Is a “soft landing” possible?

In this new working paper with Anton Cheremukhin we contribute to the debate by bringing to the table a new theoretical argument that says that it is not only possible but reasonable in the current context of the labor market: 🧵(1/8)

In this new working paper with Anton Cheremukhin we contribute to the debate by bringing to the table a new theoretical argument that says that it is not only possible but reasonable in the current context of the labor market: 🧵(1/8)

We show that if there are two different matching processes, one for unemployed workers and another one for job-to-job transitions, then implications for the Beveridge curve are potentially very different (because job-to-job transitions don’t affect unemployment). (2/8)

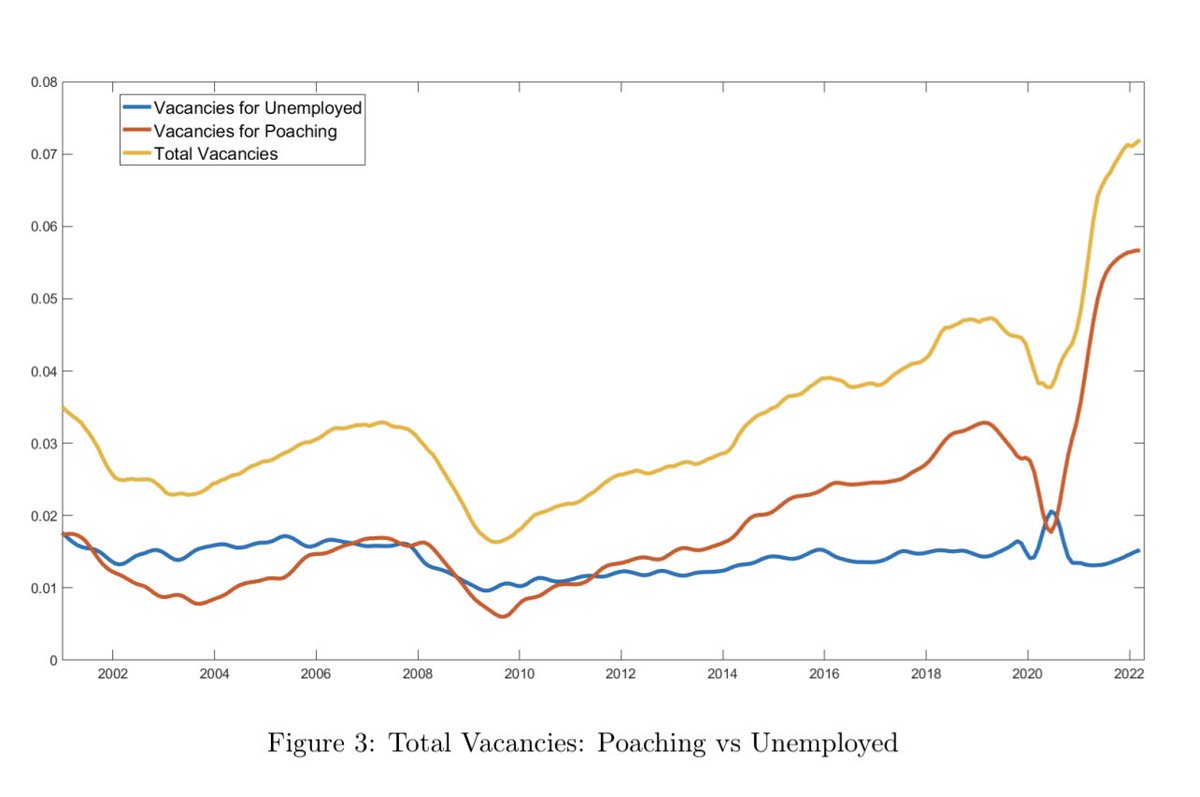

We use our model to estimate what we call “poaching vacancies” which are those vacancies that are meant to hire already employed workers from other firms and vacancies opened to hire from the unemployment pool. (3/8)

We find that “poaching vacancies” have expanded disproportionately relative to “unemployment vacancies” over the years, and show that the puzzling behavior that we have been observing in the Beveridge curve can be attributed to this disproportional expansion. (4/8)

The way that this translates to monetary policy is the following. Consider a monetary tightening that reduces demand and suppresses job openings proportionally. Compare the response of vacancies and unemployment in the mid 2000s and mid 2020s. (5/8)

In the 2000s, job openings were nearly evenly split between the two types of vacancies, while in the 2020s the majority of job openings are poaching vacancies. Therefore, in the second period a disproportionately large fraction of the decline in overall job openings (6/8)

would likely apply to poaching vacancies, which do not affect unemployment. Thus, our results suggest that the response of unemployment to a slowdown in the demand for workers has likely decreased. (7/8)

Namely, a monetary tightening in the 2020s could lead to a relatively large decline in job openings corresponding to only a mild increase in the unemployment rate, consistent with the notion of a "soft landing."

Link to Working Paper: research.stlouisfed.org (8/8)

Link to Working Paper: research.stlouisfed.org (8/8)

Loading suggestions...