Business

Economics

Finance

Industry

Company Overview

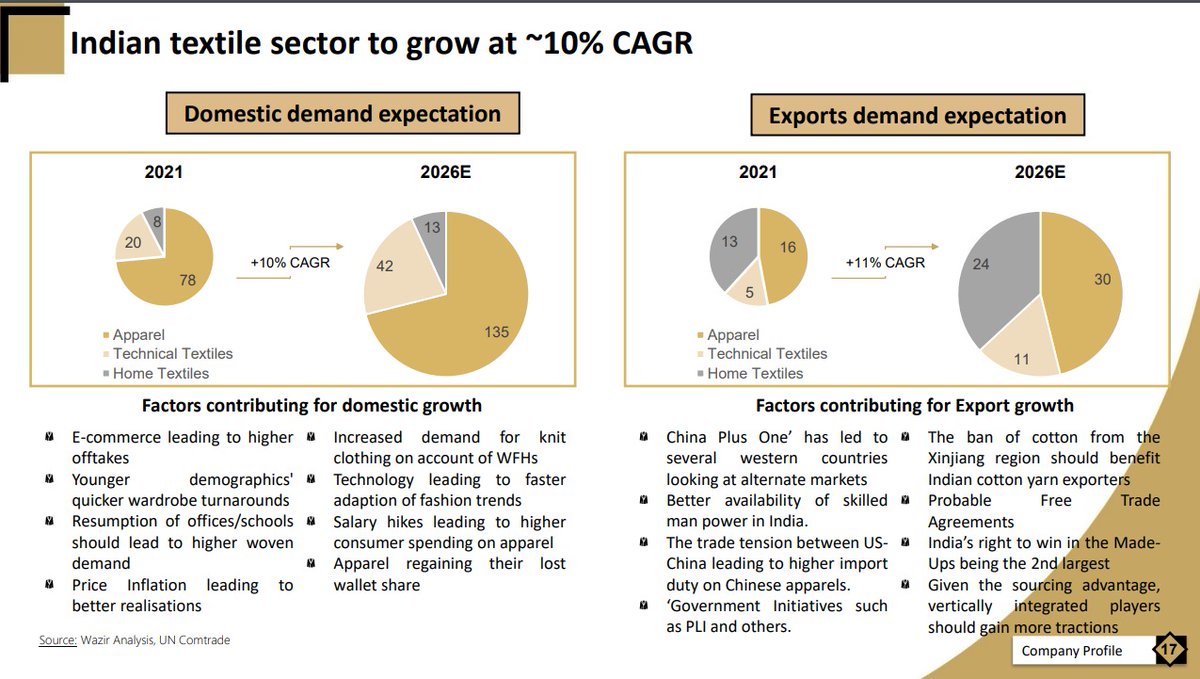

Market Expansion

Domestic Demand

Domestic Sales

Raw Material Price Hike

Cotton Prices

Industry Outlook

China's Plus One Strategy

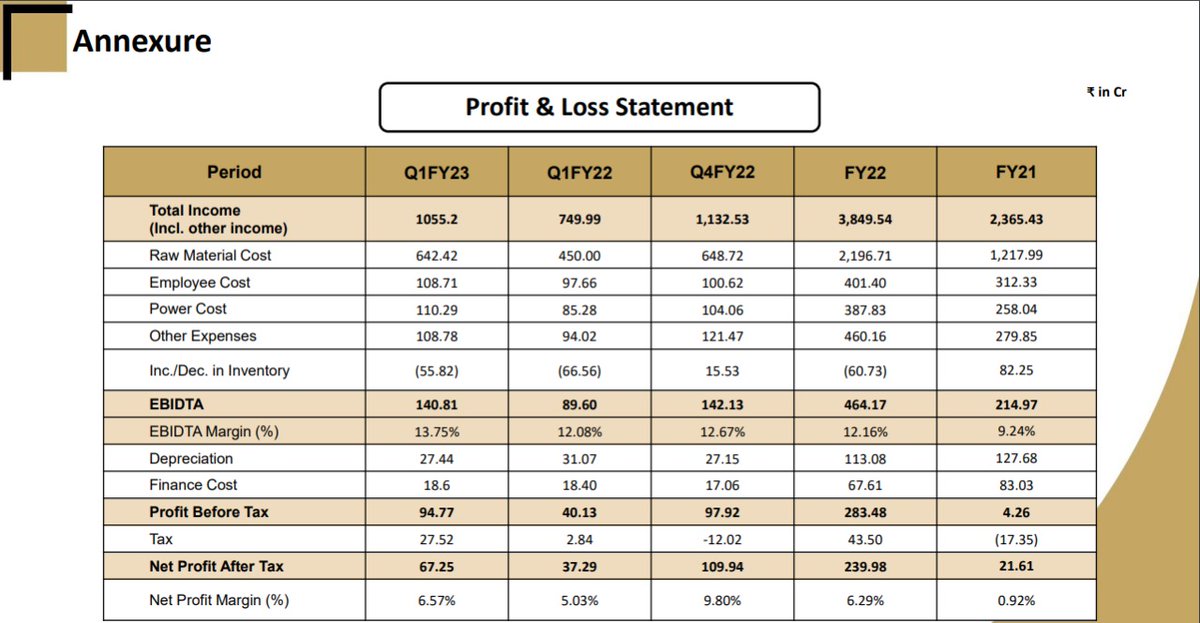

RSWM Ltd. conducted their Q1 FY23 con call on 10th August 2022

Here are the key highlights 👇👇👇

Here are the key highlights 👇👇👇

•Overview

-Company reparted high domestic sales this quarter.

-Q1 Fy23 is treated as lean quarter given the challenges of hike in raw material price

-Due to pass through strategy margins were not much affected.

-Company reparted high domestic sales this quarter.

-Q1 Fy23 is treated as lean quarter given the challenges of hike in raw material price

-Due to pass through strategy margins were not much affected.

-Drop of cotton prices by 25-30% has positively affected the industry in H2 FY23

-In India 20-25% area would expand 10 cotton growing states.

-Company is optimistic about domestic demand on back of China's plus one strategy.

-In India 20-25% area would expand 10 cotton growing states.

-Company is optimistic about domestic demand on back of China's plus one strategy.

-School uniform requirements increased the demand of yarn.

-Wedding season increased foot falls on retail.

-There are headwind on export side due to fear of recession.

-Government is supporting industry via various schemes

-Wedding season increased foot falls on retail.

-There are headwind on export side due to fear of recession.

-Government is supporting industry via various schemes

•Financials

-Gross profits grew by 44.5% due to resource optimization.

-EBITDA margin contracted 30 bps on account of high input cost during quarter.

-Company had 46 megawatt power plant, as of now power cost is ₹530 per unit for purchasing it from state power board.

-Gross profits grew by 44.5% due to resource optimization.

-EBITDA margin contracted 30 bps on account of high input cost during quarter.

-Company had 46 megawatt power plant, as of now power cost is ₹530 per unit for purchasing it from state power board.

-Company has 45-60 of inventory days for cotton.

•Segmental Performance

-YARN

~High competition and pricing pressure influencing demand for cotton and PC mélange.

~Mills producing cotton and blends have shifted to other blends

~Margins for 100% cotton can be affected due to seasonal change.

~30k spindle yarn capacity

-YARN

~High competition and pricing pressure influencing demand for cotton and PC mélange.

~Mills producing cotton and blends have shifted to other blends

~Margins for 100% cotton can be affected due to seasonal change.

~30k spindle yarn capacity

~Domestic space remained disturbed due to expected price correction on back of softening of cotton prices

-DENIMS

~Domestic collection due in healthy range of 4%.

~Denim fabric capacity in Marswada started last year and they will help in future growth.

-DENIMS

~Domestic collection due in healthy range of 4%.

~Denim fabric capacity in Marswada started last year and they will help in future growth.

•Expansionary measures

-Company has completed expansion of 400cr. on full capacity utilisation which will give sales of 700cr.

-Noda plant of 315cr. with 50k spindles will be completed in FY24.

-Company has completed expansion of 400cr. on full capacity utilisation which will give sales of 700cr.

-Noda plant of 315cr. with 50k spindles will be completed in FY24.

Loading suggestions...