$GOOG 3Q'22 Earnings Update

"There's no question we're operating in an uncertain environment"

Summertime is over, and winter is almost here.

Here are some of my highlights from 3Q'22.

"There's no question we're operating in an uncertain environment"

Summertime is over, and winter is almost here.

Here are some of my highlights from 3Q'22.

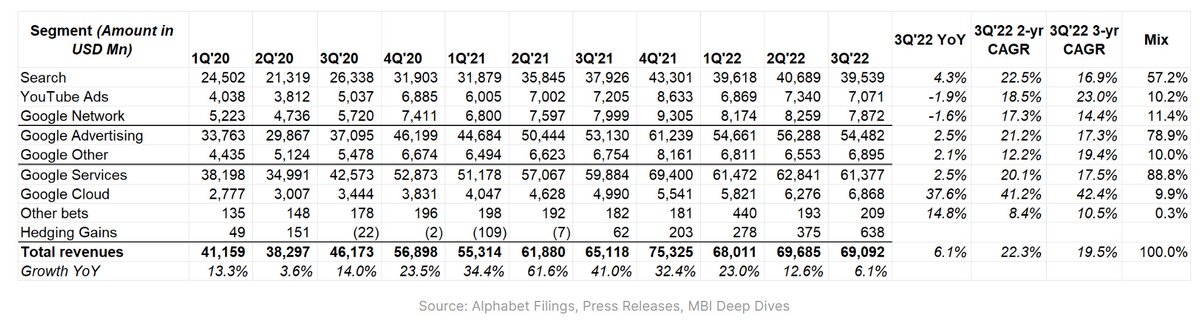

First things first, there was 5% FX headwind, so FXN revenue was +11%.

YouTube ads and Google Network revenue declined YoY. Cloud continued its growth momentum.

YouTube ads and Google Network revenue declined YoY. Cloud continued its growth momentum.

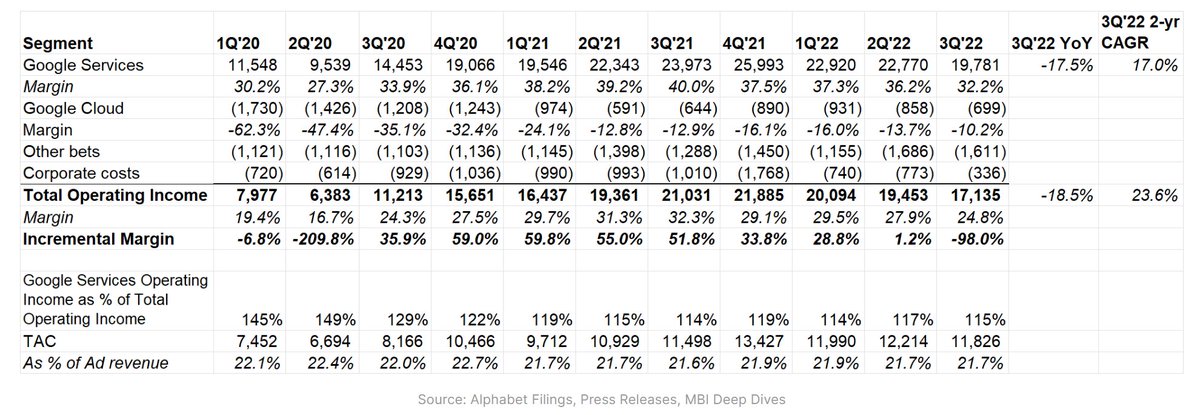

While Google Services EBIT declined by 17.5% YoY, given FX is a larger headwind for EBIT, EBIT declined by ~7-8% YoY FXN.

Google Cloud's margin was -10.2% which was its highest ever. Cloud is likely to be a nice tailwind for margin in 2023.

Google Cloud's margin was -10.2% which was its highest ever. Cloud is likely to be a nice tailwind for margin in 2023.

Search

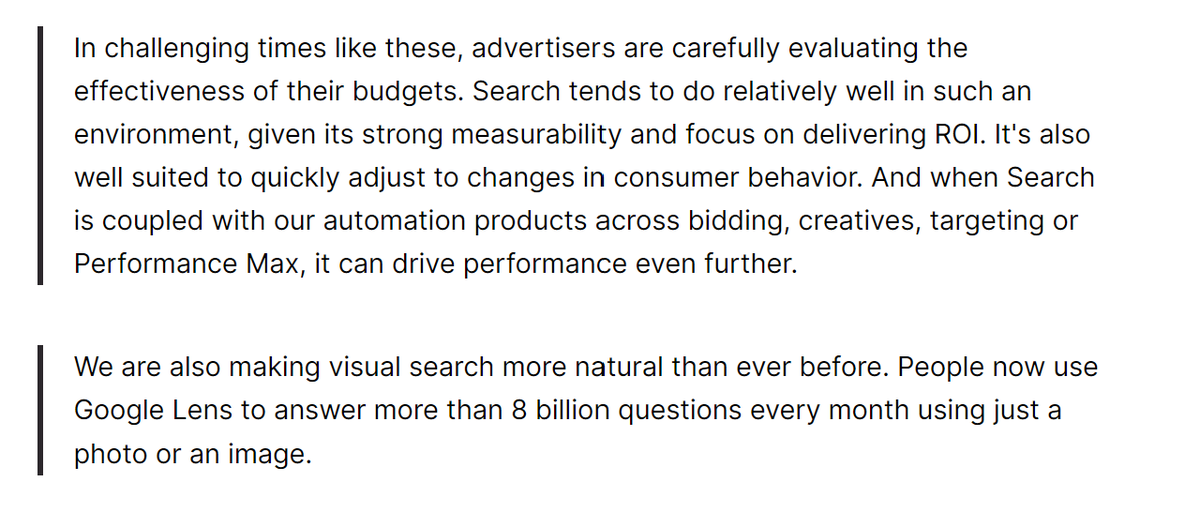

Google is optimistic about Search's performance during the economic downturn:

Google is optimistic about Search's performance during the economic downturn:

YouTube

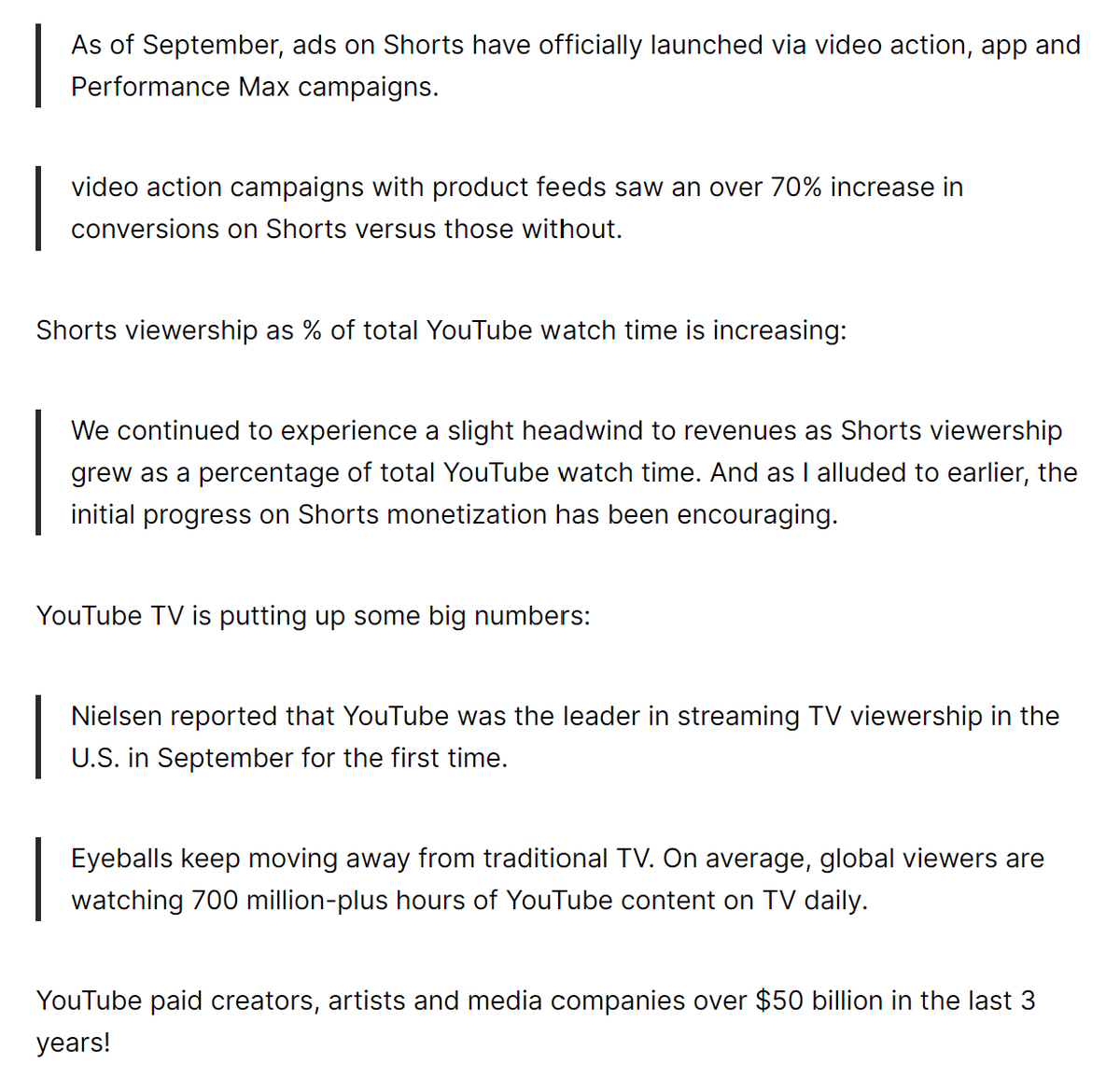

While YouTube ads declined YoY, YouTube non-advertising revenue increased YoY driven by Music Premium and YouTube TV.

Revenue sharing on Shorts will arrive early next year.

While YouTube ads declined YoY, YouTube non-advertising revenue increased YoY driven by Music Premium and YouTube TV.

Revenue sharing on Shorts will arrive early next year.

YouTube Shorts are watched by 1.5 billion users every month which lead to >30 billion daily views.

Google mentioned the exact same numbers in Q1 and Q2. Does that mean Shorts DAU/MAU is not growing?

At least, Shorts monetization is here:

Google mentioned the exact same numbers in Q1 and Q2. Does that mean Shorts DAU/MAU is not growing?

At least, Shorts monetization is here:

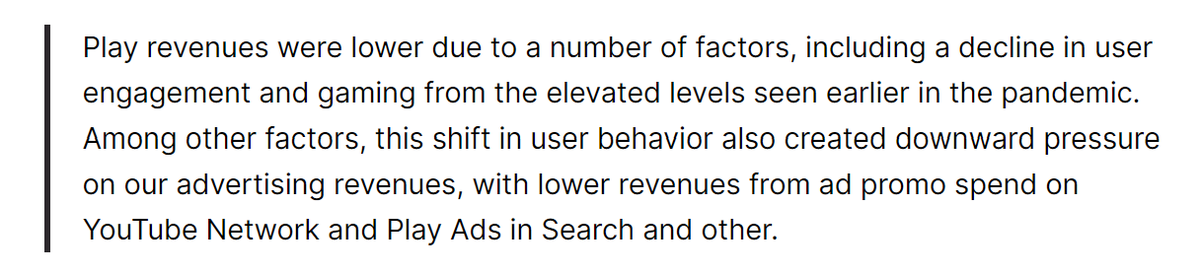

Play revenues declined YoY (see more in the image)

More advertisers pulled back in Q3. Some sectors that pulled back within financial services (for example): insurance, loan, mortgage and crypto subcategories.

More advertisers pulled back in Q3. Some sectors that pulled back within financial services (for example): insurance, loan, mortgage and crypto subcategories.

Cloud

"Google Workspace is now used by more than 8 million businesses and organizations worldwide" (earlier disclosure: 5 mn in Feb'19, 6 mn in Apr'20)

Cloud may not be immune from macro softness:

"Google Workspace is now used by more than 8 million businesses and organizations worldwide" (earlier disclosure: 5 mn in Feb'19, 6 mn in Apr'20)

Cloud may not be immune from macro softness:

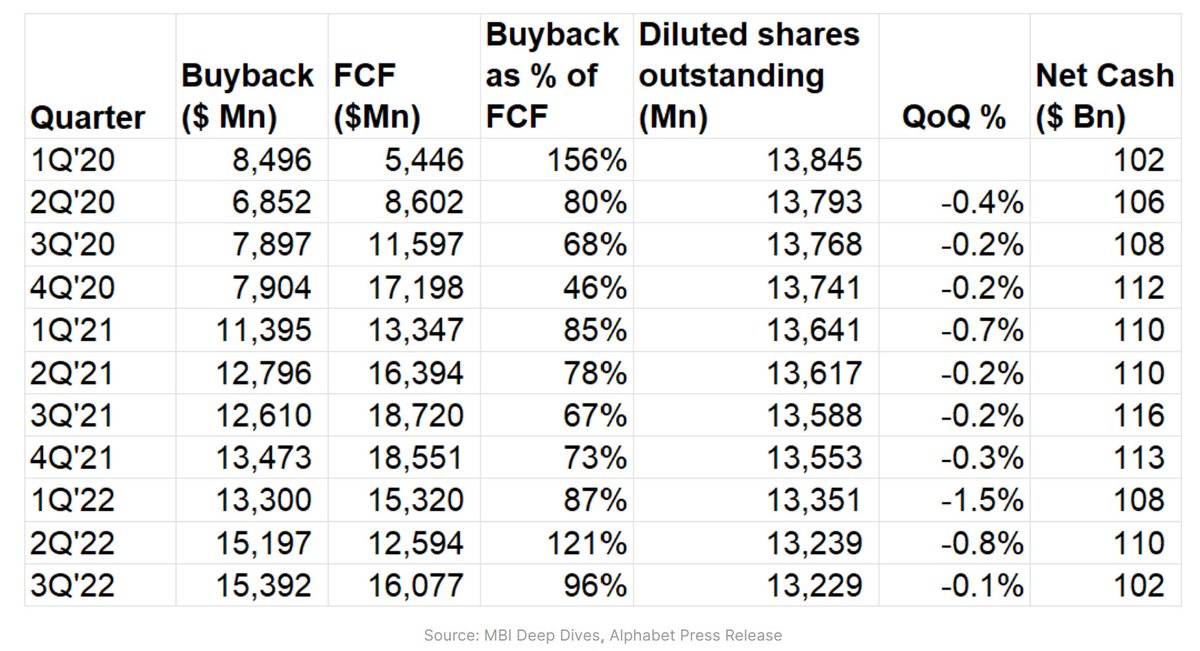

Buyback

One disappointing aspect from the earnings was slower buyback cadence. One would imagine this is the time to use the $100 Bn net cash to put it to some good use. Even more disappointing is shares outstanding is barely budging despite the buybacks.

One disappointing aspect from the earnings was slower buyback cadence. One would imagine this is the time to use the $100 Bn net cash to put it to some good use. Even more disappointing is shares outstanding is barely budging despite the buybacks.

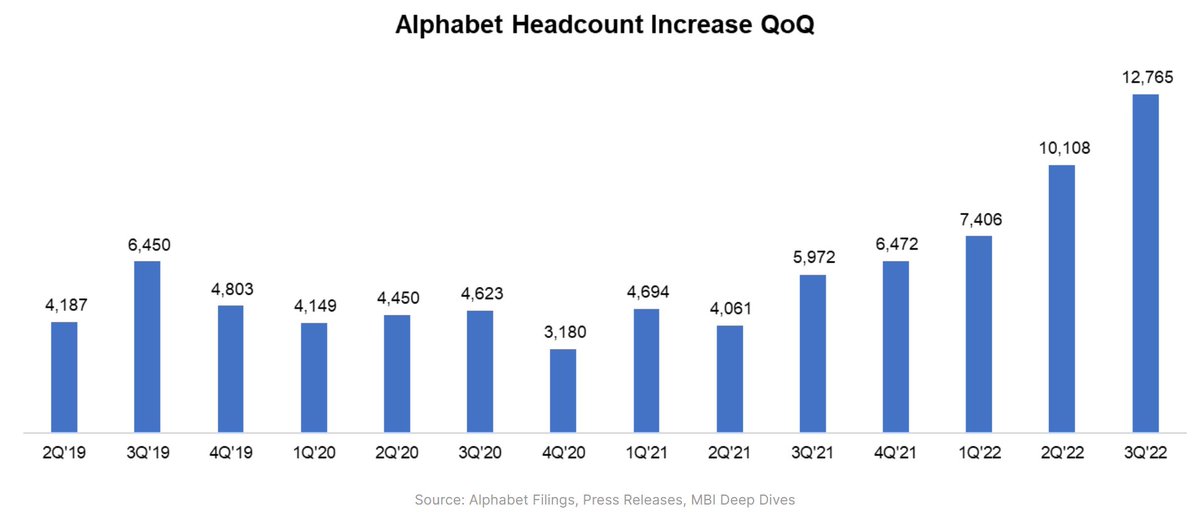

That's probably not surprising when you see the headcount (+12.8k QoQ, excluding Mandiant acquisition ~10k QoQ).

I hope you are sitting, because I'm going to say something astonishing:

I hope you are sitting, because I'm going to say something astonishing:

Number of headcount added by Google in the last 14 quarters (2Q'19-3Q'22) = Meta's total employees as of 2Q'22

Google management, however, promised that Q4 headcount add will be less than half of Q3, and 2023 will exhibit more cost discipline in terms of headcount add.

Google management, however, promised that Q4 headcount add will be less than half of Q3, and 2023 will exhibit more cost discipline in terms of headcount add.

Capex

Capex YTD $23.8 Bn (vs $24.6 Bn for full year of 2021)

"servers really has been the largest driver of the investment dollars. The technical infrastructure team has consistently focused on levers to improve utilization and efficiency and they continue to do so."

Capex YTD $23.8 Bn (vs $24.6 Bn for full year of 2021)

"servers really has been the largest driver of the investment dollars. The technical infrastructure team has consistently focused on levers to improve utilization and efficiency and they continue to do so."

Outlook

Google expects even larger FX headwind in Q4

"In the fourth quarter, the very strong revenue performance last year will continue to create tough comps that will weigh on the year-on-year growth rates of advertising revenues."

Google expects even larger FX headwind in Q4

"In the fourth quarter, the very strong revenue performance last year will continue to create tough comps that will weigh on the year-on-year growth rates of advertising revenues."

Valuation

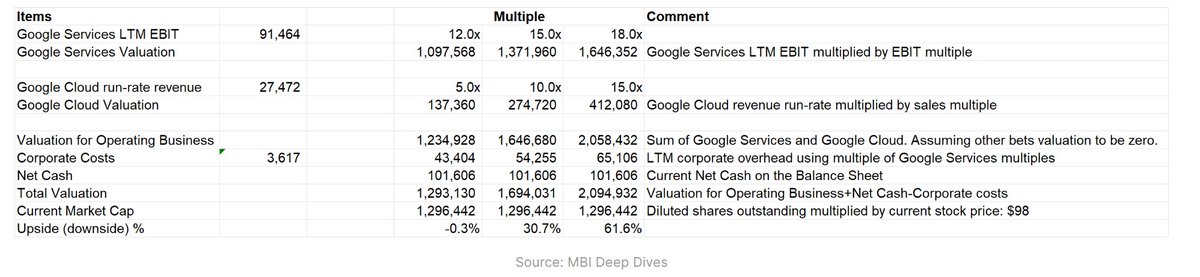

It is hard to argue Google's valuation is expensive. The core Google Service business is trading at ~12x LTM EBIT if we value Google Cloud at 5x run-rate revenue.

But let's hope they don't add a "Meta" in the next 3-4 years in their headcount.

It is hard to argue Google's valuation is expensive. The core Google Service business is trading at ~12x LTM EBIT if we value Google Cloud at 5x run-rate revenue.

But let's hope they don't add a "Meta" in the next 3-4 years in their headcount.

Website version of this thread: mbi-deepdives.com

I will post my thoughts on $SPOT earnings later tonight. Subscribe here: mbi-deepdives.com

I will post my thoughts on $SPOT earnings later tonight. Subscribe here: mbi-deepdives.com

Correction to Buyback data

Loading suggestions...