A recent Electronics Retail co I added to portfolio, Aditya Vision

Please consider retweeting if you find it useful.

🧵 👇

Please consider retweeting if you find it useful.

🧵 👇

Q: How does AVL earn its money?

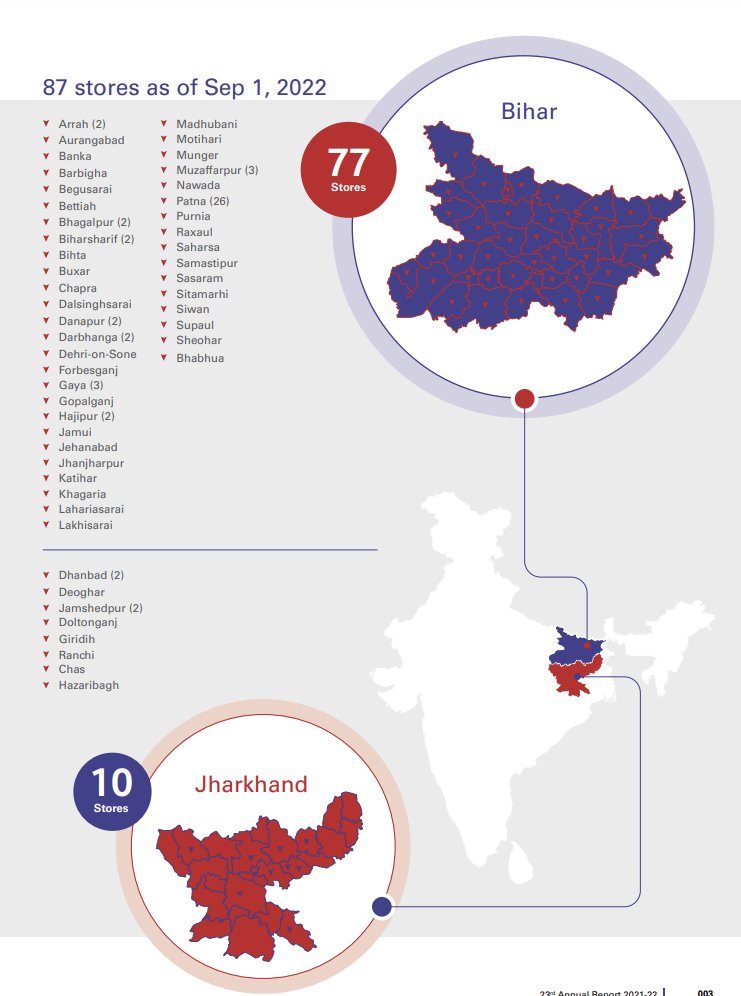

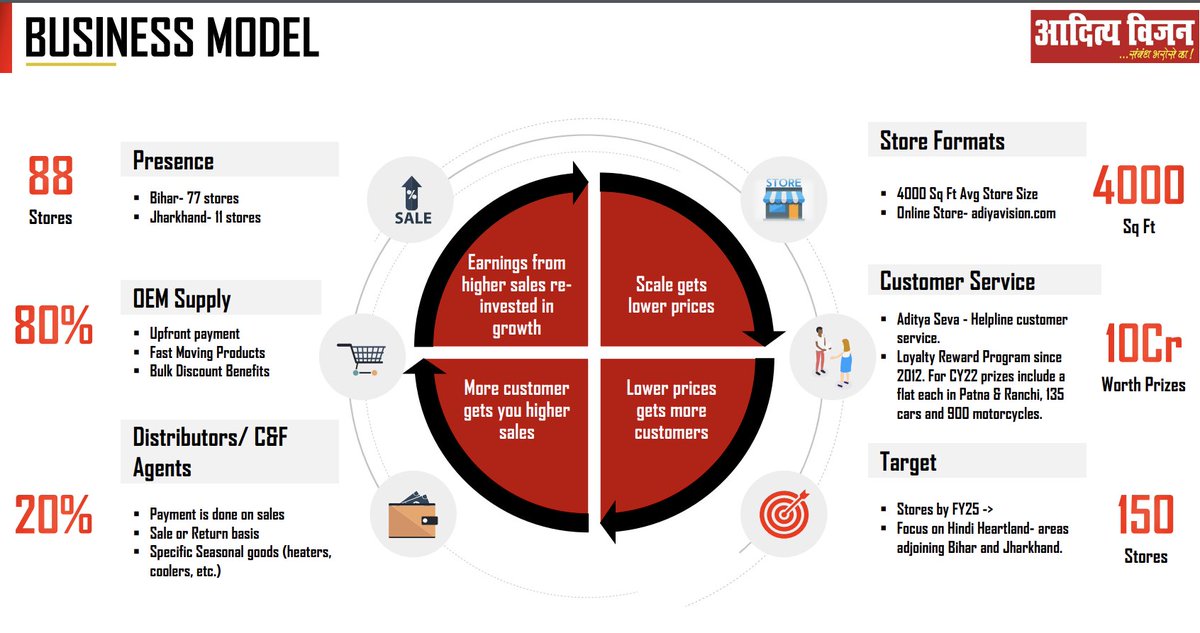

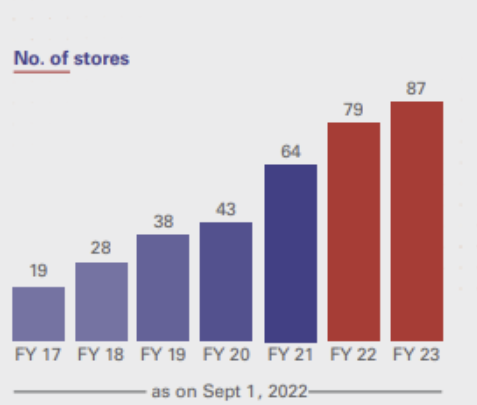

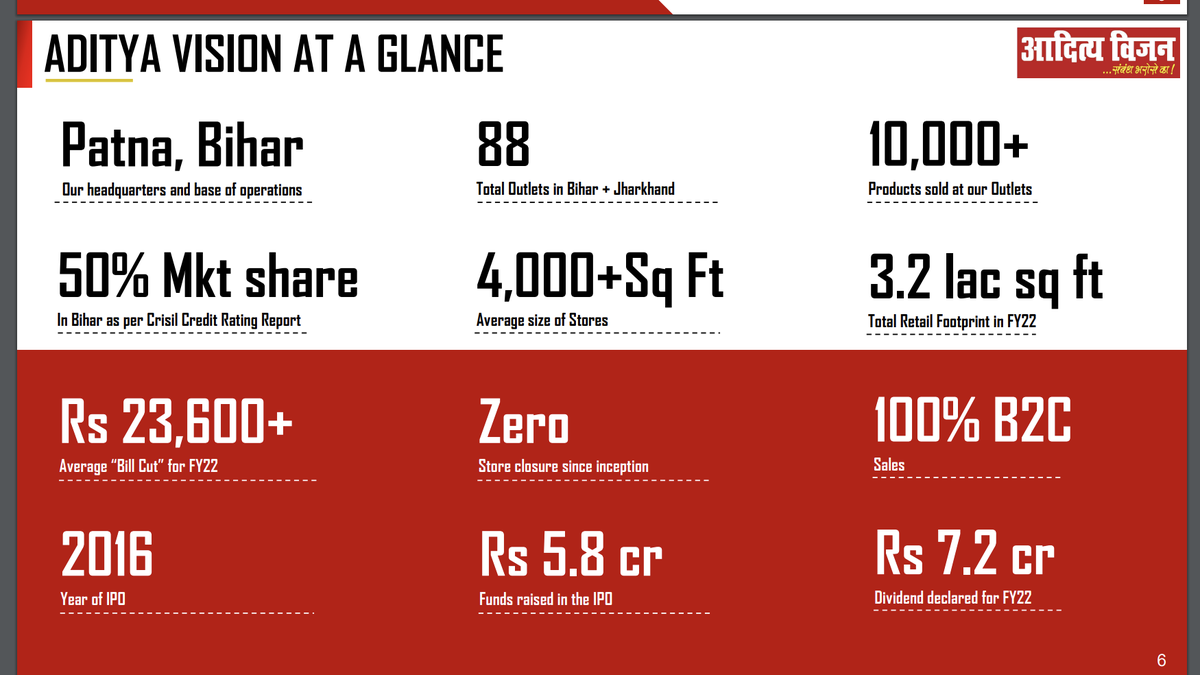

A: Aditya Vision is a Brick & mortar retailer of electronics (Televisions, Air conditioners, Refrigerators, Mobile phones). Started in 1999 with 1 store & and slowly scaled up to 89 stores today. Majority in Bihar. Some in Jharkhand.

A: Aditya Vision is a Brick & mortar retailer of electronics (Televisions, Air conditioners, Refrigerators, Mobile phones). Started in 1999 with 1 store & and slowly scaled up to 89 stores today. Majority in Bihar. Some in Jharkhand.

Part of the inventory in Aditya’s showrooms (display models) is on the OEM’s books. The salesmen deployed in Aditya are the OEM’s salesmen. The retailer makes a small margin on the inventory that they sell, how then do they make good profits? Three things:

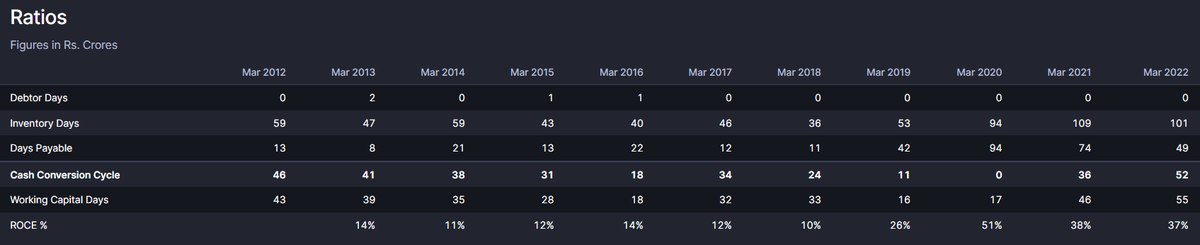

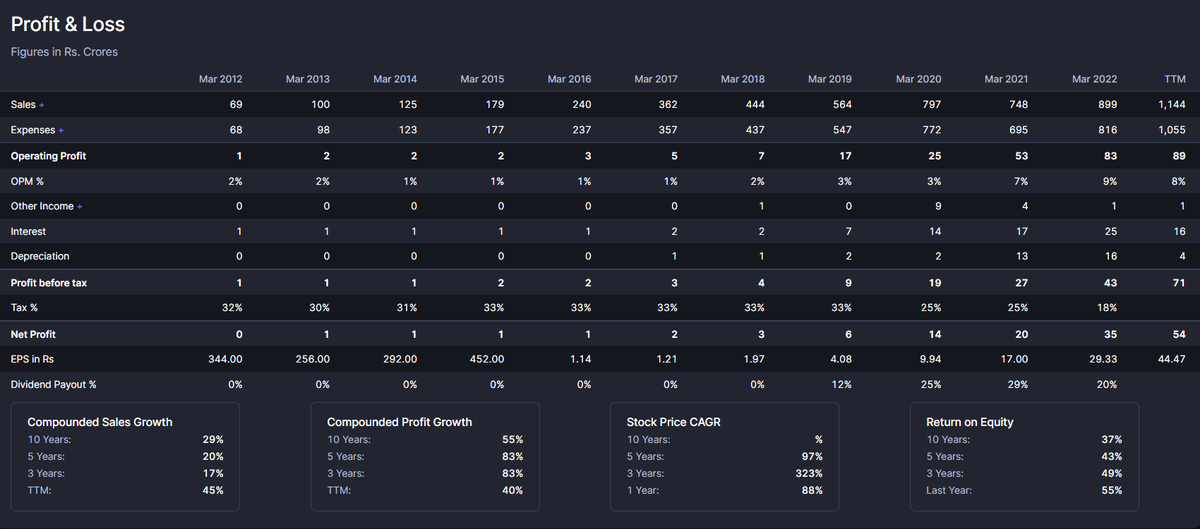

1. Inventory turnover. Aditya is extremely good here. A 5x inventory turnover (for FY22) puts it in a league of its own.

Aditya uses a differentiated biz model here.

Aditya uses a differentiated biz model here.

Each small store has an inventory alongside it which enables Aditya to make same day deliveries, whereas reliance and chroma are only able to deliver in a few days. Retail is essentially a services sector. Coz end product is commoditized. This is why it matters.

2. Scale, Scale Scale. According to the credit rating report Aditya holds 50% market share in Bihar. Think of the value proposition of a large retailer for an OEM. Lesser sales & marketing expenses. Deeper penetration.

All the pesky issues of handling last mile of sales taken care by aditya. This is how retailers gain gross margin. And that is what aditya has done.

3. Customer obsession & focus. How does aditya do this?

Through Services (Same day delivery in the hindi heartland where flipkart & amazon do not operate), service call centers (to enable their users to express their queries to 1 touch point: aditya; build loyalty, pull factor), lotteries.

All purchases of 10k & above enable each customer to enter a lucky draw with top prizes of houses, cars, motor bikes. This is the aspirational india, which gets rewarded for shopping

(Buy & Win 2021: youtube.com)

(Buy & Win 2021: youtube.com)

Q: Wait but isn't electronics retail a highly penetrated market? What will aditya Do here?

A:

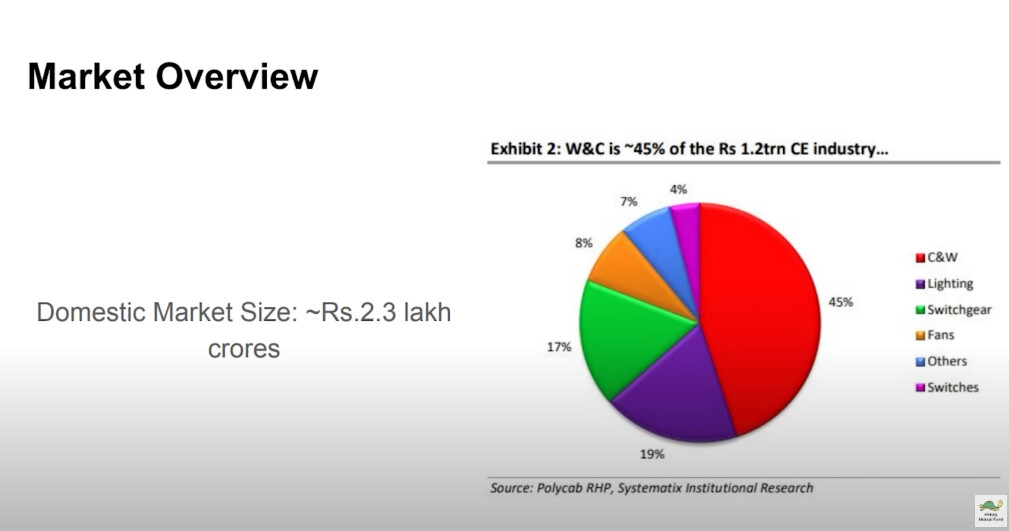

We know from this @PPFAS video (youtube.com) that the domestic white goods market is 2.3 x 0.45 = 1 lakh crore.

Aditya is hardly 1% of that maket (~1k cr sales).

A:

We know from this @PPFAS video (youtube.com) that the domestic white goods market is 2.3 x 0.45 = 1 lakh crore.

Aditya is hardly 1% of that maket (~1k cr sales).

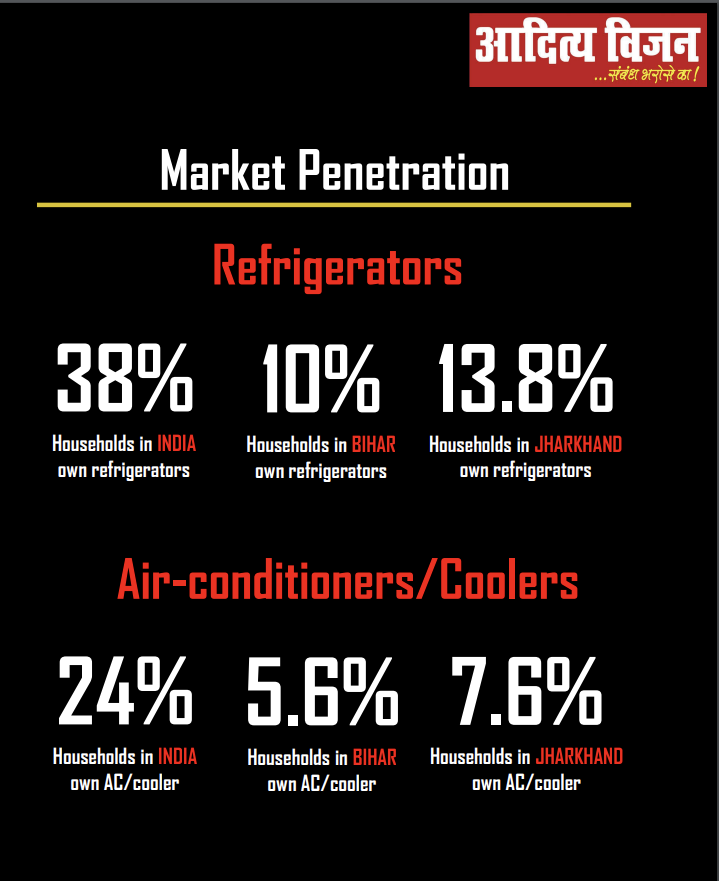

What's more? While India is decently penetrated, the geographies in which aditya operates and plans to operate are hardly one fourth as penetrated as India. Which leaves a fairly large headroom for Aditya to grow.

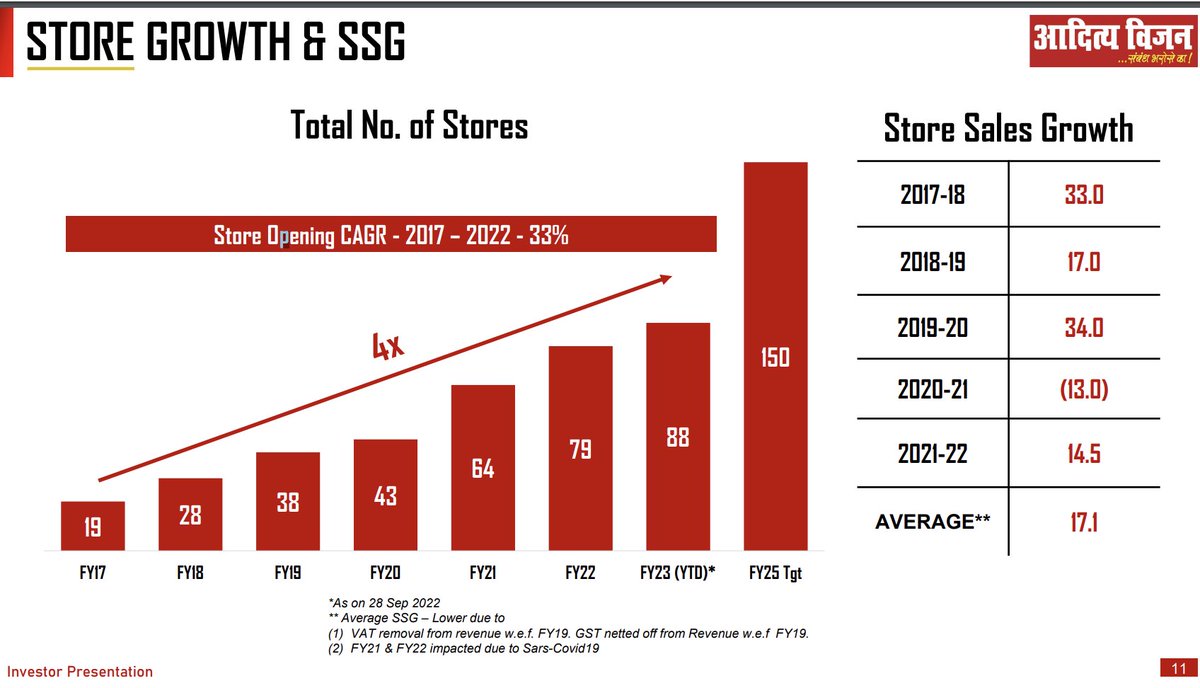

Until now, Aditya's scale up has been quite secular

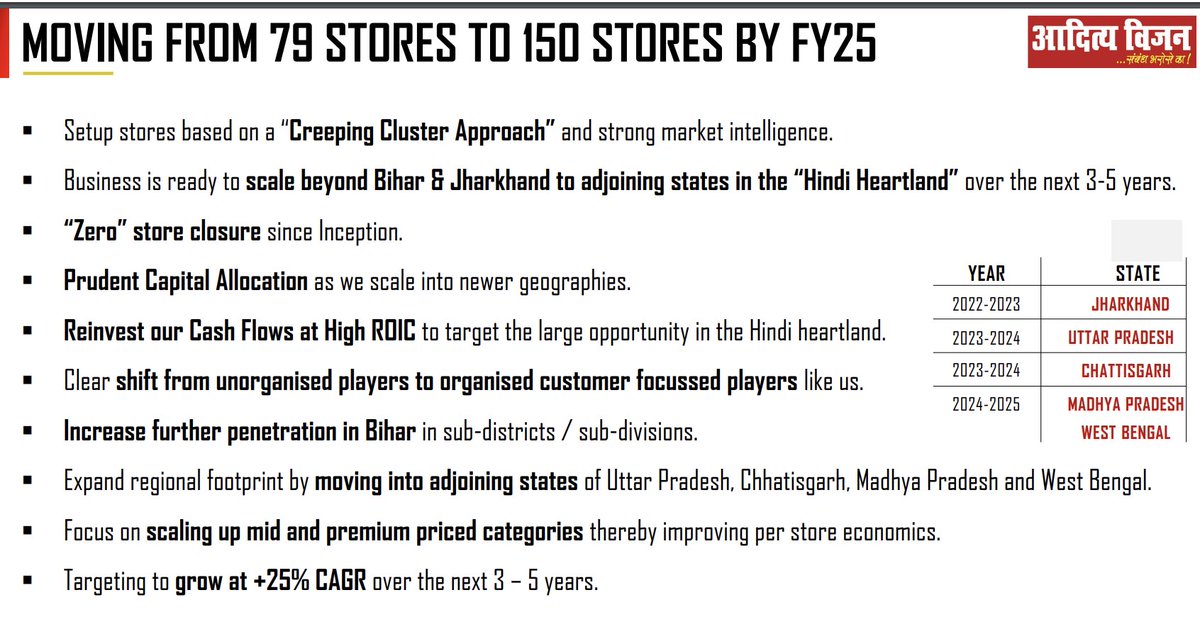

And Aditya's plans are to grow its store count at 20-25% CAGR over next 3 years.

Scale up is not mindless though. They are expanding in the hindi heartland. Jharkhand, Uttar Pradesh, Chattisgarh, Madhya Pradesh, West bengal.

Scale up is not mindless though. They are expanding in the hindi heartland. Jharkhand, Uttar Pradesh, Chattisgarh, Madhya Pradesh, West bengal.

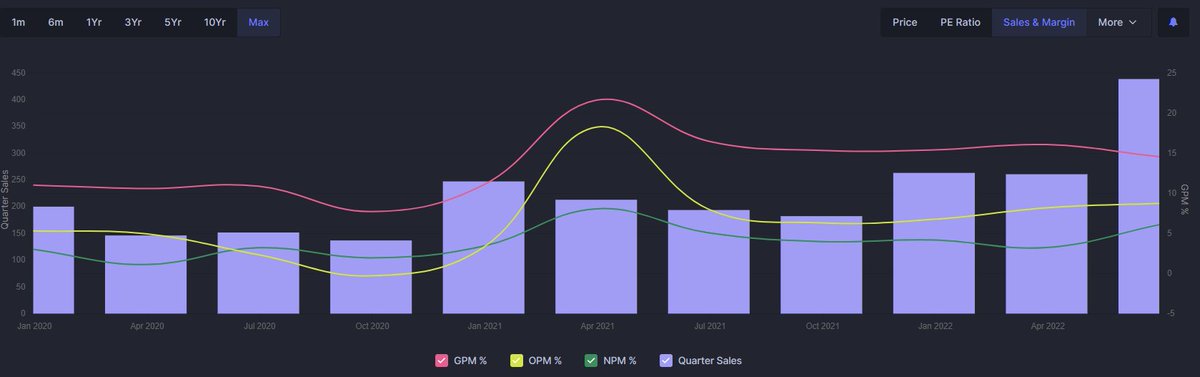

Q: I have observed that Aditya doubled its store count in last 2-3 years but revenue has hardly moved up?

A: A very astute observation.

A: A very astute observation.

In fact, management revealed in the AGM (Recording here: youtube.com) that ~ 80-85% of their FY22 revenue comes from stores opened before FY20.

The new stores have not yet ramped up due to covid. This brings in massive operating leverage going forward, which is what we see playing out in Q1 results.

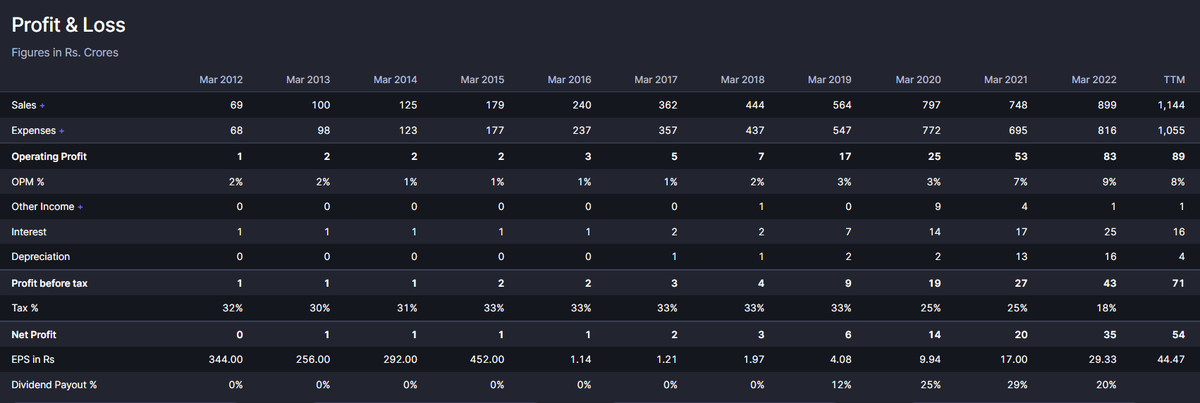

Q: In the last 2 years, Aditya's gross margin has strongly shot up from 10% to 15% is this sustainable & why did this happen?

A: According to management, 13-15% is a sustainable margin number.

A: According to management, 13-15% is a sustainable margin number.

Part of the reason for gross margin expansion has been the reduction in competitive intensity as the mom & pop stores found it hard to operate profitably at partial capacities (last 2 years brick and mortar retail has been severely disrupted by covid)

Q: Given that their gross margins are only ~14% how do they make money?

A: That gross margin is structural to retail industry. See D-mart for example.

A: That gross margin is structural to retail industry. See D-mart for example.

Or Vijay sales (Unlisted, can find on instafinancials or credit rating reports), or electronics mart india who is getting IPO'd as we speak.

Due to Aditya's efficient operations & the geographies they operate in, their lease costs are low, employee costs are low, up front capex is low, large capital requirement is for inventory only, their operating margins are good.

It is due to Aditya's strong brand that their strong inventory turns of 5x enable high asset turns enabling high ROCEs. From channel checks, Aditya's per sqft revenue is 3x Reliance digital or chroma's in Bihar. This is the reason below strong unit economics.

Q: Wouldnt amazon & Flipkart negatively impact Aditya Vision's business?

A: In this geography, the sort of strata of consumers that Aditya targets do not trust e-commerce enough to make large ticket purchases without viewing & interacting with it physically.

A: In this geography, the sort of strata of consumers that Aditya targets do not trust e-commerce enough to make large ticket purchases without viewing & interacting with it physically.

Aditya offers EMI purchases, same day delivery, unified call center all these services along with a physical presence make aditya the place of choice for 1st time TV/Refrigerator buyers. What's more?

Because Aditya moves 50% of bihar's volumes, OEM cannot afford to make any other player more profitable or efficient than Aditya (OEMs are invested in Aditya's financial stability)

Q: In Retail, inventory management is the key. How does Aditya handle dated or old or stale inventory?

A: If any model remains unsold when new models are to come in, OEMs help clear inventory by giving heavy discounts (AVL margins are protected). Despite 100% of Sales being B2C

A: If any model remains unsold when new models are to come in, OEMs help clear inventory by giving heavy discounts (AVL margins are protected). Despite 100% of Sales being B2C

Q: What sort of SSSG (Same store sales growth) does AVL do?

A: Some of the mature stores do 12%. Average growth is 15%. I'd be surprised if AVL's revenue growth is less than 2x in next 3 years.

A: Some of the mature stores do 12%. Average growth is 15%. I'd be surprised if AVL's revenue growth is less than 2x in next 3 years.

Q: Is not it overvalued at 35 time earnings?

A: In India, good retailers get good valuations due to the secular growth runway. Specially since most of these are discretionary purchases. My own home used to have 1 TV for 20 years. Last 3-4 years we tripled it to 3 TVs.

A: In India, good retailers get good valuations due to the secular growth runway. Specially since most of these are discretionary purchases. My own home used to have 1 TV for 20 years. Last 3-4 years we tripled it to 3 TVs.

Growth runway here is massive.

Electronics mart india (EMI) is expected to list at similar or higher valuations and serves as a peer comparison (though both are not same biz model since EMI also does B2B sales through Amazon/Flipkart etc).

Look at the growth.

Electronics mart india (EMI) is expected to list at similar or higher valuations and serves as a peer comparison (though both are not same biz model since EMI also does B2B sales through Amazon/Flipkart etc).

Look at the growth.

Look at the scale up. Look at the ROCE. We cannot see P/E in isolation. Need to view it in the context of what is happening.

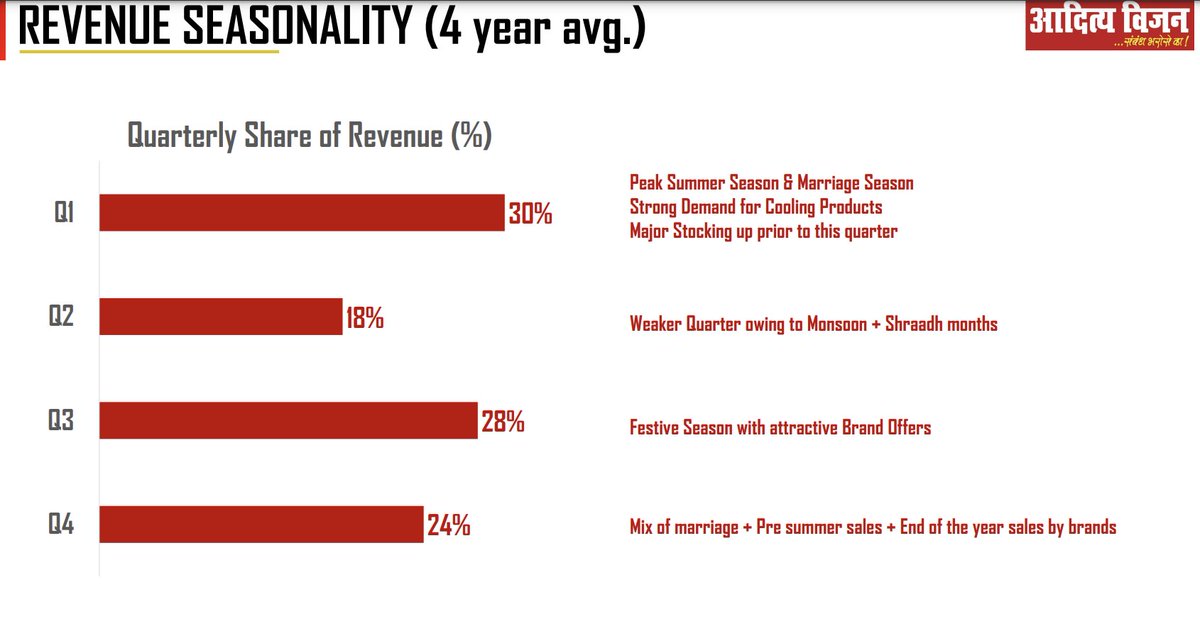

Typically, AVL does 30% revenue in Q1. Using this, i estimate that it might do 1450 cr revenue in FY23 and around 70 cr PAT in FY23. It is at around 27 times FY23 earnings. Given that half the year has gone by, i think that is reasonable.

Electronics manufacturing in India is a secular megatrend. I am happy to capture the very last part of that supply chain now.

Q: What are the risks to be aware about?

A: Many actually. Investor has to tread with caution here.

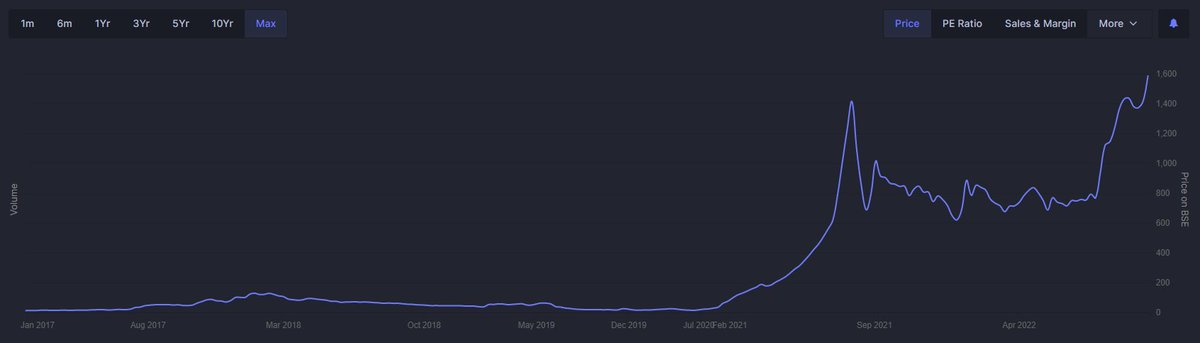

1. Price is up 50x compared to pre-covid levels. Everyone wants to be not anchored to price but this is a risk one has to be aware about.

A: Many actually. Investor has to tread with caution here.

1. Price is up 50x compared to pre-covid levels. Everyone wants to be not anchored to price but this is a risk one has to be aware about.

Also, for the beginning part, price rise was exponential curve. To some seasoned investors this reeks of price manipulation/operator-driven. Something to be very aware and careful about.

2. At 35 time TTM earnings this is not cheap or undervalued by any stretch of imagination. Having said that, any efficient scaled up retailer gets good valuations (Trent, Dmart, Vmart, EMI).

3. Until now, competition has largely been not been successful in competing with AVL in Eastern part of India. Patna & Ranchi do have presence of reliance digital, chroma. They havent been able to compete successfully with AVL yet. This remains a key monitorable.

Also, in bihar, AVL was the incumbent, in jharkhand and other states where it is expanding, it is likely to find other incumbents it has to deal with.

4. Key advantage of AVL remains the whitespace left by the inability of the populace here to trust & work with e-commerce like Amazon & Flipkart. That whitespace can eventually get bridged like it did in the metro cities. Remains a key monitorable.

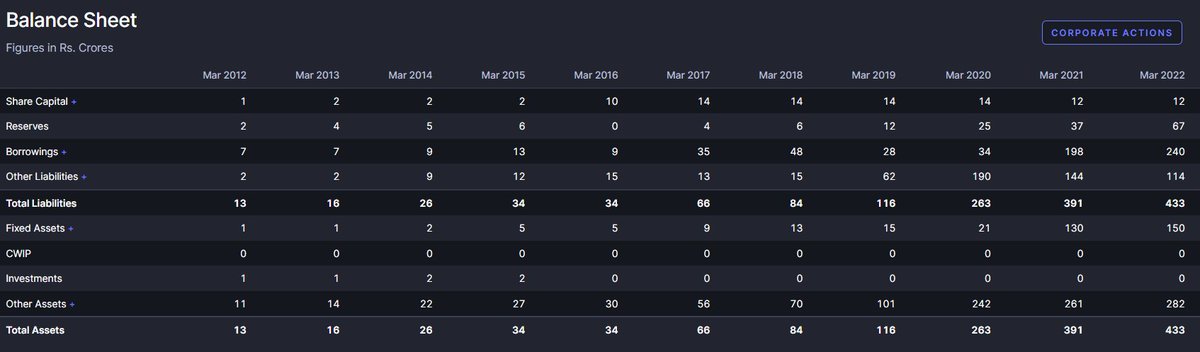

5. If we look at the FY20 interest payment and the FY20 borrowings, there is a mismatch. How can the interest payment be 14 cr on 34 cr borrowings?

Caveat: Borrowings are at a point in time, interest is over the period. Comparison is difficult.

Caveat: Borrowings are at a point in time, interest is over the period. Comparison is difficult.

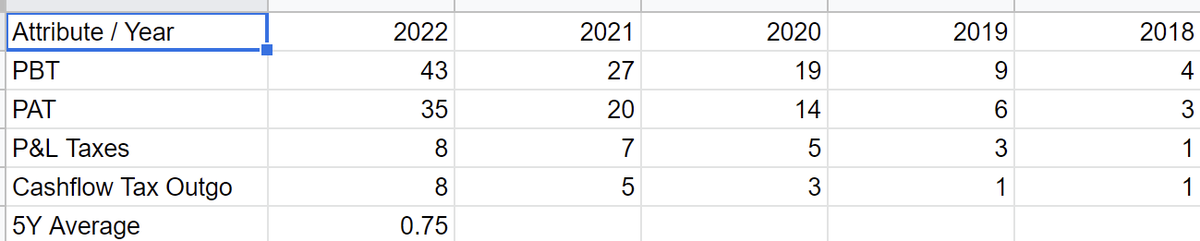

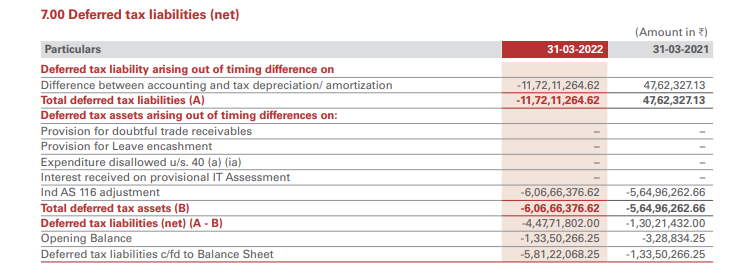

6. The cash taxes paid are around 75% of the P&L taxes accrued in last 5 years.

THis seems to be largely explained by Deferred tax liabilities but this is something to be aware about.

Q: What is your average buying price?

A: Smallcaps are risky. Everyone ought to do their own due diligence and study before putting their risk capital at work. Do not clone anyone mindlessly. Including me. I can change my mind at any time. Specially if i find a better idea.

A: Smallcaps are risky. Everyone ought to do their own due diligence and study before putting their risk capital at work. Do not clone anyone mindlessly. Including me. I can change my mind at any time. Specially if i find a better idea.

(I have hardly read 300 out of 6000 companies). My average buying price is ~18% lower than CMP of 1590.

If you like this thread, please feel free to follow me @sahil_vi I write such company threads once in a while.

You can find other company threads I've written here:

Have a good Sunday

You can find other company threads I've written here:

Have a good Sunday

Loading suggestions...