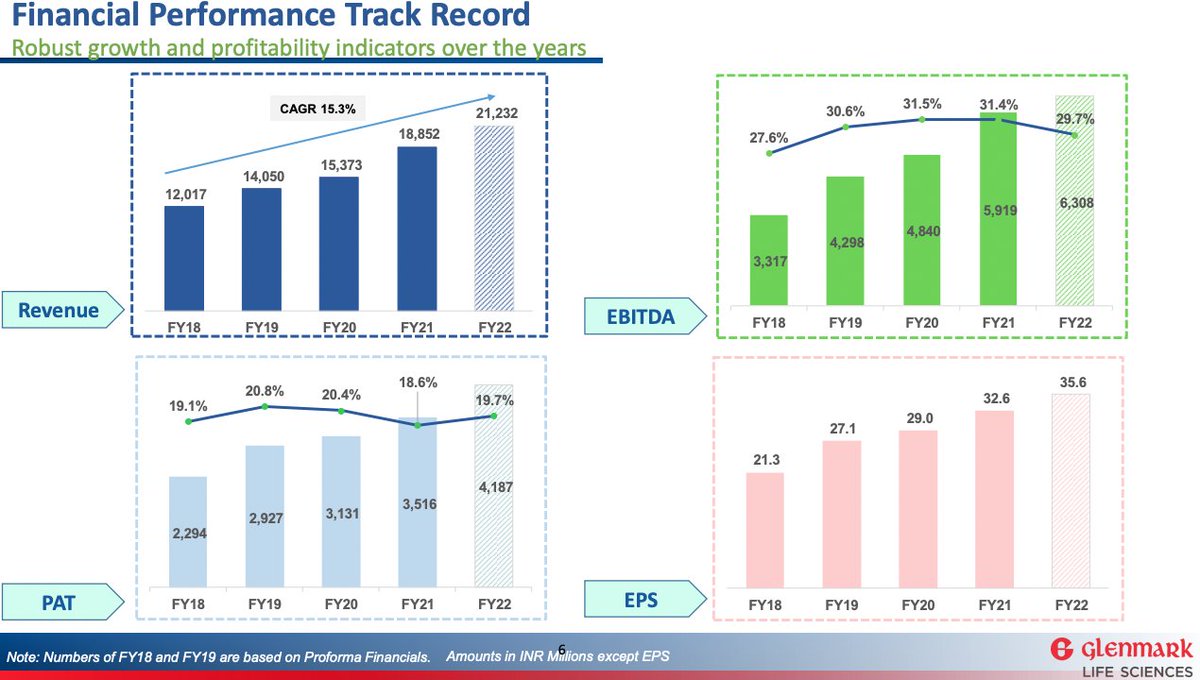

Glenmark Life Sciences is now a too-cheap-to-ignore story 🚀

7x TTM EV/EBITDA, Next year (FY24) -> it will be much lower!

The Narratives of

1. Glenmark's dependence on its parent company

2. The parent's past capital misallocation

will perish with the higher prices 🖋️

7x TTM EV/EBITDA, Next year (FY24) -> it will be much lower!

The Narratives of

1. Glenmark's dependence on its parent company

2. The parent's past capital misallocation

will perish with the higher prices 🖋️

1/ My notes from their IPO.

Looked interesting then, now with a 50% price correction; the risk reward is a lot better ✨

Looked interesting then, now with a 50% price correction; the risk reward is a lot better ✨

2/ "Have added complex molecules with an even higher entry barrier, from a chemistry perspective & a characterization perspective." ~ FY22

1st wave of APIs: Speed to market (26 in dev)

2nd wave of APIs: Cost improvement projects

All capacities -> Multipurpose with ZLD 👀

1st wave of APIs: Speed to market (26 in dev)

2nd wave of APIs: Cost improvement projects

All capacities -> Multipurpose with ZLD 👀

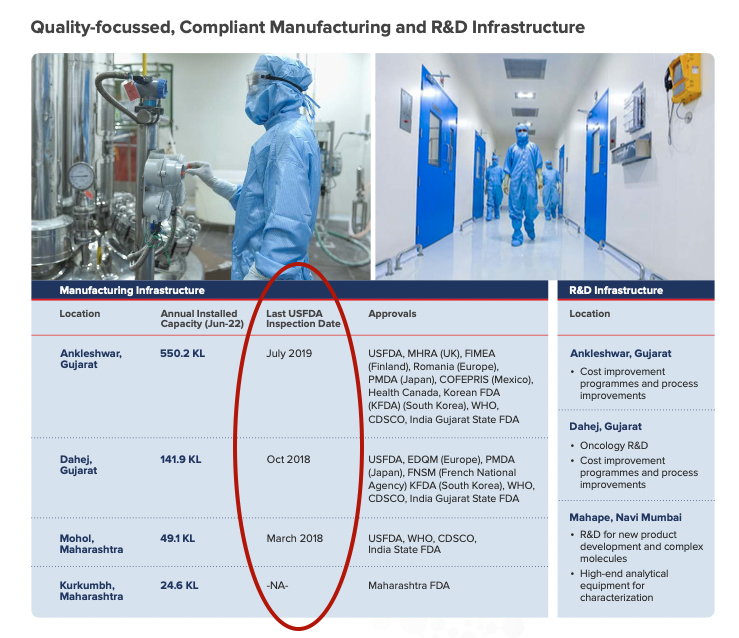

3/ The biggest risk is the next leg of USFDA visits to their various facilities: should happen over the next 1-2 years (Photo 1)

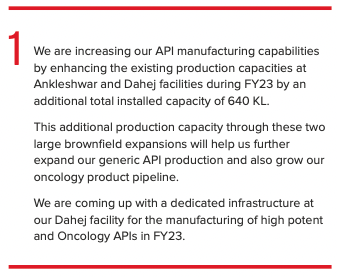

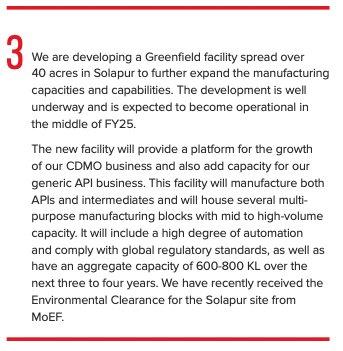

Capacity additions in 3 stages will trigger that (Photos 2-4)

Capacity additions in 3 stages will trigger that (Photos 2-4)

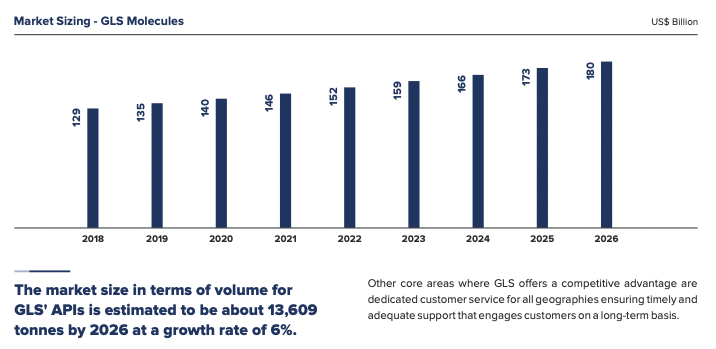

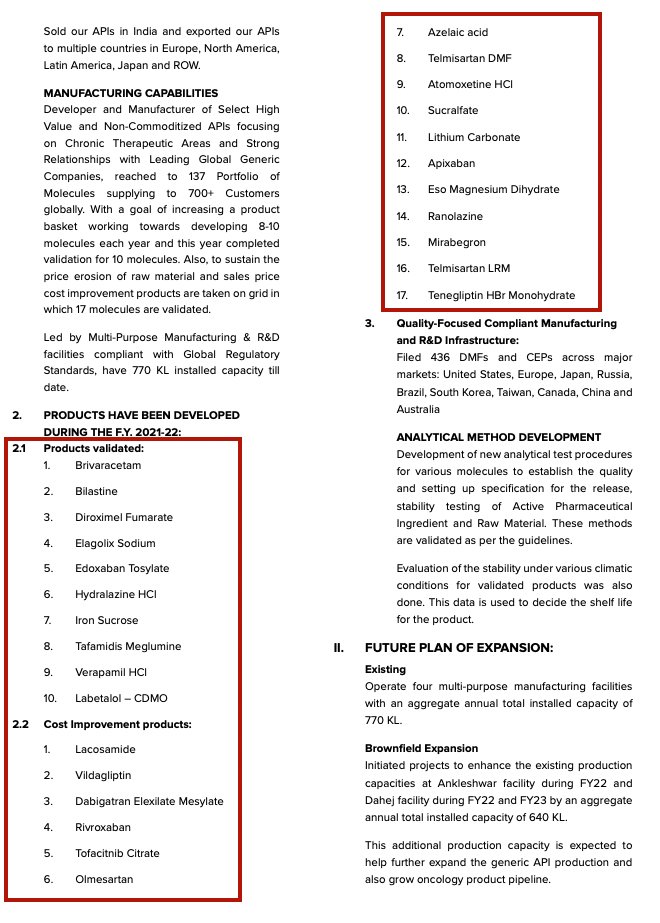

4/ Expanding TAM by 8-10 products every year.

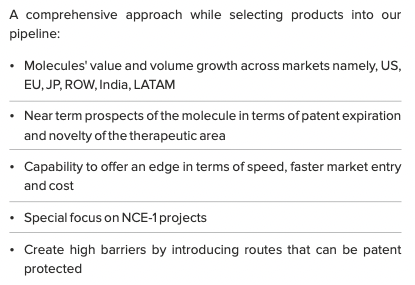

The process to decide which molecules to go for 👇

10 new products got validated in FY22 & 17 went for cost improvement; the names are in photo 3 (Too much transparency? @unseenvalue)

The process to decide which molecules to go for 👇

10 new products got validated in FY22 & 17 went for cost improvement; the names are in photo 3 (Too much transparency? @unseenvalue)

Loading suggestions...