(1/16)

About:

H.G. Infra Engineering Limited was incorporated in 2003.

HGIEL, along with its nine HAM SPVs, is primarily involved in the construction of roads and

highways in Odisha, Telangana, Rajasthan, Delhi, Andhra Pradesh, Haryana and Uttar Pradesh

About:

H.G. Infra Engineering Limited was incorporated in 2003.

HGIEL, along with its nine HAM SPVs, is primarily involved in the construction of roads and

highways in Odisha, Telangana, Rajasthan, Delhi, Andhra Pradesh, Haryana and Uttar Pradesh

(2/16)

Clientele:

• National Highways Authority of India (NHAI)

• Ministry of Road Transport and Highways (MoRTH)

• IRB Infrastructure Developers

• Tata Projects Limited

• Adani Road Transport Limited, etc

Clientele:

• National Highways Authority of India (NHAI)

• Ministry of Road Transport and Highways (MoRTH)

• IRB Infrastructure Developers

• Tata Projects Limited

• Adani Road Transport Limited, etc

(3/16)

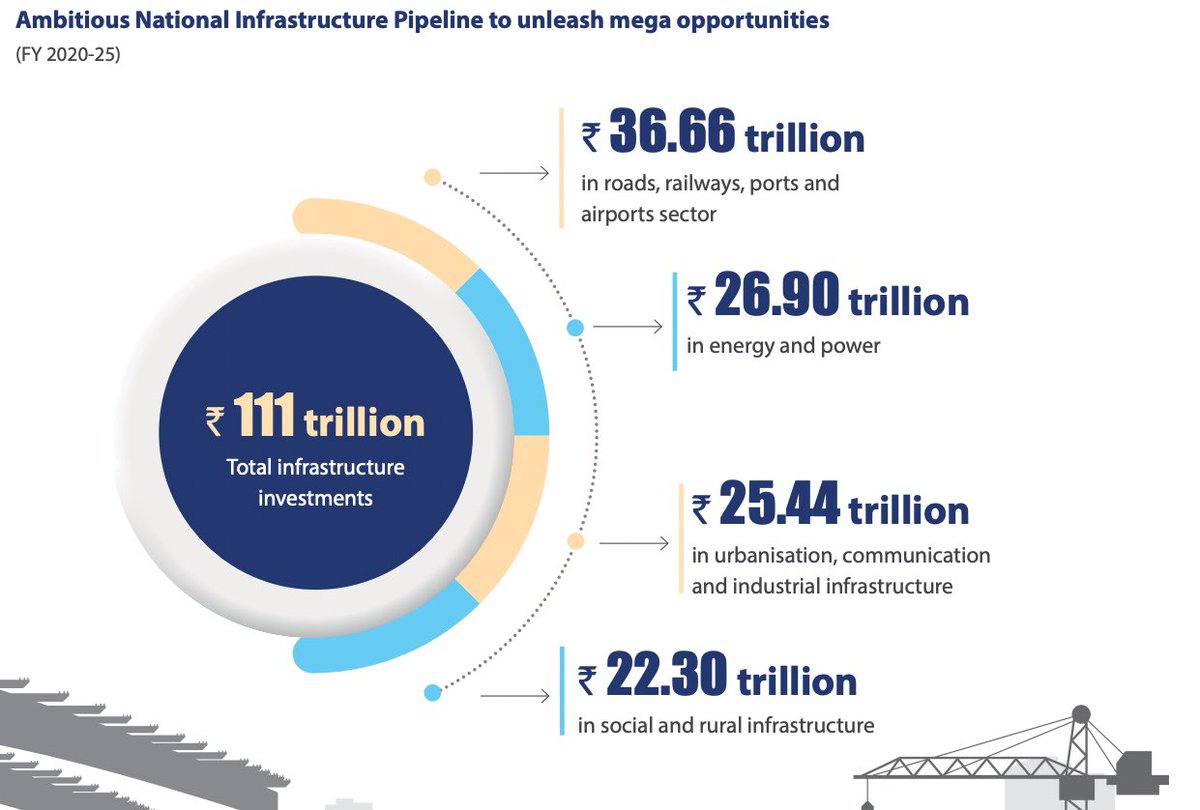

Industry Opportunities:

India’s infrastructure segment is all set for explosive growth. The GOI’s

initiative around creating a ₹111 trillion National Infrastructure Pipeline (NIP), plans

to monetise assets & expedite transportation projects with Gati Shakti Master Plan.

Industry Opportunities:

India’s infrastructure segment is all set for explosive growth. The GOI’s

initiative around creating a ₹111 trillion National Infrastructure Pipeline (NIP), plans

to monetise assets & expedite transportation projects with Gati Shakti Master Plan.

(4/16)

Gati Shakti Push

Under the initiative,

16 ministries and their schemes including flagship ones like

Bharatmala, Sagarmala, Udaan, expansion of railway network,

inland waterways and Bharat Net will be integrated.

Gati Shakti Push

Under the initiative,

16 ministries and their schemes including flagship ones like

Bharatmala, Sagarmala, Udaan, expansion of railway network,

inland waterways and Bharat Net will be integrated.

(5/16)

HG Infra’s Business Strategy:

• Core focus on road EPC & HAM:

EPC projects: timely execution with strong discipline in order

selection

HAM projects: bid selectively to maintain healthy IRR &

explore monetisation to free equity

• Diversification to other infra sector

HG Infra’s Business Strategy:

• Core focus on road EPC & HAM:

EPC projects: timely execution with strong discipline in order

selection

HAM projects: bid selectively to maintain healthy IRR &

explore monetisation to free equity

• Diversification to other infra sector

(6/16)

• Established new business division to diversify

• Modernising construction capabilities

• Strengthened P&M capabilities:

Invested ₹640.78 million towards

upgrading our project execution capabilities.

• Established new business division to diversify

• Modernising construction capabilities

• Strengthened P&M capabilities:

Invested ₹640.78 million towards

upgrading our project execution capabilities.

(7/16)

Strengths:

• An established contractor with a proven execution track record of more than 19 years

• A strong presence spread across 9 states

• A prequalification which is high enough to independently

bid on big EPC and HAM projects

Strengths:

• An established contractor with a proven execution track record of more than 19 years

• A strong presence spread across 9 states

• A prequalification which is high enough to independently

bid on big EPC and HAM projects

(8/16)

• An integrated business model with focus on cost efficiencies

in real time

• A continuous investment in advanced equipment &

technologies deployed at project sites

• An organisation-wide SAP implementation to improve

operational effectiveness & increased transparency

• An integrated business model with focus on cost efficiencies

in real time

• A continuous investment in advanced equipment &

technologies deployed at project sites

• An organisation-wide SAP implementation to improve

operational effectiveness & increased transparency

(9/16)

Weakness:

• The weather and different seasons impact operations of the

Company

• Working Capital Intensive business

• Relatively underpenetrated market presence in southern

and eastern states

Weakness:

• The weather and different seasons impact operations of the

Company

• Working Capital Intensive business

• Relatively underpenetrated market presence in southern

and eastern states

(10/16)

Vulnerability of profitability to price fluctuations; – The heightened competition in the road sector along with the steep increase in input costs could exert pressure on HGIEL's profitability

despite the presence of a price escalation clauses in these contracts.

Vulnerability of profitability to price fluctuations; – The heightened competition in the road sector along with the steep increase in input costs could exert pressure on HGIEL's profitability

despite the presence of a price escalation clauses in these contracts.

(11/16)

• High sectorial & client concentration risk: HG is exposed to high segment and client concentration risks with entire order book consisting of road works mainly from

the NHAI. Any downcycle in the road construction sector may adversely impact its business returns.

• High sectorial & client concentration risk: HG is exposed to high segment and client concentration risks with entire order book consisting of road works mainly from

the NHAI. Any downcycle in the road construction sector may adversely impact its business returns.

(12/16)

• Liquidity:

HGIEL's average utilisation of the fund-based limits during the last 13-month period ended March 2022 is moderate at 56%.

HGIEL’s liquidity is supported by undrawn working capital limits of ~₹100 cr & free cash & liquid investments of ₹65 cr (March End)

• Liquidity:

HGIEL's average utilisation of the fund-based limits during the last 13-month period ended March 2022 is moderate at 56%.

HGIEL’s liquidity is supported by undrawn working capital limits of ~₹100 cr & free cash & liquid investments of ₹65 cr (March End)

(13/16)

HG has repayments of ~₹45 crore & equity commitment of ₹460 crore in FY2023.

Recovery of ~₹100 cr from sticky receivables will also aid CF in FY2023. The estimated CFO is expected to be sufficient for the equity commitments towards

HAM projects & the debt repayments

HG has repayments of ~₹45 crore & equity commitment of ₹460 crore in FY2023.

Recovery of ~₹100 cr from sticky receivables will also aid CF in FY2023. The estimated CFO is expected to be sufficient for the equity commitments towards

HAM projects & the debt repayments

(14/16)

Key Ratios:

• Stock P/E: 9.47

• RoCE: 28.50%

• RoE: 30.5%

• PEG: 0.20

• Price to Sales: 0.94

• Interest coverage: 5.21

• Sales Growth 3 Years : 23%

• D/E: 0.82

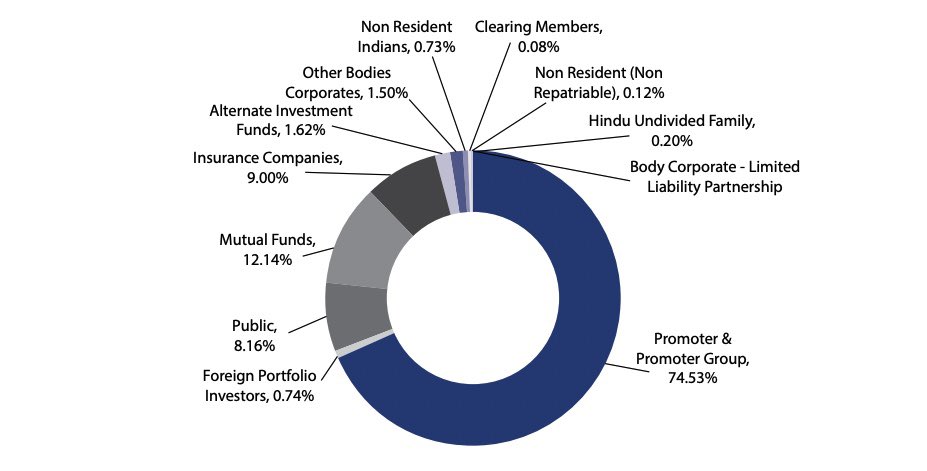

Shareholding:

Key Ratios:

• Stock P/E: 9.47

• RoCE: 28.50%

• RoE: 30.5%

• PEG: 0.20

• Price to Sales: 0.94

• Interest coverage: 5.21

• Sales Growth 3 Years : 23%

• D/E: 0.82

Shareholding:

Loading suggestions...