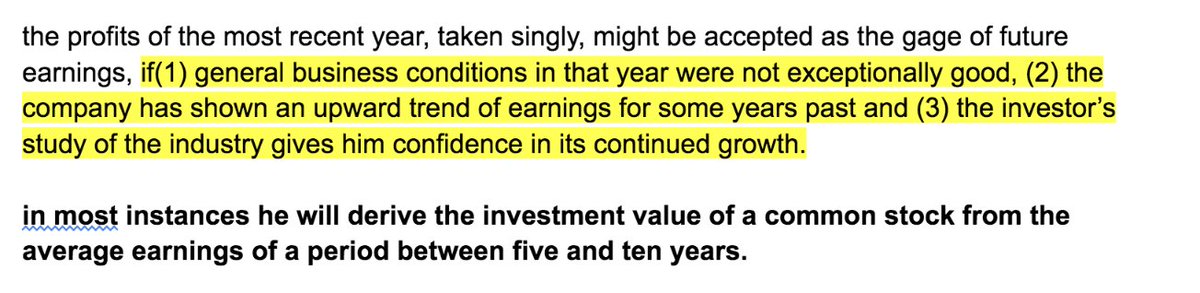

18. It's always about the history of the company, never the latest earnings results

This too, is why Graham is amazing.

A company is not expensive just because its recent earnings fall off a cliff and the PE shoots up.

Look further back before you conclude.

This too, is why Graham is amazing.

A company is not expensive just because its recent earnings fall off a cliff and the PE shoots up.

Look further back before you conclude.

Fun fact: I didn't finish the book.

Correction: I couldn't finish the book.

It's not an easy read.

I made it only halfway through. But still drew out pages of nuggets from that.

Maybe I'll try again in future.

I hope this is helpful to you!

Correction: I couldn't finish the book.

It's not an easy read.

I made it only halfway through. But still drew out pages of nuggets from that.

Maybe I'll try again in future.

I hope this is helpful to you!

Loading suggestions...