Housing

Economics

Finance

Financial Markets

Monetary Policy

Federal Reserve

Equities

Fixed Income

Macro Overview

Macro Overview from a former senior trader at the Federal Reserve.

We studied Joseph Wang (@fedguy12) to learn what may be next for financial markets and monetary policy.

An inside look into the Fed and what the market may be misunderstanding 🧵👇

We studied Joseph Wang (@fedguy12) to learn what may be next for financial markets and monetary policy.

An inside look into the Fed and what the market may be misunderstanding 🧵👇

(2/41) This thread summarizes a recent interview with @FedGuy12 and @MoneyMorningAU.

It also features insights from Wang's recent blog posts.

This thread covers:

- Fed Pivot

- QE and Yield Curve Control

- What's next for equities, housing, fixed income and more.

Let's dive in!

It also features insights from Wang's recent blog posts.

This thread covers:

- Fed Pivot

- QE and Yield Curve Control

- What's next for equities, housing, fixed income and more.

Let's dive in!

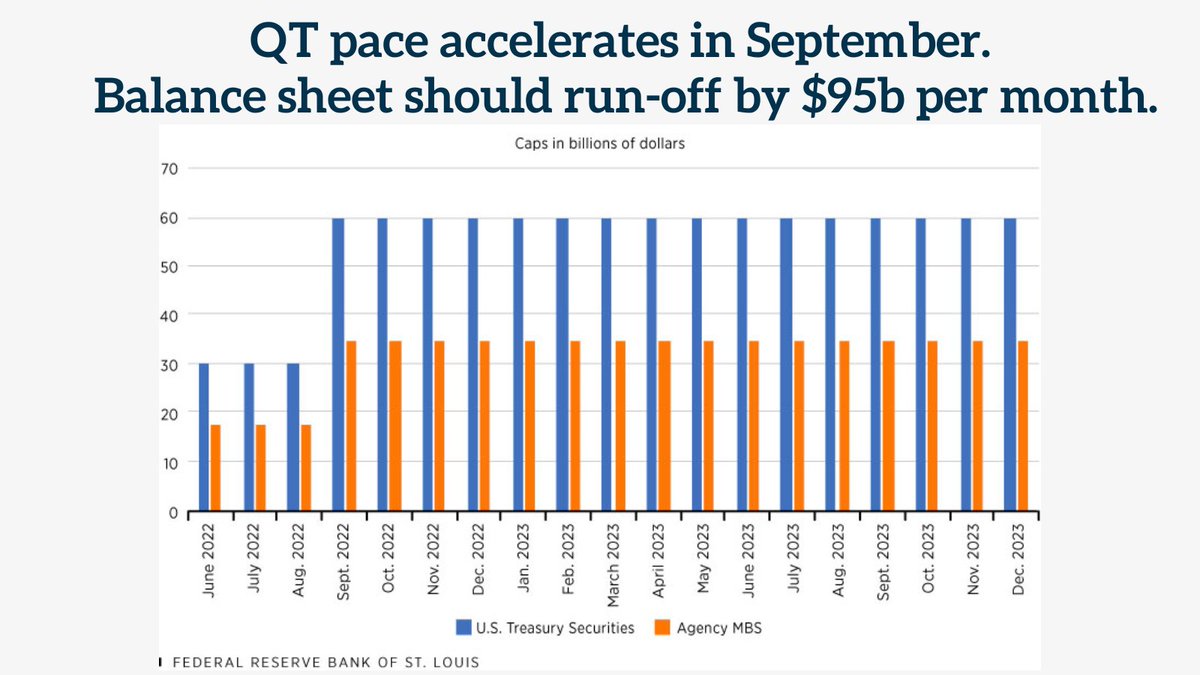

Joseph on Quantitative Tightening (QT).

The Fed ramps up QT in Sept. and allows $95 billion in assets / month to roll off its balance sheet.

QT doesn't necessarily contract the money supply, but changes its composition to:

More 💵 in treasuries.

Less 💵 in bank accounts.

The Fed ramps up QT in Sept. and allows $95 billion in assets / month to roll off its balance sheet.

QT doesn't necessarily contract the money supply, but changes its composition to:

More 💵 in treasuries.

Less 💵 in bank accounts.

This impacts financial markets because the Fed buys fewer treasuries, resulting in an increase in available supply.

Private entities in the market need to do the buying instead.

They are not the Fed so they will demand lower prices and higher yields.

Private entities in the market need to do the buying instead.

They are not the Fed so they will demand lower prices and higher yields.

Regardless, many investors have been buying bonds as we enter a technical recession and terrible economic data keeps popping up.

The market expects treasury yields to cap off as it believes that the Fed will need to cut rates sooner than anticipated.

The market expects treasury yields to cap off as it believes that the Fed will need to cut rates sooner than anticipated.

In the past decades, it made sense to immediately buy bonds when there's a recession.

But with 9% inflation, we could very well be in a regime change.

Markets have not been good at responding to new regimes.

Wang does not see an early dovish pivot to be likely.

But with 9% inflation, we could very well be in a regime change.

Markets have not been good at responding to new regimes.

Wang does not see an early dovish pivot to be likely.

Can the Fed suppress inflation with rate hikes and QT?

While raising rates doesn't increase the supply of oil, grains and housing, it has a clear impact on these prices.

We've seen the price of the commodity complex tumble due to demand destruction as the Fed has raised rates.

While raising rates doesn't increase the supply of oil, grains and housing, it has a clear impact on these prices.

We've seen the price of the commodity complex tumble due to demand destruction as the Fed has raised rates.

Wang distinguishes between the paper & physical market for commodities.

The paper market includes derivatives like:

Futures, Swaps & Options for underlying commodities.

The physical market is for trades involving the commodity itself. (i.e. Buying physical barrels of oil.)

The paper market includes derivatives like:

Futures, Swaps & Options for underlying commodities.

The physical market is for trades involving the commodity itself. (i.e. Buying physical barrels of oil.)

The paper market is much larger than the physical market and it's very sensitive to interest rates.

Tanking the paper market through rate hikes leads to lower prices in the physical market as well.

Tanking the paper market through rate hikes leads to lower prices in the physical market as well.

(10/41) With so much debt in the world, can the US afford to let rates rise a lot?

Need to distinguish between public and private debt.

Public debt is issued by the gov't.

There is no issue of affordability because the Fed can print money and buy the debt.

Need to distinguish between public and private debt.

Public debt is issued by the gov't.

There is no issue of affordability because the Fed can print money and buy the debt.

Private debt can be a problem because corporations can't print currency.

But high inflation means higher revenues.

And many corporations took out loans at historically low interest rates.

So, the private sector can likely afford higher rates due to inflated revenues.

But high inflation means higher revenues.

And many corporations took out loans at historically low interest rates.

So, the private sector can likely afford higher rates due to inflated revenues.

Another way to look at this is through real interest rates - they are around 0%, which is very low.

As far as mortgage rates - most people locked in generationally low rates for 30 year mortgages.

These mortgages should be more affordable as their payments are inflated away.

As far as mortgage rates - most people locked in generationally low rates for 30 year mortgages.

These mortgages should be more affordable as their payments are inflated away.

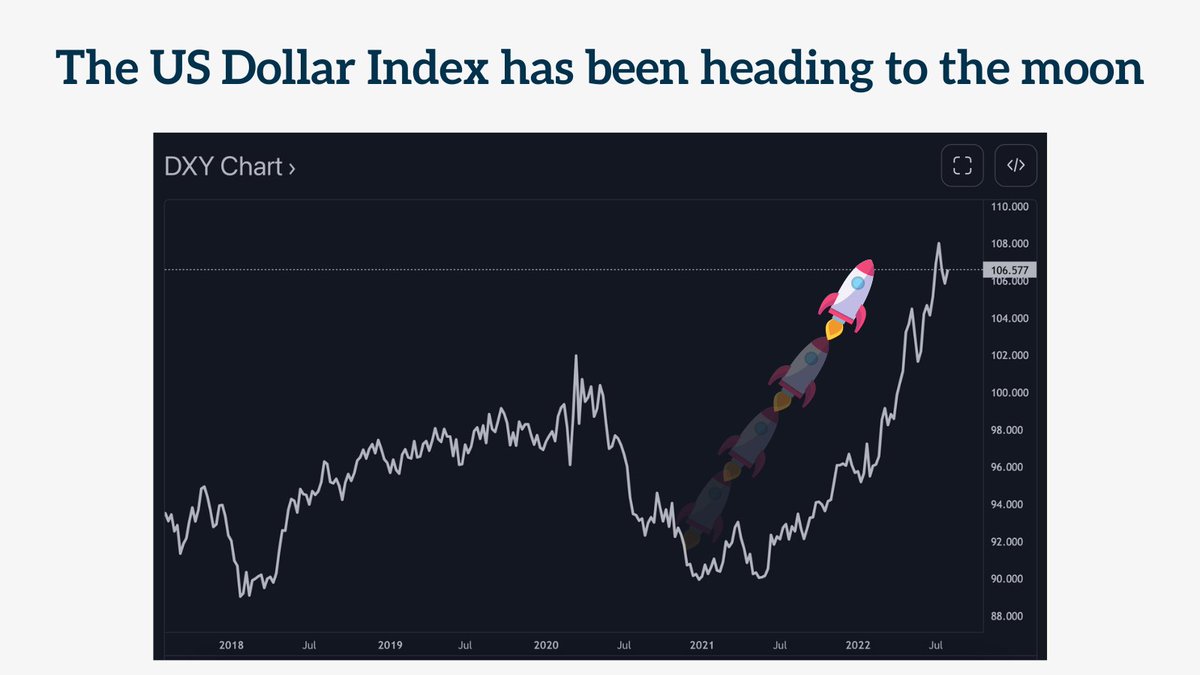

Wang on the strength of the US Dollar.

The Fed is intentionally making the dollar stronger to tame inflation.

Conventionally, we think a stronger currency makes imports cheaper.

But it doesn't impact the US import costs because almost everything is already priced in dollars.

The Fed is intentionally making the dollar stronger to tame inflation.

Conventionally, we think a stronger currency makes imports cheaper.

But it doesn't impact the US import costs because almost everything is already priced in dollars.

However, a stronger dollar has a tremendous impact on other countries.

For example, Japan imports oil which is priced in dollars.

This makes oil more expensive to Japan, which destroys their demand and consumption, making commodity prices come down.

For example, Japan imports oil which is priced in dollars.

This makes oil more expensive to Japan, which destroys their demand and consumption, making commodity prices come down.

(15/41) Does the Fed care about Bitcoin?

Fed is not interested in Bitcoin at all.

Analogy: The US Army (Fed) is not afraid of a small uprising in Springfield (Bitcoin).

However, cryptocurrencies are generating a lot of attention and may have financial stability implications.

Fed is not interested in Bitcoin at all.

Analogy: The US Army (Fed) is not afraid of a small uprising in Springfield (Bitcoin).

However, cryptocurrencies are generating a lot of attention and may have financial stability implications.

Wang sees cryptocurrency regulations from the government as the biggest headwind for the space.

They don't even need to enact a ban like China did.

They can simply require everyone that trades these to report to the IRS and pay their taxes.

They don't even need to enact a ban like China did.

They can simply require everyone that trades these to report to the IRS and pay their taxes.

What about Gold?

The Fed does not care about the price of gold - the dollar system is so much stronger and larger.

Is gold a good store of value?

It doesn't seem to be working - we've had high inflation in the last few years but gold prices are down.

The Fed does not care about the price of gold - the dollar system is so much stronger and larger.

Is gold a good store of value?

It doesn't seem to be working - we've had high inflation in the last few years but gold prices are down.

Joseph Wang's trading views.

Wang believes that macro is the biggest theme this year.

The Fed has the biggest impact on financial markets, if you can understand that then you can know how markets will behave.

Wang believes that macro is the biggest theme this year.

The Fed has the biggest impact on financial markets, if you can understand that then you can know how markets will behave.

(19/41) Ex: At the beginning of the year, the market was at ATH and bond yields were low - clearly, the Fed was going to be hawkish.

Wang believes right now that the Fed is being misunderstood.

The recent market rally implies an early dovish pivot, but this is highly unlikely.

Wang believes right now that the Fed is being misunderstood.

The recent market rally implies an early dovish pivot, but this is highly unlikely.

Has the Fed lost credibility?

Wang argues that credibility doesn't really matter.

Textbook economists say that credibility matters because it keeps inflation expectations anchored.

But, when you look at inflation exp. surveys, half the people have no idea what the Fed does.

Wang argues that credibility doesn't really matter.

Textbook economists say that credibility matters because it keeps inflation expectations anchored.

But, when you look at inflation exp. surveys, half the people have no idea what the Fed does.

Market based inflation expectations have been trending towards 2% in the medium term, but have been wrong for the past 2 years.

Instrument like TIPS, used to measure inflation expectations, are often bought mechanically from retirement funds, making it hard to get good insights.

Instrument like TIPS, used to measure inflation expectations, are often bought mechanically from retirement funds, making it hard to get good insights.

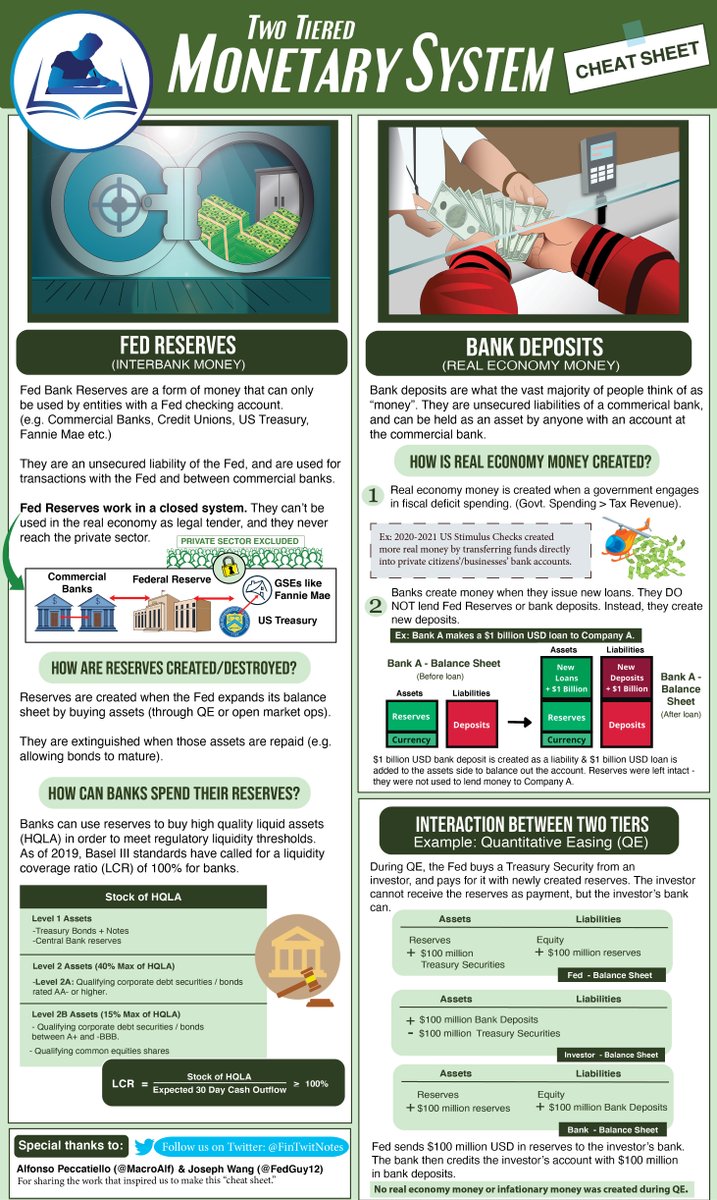

Measuring the money supply.

What you consider is money depends on who you are in the financial system.

Most people think of money as deposits at the bank, measured as M2 money supply.

If you are a bank, then money is deposits at the Fed (reserves).

What you consider is money depends on who you are in the financial system.

Most people think of money as deposits at the bank, measured as M2 money supply.

If you are a bank, then money is deposits at the Fed (reserves).

If you are a huge asset manager, money is treasuries.

You can put them up as collateral, use them for trades, and monetize them for bank deposits.

There is no single right way to define money.

You can put them up as collateral, use them for trades, and monetize them for bank deposits.

There is no single right way to define money.

(24/41) Will QE become conventional now and become part of their toolkit forever?

It's already conventional now.

The Fed did QE during the GFC, now the ECB and Bank of England do it.

The Central Banking community is very close. They talk and look at what each other are doing.

It's already conventional now.

The Fed did QE during the GFC, now the ECB and Bank of England do it.

The Central Banking community is very close. They talk and look at what each other are doing.

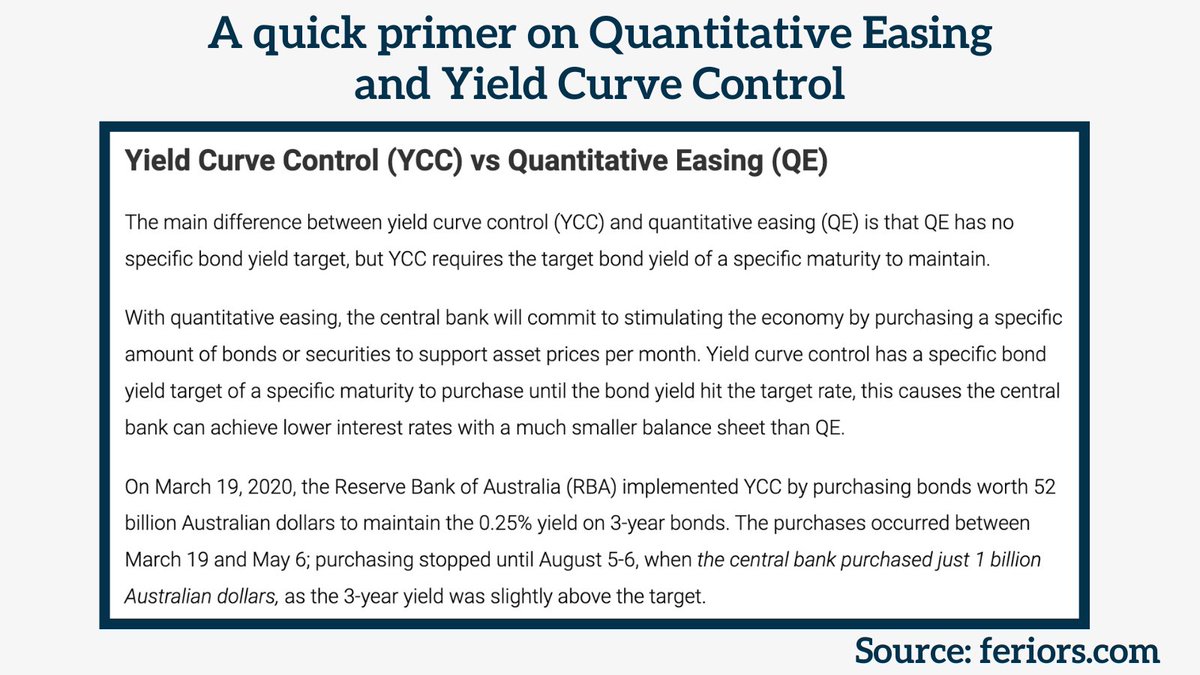

The next frontier of monetary policy is Yield Curve Control (YCC).

YCC is setting a cap on yields and buying as many bonds as needed to maintain the cap.

CBs think of YCC as a better form of QE.

With QE, you try to push down yields but don't know the exact effect it will have.

YCC is setting a cap on yields and buying as many bonds as needed to maintain the cap.

CBs think of YCC as a better form of QE.

With QE, you try to push down yields but don't know the exact effect it will have.

Side effect: when you print a lot of money to buy treasuries, you make the balance sheet of the banking sector larger.

Under the current regulatory regime, this causes problems for banks.

YCC is better - you don’t have to do lots of easing because the market won’t test you.

Under the current regulatory regime, this causes problems for banks.

YCC is better - you don’t have to do lots of easing because the market won’t test you.

The market knows what’s going to happen so they won’t challenge the central bank.

We’re transitioning from a less regulation, free market system to a system where things will be more controlled.

We have a very large treasury market and it requires more active management.

We’re transitioning from a less regulation, free market system to a system where things will be more controlled.

We have a very large treasury market and it requires more active management.

Hard Money

The perception is that if you have hard money, it’s more of a constraint on the government.

But keep history in mind - we used to use hard money.

But we just devalued it and got off the gold standard.

Even in Roman times, hard money went through devaluation.

The perception is that if you have hard money, it’s more of a constraint on the government.

But keep history in mind - we used to use hard money.

But we just devalued it and got off the gold standard.

Even in Roman times, hard money went through devaluation.

Housing Market

~60% percent of Americans own a home and it's a big part of their wealth.

Home prices have come down a bit as mortgage rates soared to 6%, though they're now back to about 5%.

If market expects rate cuts, mortgage rates fall and the housing market re-inflates.

~60% percent of Americans own a home and it's a big part of their wealth.

Home prices have come down a bit as mortgage rates soared to 6%, though they're now back to about 5%.

If market expects rate cuts, mortgage rates fall and the housing market re-inflates.

Home prices have appreciated a ton in the last two years and haven’t even come close to giving back their gains.

There’s a lot of room to the downside on almost all asset classes.

Inflation at 9% is no joke and the Fed will work very hard to get back to where they want to be.

There’s a lot of room to the downside on almost all asset classes.

Inflation at 9% is no joke and the Fed will work very hard to get back to where they want to be.

(31/41) Fed Pivot?

Wang believes that the market has misinterpreted the Fed.

He expects more rate rises and tighter conditions.

The Fed will likely have board members speak out and push back on the market’s narrative.

Wang believes that the market has misinterpreted the Fed.

He expects more rate rises and tighter conditions.

The Fed will likely have board members speak out and push back on the market’s narrative.

Fed wants inflation down, but the market thinks they will cut rates soon.

So equity market rallies, and people have more money to start spending more.

If equity markets keep rallying, rate hikes may be more aggressive.

Fed needs asset prices lower to achieve price stability.

So equity market rallies, and people have more money to start spending more.

If equity markets keep rallying, rate hikes may be more aggressive.

Fed needs asset prices lower to achieve price stability.

US Household purchasing power suggests that a dovish pivot is still far away.

We can examine a couple factors:

1. High credit creation

2. Wage growth

3. Household net worth

Wang provides insights on each of these components.

We can examine a couple factors:

1. High credit creation

2. Wage growth

3. Household net worth

Wang provides insights on each of these components.

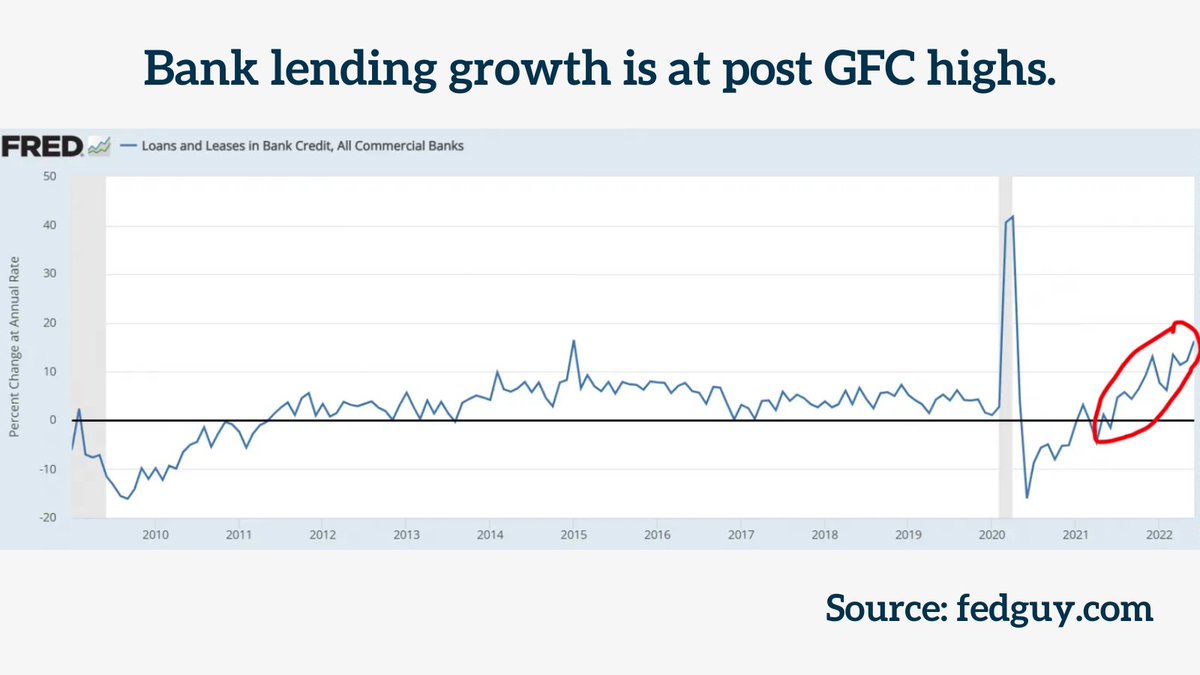

Credit creation.

Bank loan growth is accelerating, despite the fact that borrowing costs are increasing due to rising rates.

This shows household strength as they have historically high levels of wealth and wage growth.

They are not deterred from borrowing at higher rates.

Bank loan growth is accelerating, despite the fact that borrowing costs are increasing due to rising rates.

This shows household strength as they have historically high levels of wealth and wage growth.

They are not deterred from borrowing at higher rates.

Banks are incentivized to issue more loans as they receive more interest from higher rates.

Banks create new money out of thin air when they make loans -this money flows through the economy and drives up prices.

Rates need to get to a point where borrowers can't afford loans.

Banks create new money out of thin air when they make loans -this money flows through the economy and drives up prices.

Rates need to get to a point where borrowers can't afford loans.

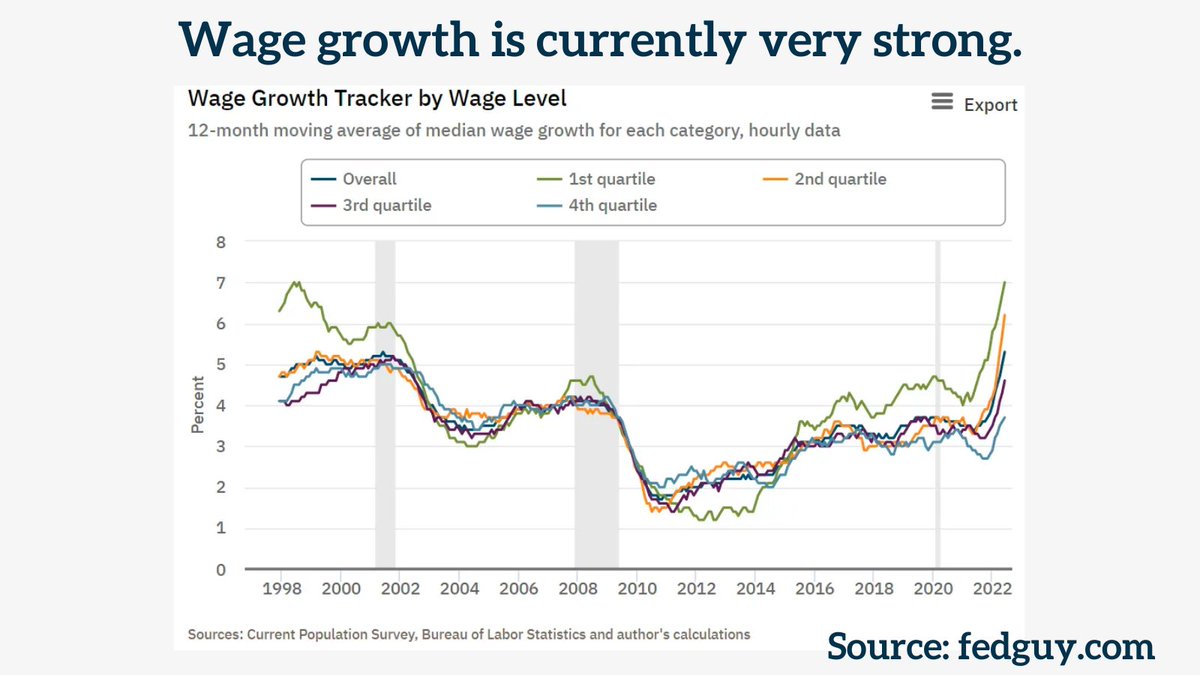

(36/41) Wages.

Wage growth has been very strong and likely to remain so because of a shortage of labor across many industries.

5% overall wage growth is historically high and appears to be accelerating.

Major labor market indicators suggest continued labor strength.

Wage growth has been very strong and likely to remain so because of a shortage of labor across many industries.

5% overall wage growth is historically high and appears to be accelerating.

Major labor market indicators suggest continued labor strength.

We are seeing historically low unemployment levels and two job postings per unemployed worker.

The labor shortage seems to be structural due to declining workforce, suggesting less sensitivity to rising rates.

Therefore, policy needs to be very restrictive to slow wage growth.

The labor shortage seems to be structural due to declining workforce, suggesting less sensitivity to rising rates.

Therefore, policy needs to be very restrictive to slow wage growth.

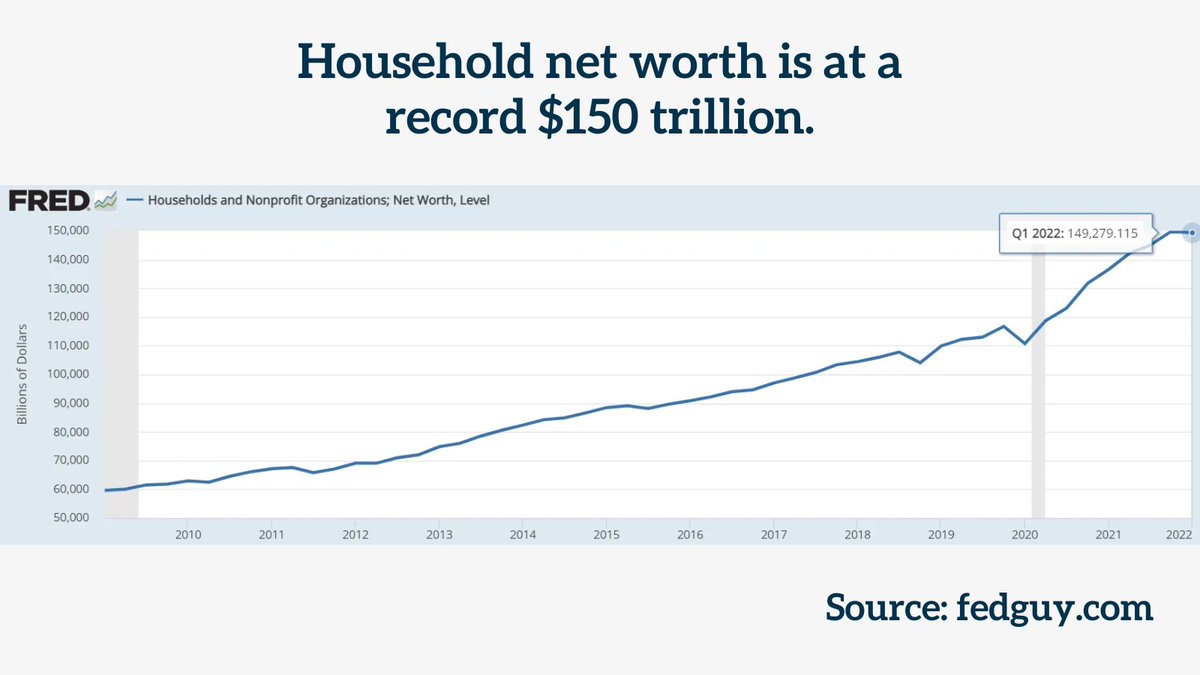

Household wealth.

Household net wealth rose to $150t earlier this year largely from asset inflation and is still notably above pre-pandemic levels after recent declines.

Many households also increased their wealth by refinancing their debt at historically low interest rates.

Household net wealth rose to $150t earlier this year largely from asset inflation and is still notably above pre-pandemic levels after recent declines.

Many households also increased their wealth by refinancing their debt at historically low interest rates.

Fed tightening stance has reduced asset prices, but the recent rally has undone a lot of that reduction.

Market is undoing the tightening by reviving risk-on sentiment.

Stubbornly high household wealth makes higher inflation affordable and a return to 2% inflation less likely.

Market is undoing the tightening by reviving risk-on sentiment.

Stubbornly high household wealth makes higher inflation affordable and a return to 2% inflation less likely.

Fed's priority is inflation and then full employment.

Declining economic activity is a desired outcome for tighter monetary policy. Not a reason to expect a dovish pivot.

Wages, wealth and credit seem to be growing at an exceptional rate - policy is still too accommodative.

Declining economic activity is a desired outcome for tighter monetary policy. Not a reason to expect a dovish pivot.

Wages, wealth and credit seem to be growing at an exceptional rate - policy is still too accommodative.

(41/41) That's the thread!

Many thanks to @FedGuy12 for providing an insider's perspective into how the Fed and monetary policy work.

Thanks to @MoneyMorningAU for hosting the interview.

Sources:

#more-4856" target="_blank" rel="noopener" onclick="event.stopPropagation()">fedguy.com

youtube.com

Many thanks to @FedGuy12 for providing an insider's perspective into how the Fed and monetary policy work.

Thanks to @MoneyMorningAU for hosting the interview.

Sources:

#more-4856" target="_blank" rel="noopener" onclick="event.stopPropagation()">fedguy.com

youtube.com

We'll be regularly sharing our notes and research across various topics in finance.

The financial world is complex, and we aim to produce content that is valuable to readers of all levels.

A follow, like and retweet 👇is greatly appreciated!

The financial world is complex, and we aim to produce content that is valuable to readers of all levels.

A follow, like and retweet 👇is greatly appreciated!

Loading suggestions...