Clearly I've been wrong about the market recovery since Aug. The questions here are (1) what are the key drivers for forward returns over the next 3-6M, (2) what are priced in, (3) where will surprises come from, (4) the general conditions (trend/vol) & potential changes?

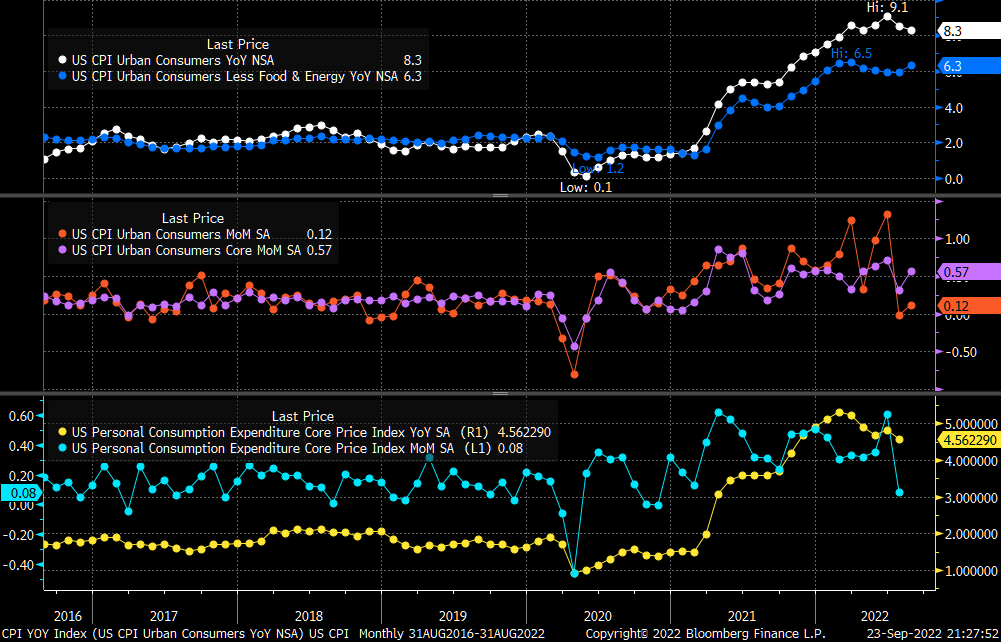

Summary of current conditions: 1) The Fed is firmly hawkish and will keep raising rates until there are clear evidence of inflation returning to its 2% target. One piece of lagging evidence is that core PCE grew 0.2% m/m over a few months, as per Brainard (h/t @aRishisays).

1/n

1/n

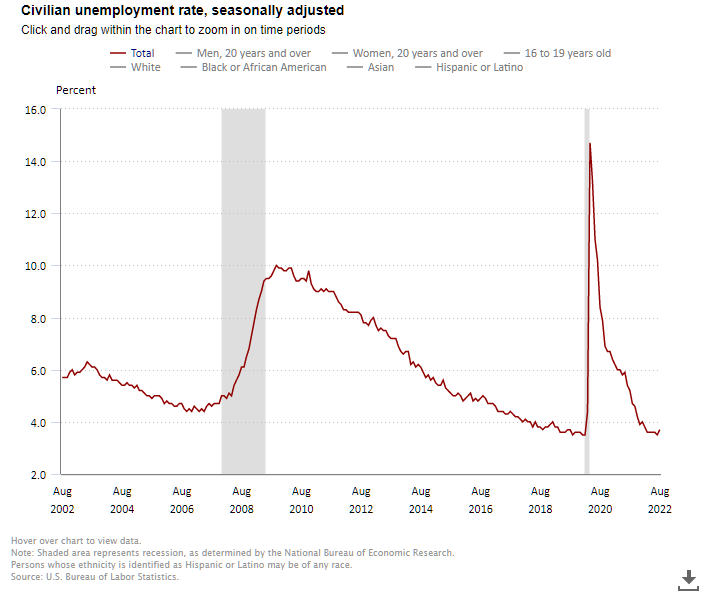

Another piece would be evidence of easing labor market conditions: falling job opening, increasing unemployment, limited wage growth. For now, inflation is too high and the labor market is too tight. However, commodity prices have been falling and should help lower headline. 2/n

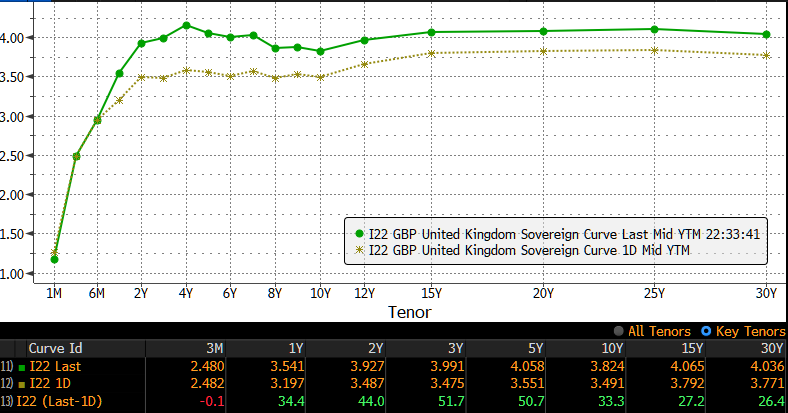

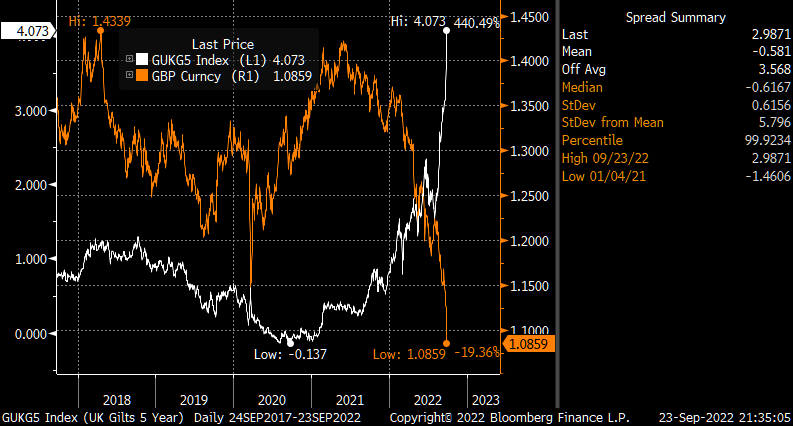

2. Global CBs are dealing with the challenges of slowing growth (and in some cases, recession) and high inflation, a situation exacerbated by US MP tightening (higher rates + stronger USD). Europe and UK are still in a bad spot, and UK today just firmly turned into an EM. 3/n

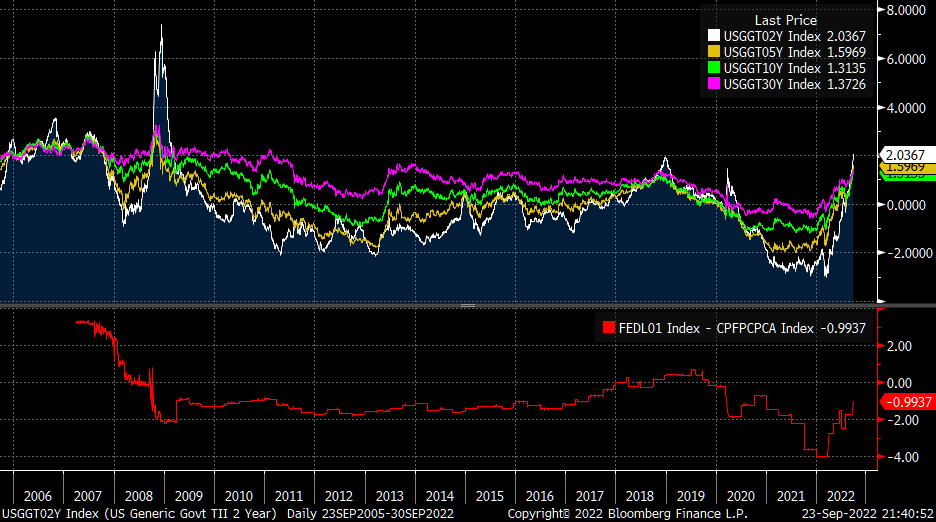

3. So now we have really tight monetary policy conditions almost everywhere. US policy rate +300bps YTD, USD sharply higher. Real yields are positive across the curve except for the ex-post. BoE is forecasting a recession, so as the EZ. Other countries are slowing as well. 4/n

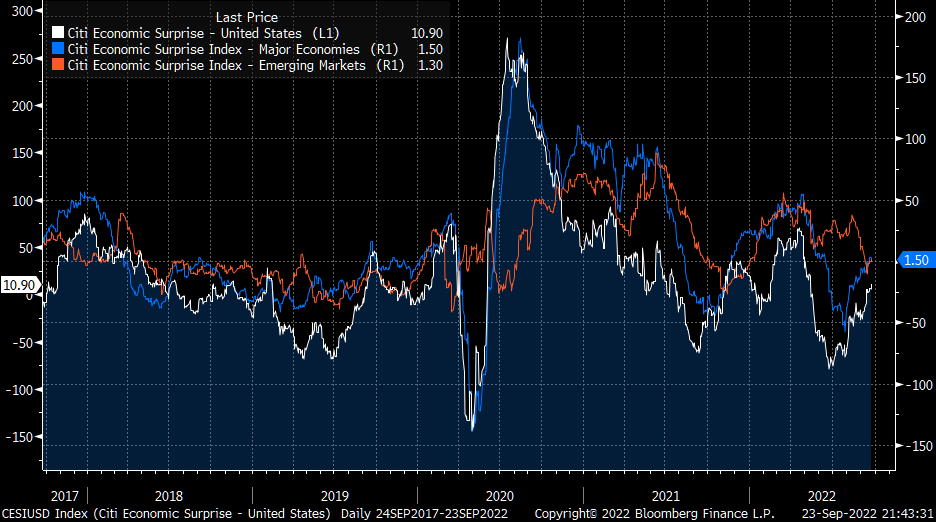

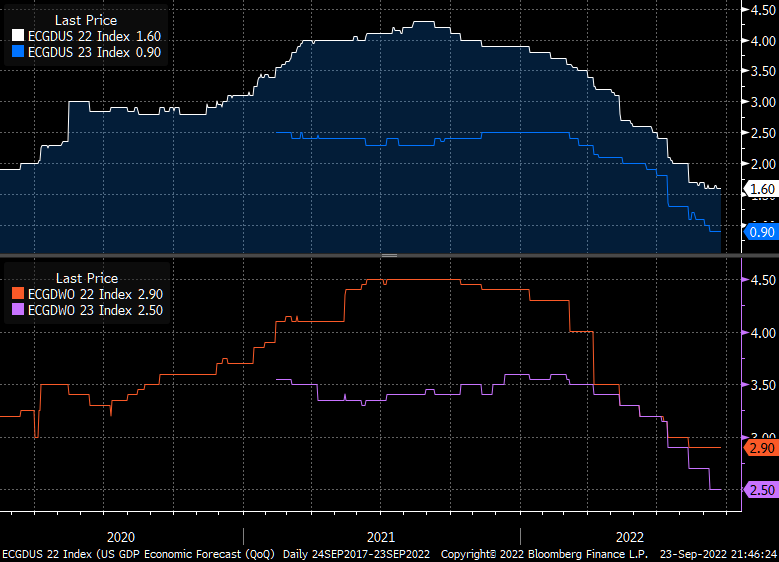

4. Recent macro data has been holding up better than lowered expectations, esp in the US. That said, growth is expected to slow in 2023, with balance of risks (consensus view) to the downside due to the cumulative impact of tightening and profit margin compression. 5/n

5. Geopolitical risks are still elevated. Russia just mobilized the country for its ongoing invasion of Ukraine. The tension in SE Asia appears to be growing. No idea about how they play out, but it is reasonable to expect higher volatility in commodities & FX markets. 6/n

Given these backdrops, how should we think about the market? What are priced in and what are the potential surprises?

No investment advice. I use this as a scrapbook to scrutinize my views and learn from others. Discussion welcome. 7/n

No investment advice. I use this as a scrapbook to scrutinize my views and learn from others. Discussion welcome. 7/n

First, let's see major market trends and sentiment.

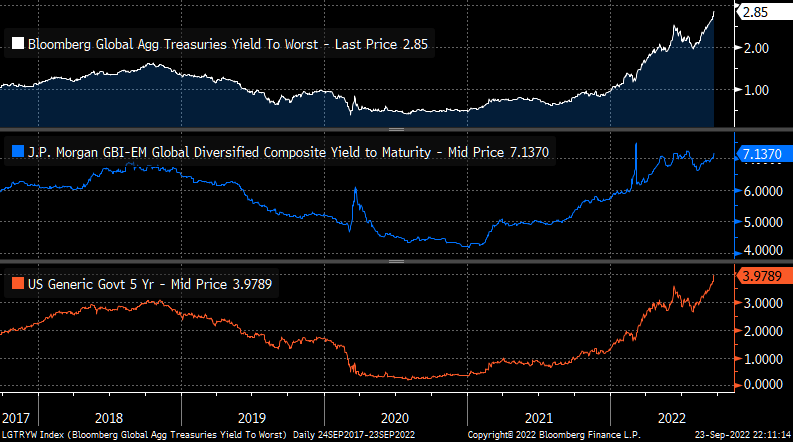

1. Rates have been exploding higher. Sentiment very bearish.

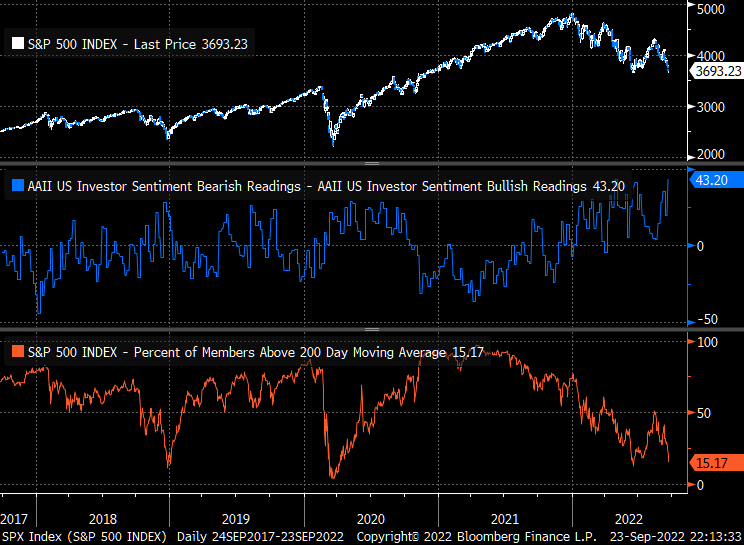

2. Equities have been sold heavily. Sentiment ST bearish.

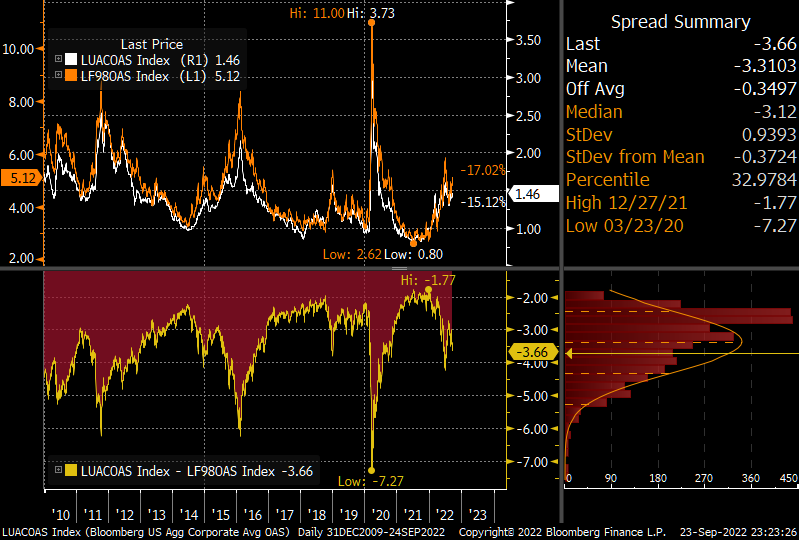

3. Credit spreads are wider and cross asset volatility are high.

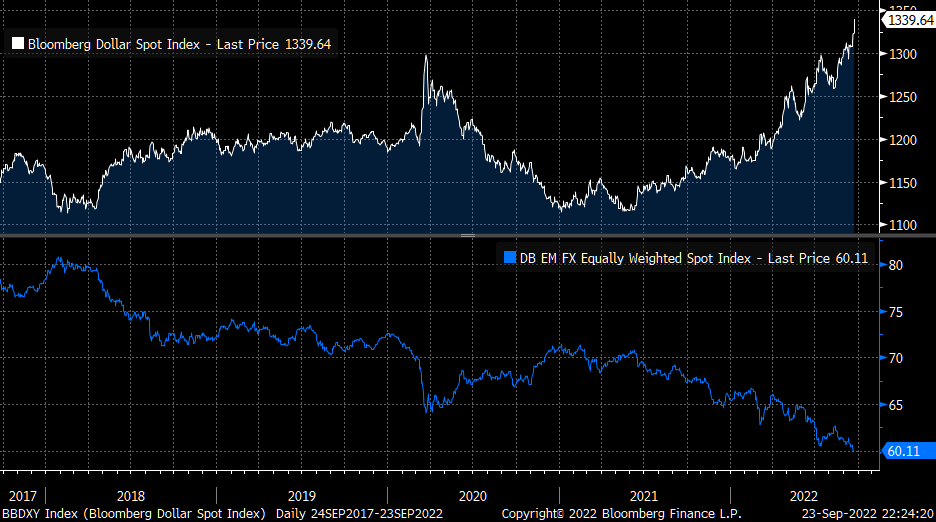

4. USD has been appreciating sharply.

8/n

1. Rates have been exploding higher. Sentiment very bearish.

2. Equities have been sold heavily. Sentiment ST bearish.

3. Credit spreads are wider and cross asset volatility are high.

4. USD has been appreciating sharply.

8/n

So we could reasonably say that (1) MP, Fed especially, is driving the bus, and (2) the market is pricing in a good slowdown, if not a recession, in the US based on credit spreads and equity drawdowns, (3) the market is pricing in things breaking in EMs (that includes UK). 9/n

These are the trends, and the expectations for their fundamentals will predominantly be tied back to the US monetary policy unless they can prove themselves being resilient to the major driving force. 10/n

For rates to rally, we need the Fed to slow down. There are idiosyncratic EM stories that can be multi-year trades, but they won't be immune near-term. For the Fed to slow down, we know we need inflation to come down, preferably quickly, otherwise things will break, badly 11/n

Will there be surprises for rates? Yes, with inflationary pressure and labor market easing. Commodities prices have been falling, even for stuff with supply issues. The US housing market is shot. Global growth slows (FedEx guidance). Poor business sentiment... 12/n

What about upside risks? Shelter inflation will likely keep core elevated, and the Fed ignores the other stuff as long as the unemployment rate is still low. We may get more supply shocks. That said, giving the current Fed pricing, the asymmetry looks better for rates. 13/n

Equities are now back to pricing in a shallow recession. Hard landing is a substantial risk as earnings contract, and flows look better for rates. Easing geopolitical and Fed concerns are upside risks given the positioning. Fundamentals may be more resilient than thought. 14/n

Credits are priced attractively if we can avoid a hard landing, similar to the case of equities. Also, one has to ask, what unleashed the animal spirit after the tightening in the early 90s even with things blowing up left and right later. 15/n

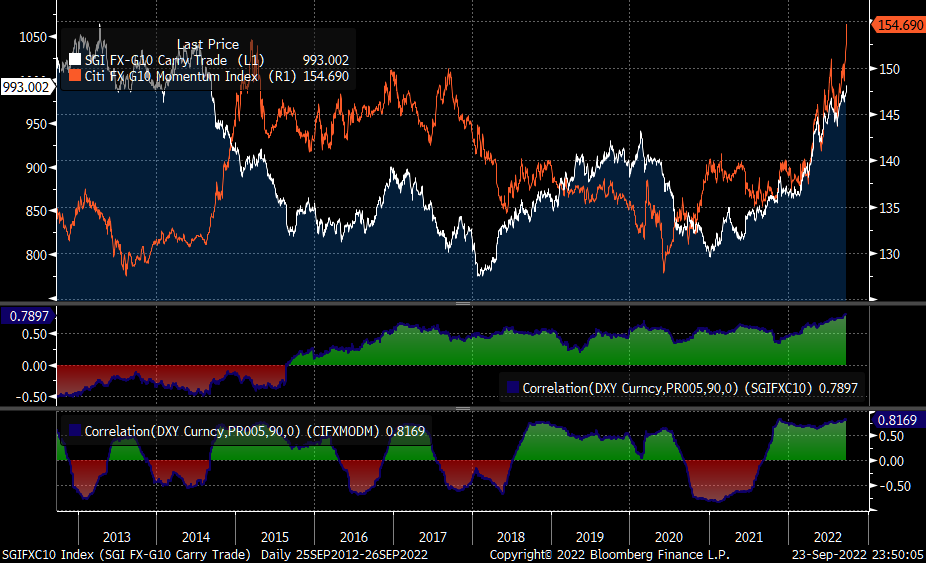

FX is mostly a rate trade atm. Until the Fed pricing stabilizes or eases, traders will keep pressing the same trade: positive USD carry/momentum. Interventions will not work unless it is also coordinated with the US and the Fed will likely have backed off then. 16/n

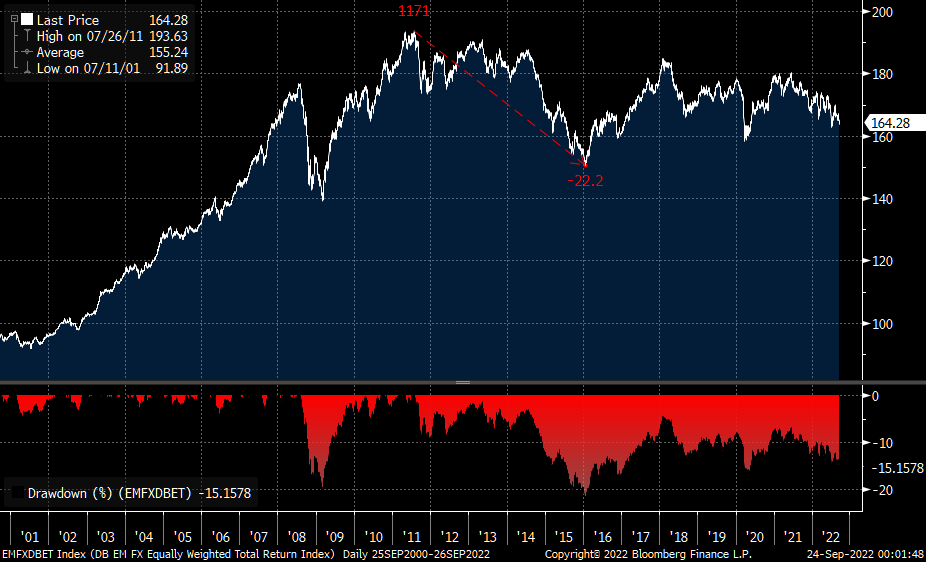

EMFX performance has been very weak. EMFX may work once USD turns. Broadly speaking, not a lot of tailwinds, there are a few good ones with positive structural stories or improving fundamentals and cheap starting valuation. One can do well with EM crosses. Tough one. 17/n

So what do you think about the macro outlook? What things (catalysts, recognition of overlooked data) you can think of that will durably change the current trend? (fin)

Potential bull case. (h/t @aRishisays for this find).

Loading suggestions...