There is so much going on in financial markets around the world.

And as most of it is actually happening outside the US, it can easily get overlooked.

A global macro thread.

1/

And as most of it is actually happening outside the US, it can easily get overlooked.

A global macro thread.

1/

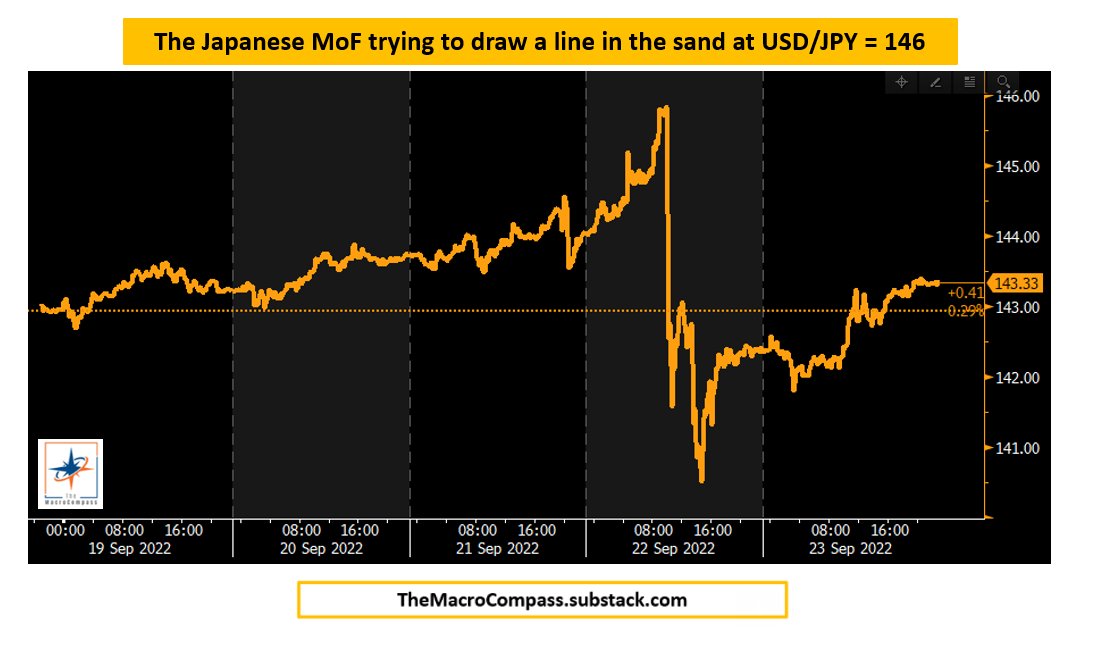

Let's start from Japan.

Last week, Japanese authorities intervened to try and draw a line in the sand in USDJPY at roughly 146.

How does this exactly work, and will they succeed?

2/

Last week, Japanese authorities intervened to try and draw a line in the sand in USDJPY at roughly 146.

How does this exactly work, and will they succeed?

2/

Japan has accumulated $1.2 trillion in FX reserves, roughly split as follows:

- $1.0 trillion in foreign securities (mostly USD & EUR bonds)

- $0.2 trillion in deposits at foreign Central Banks or invested in FX derivatives (mostly to lend $)

3/

- $1.0 trillion in foreign securities (mostly USD & EUR bonds)

- $0.2 trillion in deposits at foreign Central Banks or invested in FX derivatives (mostly to lend $)

3/

Despite all the excitement, the first step is not to sell bonds but to deploy the $$$ sitting in foreign Central Banks accounts and FX derivatives - it's not a small amount.

Why?

Two main reasons.

4/

Why?

Two main reasons.

4/

A) Selling bonds here often pushes a Central Bank loss from ''unrealized'' into a proper P&L loss - accounting magic in reverse...

B) Bonds can be used as collateral to get $$$ funding (e.g. from the Fed), and selling them in size can be geopolitically tricky too

5/

B) Bonds can be used as collateral to get $$$ funding (e.g. from the Fed), and selling them in size can be geopolitically tricky too

5/

In any case, Japan has been selling US Dollars to prop up the Yen: will it work?

Unless a combo of global inflation slowdown, yield differentials collapse & friendlier energy prices materializes...in the long term: no

But it achieves something: it deters short Yen positions

6/

Unless a combo of global inflation slowdown, yield differentials collapse & friendlier energy prices materializes...in the long term: no

But it achieves something: it deters short Yen positions

6/

Long USD/JPY was a positive carry trade with unlimited upside backed by clear macro momentum dictated by fundamentals: terrible JPY terms of trades (energy imports etc), rates differentials etc.

A macro investor dream.

Now, the MoF is telling you they'll stop you out.

7/

A macro investor dream.

Now, the MoF is telling you they'll stop you out.

7/

Short JPY (and not Japanese bonds) was the clear release valve for the dissonant BoJ policy: why?

Because shorting bonds (still) is a negative carry trade - you must pay to be in the trade and wait until the BoJ gives up.

But actually: will the BoJ give up, and when?

8/

Because shorting bonds (still) is a negative carry trade - you must pay to be in the trade and wait until the BoJ gives up.

But actually: will the BoJ give up, and when?

8/

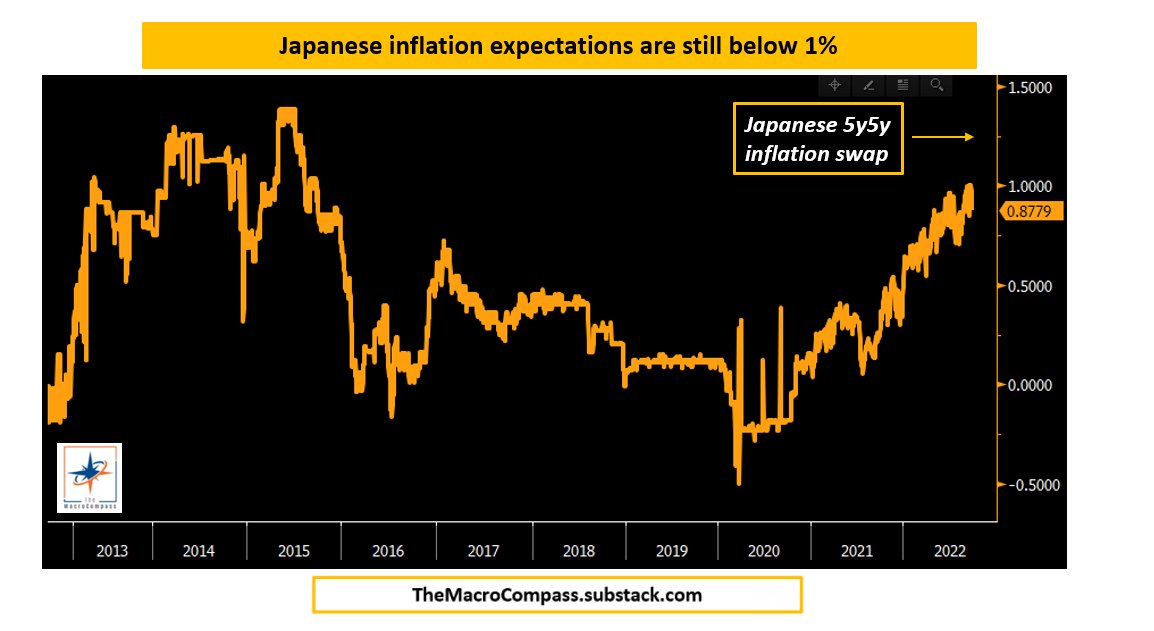

For the last decade:

- Japanese core inflation has averaged 0.2%

- 5y5y inflation swaps have averaged 0.5%

Kuroda has miserably failed in achieving the 2% target, and his term ends in April 2023

Incentive schemes are important - there will be BoJ resistance for a bit more

9/

- Japanese core inflation has averaged 0.2%

- 5y5y inflation swaps have averaged 0.5%

Kuroda has miserably failed in achieving the 2% target, and his term ends in April 2023

Incentive schemes are important - there will be BoJ resistance for a bit more

9/

Moving to another interesting country: Switzerland

In their attempt to weaken the CHF, the Swiss have accumulated roughly $900 bn (>120% of GDP!) in foreign reserves over time

But contrary to the BoJ, the SNB is a very orthodox Central Bank

Inflation above target? Hike.

10/

In their attempt to weaken the CHF, the Swiss have accumulated roughly $900 bn (>120% of GDP!) in foreign reserves over time

But contrary to the BoJ, the SNB is a very orthodox Central Bank

Inflation above target? Hike.

10/

This orthodox monetary policy reaction function coupled with the outsized amount of FX reserves has sheltered a bit the CHF from the USD wrecking ball.

But the Swiss will be selling FX reserves to prop up the CHF anyway.

So, what's in their $900 bn portfolio?

11/

But the Swiss will be selling FX reserves to prop up the CHF anyway.

So, what's in their $900 bn portfolio?

11/

The five largest holdings are:

- $225 bn in global equities (mostly US)

- $200 bn in US bonds

- $200 bn in EUR bonds

- $100 bn in deposits at foreign Central Banks (or BIS)

- $50 bn in gold

Also here: cash at foreign CBs first, but these equities and EUR bond holdings...

12/

- $225 bn in global equities (mostly US)

- $200 bn in US bonds

- $200 bn in EUR bonds

- $100 bn in deposits at foreign Central Banks (or BIS)

- $50 bn in gold

Also here: cash at foreign CBs first, but these equities and EUR bond holdings...

12/

Europe is by far Switzerland's largest trading partner, and EUR/CHF is very important for Swiss policymakers when steering CPI and inflation expectations => sell EUR => additional pressure on German government bonds?

Also, in today's macro environment the SNB must be...

13/

Also, in today's macro environment the SNB must be...

13/

...thinking about their large equity exposure.

In general, I really like Long CHF/EUR here:

- Better terms of trade

- A much more (credibly) orthodox SNB vs ECB

- Idiosyncratic issues in Europe (e.g. Italy)

It's gone parabolic, but it could be a good macro trending trade.

14/

In general, I really like Long CHF/EUR here:

- Better terms of trade

- A much more (credibly) orthodox SNB vs ECB

- Idiosyncratic issues in Europe (e.g. Italy)

It's gone parabolic, but it could be a good macro trending trade.

14/

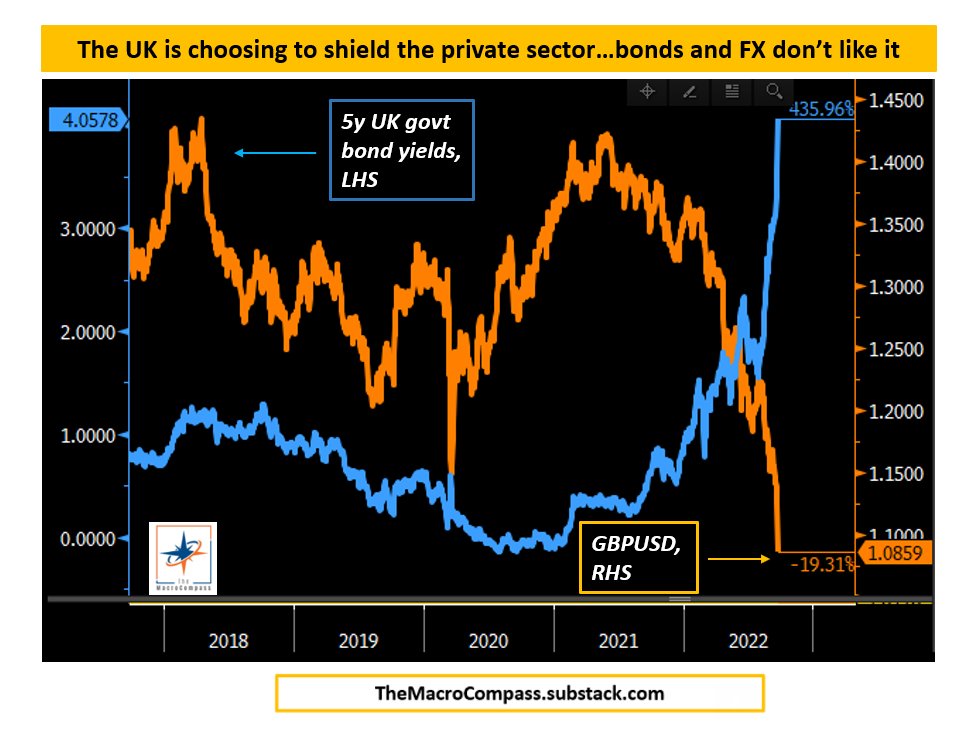

Now, a word about the UK.

The 5% drawdown in the Sterling vs USD we experienced over the last month ranks as a very large volatility-adjusted move.

The UK is (as many other countries) going through a EM-like external shock - it just got worse with the last fiscal news.

15/

The 5% drawdown in the Sterling vs USD we experienced over the last month ranks as a very large volatility-adjusted move.

The UK is (as many other countries) going through a EM-like external shock - it just got worse with the last fiscal news.

15/

The UK is very dependent on stuff coming from the outside - goods, energy and so on.

When exogenous shocks hit (e.g. wars), there is not much policymakers can do to fix the problem straight away - you can print GBP, but not economic inputs.

The EM experience says...

16/

When exogenous shocks hit (e.g. wars), there is not much policymakers can do to fix the problem straight away - you can print GBP, but not economic inputs.

The EM experience says...

16/

...the typical responses are:

- Tighten up and go through some pain: very positive real rates, private sector deleveraging, fiscal austerity and some currency weakness => very painful

- Use the govt balance sheet to shield the private sector => FX & bonds down, BOTH!

17/

- Tighten up and go through some pain: very positive real rates, private sector deleveraging, fiscal austerity and some currency weakness => very painful

- Use the govt balance sheet to shield the private sector => FX & bonds down, BOTH!

17/

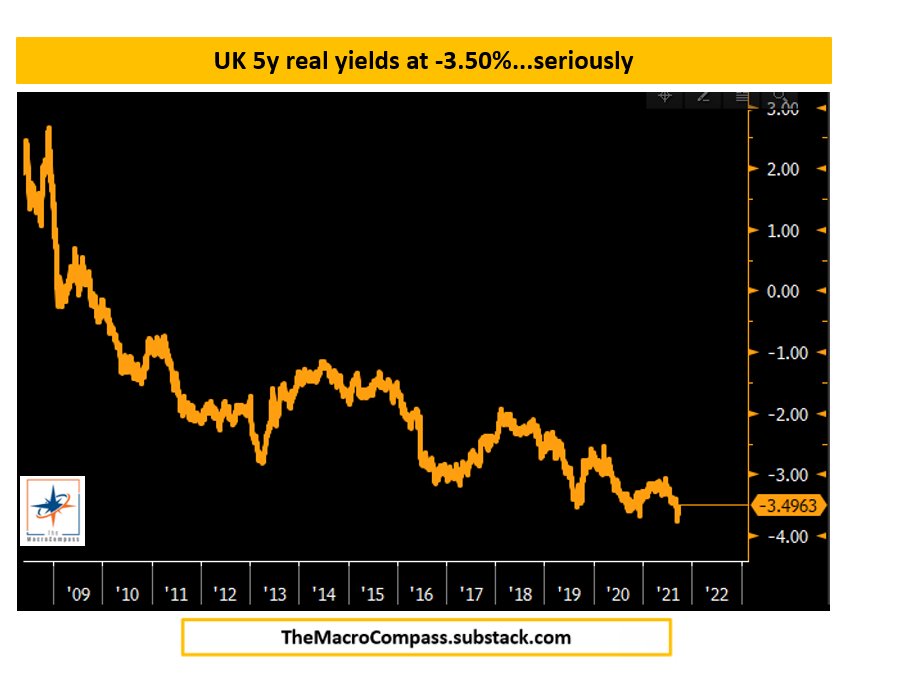

The market is giving very clear signals that it won't be happy to fund the UK’s external deficit position at today's real yields or FX levels.

Hence it's going to force real yields higher and FX down.

Look at where 5y UK real yields are...

18/

Hence it's going to force real yields higher and FX down.

Look at where 5y UK real yields are...

18/

This won't stop until real yields reach decent levels and/or FX depreciates massively.

The only alternative escape routes are:

- More orthodox policymaking

- A configuration of slowing CPI and cheaper input costs (e.g. luck)

Not only a UK situation, btw...

19/

The only alternative escape routes are:

- More orthodox policymaking

- A configuration of slowing CPI and cheaper input costs (e.g. luck)

Not only a UK situation, btw...

19/

In general, there is a huge amount of systemically important macro developments going on around the world.

This is the time to also look beyond the EU and US.

Japan, Switzerland and the UK were only 3 examples: have a look at the Chinese real estate market for instance.

20/

This is the time to also look beyond the EU and US.

Japan, Switzerland and the UK were only 3 examples: have a look at the Chinese real estate market for instance.

20/

I often discuss ongoing market developments, but very rarely do deep dives into my general framework

Last week, I recorded a video interview with @ChrisWeston_PS that goes through my macro framework, trade/portfolio construction process and risk management approach

Where?

21/

Last week, I recorded a video interview with @ChrisWeston_PS that goes through my macro framework, trade/portfolio construction process and risk management approach

Where?

21/

The link to access this interview is here: bit.ly

It's totally free, by the way!

The short clip below is a small excerpt :)

22/

It's totally free, by the way!

The short clip below is a small excerpt :)

22/

Markets are a never-ending learning journey.

The Macro Compass is my (free!) platform where I go the extra mile to share macro insights & investment ideas with over 96,000 investors.

I also reply to every single comment & question in there!

If you want to have a look...

23/

The Macro Compass is my (free!) platform where I go the extra mile to share macro insights & investment ideas with over 96,000 investors.

I also reply to every single comment & question in there!

If you want to have a look...

23/

...this is the link: TheMacroCompass.substack.com.

Next week I'll release a piece covering more global macro developments and releasing some trade and portfolio allocation ideas.

Consider subscribing so you'll receive it directly in your inbox.

It's free!

24/24

Next week I'll release a piece covering more global macro developments and releasing some trade and portfolio allocation ideas.

Consider subscribing so you'll receive it directly in your inbox.

It's free!

24/24

Loading suggestions...