Ester industries Ltd conducted Q1 FY23 con call on 12 August 2022.

Here are the key highlights👇👇👇

Here are the key highlights👇👇👇

•Overview

-Company core business films and special polymer registered good growth despite challenging inflationary environment.

-EPA transaction rectification within 25-30 days would deleverage balance sheet and that funds would be used for planned cap ex.

-Company core business films and special polymer registered good growth despite challenging inflationary environment.

-EPA transaction rectification within 25-30 days would deleverage balance sheet and that funds would be used for planned cap ex.

-Better product mix and improved realisations with high sales volume resulted in delivering better operating profit despite high feed stock price and fuel prices.

-Lower finance expenses resulted in strong performance of core businesses.

-Lower finance expenses resulted in strong performance of core businesses.

-Good uptake for marquee established products.

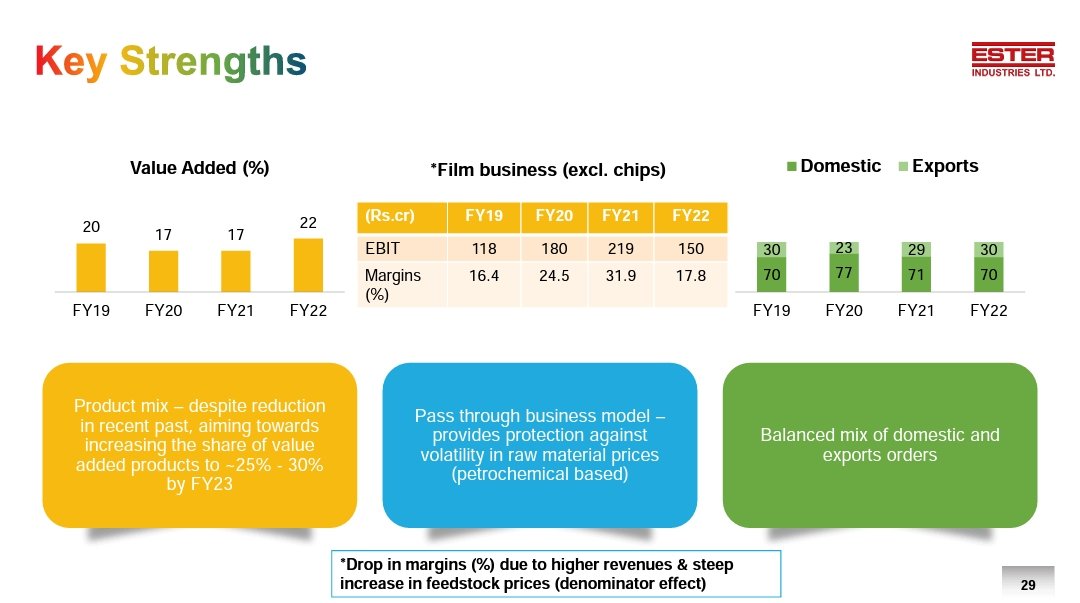

-Improving product mix to de-commodities product portfolio and make it more towards specialty do that margins do not fluctuate.

-Improving product mix to de-commodities product portfolio and make it more towards specialty do that margins do not fluctuate.

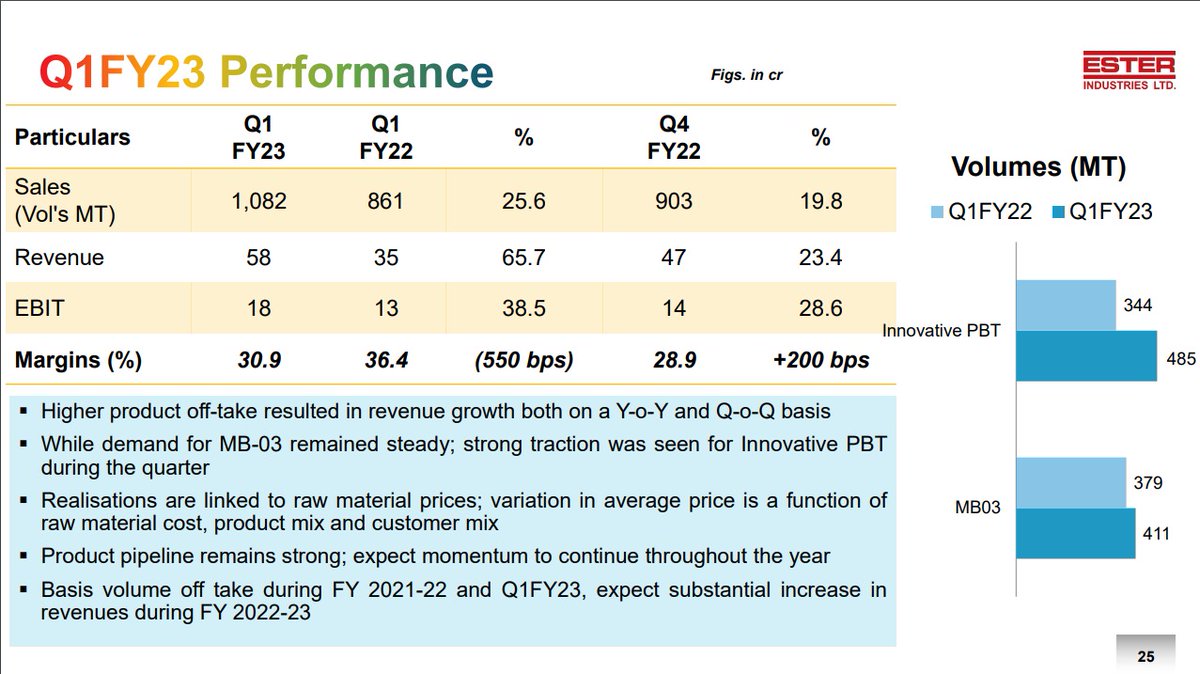

-Avg sales realisations is function of raw material cost, product mix and customer mix.

-Product pipeline remains increasing offering better visibility and potential for improved performance.

-Product pipeline remains increasing offering better visibility and potential for improved performance.

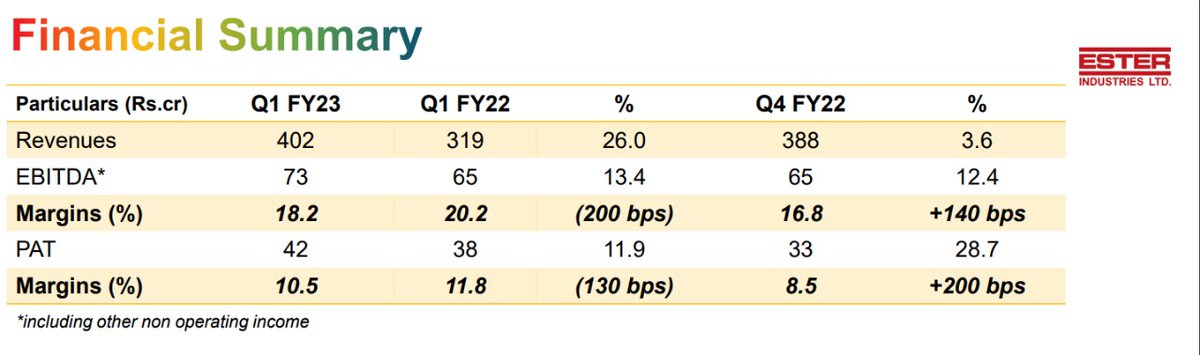

•Financials

-Margins stood at 31% for quarter

-Finished goods prices increase substantially resulting in high input cost.

-Value added constituted of 22% of overall sales volume.

-Margins stood at 31% for quarter

-Finished goods prices increase substantially resulting in high input cost.

-Value added constituted of 22% of overall sales volume.

-Demand-supply imbalance caused by commissioning of new production line may cause margin compression in short term.

-There is no operational debt but interest bearing debt is about 300cr.

-There is no operational debt but interest bearing debt is about 300cr.

•Segmental performance

-Special polymer

~Special polymer have been a patent protected and innovation driven business with realisations tied to raw material prices.

~Due to entry barriers special polymer would be profitable business.

-Special polymer

~Special polymer have been a patent protected and innovation driven business with realisations tied to raw material prices.

~Due to entry barriers special polymer would be profitable business.

-Film business

~Growth in revenue and profitability ~Demand continue to remain stable

~Margin movement was better

~Normalisation of margins in near term due to commissioning of new production line.

~Growth in revenue and profitability ~Demand continue to remain stable

~Margin movement was better

~Normalisation of margins in near term due to commissioning of new production line.

-Engineering plastic business

~Entered into business transfer agreement to sell the business to Radici plastic.

~In Q1 FY23 Performance of business was benign.

~Low volume of engineering plastics compound and moderation in realisations led to margins compression.

~Entered into business transfer agreement to sell the business to Radici plastic.

~In Q1 FY23 Performance of business was benign.

~Low volume of engineering plastics compound and moderation in realisations led to margins compression.

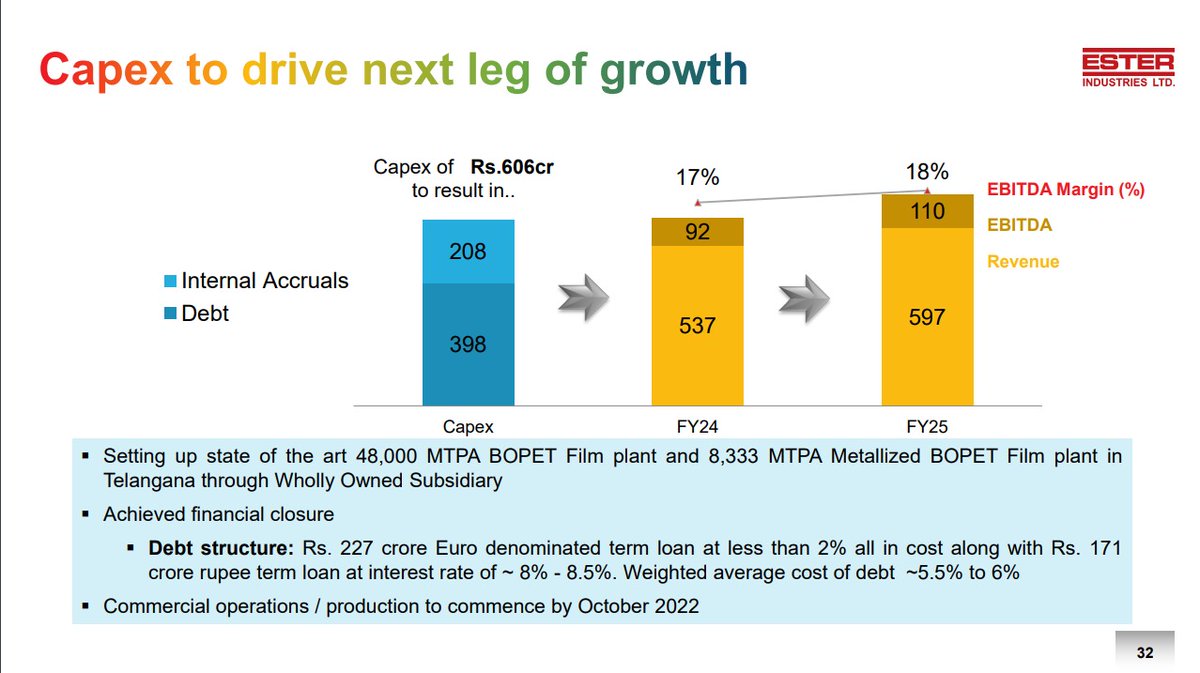

•Cap ex

-Setting up a 48,000 tons plant at Telangana is progressing.

-New capacities are expected to come up in Karnataka, Gujarat which would increase the margins of company.

-Total cap ex is of 200cr. which would be spent in 12-18 months.

-Setting up a 48,000 tons plant at Telangana is progressing.

-New capacities are expected to come up in Karnataka, Gujarat which would increase the margins of company.

-Total cap ex is of 200cr. which would be spent in 12-18 months.

Loading suggestions...