1/

For most of us, the path to financial freedom consists of:

(a) SAVING our money diligently, and

(b) INVESTING these savings intelligently.

Here are 4 key ideas to help you understand the interplay between SAVING and INVESTING.

For most of us, the path to financial freedom consists of:

(a) SAVING our money diligently, and

(b) INVESTING these savings intelligently.

Here are 4 key ideas to help you understand the interplay between SAVING and INVESTING.

2/

Key Idea 1.

SAVING is (usually) much more under our control than INVESTING.

If we look closely enough, most of us can probably find some expense we can cut. Some fat we can trim.

Or some way to make a little more money.

These are actions we can take to boost our savings.

Key Idea 1.

SAVING is (usually) much more under our control than INVESTING.

If we look closely enough, most of us can probably find some expense we can cut. Some fat we can trim.

Or some way to make a little more money.

These are actions we can take to boost our savings.

3/

By contrast, the returns we get from INVESTING tend to be mostly outside our control.

Stocks can move sideways for a long time.

Our returns may be driven by sentiment, macro factors, or just pure randomness/luck.

Even with a good process, good returns are NOT guaranteed.

By contrast, the returns we get from INVESTING tend to be mostly outside our control.

Stocks can move sideways for a long time.

Our returns may be driven by sentiment, macro factors, or just pure randomness/luck.

Even with a good process, good returns are NOT guaranteed.

4/

As the Stoics would say, we should try to focus on what we CAN control, as opposed to worrying too much about things we CAN'T control.

This means most of us would do well to focus at least *some* of our energy on SAVING, as opposed to worrying only about INVESTING.

As the Stoics would say, we should try to focus on what we CAN control, as opposed to worrying too much about things we CAN'T control.

This means most of us would do well to focus at least *some* of our energy on SAVING, as opposed to worrying only about INVESTING.

5/

Key Idea 2.

SAVING gives us *capital* -- the "raw material" we need for INVESTING.

How this works:

a) Our SAVINGS go into our "portfolio",

b) This portfolio GROWS over time (assuming it's invested well), and

c) As the portfolio grows, we keep adding MORE savings to it.

Key Idea 2.

SAVING gives us *capital* -- the "raw material" we need for INVESTING.

How this works:

a) Our SAVINGS go into our "portfolio",

b) This portfolio GROWS over time (assuming it's invested well), and

c) As the portfolio grows, we keep adding MORE savings to it.

6/

In this way, our SAVINGS provide the "grist" for our INVESTING "mill".

If we keep contributing to our portfolio, and our portfolio keeps growing over time, there's usually a good chance we'll achieve financial freedom before we retire.

In this way, our SAVINGS provide the "grist" for our INVESTING "mill".

If we keep contributing to our portfolio, and our portfolio keeps growing over time, there's usually a good chance we'll achieve financial freedom before we retire.

7/

Key Idea 3.

During the early years, SAVING matters more. But as time passes, INVESTING starts to matter more and more.

For example, let's take Jim -- a recent college graduate.

Let's say Jim has $0 to his name. But he just landed a job that pays him $80K per year.

Key Idea 3.

During the early years, SAVING matters more. But as time passes, INVESTING starts to matter more and more.

For example, let's take Jim -- a recent college graduate.

Let's say Jim has $0 to his name. But he just landed a job that pays him $80K per year.

8/

Of this $80K, let's say Jim is able to SAVE $20K every year.

So, at the end of Year 1, Jim is worth $20K (one year of savings).

Now, suppose Jim invests this $20K and earns a 10% per year return on it.

How much will Jim be worth at the end of Year 2?

Of this $80K, let's say Jim is able to SAVE $20K every year.

So, at the end of Year 1, Jim is worth $20K (one year of savings).

Now, suppose Jim invests this $20K and earns a 10% per year return on it.

How much will Jim be worth at the end of Year 2?

9/

Well, during Year 2, Jim's $20K will earn him 10% -- or $2K -- in investment gains.

Also, during Year 2, Jim will SAVE another $20K from his $80K salary.

Well, during Year 2, Jim's $20K will earn him 10% -- or $2K -- in investment gains.

Also, during Year 2, Jim will SAVE another $20K from his $80K salary.

10/

So, at the *end* of Year 2, Jim will be worth:

- The $20K he had at the end of Year 1,

- Plus $2K of investment gains,

- Plus $20K of additional savings.

That's $42K.

So, at the *end* of Year 2, Jim will be worth:

- The $20K he had at the end of Year 1,

- Plus $2K of investment gains,

- Plus $20K of additional savings.

That's $42K.

11/

So, Jim's net worth GROWS from $20K at the end of Year 1 to $42K at the end of Year 2.

Notice that, of this $42K - $20K = $22K growth, ONLY $2K came from investment gains.

The lion's share -- $20K -- came from additional savings.

This is typical during the early years.

So, Jim's net worth GROWS from $20K at the end of Year 1 to $42K at the end of Year 2.

Notice that, of this $42K - $20K = $22K growth, ONLY $2K came from investment gains.

The lion's share -- $20K -- came from additional savings.

This is typical during the early years.

12/

But IF Jim keeps this up EVERY year:

a) Grow the portfolio 10%,

b) Save an additional $20K, and

c) Add this $20K to the portfolio,

THEN, eventually, Jim's net worth will come to be dominated by his *investment gains*, NOT his *savings*.

But IF Jim keeps this up EVERY year:

a) Grow the portfolio 10%,

b) Save an additional $20K, and

c) Add this $20K to the portfolio,

THEN, eventually, Jim's net worth will come to be dominated by his *investment gains*, NOT his *savings*.

13/

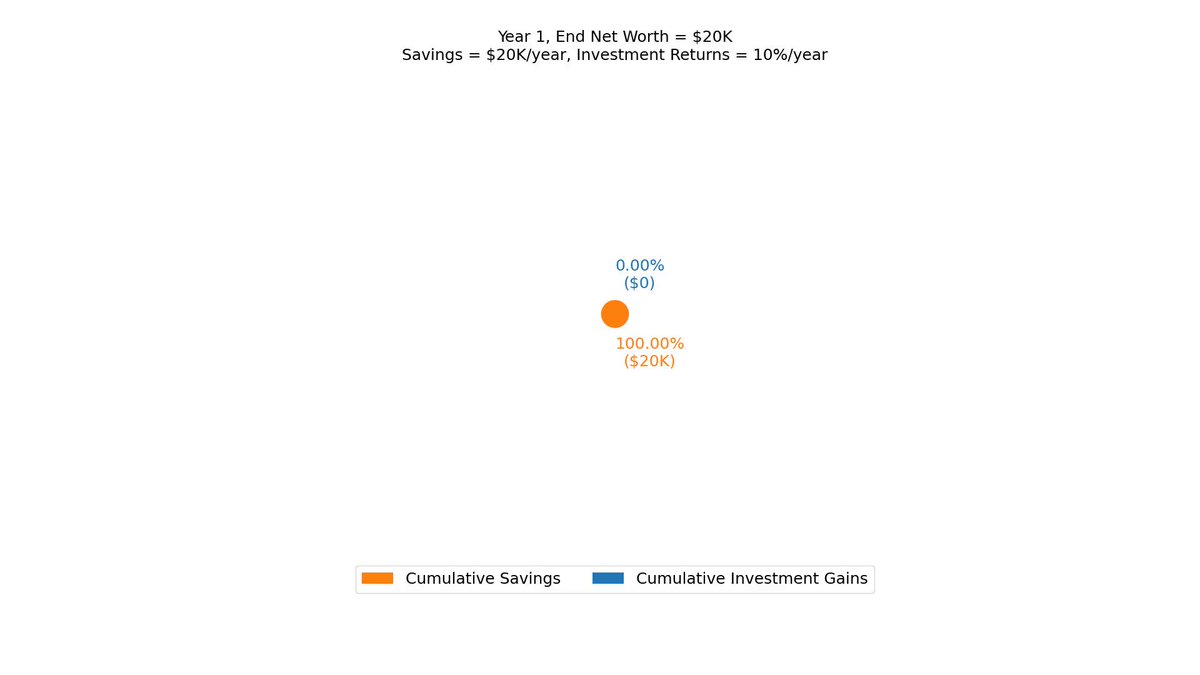

Here's a 30-year simulation illustrating this.

At each year end, Jim's net worth contains 2 components: his cumulative savings (ORANGE), and his cumulative investment gains (BLUE).

During the early years, ORANGE dominates.

But after Year ~15 or so, BLUE takes over.

Here's a 30-year simulation illustrating this.

At each year end, Jim's net worth contains 2 components: his cumulative savings (ORANGE), and his cumulative investment gains (BLUE).

During the early years, ORANGE dominates.

But after Year ~15 or so, BLUE takes over.

14/

And here's an animation showing Jim's net worth as a pie chart over time.

As the years go by, the pie becomes BIGGER.

And INVESTING starts to account for more and more of the pie, not SAVING.

And here's an animation showing Jim's net worth as a pie chart over time.

As the years go by, the pie becomes BIGGER.

And INVESTING starts to account for more and more of the pie, not SAVING.

15/

Key Idea 4. The Saving vs Investing Frontier.

This is a simple plot that illuminates for us the trade-offs between SAVING and INVESTING.

Let's do an example.

Say we're worth $50K now.

And we want to be worth $5M in 30 years time.

That's our "goal".

Key Idea 4. The Saving vs Investing Frontier.

This is a simple plot that illuminates for us the trade-offs between SAVING and INVESTING.

Let's do an example.

Say we're worth $50K now.

And we want to be worth $5M in 30 years time.

That's our "goal".

16/

To achieve this goal:

a) How much should we SAVE per year? And,

b) At what return should we INVEST these savings?

To achieve this goal:

a) How much should we SAVE per year? And,

b) At what return should we INVEST these savings?

17/

For example, suppose we SAVE $30K every year, and our portfolio gains 10% every year from INVESTING.

Starting at $50K, in 30 years time, we'll be worth about $5.8M -- more than enough to meet our goal.

For example, suppose we SAVE $30K every year, and our portfolio gains 10% every year from INVESTING.

Starting at $50K, in 30 years time, we'll be worth about $5.8M -- more than enough to meet our goal.

18/

But suppose we SAVE $50K per year, and earn 5% via INVESTING.

Now, starting at the same $50K, we'll only end up with $3.54M.

This is NOT enough to meet our goal.

But suppose we SAVE $50K per year, and earn 5% via INVESTING.

Now, starting at the same $50K, we'll only end up with $3.54M.

This is NOT enough to meet our goal.

19/

So, *some* combinations of SAVING and INVESTING will successfully get us to our goal.

And other combinations won't.

The "Saving vs Investing Frontier" tells us exactly *which* combinations will succeed and which won't.

So, *some* combinations of SAVING and INVESTING will successfully get us to our goal.

And other combinations won't.

The "Saving vs Investing Frontier" tells us exactly *which* combinations will succeed and which won't.

20/

Here's how it works:

We take our SAVINGS per year on the X-axis. And our INVESTMENT returns per year on the Y-axis.

We draw a BLUE curve ("the frontier") that separates successful (SAVE, INVEST) combos from unsuccessful ones.

Like so:

Here's how it works:

We take our SAVINGS per year on the X-axis. And our INVESTMENT returns per year on the Y-axis.

We draw a BLUE curve ("the frontier") that separates successful (SAVE, INVEST) combos from unsuccessful ones.

Like so:

21/

This "frontier" is NOT perfect.

After all, both our savings and our investment returns are likely to vary from year to year.

And the "frontier" plot assumes that both will remain roughly constant.

That's not very realistic.

This "frontier" is NOT perfect.

After all, both our savings and our investment returns are likely to vary from year to year.

And the "frontier" plot assumes that both will remain roughly constant.

That's not very realistic.

22/

Still, I've found this "frontier" diagram useful for financial planning.

Given a "financial freedom" goal, this plot lets me visualize all possible (SAVE, INVEST) combos that will get me there.

This gives me a feel for how difficult the goal is, and how to plan for it.

Still, I've found this "frontier" diagram useful for financial planning.

Given a "financial freedom" goal, this plot lets me visualize all possible (SAVE, INVEST) combos that will get me there.

This gives me a feel for how difficult the goal is, and how to plan for it.

22/

The idea is to be *conservative*.

For example, we want to SAVE so much that, EVEN if we materially under-perform the S&P 500 on the INVESTING side, we will STILL likely reach our goal.

Like so:

The idea is to be *conservative*.

For example, we want to SAVE so much that, EVEN if we materially under-perform the S&P 500 on the INVESTING side, we will STILL likely reach our goal.

Like so:

23/

If you're still with me, thank you very much!

FinTwit tends to focus a lot on INVESTING. And that's great.

But we should remember that SAVING is pretty important too -- especially during the early stages of our investing journey.

Have a great weekend!

/End

If you're still with me, thank you very much!

FinTwit tends to focus a lot on INVESTING. And that's great.

But we should remember that SAVING is pretty important too -- especially during the early stages of our investing journey.

Have a great weekend!

/End

Loading suggestions...