Yesterday, I tweeted about @abhishec_s latest compilation of The Transcript. See

I like everything Abhishek writes and recommend you to read his threads on investing on Twitter. He asked me to contribute, so I took one of the extracts of The Transcript and created a debate. Here is the extract about a very well-run, and value creating business.

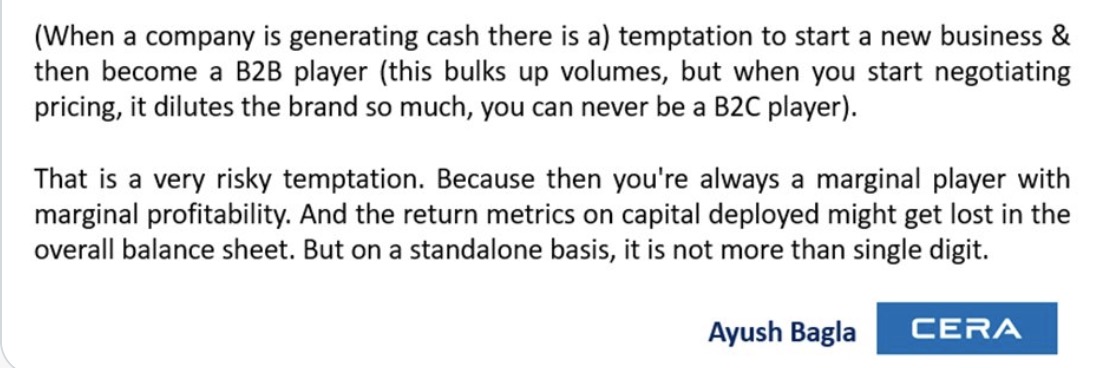

This thread is for arguments in favour - see

And this one is for arguments against - see

There were good arguments tweeted in both threads, which shows that in such topics one can argue in favour as well as against. This is not physics with usually one right answer...

Let’s focus instead on the idea of “risky temptation” in the Cera quote. This is a useful phrase for us. Under what circumstances can temptations be risky?

One, of course, is the risk of making large bets, which if they go wrong, can cause serious harm to the firm. Those are direct losses.

Then, there is the opportunity loss of doing something different and losing focus on what you are already doing so well. This can be very costly too because the other thing takes the focus away from “core competency.”

Cera has decided to not get tempted by distractions and to focus on B2C. This strategy has worked very well. And Cera has articulated good reasons to continue with it. There is no reason for us to doubt this, in my view.

But what is good for Cera may not be good for other businesses. Many businesses thrive because they focus on B2B or cater to both B2B and B2C segments. This was highlighted in the thread that argued against Cera’s strategy.

So, without questioning Cera’s strategy, I think we can agree that there cannot be a principle which requires a single-minded focus on B2C alone, that’s universally applicable. That can never be the case.

I read this book, The Value Imperative, a long time ago and it has a passage that I loved. Here is that passage:

"The objective of our company is to increase the intrinsic value of our equity shares. We are not in business to grow bigger for the sake of size, nor to become more diversified, not to make the most or the best of anything, nor to provide jobs, or have the most modern plants,...

...the happiest customers, lead in new product development or achieve any other status which has no relation to the economic use of capital. Any or all of these may be, from time to time, a means to our objective, but means and ends must never be confused...

...we are in the business solely to improve the inherent value of the equity shareholders' equity in the company."

I think the authors got that right. Means and ends must never be confused. The idea is not to maximise margins, ROCE or revenues but to maximise wealth. This brings us to the second point of interest to me in the Cera quote.

That other point is about return metrics being diluted because when you combine a highly profitable B2C business with a new B2B business with a low ROCE, then the overall ROCE of the company will fall.

To argue that this is always a bad idea is wrong in my view. Many new businesses, even if they have low ROCE right now, may, over time, gravitate towards earnings handsome ROCEs as they become larger, get economies of scale etc.

A second reason why a lower ROCE business could be value accretive is that it opens doors. It brings optionality or some other advantages to the core business.

So, to reject a good business idea because, in the near term, it will dilute company ROCE, is not valid. The idea is not to maximize ROCE but to invest in projects that, over time, will deliver returns well in excess of the cost of capital.

Over to you @abhishec_s.

Loading suggestions...