I’m excited to share my new paper, "Macroprudential considerations for tokenized cash":

papers.ssrn.com

Policy discussions on stablecoins can be enriched with data. This is one of the first attempts quantifying payment stablecoins’ usage and financial stability risks

1/

papers.ssrn.com

Policy discussions on stablecoins can be enriched with data. This is one of the first attempts quantifying payment stablecoins’ usage and financial stability risks

1/

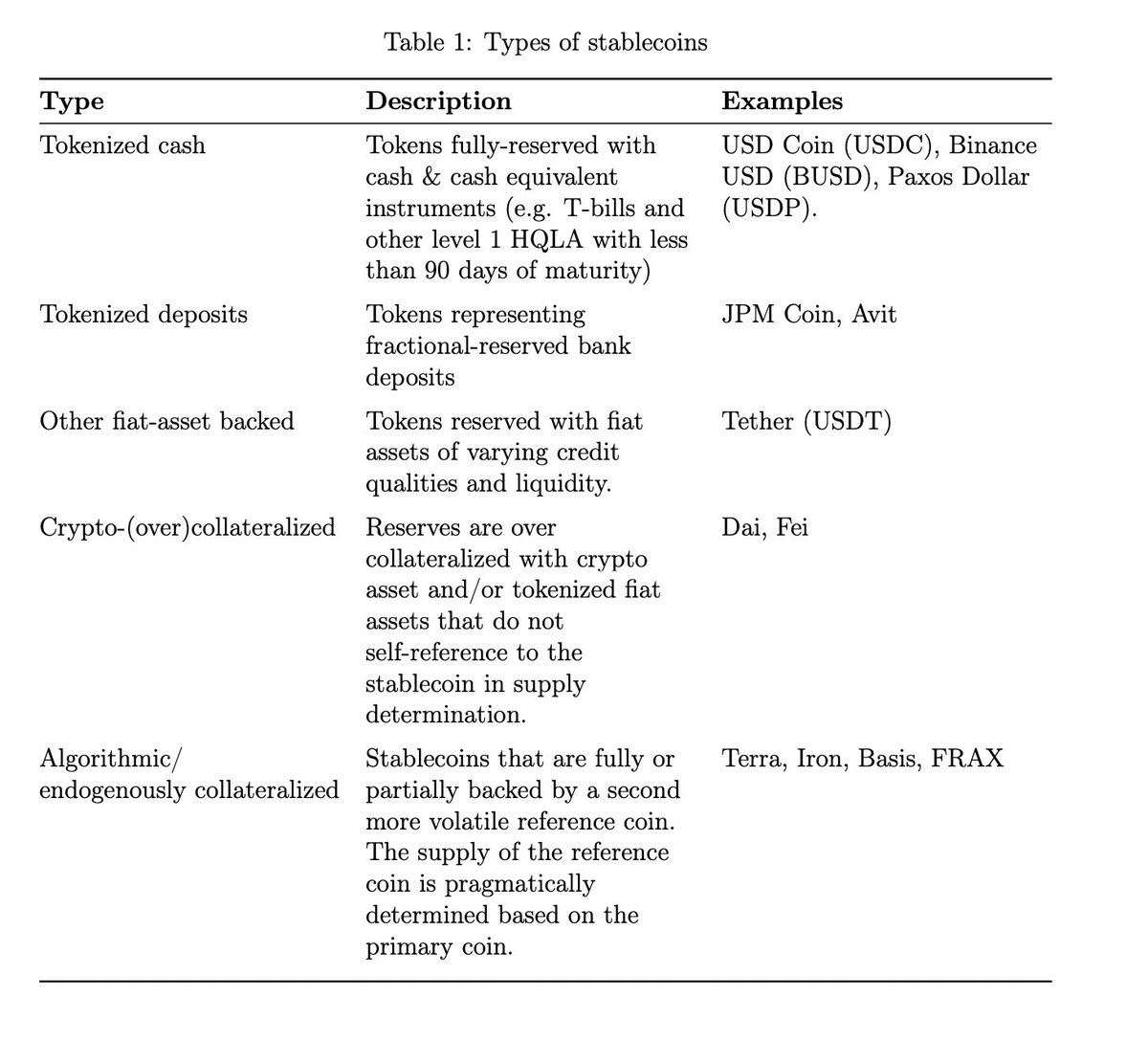

Terra's collapse has tinted the term “stablecoin”. But not all stablecoins are created equal.

Tokenized cash, or stablecoins fully reserved by cash equivalents, have asset quality and liquidity that surpass most banks and money market funds, hence low run risks.

2/

Tokenized cash, or stablecoins fully reserved by cash equivalents, have asset quality and liquidity that surpass most banks and money market funds, hence low run risks.

2/

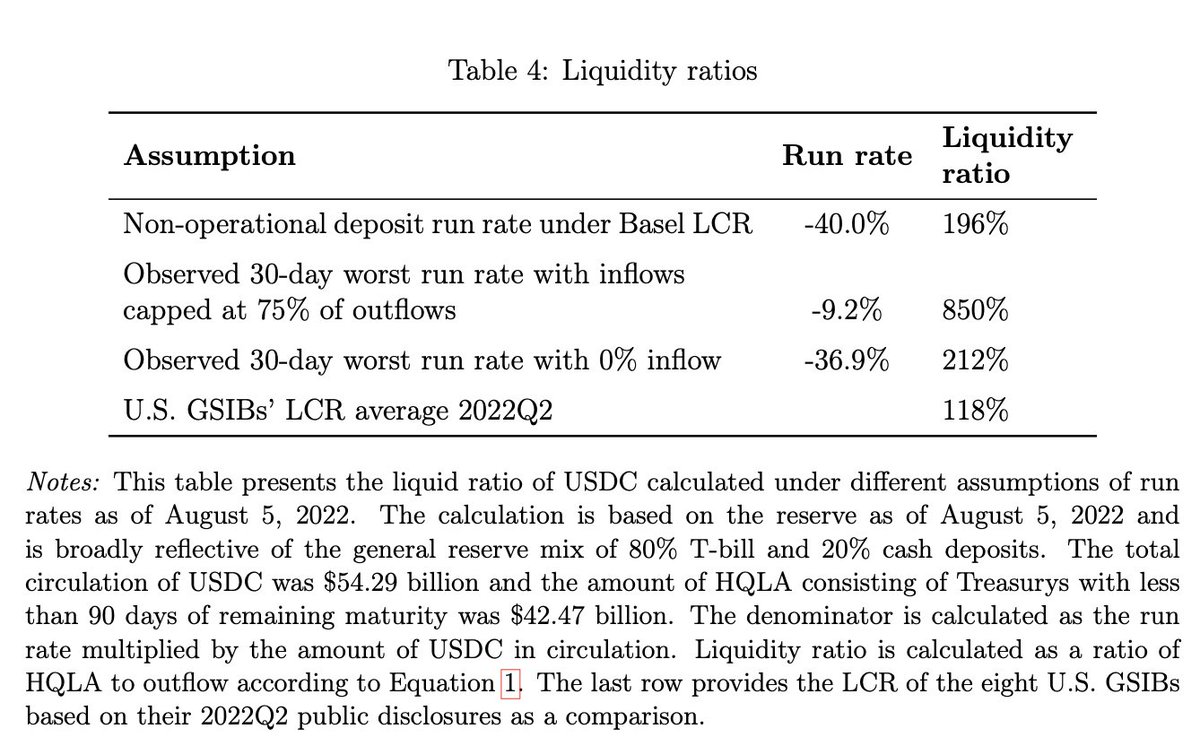

Applying the Basel framework, the liquidity ratio of the largest cash token, USDC, ranges from 196% on the low end to 850% on the high end. These liquidity ratios far exceed the typical LCR for the eight U.S. GSIBs that averaged around 118% in Q2 2022.

3/

3/

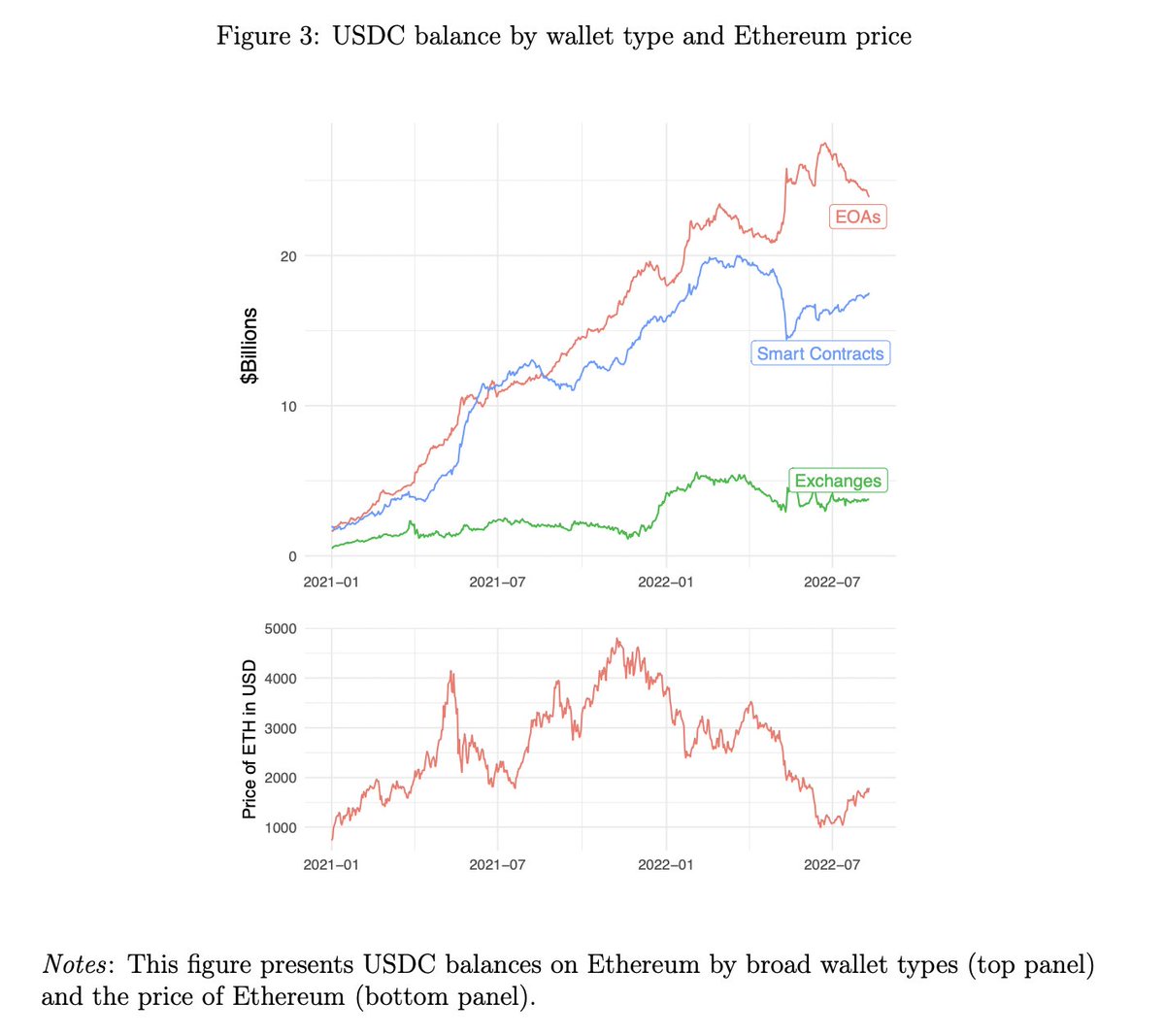

With less than 10% of USDC held on exchanges and almost no demand correlation with crypto prices, tokenized cash do not jump out as the “poker chips” at the “wild west” crypto casino.

4/

4/

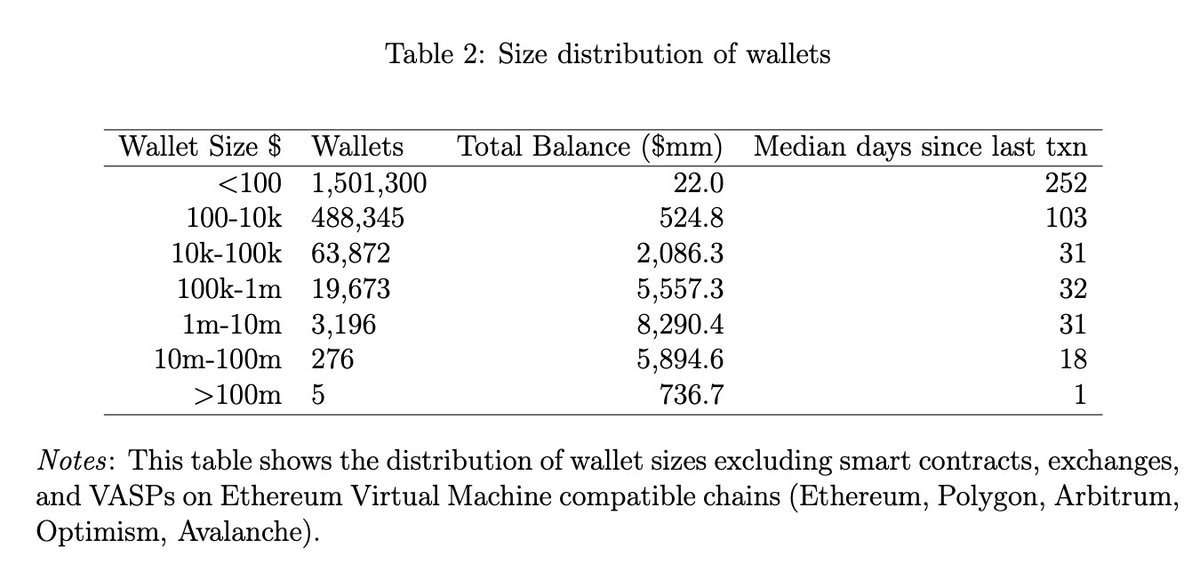

Tokenized cash are inclusive stores of value --- more than 75% of USDC-enabled wallets hold less than $100, which is less than the typical minimum balance requirements of banks.

5/

5/

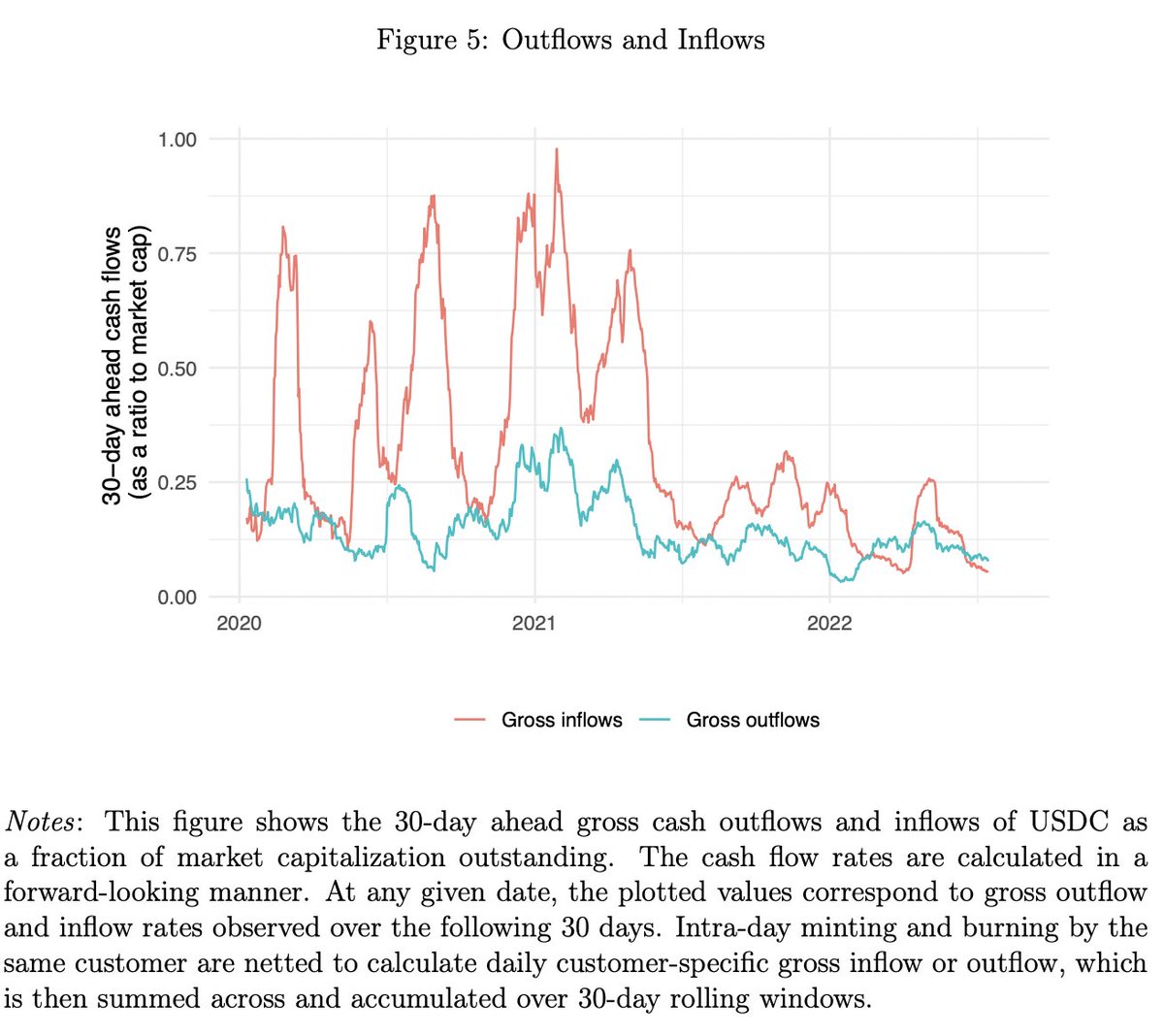

Transparency of public blockchain allows far greater information on liquidity and run risks to be monitored in real-time. This beats call reports!

6/

6/

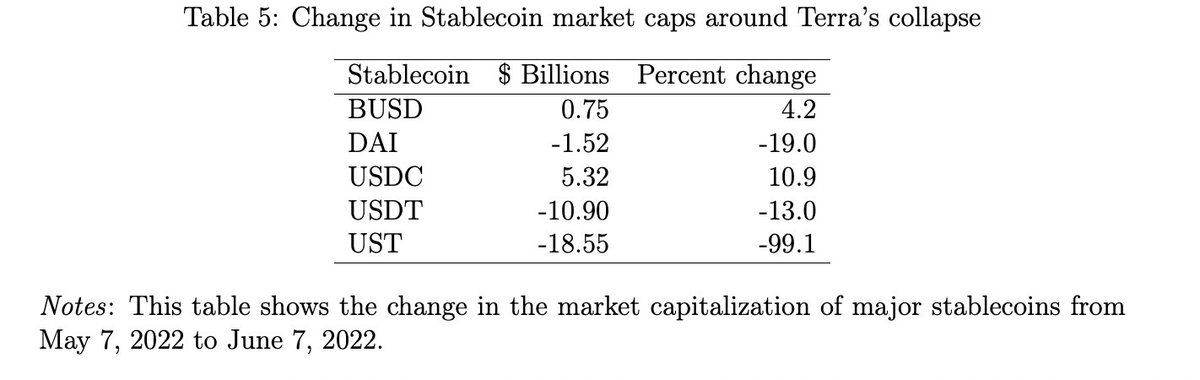

Revealed preference is often the most telling. Around Terra’s collapse, tokenized cash gained shares at the expense of other stablecoins.

7/

7/

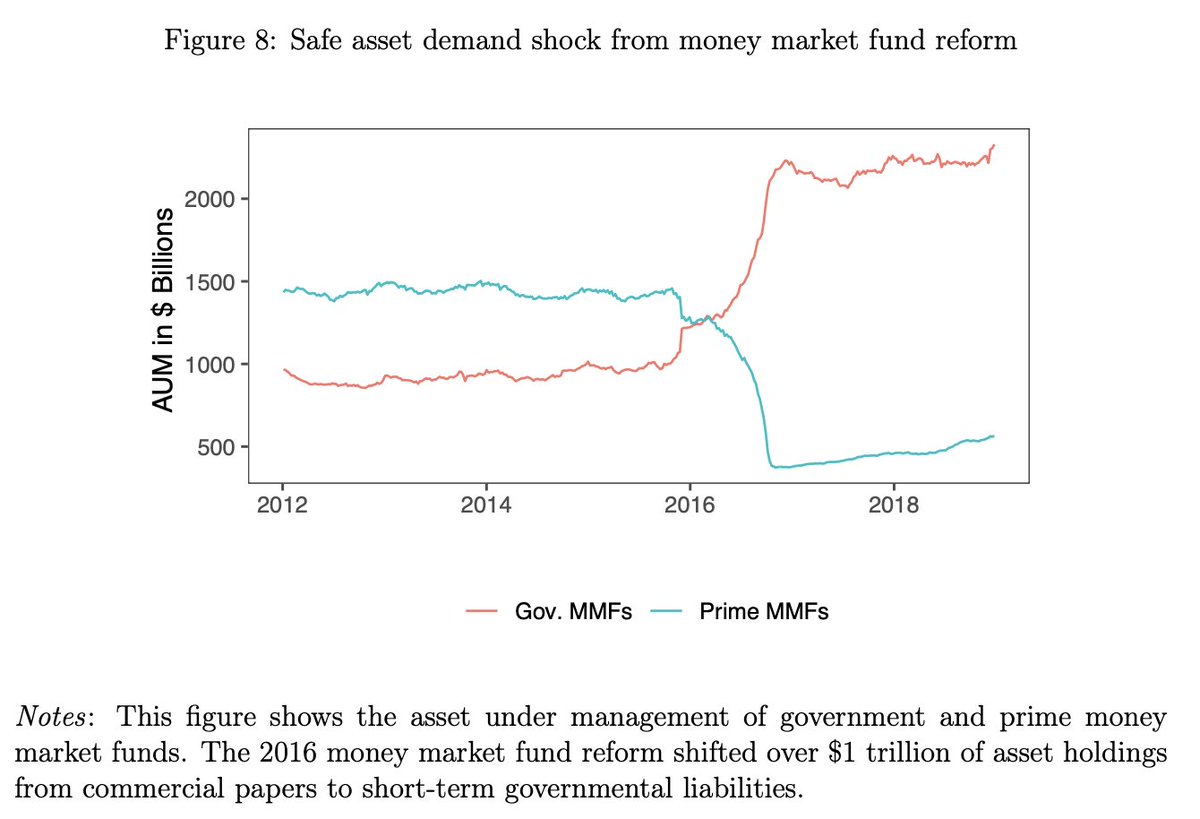

On the other extreme, the fear of stablecoins being too safe and gobbling up safe asset collaterals is over-emphasized. The 2016 money market fund reform showed that the $1 trillion Treasury demand shock from PMMF conversion caused little disruptions to safe assets and banks.

8/

8/

Deposit competition can be healthy - raising deposit rates can crowd-in cash and tighten monetary policy transmission, at the same time benefit depositors.

9/

9/

Narrow “bank” concepts are not new. Though this time, smart contracts for market-based lending can reduce the reliance on “soft information” in credit intermediation, resulting in expanded credit access. @goldfinch_fi

10/

10/

Lastly, tokenizing cash can plausibly lower overall systemic risk by reducing moral hazard in banking, limiting the excess risk-taking that are subsidized by the public.

Additional reads @DanAwrey and Pennacchio (2012)

papers.ssrn.com

papers.ssrn.com

11/11

Additional reads @DanAwrey and Pennacchio (2012)

papers.ssrn.com

papers.ssrn.com

11/11

Loading suggestions...