1/ $GMX is currently #4 on the crypto fees leaderboard, 30% of those fees go directly to GMX stakers!

GMX is currently trading at a ~8.2x P/E (at $41 GMX).

Lets discuss how @GMX_IO unique design is able to satisfy all major stakeholders: Traders, LPs, and $GMX stakers.

GMX is currently trading at a ~8.2x P/E (at $41 GMX).

Lets discuss how @GMX_IO unique design is able to satisfy all major stakeholders: Traders, LPs, and $GMX stakers.

2/ Firstly Traders.

GMX is available on both @arbitrum and @avalancheavax, it allows traders to trade BTC, ETH, AVAX, UNI and LINK with 0% slippage, a 10bps fee, and up to 30x leverage.

With 0% slippage and a flat 10bps fee, GMX can offer very competitive execution on trades.

GMX is available on both @arbitrum and @avalancheavax, it allows traders to trade BTC, ETH, AVAX, UNI and LINK with 0% slippage, a 10bps fee, and up to 30x leverage.

With 0% slippage and a flat 10bps fee, GMX can offer very competitive execution on trades.

3/ 0% slippage? How does that work?

GMX utilizes oracle pricing which pulls prices in real time from the top CEXs in order to give traders the best execution possible.

This pricing mechanism also helps out GMX liquidity providers, but more on this later.

GMX utilizes oracle pricing which pulls prices in real time from the top CEXs in order to give traders the best execution possible.

This pricing mechanism also helps out GMX liquidity providers, but more on this later.

4/ GMX's model is especially helpful for market orders.

On an orderbook exchange if a large market order is executed, the order will be filled at the best possible price and can eat up a large portion of the orderbook.

This can cause huge slippage on large market orders.

On an orderbook exchange if a large market order is executed, the order will be filled at the best possible price and can eat up a large portion of the orderbook.

This can cause huge slippage on large market orders.

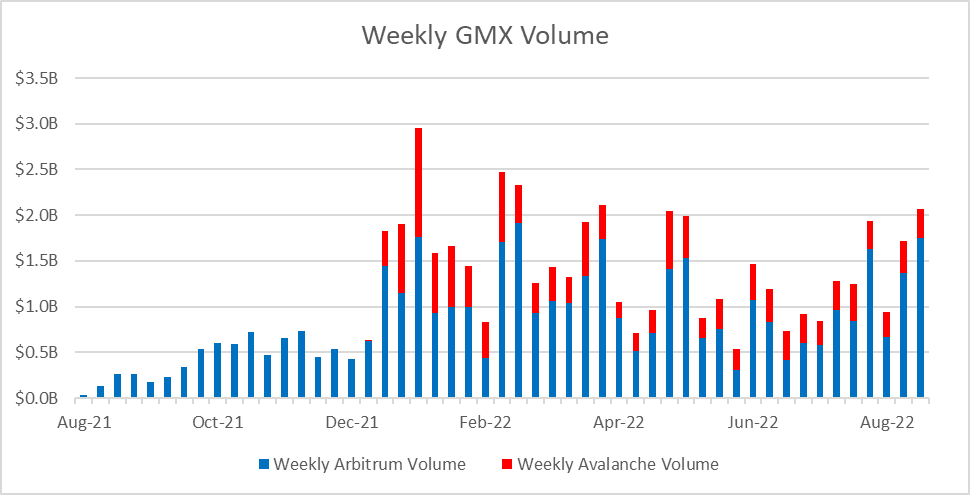

5/ So if GMX can offer traders execution that is comparable to CEXs, what has it done in volume?

GMX has generated over $56B in volume since its launch ~1 year ago!

GMX has generated over $56B in volume since its launch ~1 year ago!

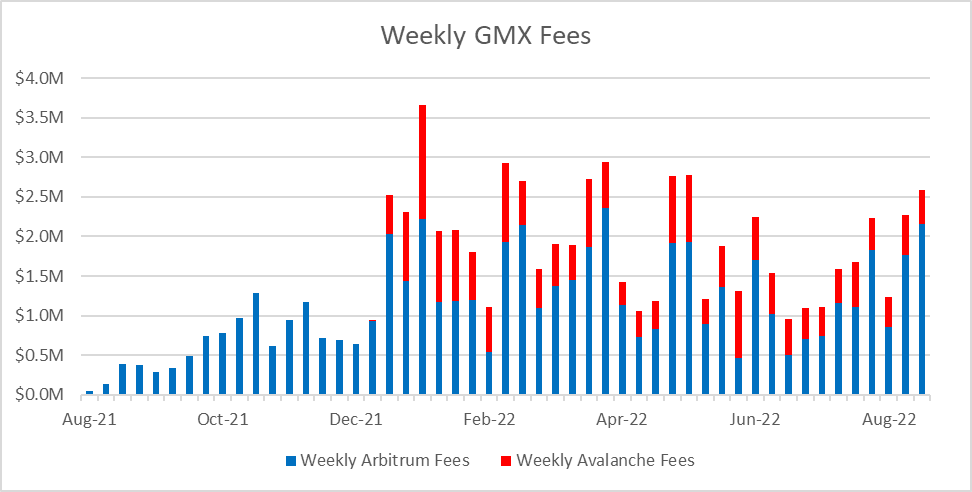

6/ With this level of volume GMX has generated a whopping $76M in fees!

Which leads us nicely to our next two stakeholders, liquidity providers and GMX stakers.

All fees generated on GMX are split at a 70% - 30% rate between these two groups.

Which leads us nicely to our next two stakeholders, liquidity providers and GMX stakers.

All fees generated on GMX are split at a 70% - 30% rate between these two groups.

7/ Lets talk about Liquidity Providers first.

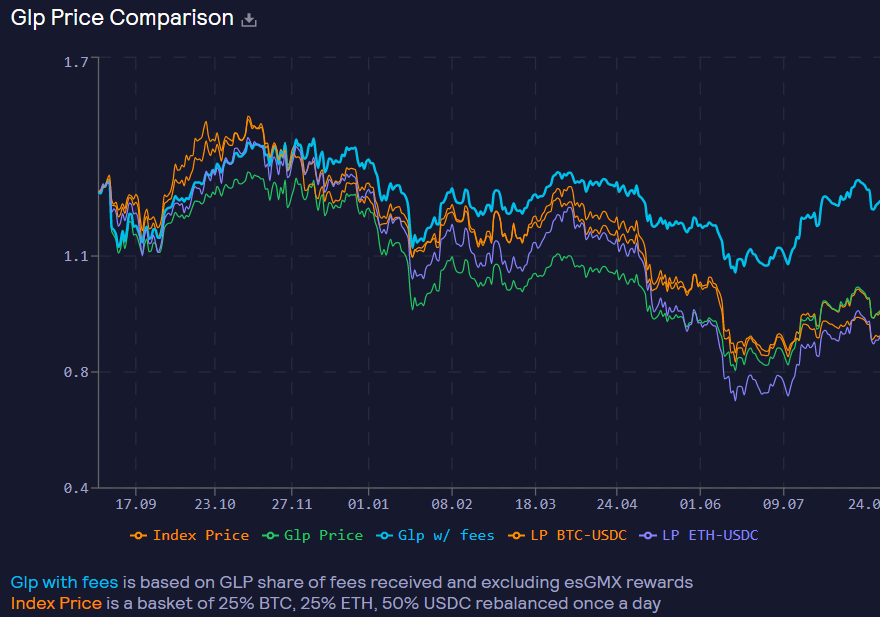

So far 70% of fees is ~$53M which have been distributed in ETH directly to LPs.

Annualizing the most recent weeks liquidity and fees on Arbitrum shows us that LPs are earning a 31% APR (real yield!)

Yet there is some nuance here.

So far 70% of fees is ~$53M which have been distributed in ETH directly to LPs.

Annualizing the most recent weeks liquidity and fees on Arbitrum shows us that LPs are earning a 31% APR (real yield!)

Yet there is some nuance here.

8/ LPs on GMX provide liquidity in the form of "GLP".

GLP is a basket of assets that includes BTC, ETH, UNI, LINK and stablecoins.

When traders take a long position it can be simply thought as "renting" the upside out from GLP in the asset they want exposure to.

GLP is a basket of assets that includes BTC, ETH, UNI, LINK and stablecoins.

When traders take a long position it can be simply thought as "renting" the upside out from GLP in the asset they want exposure to.

9/ For example, if a trader wants 2 ETH of leverage, 2 ETH from GLP is “rented out” to give the trader their desired exposure.

Similarly, a 2 ETH short at $2,000 per ETH is akin to

"reserving" $4,000 worth of stablecoin exposure.

Similarly, a 2 ETH short at $2,000 per ETH is akin to

"reserving" $4,000 worth of stablecoin exposure.

10/ This means that GLP is the counterparty to all traders on GMX.

If traders make money then GLP needs to pay out BTC/ETH for longs or USDC for shorts.

Meaning trader profitability will effect GLPs overall returns vs holding the underlying assets that make up GLP.

If traders make money then GLP needs to pay out BTC/ETH for longs or USDC for shorts.

Meaning trader profitability will effect GLPs overall returns vs holding the underlying assets that make up GLP.

11/ So far with fees, GLP has significantly outperformed a basket of its underlying assets.

This had lead to strong GLP inflows as other sources of DeFi yield compress.

*note that GLP returns could deteriorate if volume on GMX drops or traders become more profitable*

This had lead to strong GLP inflows as other sources of DeFi yield compress.

*note that GLP returns could deteriorate if volume on GMX drops or traders become more profitable*

12/ The beauty of the GMX oracle pricing model is that it doesn't make GLP liquid providers incur the cost of price discovery like a typical AMM would.

Instead market makers on the top CEXs do all the hard work and GMX just borrows the price from them.

Instead market makers on the top CEXs do all the hard work and GMX just borrows the price from them.

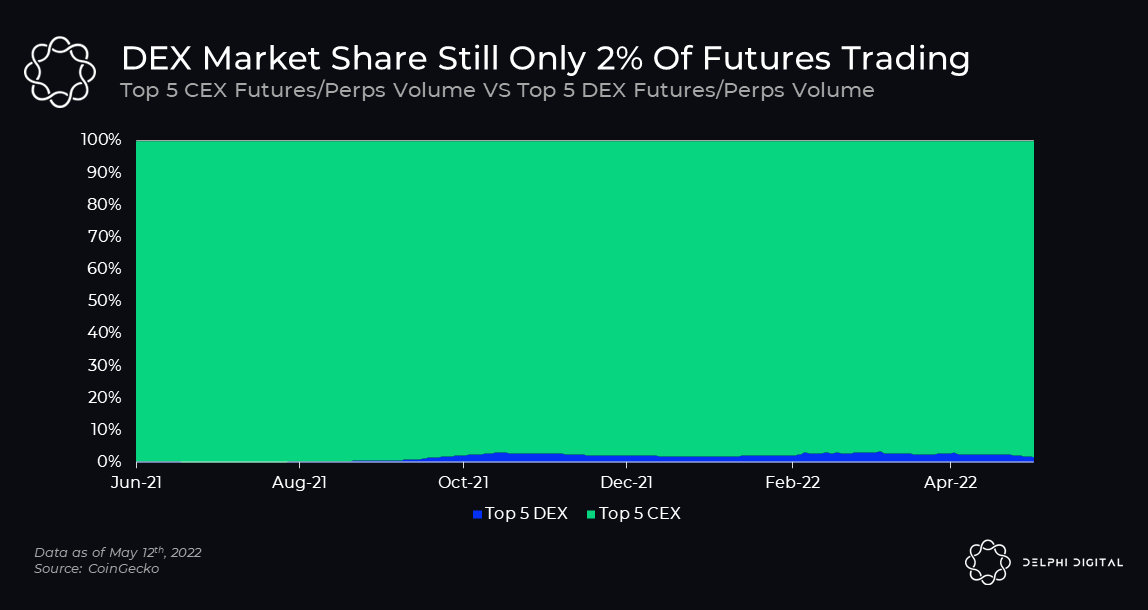

13/ This works extremely well if GMX is not the most liquid place to trade the assets it's offering, but if one day it reaches this level of volume then adjustments will need to be made.

14/ Leveraged DeFi exchanges (including GMX) are very far off from truly competing with their CEX counterparts in terms of volume.

Meaning there is still a ton of room for GMX to grow before it runs into this issue.

Meaning there is still a ton of room for GMX to grow before it runs into this issue.

15/ Finally this leads us to $GMX stakers.

If we annualize fees over the last week we get ~$134M, 30% of which goes to GMX stakers = ~$40M.

At a GMX price of $41 this gives us a circulating market cap of $331M.

Combining these two data points we get a ~8.2x P/E

If we annualize fees over the last week we get ~$134M, 30% of which goes to GMX stakers = ~$40M.

At a GMX price of $41 this gives us a circulating market cap of $331M.

Combining these two data points we get a ~8.2x P/E

16/ GMX is currently working on supporting more assets to be tradable on the platform and improving user experience.

If you want to learn more about GMX check out this thread:

If you want to learn more about GMX check out this thread:

END/

Disclosure: I am an advisor to GMX, and you should always do your own research. Nothing in this thread is financial advice.

Disclosure: I am an advisor to GMX, and you should always do your own research. Nothing in this thread is financial advice.

Loading suggestions...