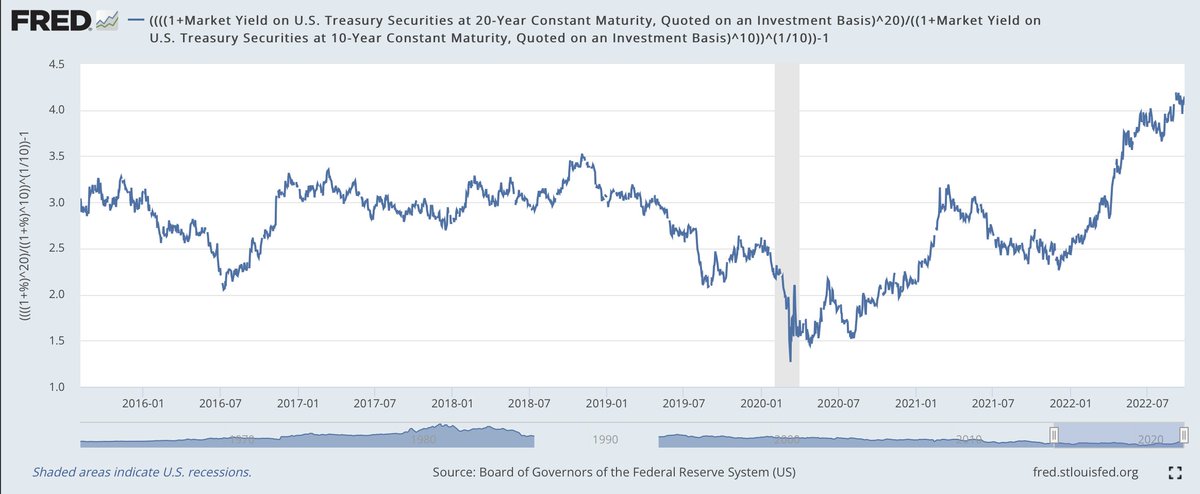

Just checked the 10yr/10yr Treasury rate (ie, the markets forecast of the 10yr rate a decade from now).

Is 4.33%.

That is up 19bp in a day (largest 1 day increase in over a year).

Up 28bp in 2 days (largest tw2o day increase in over two years).

(FYI FRED doesn't have today.)

Is 4.33%.

That is up 19bp in a day (largest 1 day increase in over a year).

Up 28bp in 2 days (largest tw2o day increase in over two years).

(FYI FRED doesn't have today.)

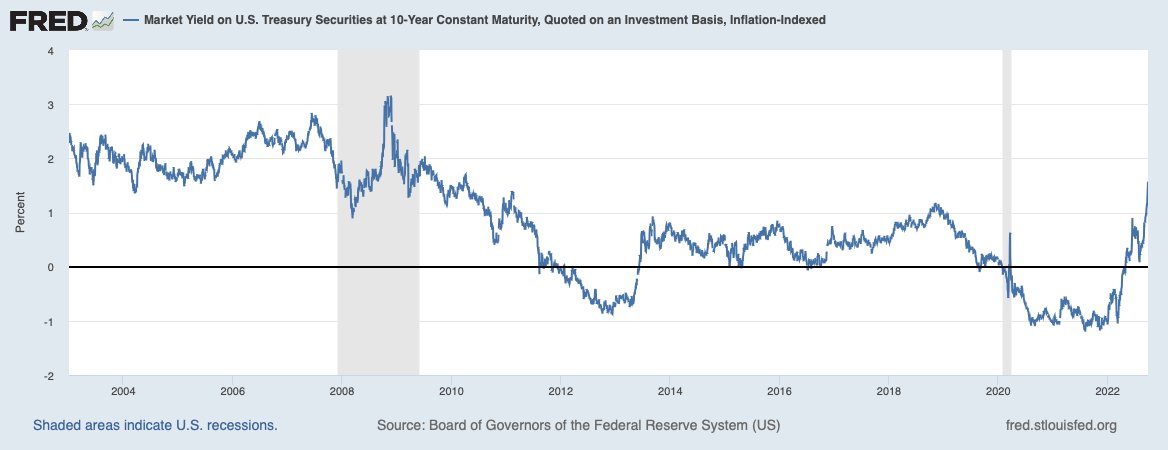

The real rate implied by TIPS is also very high: 1.60%. That would exceed real rates any time since the end of the financial crisis. If you multiple it by debt>100% of GDP would result in real net interest at worrying levels.

For most the last decade+ economic forecasts of the 10yr Treasury (nominal & real) were higher than what you would infer from the market pricing of the 10yr/10yr rate. I usually thought that a mistake & too pessimistic--was an argument I would make in doing the Admin's forecast.

Now I'm worried in the opposite direction--that budget models have not caught up with the likely path of interest rates even after the Fed is done with tightening. CBO has 3.8% and Treasury has 3.4%. Raising those to market forecasts would mean more interest, deficits & debt.

It also means we're close to the neighborhood where r > g on a forward basis (maybe not there yet because short rates are still lower and the government borrows at a duration less than ten years). So less room to run primary budget deficits--and perhaps no room--if this keeps up.

Loading suggestions...