Fed pivot my a*s.

Let's look at the US labor market report and its implications for the Fed and markets.

A thread.

1/

Let's look at the US labor market report and its implications for the Fed and markets.

A thread.

1/

Let's start with some data.

The US added 263k jobs last month.

The trend in job creation is moving donwardws, but the 3m moving average remains very robust at +370k.

For inflationary pressures to ease, this number needs to move down to the 100-125k area.

2/

The US added 263k jobs last month.

The trend in job creation is moving donwardws, but the 3m moving average remains very robust at +370k.

For inflationary pressures to ease, this number needs to move down to the 100-125k area.

2/

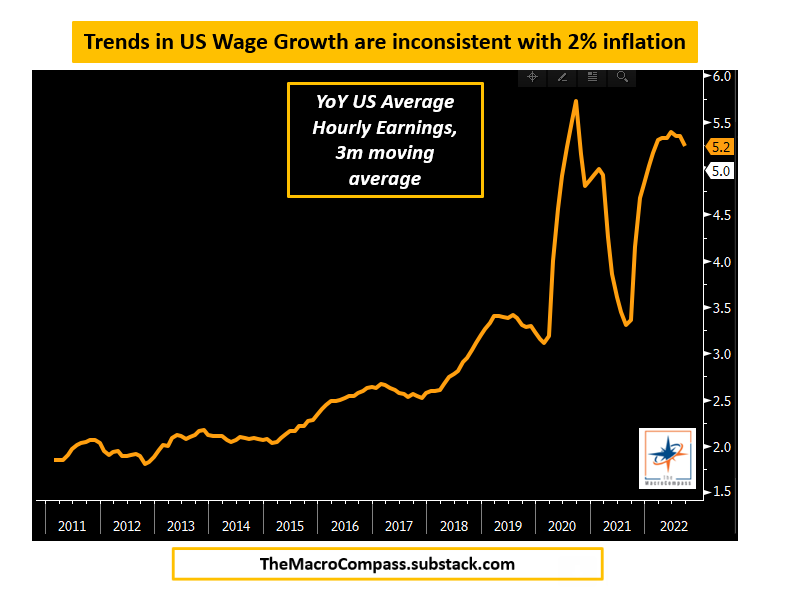

This is very visible in wage growth, which remains way too high for the Fed to hit its 2% inflation target.

Also here the trend seems to move in the right direction, but YoY wage increases north of 5% are not going to tame inflation.

A 3%-ish figure is needed here.

3/

Also here the trend seems to move in the right direction, but YoY wage increases north of 5% are not going to tame inflation.

A 3%-ish figure is needed here.

3/

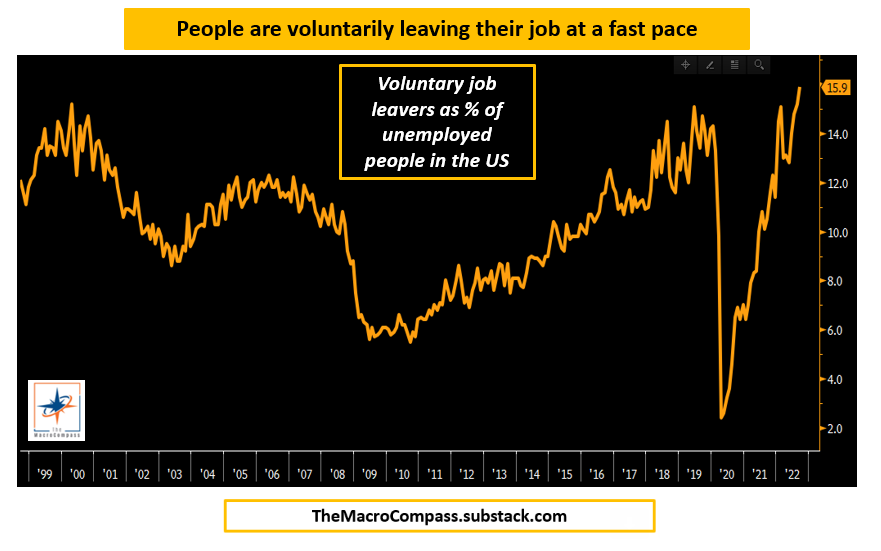

One of the reasons why wage growth remains stubbornly high is that people feel very confident in quitting and get a higher paid job elsewhere

Please notice how this % was very elevated in 2000 and 2007 as well - things can quickly turn in the labor market, but not there yet

4/

Please notice how this % was very elevated in 2000 and 2007 as well - things can quickly turn in the labor market, but not there yet

4/

Both the narrow and broad definitions of unemployment saw a drop, too!

So, was it all this strong?

As always, the devil is in the details

Most of the drop in unemployment rate was not due to large additional employment creation, but to a shrinking labor force

Yes, again!

5/

So, was it all this strong?

As always, the devil is in the details

Most of the drop in unemployment rate was not due to large additional employment creation, but to a shrinking labor force

Yes, again!

5/

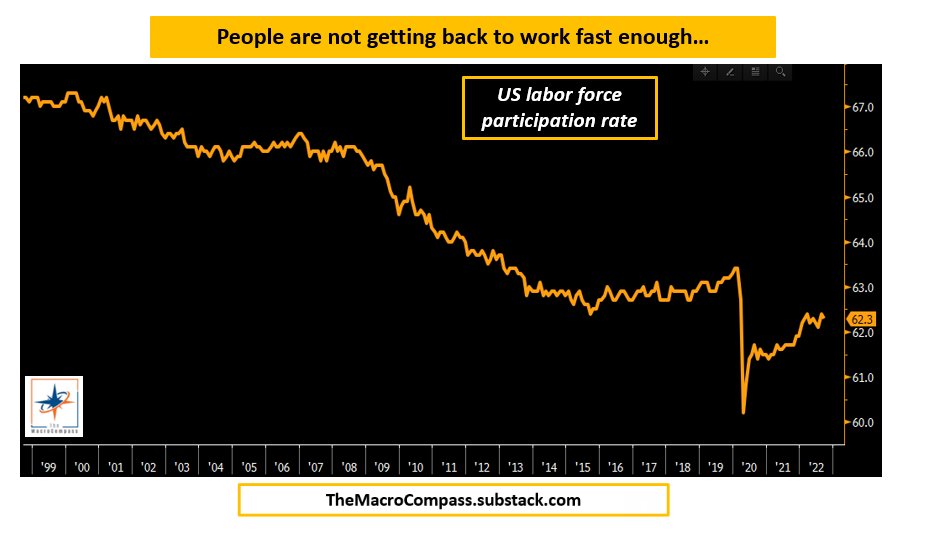

The US participation rate is still 1.2pp below the pre-pandemic levels, and even when accounting for an ageing population the long-term damage is evident.

This time, women were mostly responsible for the hit to the labor force.

Less people actively contributing...

6/

This time, women were mostly responsible for the hit to the labor force.

Less people actively contributing...

6/

...to economic and labor force growth is a big problem for the Fed here.

It both increases the probability of a recession and keeps wage pressures elevated as the supply of labor remains scarce.

Before we move to implications for the Fed and markets, one last word...

7/

It both increases the probability of a recession and keeps wage pressures elevated as the supply of labor remains scarce.

Before we move to implications for the Fed and markets, one last word...

7/

...on this labor market report.

The labor market IS slowing down - this is visible in the declining trend of job creation and wage growth.

At this point in the cycle though, the slowdown should be much more marked for policymakers to feel confident CPI will slow too.

8/

The labor market IS slowing down - this is visible in the declining trend of job creation and wage growth.

At this point in the cycle though, the slowdown should be much more marked for policymakers to feel confident CPI will slow too.

8/

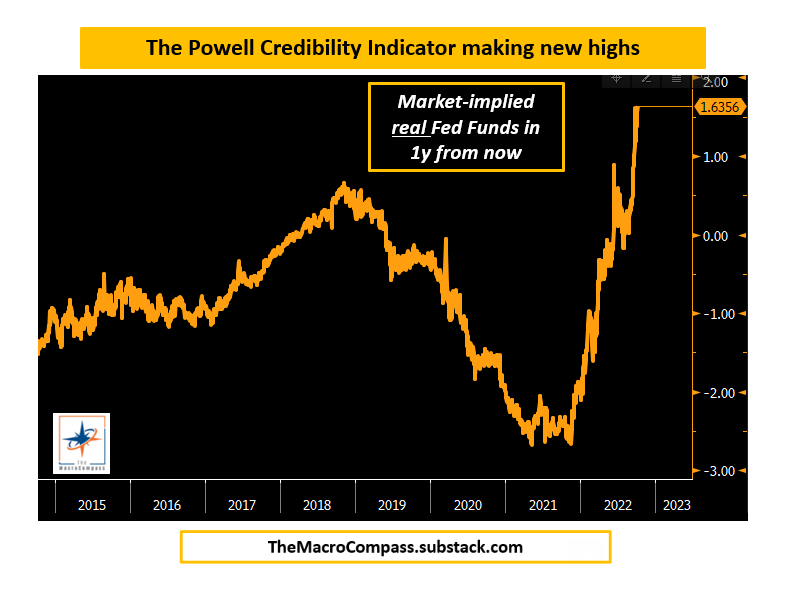

Markets are correctly interpreting what this labor market report means.

US terminal rates have been pushed back above 4.5%, but most importantly the Powell's credibility indicator is making new highs!

What's that?

9/

US terminal rates have been pushed back above 4.5%, but most importantly the Powell's credibility indicator is making new highs!

What's that?

9/

It's the market-implied real (!) Fed Funds in 1 year from now.

If markets believe Powell will keep at it until he beats inflation down, real Fed Funds 1 year from now will be easily above +1%.

They just made new highs - markets believe J-Pow will press hard.

10/

If markets believe Powell will keep at it until he beats inflation down, real Fed Funds 1 year from now will be easily above +1%.

They just made new highs - markets believe J-Pow will press hard.

10/

Gold can be considered as an alternative, non-interest bearing form of money.

As the USD denominated risk-free form of money (short-end Treasuries) starts rewarding holders better and better through higher real yields, the alternative...

...becomes less attractive.

11/

As the USD denominated risk-free form of money (short-end Treasuries) starts rewarding holders better and better through higher real yields, the alternative...

...becomes less attractive.

11/

Equities must also discount a tighter for longer Fed, which will ultimately succeed in weakening earnings and at the same time keep discounting rates elevated.

Not a nice combination.

So:

- Bad for equities

- Bad for gold

- Bad for bonds

This is annoying.

How long still?

12/

Not a nice combination.

So:

- Bad for equities

- Bad for gold

- Bad for bonds

This is annoying.

How long still?

12/

Yesterday I released an article that refreshed my entire macro framework and looked at historical parallels between today and 2001.

The evidence was striking, and so was the resulting asset allocation strategy.

Investors should soon be able to buy at least SOMETHING...

13/

The evidence was striking, and so was the resulting asset allocation strategy.

Investors should soon be able to buy at least SOMETHING...

13/

...without getting slaughtered the whole time like in 2022.

The piece is available here - and it's free!

Go have a look.

👇

14/14

#details" target="_blank" rel="noopener" onclick="event.stopPropagation()">themacrocompass.substack.com

The piece is available here - and it's free!

Go have a look.

👇

14/14

#details" target="_blank" rel="noopener" onclick="event.stopPropagation()">themacrocompass.substack.com

Loading suggestions...