Professional options traders don’t take directional bets.

They spend their time finding mispricings.

Usually, they start with GARCH.

Here’s how you can too:

They spend their time finding mispricings.

Usually, they start with GARCH.

Here’s how you can too:

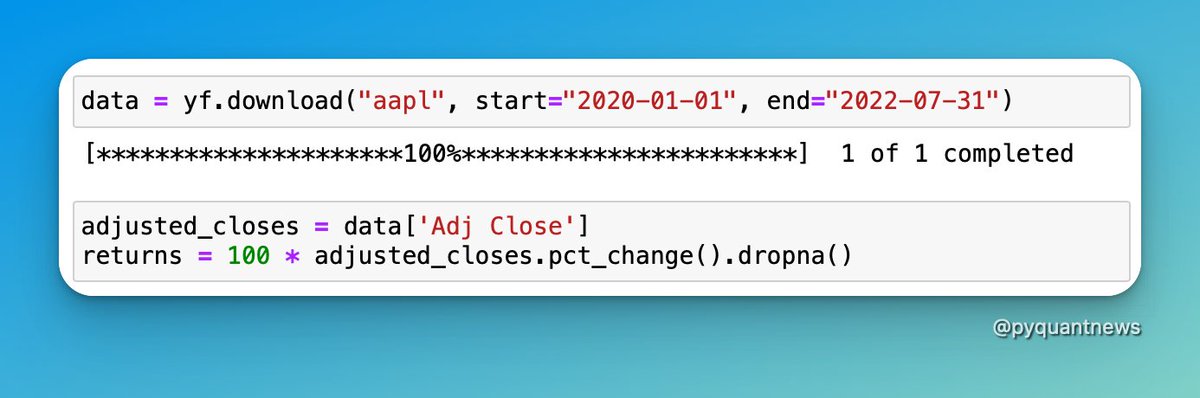

1/ Get data

Use yfinance to download data and compute the returns.

Use yfinance to download data and compute the returns.

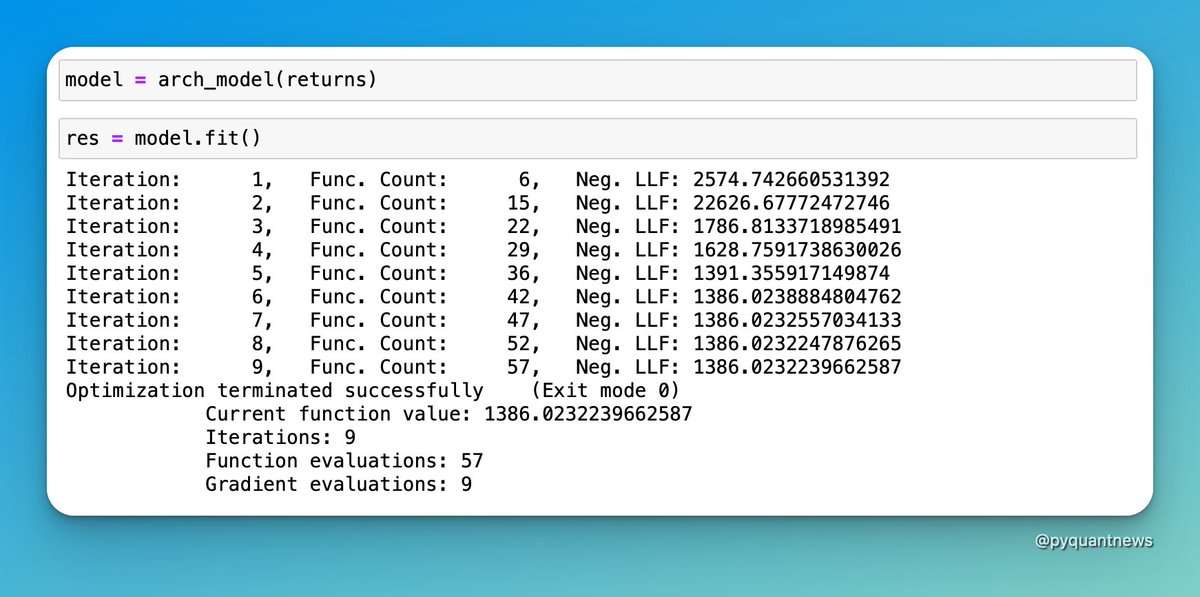

2/ Fit a GARCH model

Use the excellent arch package to fit a GARCH model.

Use the excellent arch package to fit a GARCH model.

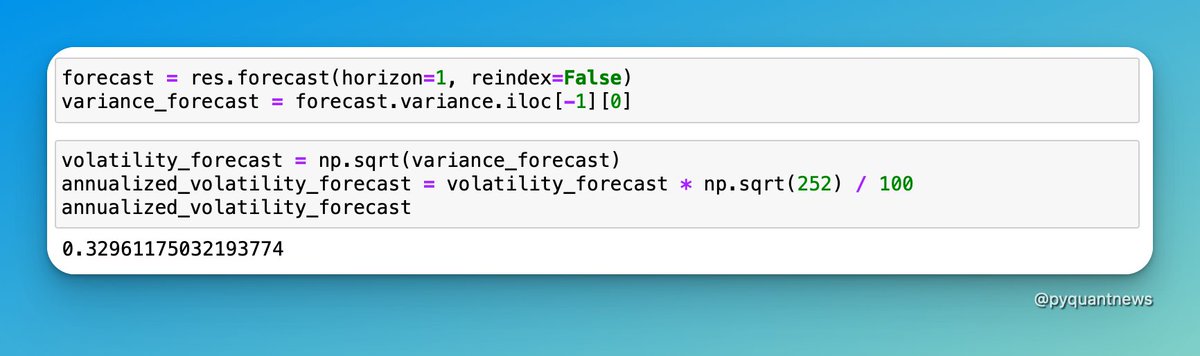

3/ Forecast volatility

Get the variance forecast, take the square root, and annualize.

Get the variance forecast, take the square root, and annualize.

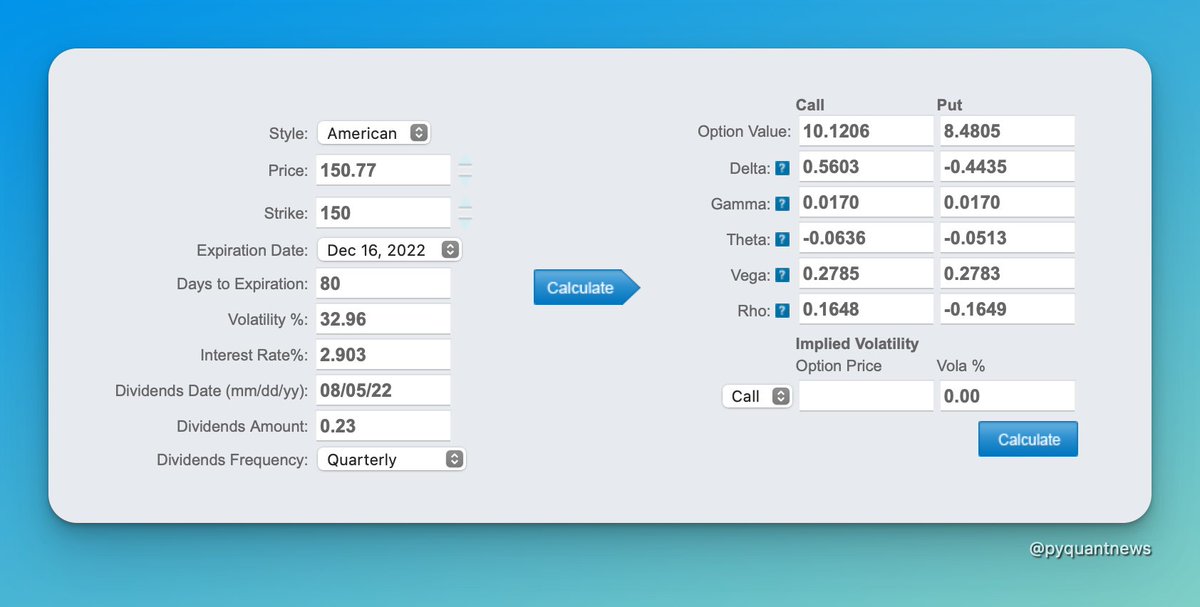

4/ Find mispricings

Use your forecast in the pricing model.

Compare the value to the market.

If your forecast shows a lower price, buy.

Higher price, sell.

Use your forecast in the pricing model.

Compare the value to the market.

If your forecast shows a lower price, buy.

Higher price, sell.

I break down the details in a recent newsletter.

• Data

• GARCH

• Mipricings

And more…

Read it here, for free:

pyquantnews.com

• Data

• GARCH

• Mipricings

And more…

Read it here, for free:

pyquantnews.com

Getting Started With Python for Quant Finance.

Go from complete beginner to up and running with Python for quant finance in 30 days.

• Community

• Frameworks

• Live sessions

• Special guests

• Jupyter Notebooks

Starts 13 November - only 50 spots.

gettingstartedwithpythonforquantfinance.com

Go from complete beginner to up and running with Python for quant finance in 30 days.

• Community

• Frameworks

• Live sessions

• Special guests

• Jupyter Notebooks

Starts 13 November - only 50 spots.

gettingstartedwithpythonforquantfinance.com

Loading suggestions...