QE leads to steeper yield curves and under certain circumstances to higher (not lower) long-end bond yields.

It's QT that generates flatter yield curves and possibly lower yields.

Seems counterintuitive, I know - but let's find out how it works.

A thread.

1/

It's QT that generates flatter yield curves and possibly lower yields.

Seems counterintuitive, I know - but let's find out how it works.

A thread.

1/

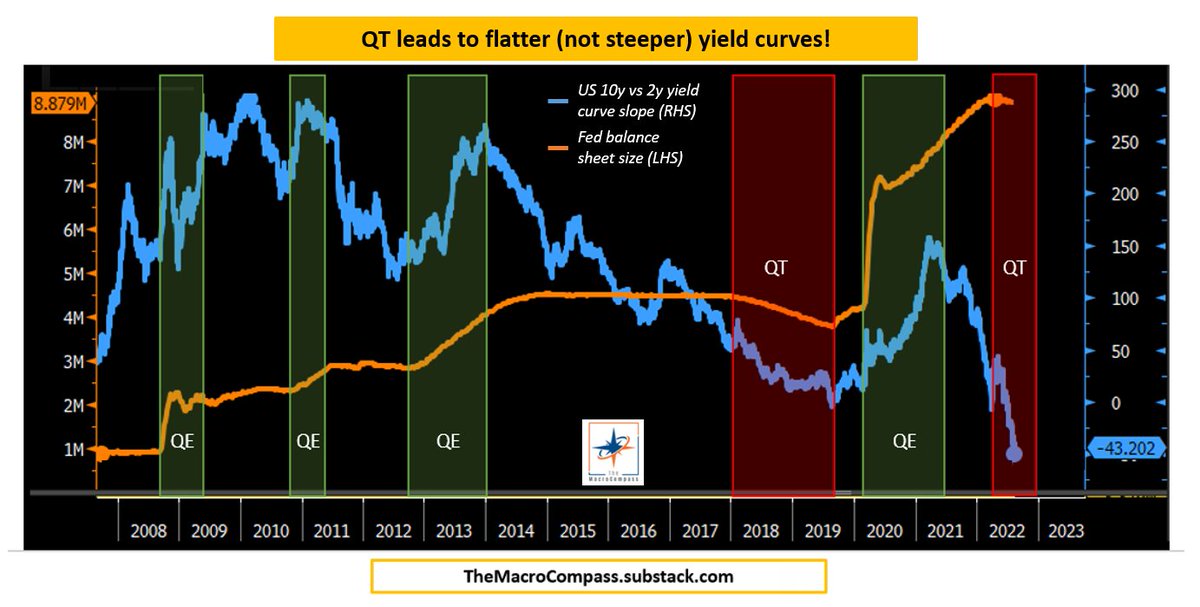

In the US, we've had 4 major QE episodes which started in 2008, 2010, 2012, & 2020 (all marked in green) and 2 attempts at QT (2018 & 2022, both marked in red).

It's very clear that the 10y vs 2y curve slope (blue) steepened in QE periods and flattened in QT periods.

Why?

2/

It's very clear that the 10y vs 2y curve slope (blue) steepened in QE periods and flattened in QT periods.

Why?

2/

Central Banks have a strong and direct impact on the front-end (3m to 2y) of the bond market - through their monetary policy actions they can effectively force markets to price in what they want

But QE generally buys bonds all the way to the 10-30y part of the curve!

3/

But QE generally buys bonds all the way to the 10-30y part of the curve!

3/

Nevertheless, curve tend to steepen into the dominant phases of QE

That's because long-term bond yields can be thought of as the sum of real yields + inflation expectations + term premium

And when QE is deemed to be successful, here is what happen to each component

4/

That's because long-term bond yields can be thought of as the sum of real yields + inflation expectations + term premium

And when QE is deemed to be successful, here is what happen to each component

4/

Let's use 2020 as an example

In the 6m after the Fed started QE, 10y real yields (blue) dropped by 50 bps & inflation expectations (orange) rose by 60 bps - pretty much a wash

But in the following 6 months, inflation expectations kept marching higher while real yields...

5/

In the 6m after the Fed started QE, 10y real yields (blue) dropped by 50 bps & inflation expectations (orange) rose by 60 bps - pretty much a wash

But in the following 6 months, inflation expectations kept marching higher while real yields...

5/

...didn't drop anymore

Actually, as soon as the economy was back on its knees real yields quickly repriced back higher joining inflation expectations on the move up

This is because a successful QE achieves the following:

1) Compress risk premia (lower real yields)

6/

Actually, as soon as the economy was back on its knees real yields quickly repriced back higher joining inflation expectations on the move up

This is because a successful QE achieves the following:

1) Compress risk premia (lower real yields)

6/

2) Lower volatility and encourage the flow of credit towards the real economy

3) This helps kickstarting economic activity, with inflation expectations reflecting this at first

4) Once economic activity picks up, real yields can slowly start to reflect that too

7/

3) This helps kickstarting economic activity, with inflation expectations reflecting this at first

4) Once economic activity picks up, real yields can slowly start to reflect that too

7/

A combination of higher inflation expectations first and later on higher real yields too as the economy picks up lead to higher 10-30y nominal yields while front-end yields remain much more anchored by Central Bank policy

QE = steeper, not flatter yield curves

8/

QE = steeper, not flatter yield curves

8/

Another more technical reason stems from QE's ability to lower cross-asset volatility

As that happens and the economy picks up, investors are very tempted to put ''positive carry'' trades on - those are trades that continue to make money as long as nothing happens (low vol)

9/

As that happens and the economy picks up, investors are very tempted to put ''positive carry'' trades on - those are trades that continue to make money as long as nothing happens (low vol)

9/

Curve steepeners are generally positive carry trades, same as being long risky investments - the idea is that you must be rewarded for the risk you are taking

Today, betting that the US 2y-10y yield curve slope will steepen makes you roughly 18 bps/year to start with!

10/

Today, betting that the US 2y-10y yield curve slope will steepen makes you roughly 18 bps/year to start with!

10/

So you can understand if there is no volatility and investors expect QE to help the economic recovery process, they will be tempted to steepen the curve.

Now, what about QT?

Well, the opposite is true: yield curves flatten during QT.

11/

Now, what about QT?

Well, the opposite is true: yield curves flatten during QT.

11/

That's because:

A) QT generally happens when Central Banks are also raising rates, and hence front-end bond yields are moving higher

B) QT tends to weaken future prospects for growth and inflation, and hence long-end bond yields struggle to follow much higher

12/

A) QT generally happens when Central Banks are also raising rates, and hence front-end bond yields are moving higher

B) QT tends to weaken future prospects for growth and inflation, and hence long-end bond yields struggle to follow much higher

12/

Yes but.

QT removes reserves from the system and it forces the private sector to absorb more supply of bonds: how can this lead to flatter yield curves and potentially lower bond yields?

It's indeed true that if you stuff the private sector with a lot of bonds very quickly

13/

QT removes reserves from the system and it forces the private sector to absorb more supply of bonds: how can this lead to flatter yield curves and potentially lower bond yields?

It's indeed true that if you stuff the private sector with a lot of bonds very quickly

13/

Dealers first and investors after will have to rethink what is their marginal required yield to swallow this new supply of bonds.

But once the (potential) initial effect fades away, the big picture comes back into play: what about long-term growth and inflation?

14/

But once the (potential) initial effect fades away, the big picture comes back into play: what about long-term growth and inflation?

14/

Also, the structural demand for long-end bond yields is very strong and inelastic due to the structure of our system.

- Pension funds & insurance companies have huge duration gaps to cover

- Banks have strong regulatory incentives to buy bonds

- Government bonds are so..

15/

- Pension funds & insurance companies have huge duration gaps to cover

- Banks have strong regulatory incentives to buy bonds

- Government bonds are so..

15/

...crucial for a bunch of investors (asset managers, corporate treasuries etc) which own a lot of ''cash'' and that have no access to Central Bank deposits.

Instead of unsecured deposits at a commercial bank, they often prefer a better collateral (Treasuries).

16/

Instead of unsecured deposits at a commercial bank, they often prefer a better collateral (Treasuries).

16/

Summarizing:

- QE leads to steeper yield curves

- QT leads to flatter yield curves

That's because while CBs can greatly affect front-end yields, long-end yields are mostly driven by expectations about future growth and inflation (QE helps, QT doesn't!).

Finally...

17/

- QE leads to steeper yield curves

- QT leads to flatter yield curves

That's because while CBs can greatly affect front-end yields, long-end yields are mostly driven by expectations about future growth and inflation (QE helps, QT doesn't!).

Finally...

17/

If you enjoyed this thread, it's very likely you'll find the educational & market coverage material I publish in my free newsletter TheMacroCompass.substack.com pretty interesting - there is much more over there!

It's free and 85,000+ people joined already - go have a look! :)

18/18

It's free and 85,000+ people joined already - go have a look! :)

18/18

Loading suggestions...