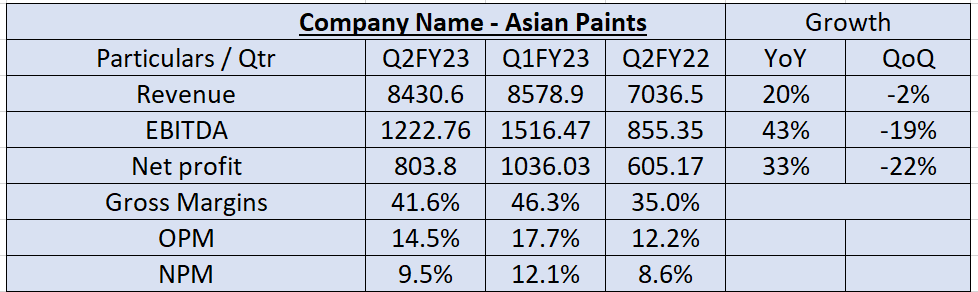

Asian Paints Q2FY23 Review -

- Revenue up 20% to Rs 8431 cr

- EBITDA up 43% to Rs 1223 cr

- Net profit up 33% to Rs 804 cr

- OPM and NPM are up YoY, down QoQ

- Gross margins are up YoY, Down QoQ

- Borrowings of 1000 cr as of H2FY23 v/s 770 cr as at FY22

- Revenue up 20% to Rs 8431 cr

- EBITDA up 43% to Rs 1223 cr

- Net profit up 33% to Rs 804 cr

- OPM and NPM are up YoY, down QoQ

- Gross margins are up YoY, Down QoQ

- Borrowings of 1000 cr as of H2FY23 v/s 770 cr as at FY22

- Cash Flows - H2HY23 CFO at 1336 cr v/s -580 cr in H2FY22 | FCF at 907 cr v/s -837 cr

- Dividend - interim dividend of Rs. 4.40 (record date 1st Nov and payment on or after 10 Nov 2022)

- Dividend - interim dividend of Rs. 4.40 (record date 1st Nov and payment on or after 10 Nov 2022)

- The domestic Decorative business showed resilience to deliver a double-digit volume growth and healthy value growth despite subdued demand conditions, impacted by the extended monsoon

- Series of calibrated price increases to offset the impact of increased inflation on margins

- Series of calibrated price increases to offset the impact of increased inflation on margins

- International: Sales increased 15.3% to ₹ 806 Cr from Rs 699 Cr. PBT was ₹ 43.48 Cr in Q2 FY’23 v/s loss of ₹ 16.74 Cr

- Bath Fittings: Sales up 11% to ₹ 101.77 Cr v/s ₹ 91.77 cr. PBT was ₹ 0.24 Cr v/s ₹3.3 Cr YoY

- Bath Fittings: Sales up 11% to ₹ 101.77 Cr v/s ₹ 91.77 cr. PBT was ₹ 0.24 Cr v/s ₹3.3 Cr YoY

- Kitchen business: Sales up 14.2% to Rs 117.83 cr v/s ₹ 103.15 Cr. PBT loss was ₹ 4.30 Cr v/s profit of ₹ 0.25 Cr YoY

- Industrial business: APPPG Sales are up 25.4% to 225 cr v/s 179 cr. PBT was ₹ 13.65 crores v/s ₹ 4.84 Cr YoY

No reco.

- Industrial business: APPPG Sales are up 25.4% to 225 cr v/s 179 cr. PBT was ₹ 13.65 crores v/s ₹ 4.84 Cr YoY

No reco.

Loading suggestions...