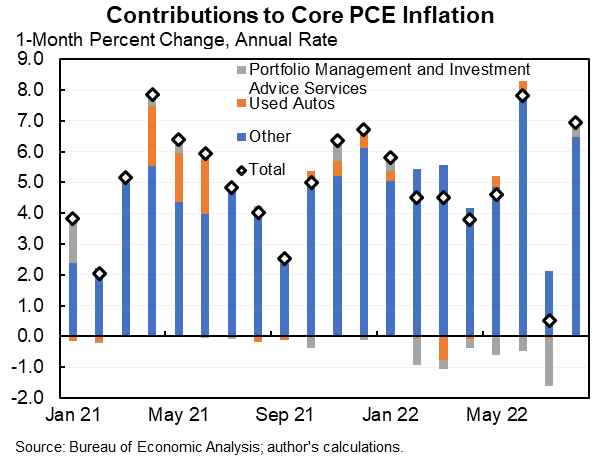

After a hiatus in July core PCE inflation snapped back to its third highest monthly value of this inflationary episode in August--0.6% or a 7.0% annual rate.

Always better to smooth, over three months is a 5.0% annual rate.

Always better to smooth, over three months is a 5.0% annual rate.

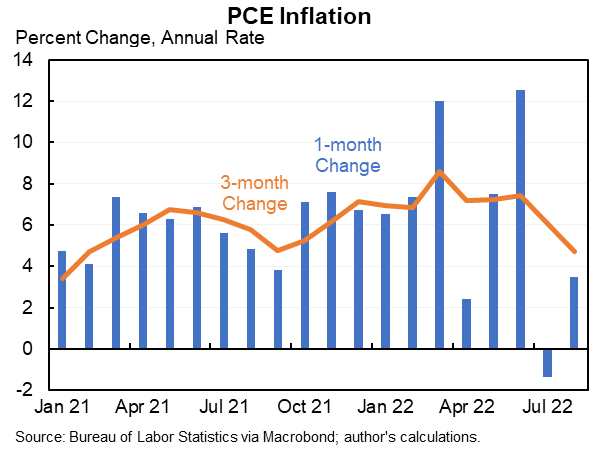

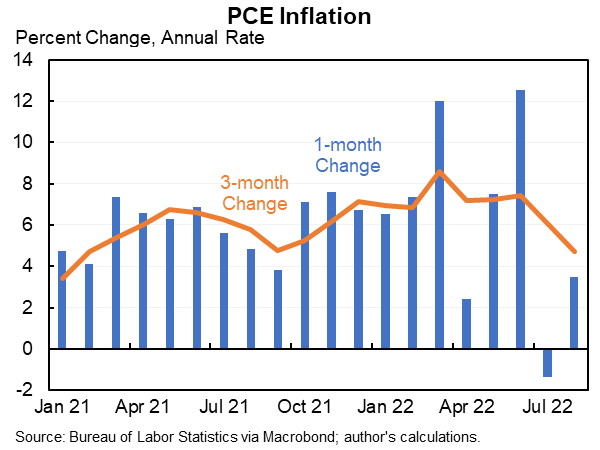

Here is what overall inflation PCE inflation looks like. Up 0.3% in August or a 3.5% annual rate--which is way above the Fed's target even though energy prices fell sharply in August at a pace that will not continue indefinitely.

Over the last three months is a 4.7% annual rate.

Over the last three months is a 4.7% annual rate.

Note one special factor holding price growth down last month was portfolio management and investment advice services. The price of that rose in August (as the market rose). Will fall again in August.

Overall surprises a bit to the upside. But what is so tough about it (like the August CPI) is that it obliterates the excuse that elevated core inflation was entirely or even much the result of the Russian invasion. Even with rapidly falling energy prices core is still very high.

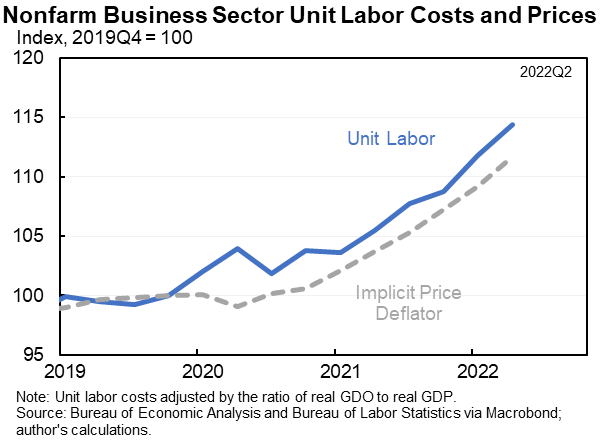

Why is core inflation so high? Because labor markets are very tight and nominal wages are rising very quickly. If wages/compensation keeps rising at a 5.5% annual rate it is extremely unlikely that price inflation will be below 4%.

In fact, if anything, prices have not grown as much as labor costs (compensation adjusted for productivity). So it is possible/plausible that we'll see more price growth to catch up with the wage growth to date.

See my adjusted ULC figure based on yesterday's GDP/GDI revisions.

See my adjusted ULC figure based on yesterday's GDP/GDI revisions.

Loading suggestions...