Laurus Labs Conducted their Q2 and H1 FY23 conference Call on 21st October.

Here are the key takeaways…

Here are the key takeaways…

Business overview

- Company has delivered flattish results during the period.

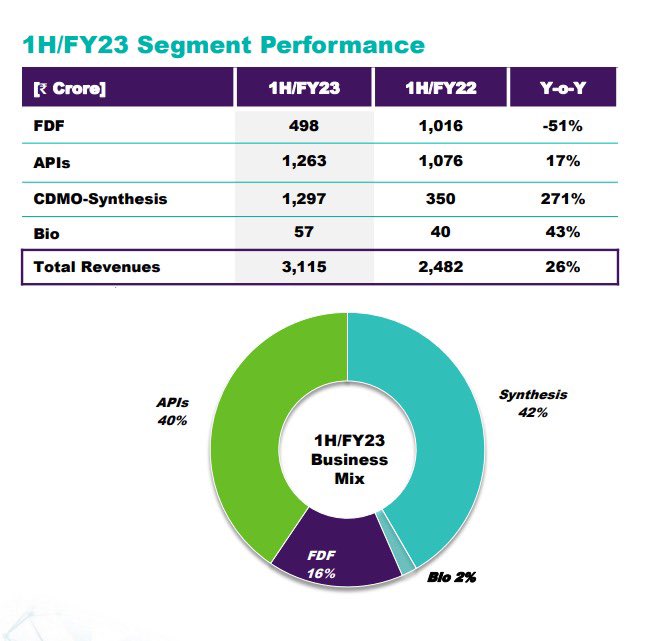

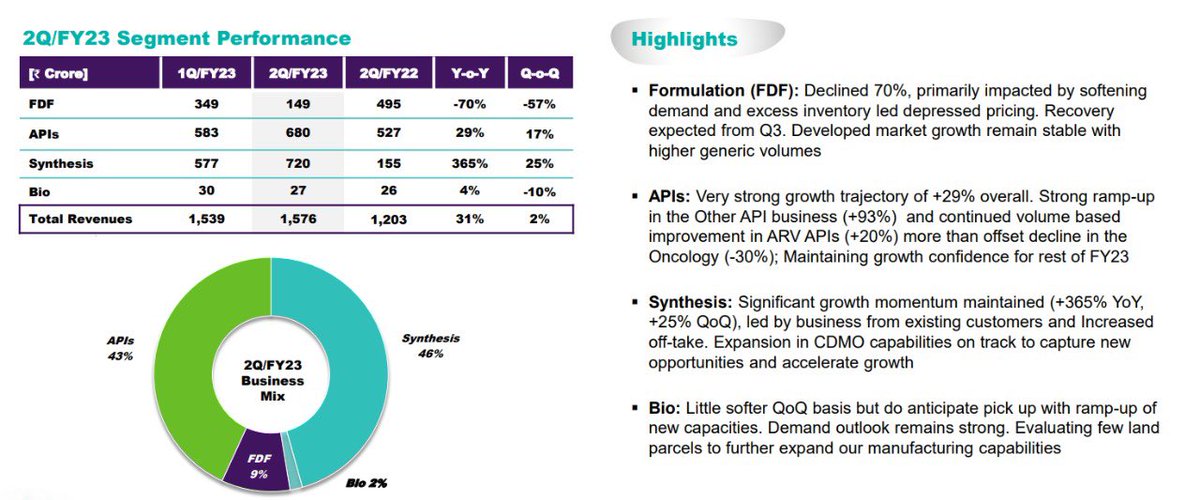

- During the half timeframe, FDF segment have declined by approximately 50% due to weak global agencies but expect a strong recovery from next quarter onwards.

- Company has delivered flattish results during the period.

- During the half timeframe, FDF segment have declined by approximately 50% due to weak global agencies but expect a strong recovery from next quarter onwards.

- FDF revenues were mainly dragged by lower ARV business, but strong recovery is expected with higher generic volumes.

- Their API business recovered 17% aided by new contracts.

- Though Oncology declined 30%, improvements are expected in 2H

- The CDMO space, delivered a solid growth of 270% through new product execution and favourable contacting trends.

- Though Oncology declined 30%, improvements are expected in 2H

- The CDMO space, delivered a solid growth of 270% through new product execution and favourable contacting trends.

- Above 50 active projects at different stages are present in synthesis phase. And they have became suppliers for 4 commercial projects.

- New CEO and COO will take over from Mr. R. Subramani who have stepped down from executive role due to personal reasons.

- New CEO and COO will take over from Mr. R. Subramani who have stepped down from executive role due to personal reasons.

- Under Bios segment, sales jumped by 43% and expect to deliver stronger with company heavy investment in this space.

- Scale,Cost and functionality have been the key drivers for this differential performance.

- Leading to better focus towards product offering and relationship.

- Scale,Cost and functionality have been the key drivers for this differential performance.

- Leading to better focus towards product offering and relationship.

Financials

- For the first half period, the revenue stood around 3100 crore levels Compared to 2500 levels previous year.

- The Companies EBITDA levels stood around 900 crores up by 21%.

- Though there is a decline of 1% in EBITDA margins.

- For the first half period, the revenue stood around 3100 crore levels Compared to 2500 levels previous year.

- The Companies EBITDA levels stood around 900 crores up by 21%.

- Though there is a decline of 1% in EBITDA margins.

- The net profit stood around 480 crores, due to heavy taxation for the timeline.

- The company has a negative cash flow on operating level due to high inventory levels and supply chain challenges.

- The company has a negative cash flow on operating level due to high inventory levels and supply chain challenges.

Capex

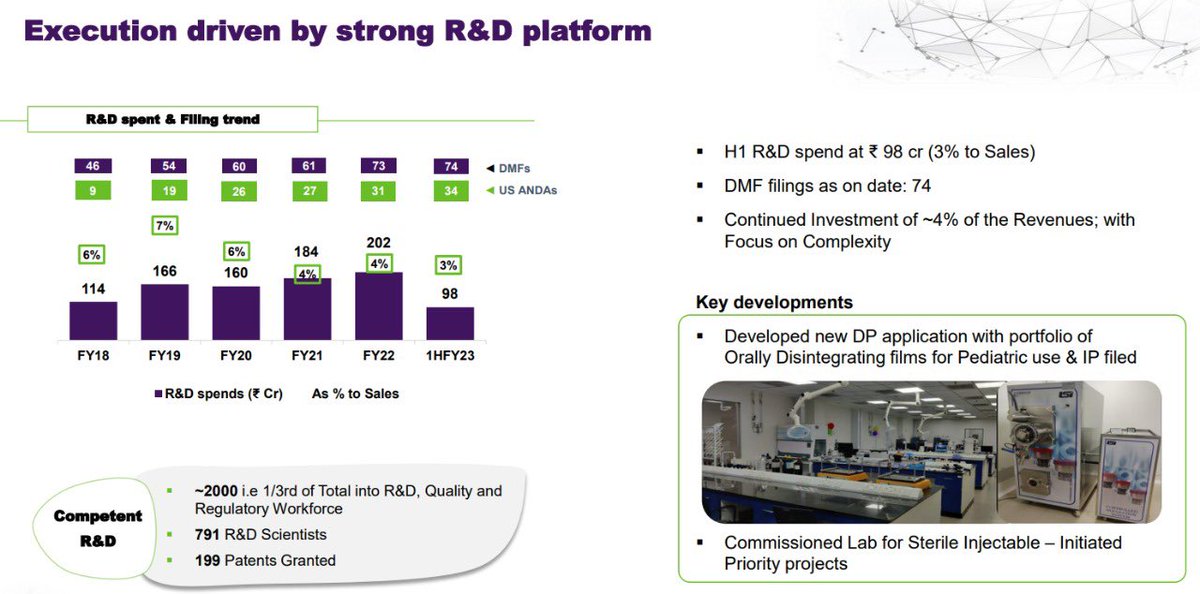

- For the 1 half timeframe there has been a decline in the RnD spending as well.

- Nearly 100 crores are been invested for the quarter and with the progress in Capex ,being inline with forecast they expect to deliver in the timeline mentioned.

- For the 1 half timeframe there has been a decline in the RnD spending as well.

- Nearly 100 crores are been invested for the quarter and with the progress in Capex ,being inline with forecast they expect to deliver in the timeline mentioned.

- Till now 400 crore Worth of Capex has been incurred.

- Under FDF, unit-2 brownfield capacity was brought online last quarter.

- Under DM filings 3 products were filed in developed markets and they have commissioned R&D lab for sterile injectables.

- Under FDF, unit-2 brownfield capacity was brought online last quarter.

- Under DM filings 3 products were filed in developed markets and they have commissioned R&D lab for sterile injectables.

- In CDMO space, with strong and wider customer base they have initiated plans for new R&D center and 3 manufacturing units.

- All above expected to be completed before 2025.

- All above expected to be completed before 2025.

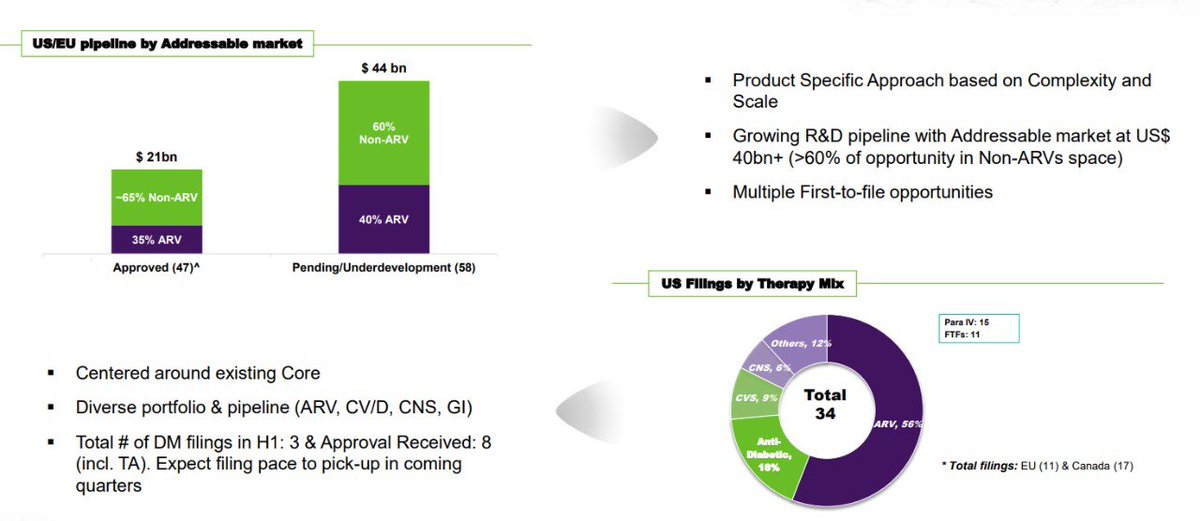

- Till now company has gained 21bn dollars worth of approved pipeline 65% to be non ARV and about 44 billion $ worth is under development in the ratio of 60/40 wherein 60% is for Non ARV.

- They tend to prepare strong pipeline in each segment area to gain market opportunities like.

- Under FDF, they expect to start monetisation in diabetic and CV portfolios.

- Under API, scale up is done in anti-diabetic,CV and PPI.

- Under FDF, they expect to start monetisation in diabetic and CV portfolios.

- Under API, scale up is done in anti-diabetic,CV and PPI.

- Synthesis, the company is trying to strengthen its presence in nutraceuticals and Cosmeceuticals area.

- And Finally, For bios scale up is done in alternate food proteins and goal to expand the biological CDMO at scale in long term.

- And Finally, For bios scale up is done in alternate food proteins and goal to expand the biological CDMO at scale in long term.

Loading suggestions...