Whilst accountants know how to prepare a BALANCE SHEET… 95% don’t know how to read them.

Interpreting balance sheets is the HARD bit.

So, here are the first 3 things I look for when reading a balance sheet.

Pull up a chair.

Let's go! 👇

Interpreting balance sheets is the HARD bit.

So, here are the first 3 things I look for when reading a balance sheet.

Pull up a chair.

Let's go! 👇

When I review a balance sheet, I need a detailed picture of how the business is funded.

I’ll build out a picture under 3 headings;

1. Capital Structure

2. Working Capital Profile

3. Liquidity Headroom

Let's tackle them each in turn

I’ll build out a picture under 3 headings;

1. Capital Structure

2. Working Capital Profile

3. Liquidity Headroom

Let's tackle them each in turn

1. Capital Structure.

The capital structure tells you how a business is funded / owned.

Is the business funded by debt or equity? What is the mix?

Who are the investors and what are their motives? And what are the rights and obligations attached to each?

The capital structure tells you how a business is funded / owned.

Is the business funded by debt or equity? What is the mix?

Who are the investors and what are their motives? And what are the rights and obligations attached to each?

Take each debt or equity instrument in the balance sheet and get clear on the following:

Who owns it?

How much have they put in?

What are they owed today?

What does their return look like if things go well

What are their rights if things don’t go well?

When does it mature?

Who owns it?

How much have they put in?

What are they owed today?

What does their return look like if things go well

What are their rights if things don’t go well?

When does it mature?

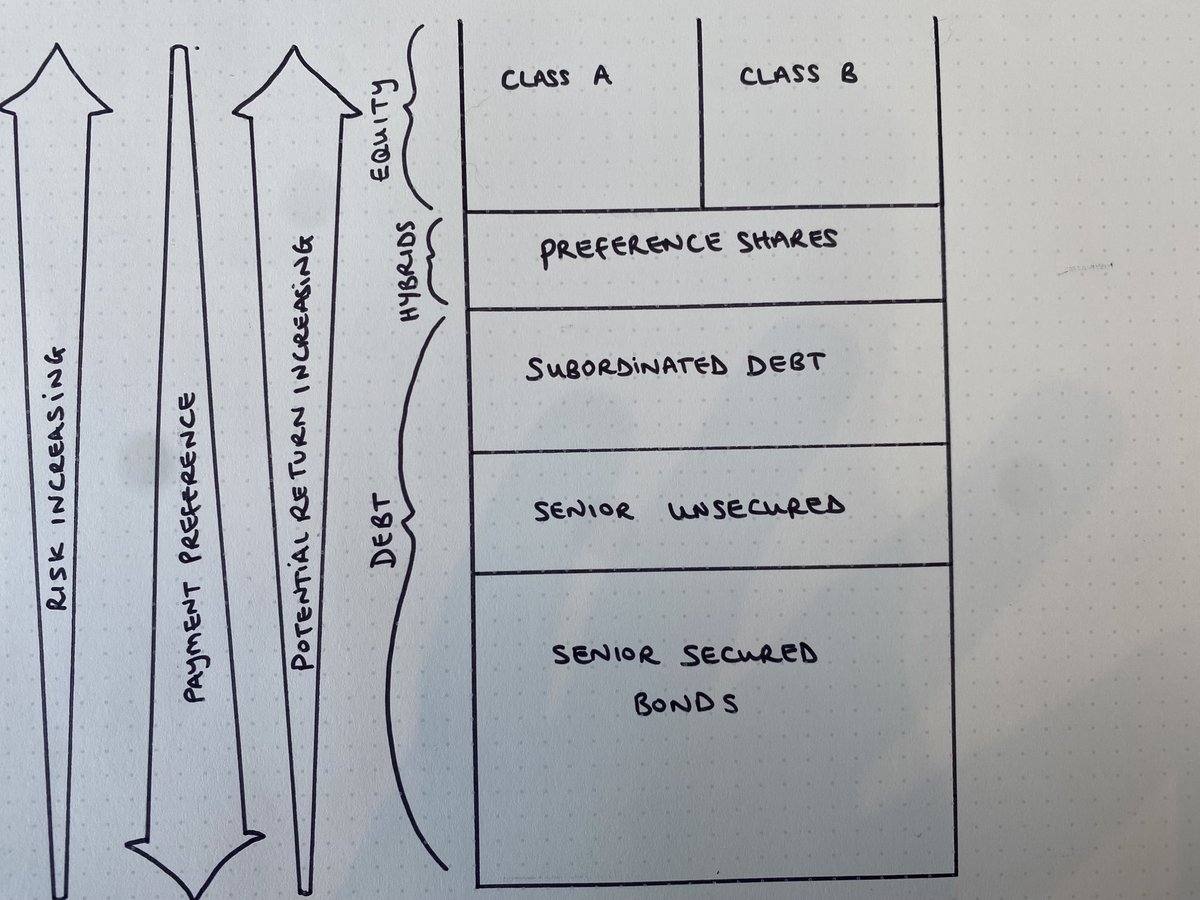

I visualize this in a table.

I put the most senior ranking debt at the bottom.

Yes, this is upside down to the way you may have seen this presented before.

What can I say, I'm a rebel 😎

I put the most senior ranking debt at the bottom.

Yes, this is upside down to the way you may have seen this presented before.

What can I say, I'm a rebel 😎

Those at the bottom of the chart get fed first.

If things go wrong. They get paid off first.

They are taking less risk. But also earn less return.

If things go wrong. They get paid off first.

They are taking less risk. But also earn less return.

The folk at the top of the list eat last.

But they get whatever’s left over. And if the company is successful that could be a hell of a banquet.

Higher risk = higher return

But they get whatever’s left over. And if the company is successful that could be a hell of a banquet.

Higher risk = higher return

Once I have my table, I would start to build a picture through the numbers, of what’s important. I’m looking for:

a) Maturity.

b) Leverage for each class (Net Debt: EBITDA)

c) Covenant headroom

d) Interest Cover (& Sensitivity)

It would look something like this

a) Maturity.

b) Leverage for each class (Net Debt: EBITDA)

c) Covenant headroom

d) Interest Cover (& Sensitivity)

It would look something like this

Note: Beware of debt dressed up as something else.

For example ...

Many receivables finance are designed to be 'off balance sheet debt.'

This means rather than it looking like debt, it is presented like an early payment of a receivable.

For example ...

Many receivables finance are designed to be 'off balance sheet debt.'

This means rather than it looking like debt, it is presented like an early payment of a receivable.

F*ck the accounting treament.

If it looks and smells like sh*t... very rarely is it Nutella.

Beware pension deficits, and other debt-like things with clever balance sheet presentation.

(In red in my earlier example)

If it looks and smells like sh*t... very rarely is it Nutella.

Beware pension deficits, and other debt-like things with clever balance sheet presentation.

(In red in my earlier example)

Equally, do you understand the equity:

Is there more than one class of shares?

What are the voting right?

Does anyone have effective control?

Effective blocking stakes?

Any preferred dividends?

Is there more than one class of shares?

What are the voting right?

Does anyone have effective control?

Effective blocking stakes?

Any preferred dividends?

There’s more to say on capital strucure, but that’s how you get an overview of who actually owns the business, and where the real power lies.

Done well, you should be able to quickly see the immediate issues facing the business in the capital structure.

Done well, you should be able to quickly see the immediate issues facing the business in the capital structure.

2. Working Capital

This is important, because it tells you how cash cycles through the business.

But it tells you something else. Something that people oftentimes miss.

It tells you what it will cost to grow the business

I'll explain

This is important, because it tells you how cash cycles through the business.

But it tells you something else. Something that people oftentimes miss.

It tells you what it will cost to grow the business

I'll explain

Working capital cycle is often measured in days.

Not how I like to do it (I'll come back to that in a minute). But it is well understood and effective.

Lets say a company has 30 days of receivables 15 days of inventory 25 days of payables

Not how I like to do it (I'll come back to that in a minute). But it is well understood and effective.

Lets say a company has 30 days of receivables 15 days of inventory 25 days of payables

The cash conversion cycle is +20 days. (30 + 15 - 35)

That means you need to have 20 days of sales (in cash) tied up in your working capital cycle.

If your sales grow, so does that funding requirement.

Expensive.

That means you need to have 20 days of sales (in cash) tied up in your working capital cycle.

If your sales grow, so does that funding requirement.

Expensive.

I once worked for a retailer once who had a cash conversion cycle of -60 days.

Yes that's a minus.

(zero receivables, 15 days inventory, 75 days payables).

We were growing aggressively.

Yes that's a minus.

(zero receivables, 15 days inventory, 75 days payables).

We were growing aggressively.

We would build two stores a week at a capex cost of $10m per store.

but the minute we opened the doors we would get $5m back in working capital inflow (because of that - 60 days)

I.e. we were collecting cash for the first 60 days of opening before we had to pay anyone.

but the minute we opened the doors we would get $5m back in working capital inflow (because of that - 60 days)

I.e. we were collecting cash for the first 60 days of opening before we had to pay anyone.

Cash on cash , the working capital profile DOUBLED our returns.

To put it another way. The suppliers were paying for half of the build cost of EVERY new store.

WUN-DER-FUL

To put it another way. The suppliers were paying for half of the build cost of EVERY new store.

WUN-DER-FUL

I love that story.

Anyway, how do I measure working capital?

Well the calc is like cash conversion cycle, except I don't express it in days.

I like to use 'cents in the dollar' in net working capital expressed in revenue

I’ll explain

Anyway, how do I measure working capital?

Well the calc is like cash conversion cycle, except I don't express it in days.

I like to use 'cents in the dollar' in net working capital expressed in revenue

I’ll explain

If receivables are $100m, payables are $70m, Inventory is $50m and revenue is 2bn

Then my net working capital is +80m. Which is 4% of revenue.

OR ... For every $1 of marginal revenue we need to assume it will cost us 4 cents in working capital.

Then my net working capital is +80m. Which is 4% of revenue.

OR ... For every $1 of marginal revenue we need to assume it will cost us 4 cents in working capital.

I like this because it gives me a quick short cut to understand the cash impact of growth.

If I know my P&L contribution % is 20% . Then I know my net CASH contribution from marginal sales (Assuming no capex required) is 16% (20% minus 4%).

This is on marginal sales only.

If I know my P&L contribution % is 20% . Then I know my net CASH contribution from marginal sales (Assuming no capex required) is 16% (20% minus 4%).

This is on marginal sales only.

3. Liquidity.

This is for the paranoid amongst us.

Job number 1, whether you are CFO, an Investor?

Make sure the business doesn’t go bust.

And remember it's only ever running out of cash that will send you bust.

This is for the paranoid amongst us.

Job number 1, whether you are CFO, an Investor?

Make sure the business doesn’t go bust.

And remember it's only ever running out of cash that will send you bust.

Now for any business, there is a set of circumstances at any given time, that could send that business bust.

No business has infinite cash resources.

So the question we need to answer, is how much available cash does the business really have?

No business has infinite cash resources.

So the question we need to answer, is how much available cash does the business really have?

The good news is that the cash number in the balance sheet is easy to find.

The bad news is that that number is only at a moment in time.

And if you are looking at an annual report, that point is the year end

The bad news is that that number is only at a moment in time.

And if you are looking at an annual report, that point is the year end

In many businesses the year end cash balance is higher than at any other point in the year.

This thread is already too long, so I’ll have to tackle why this is another time.

But to give 1 simple example.

Let’s say we are in the ice cream business with an August year end...

This thread is already too long, so I’ll have to tackle why this is another time.

But to give 1 simple example.

Let’s say we are in the ice cream business with an August year end...

By the end of August, our cash balance probably looks quite healthy.

A long balmy summer of selling sweet frozen treats.

But how about in March?

We've had 6 months of building stock (lots of cash out), with very little sales (no cash in)

A long balmy summer of selling sweet frozen treats.

But how about in March?

We've had 6 months of building stock (lots of cash out), with very little sales (no cash in)

So understanding how much cash is needed to allow for this volatility is really all that matters when considering how much liquidity is needed.

So we take the cash balance at the balance sheet date, deduct off whatever is a reasonable estimate for volatility.

Then....

So we take the cash balance at the balance sheet date, deduct off whatever is a reasonable estimate for volatility.

Then....

We add back any undrawn facilities. I.e. is there an overdraft, an RCF, or receivables facility that we can use if needed?

This is all liquidity headroom if needed. (And often can be used to fund the seasonality issued I described).

This illustration will explain

This is all liquidity headroom if needed. (And often can be used to fund the seasonality issued I described).

This illustration will explain

From this calculate a best estimate of true liquidity headroom.

Then convert this to the number of days revenue.

I.e. for how many days could we go without any revenue before the business is bust?

Then convert this to the number of days revenue.

I.e. for how many days could we go without any revenue before the business is bust?

This is a calculation many businesses did (having never done it before) at the start of COVID.

I.e. if something awful happened and our sales disappeared. How long do I have before I'm out of business.

If it sounds like I'm paranoid about running out of cash, it's because I am.

You should be too.

It's sucks.

If it sounds like I'm paranoid about running out of cash, it's because I am.

You should be too.

It's sucks.

TLDR

The 3 most important things you can read from a balance sheet:

1. Capital Structure - who owns the business, and how is it funded

2. Working Capital - what will happen to cash as I grow (or shrink)

3. Liquidity. How much available cash do I actually have?

The 3 most important things you can read from a balance sheet:

1. Capital Structure - who owns the business, and how is it funded

2. Working Capital - what will happen to cash as I grow (or shrink)

3. Liquidity. How much available cash do I actually have?

If you liked it. Please

1. Follow @SecretCFO for more crispy finance threads

2. Retweet the original post so more people see this

1. Follow @SecretCFO for more crispy finance threads

2. Retweet the original post so more people see this

Loading suggestions...