In 2017, Economist Richard Thaler won the Nobel Prize for his research on a concept called "Nudge Theory".

But, fintech companies have been using "nudging" principles for over a decade to game your dopamine receptors.

Here's how they do it 🧵

But, fintech companies have been using "nudging" principles for over a decade to game your dopamine receptors.

Here's how they do it 🧵

"Nudge Theory" essentially states that humans will default to the path of least resistance when making any decision.

But, with a proper "nudge", we can be incentivized to make smarter, healthier decisions for ourselves.

At least, that was the original intent.

But, with a proper "nudge", we can be incentivized to make smarter, healthier decisions for ourselves.

At least, that was the original intent.

For example, if you want to start eating better, you can meal prep healthy lunches for the week.

If you want to save more money, you can set up auto-transfers to your savings account.

The key is to reduce the number of decisions you need to make to build that positive habit.

If you want to save more money, you can set up auto-transfers to your savings account.

The key is to reduce the number of decisions you need to make to build that positive habit.

However, from Thaler's research, we learned that these "nudges" can be used to influence us in any direction.

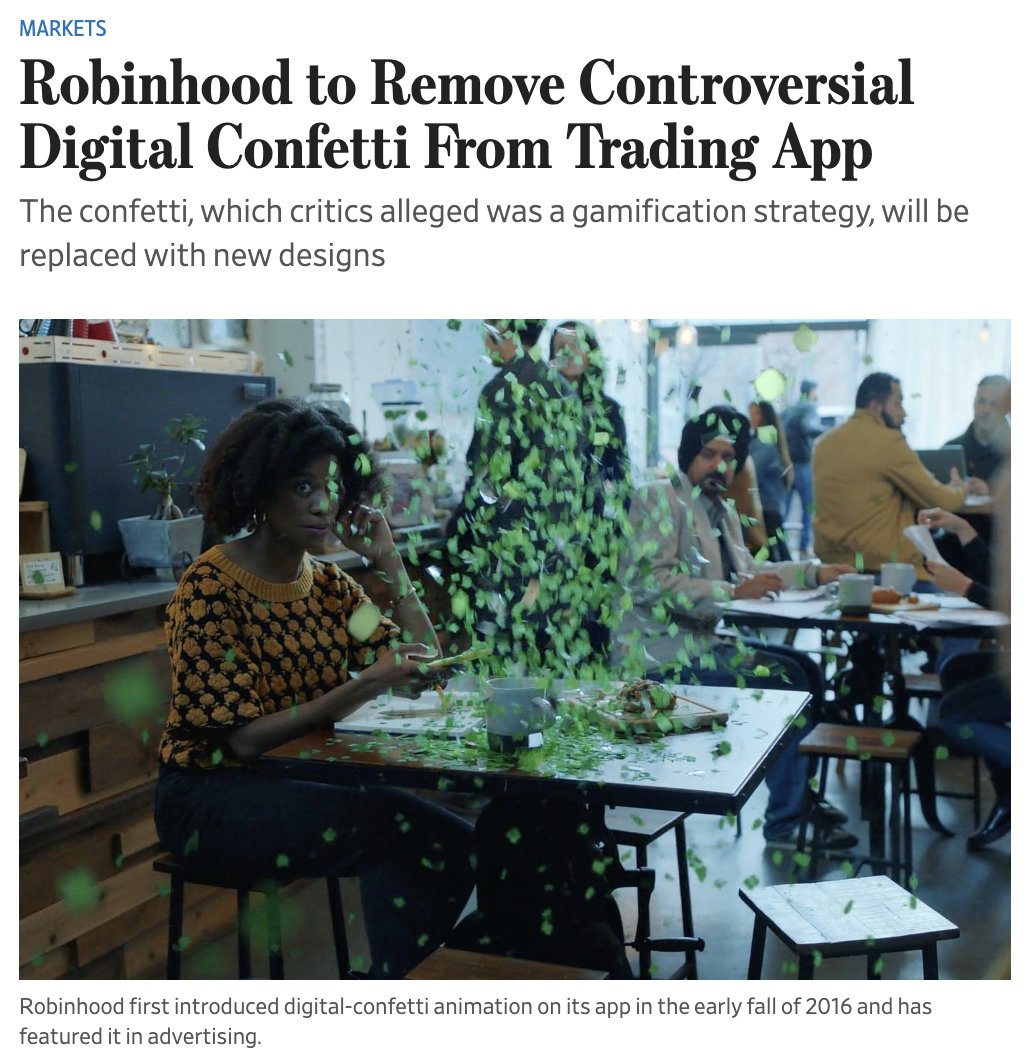

That confetti you used to see on Robinhood after buying a stock? That was a nudge, too.

No industry is more reliant on those little nudges than fintech.

That confetti you used to see on Robinhood after buying a stock? That was a nudge, too.

No industry is more reliant on those little nudges than fintech.

For years, buy-now-pay-later (BNPL) companies like Klarna have enlisted the help of researchers to learn how people behave when shopping online.

Using the results, they help eCommerce brands optimize their shopping experience to make us spend more.

(With Klarna's help, ofc)

Using the results, they help eCommerce brands optimize their shopping experience to make us spend more.

(With Klarna's help, ofc)

So what exactly did they learn?

Well, there are two main types of online shoppers:

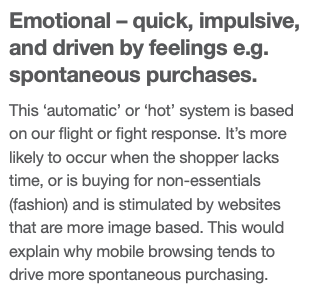

Emotional shoppers — Impulsive and driven by emotions based on our fight-or-flight response.

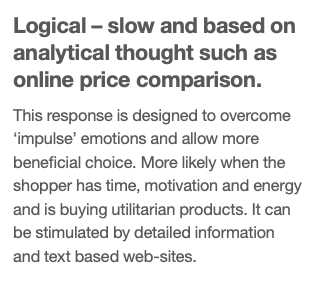

Logical shoppers — Slow and analytical, with a response meant to overcome that 'impulse'.

Well, there are two main types of online shoppers:

Emotional shoppers — Impulsive and driven by emotions based on our fight-or-flight response.

Logical shoppers — Slow and analytical, with a response meant to overcome that 'impulse'.

The key to maximizing eCommerce sales while reducing cart abandonment is to:

1. Trigger that fight-or-flight response and reduce friction before you second-guess your purchase.

2. Minimize feelings of shame or regret post-purchase so you're more likely to return.

1. Trigger that fight-or-flight response and reduce friction before you second-guess your purchase.

2. Minimize feelings of shame or regret post-purchase so you're more likely to return.

Basically, BNPL companies are using "nudges" to create positive emotions associated with shopping online.

This is also why BNPL is so effective for consumer goods like clothing and cosmetics that often rely on impulse purchases.

I call this the "Treat Yo Self" Effect.

This is also why BNPL is so effective for consumer goods like clothing and cosmetics that often rely on impulse purchases.

I call this the "Treat Yo Self" Effect.

Don't believe me?

This is a direct quote from one of Klarna's eCommerce research reports.

“Often resulting from lapses of self control, inner strength or resolve, unplanned purchases can be lucrative for retailers”

This is a direct quote from one of Klarna's eCommerce research reports.

“Often resulting from lapses of self control, inner strength or resolve, unplanned purchases can be lucrative for retailers”

So how is that fight-or-flight response triggered?

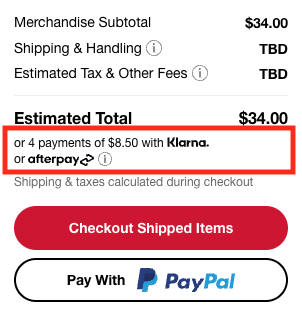

An eCommerce site might offer sales, limited discounts, or product recommendations — All to get to the checkout page quickly.

The BNPL strategy is to hit the brain's reward center while delaying any anxiety around the purchase.

An eCommerce site might offer sales, limited discounts, or product recommendations — All to get to the checkout page quickly.

The BNPL strategy is to hit the brain's reward center while delaying any anxiety around the purchase.

How do they reduce friction?

BNPL strives to make the checkout process completely seamless. Too much friction and Emotional shoppers will second-guess themselves.

eCommerce brands will set BNPL as the default payment method. These "Altering Defaults" are very powerful nudges.

BNPL strives to make the checkout process completely seamless. Too much friction and Emotional shoppers will second-guess themselves.

eCommerce brands will set BNPL as the default payment method. These "Altering Defaults" are very powerful nudges.

How do they avoid regret?

By offering cost-free return policies and price guarantees.

Klarna also found that, "Consumers rarely search any further once purchase has been made."

"Once they have the goods, the ‘endowment’ effect normally reduces their desire to make a return.”

By offering cost-free return policies and price guarantees.

Klarna also found that, "Consumers rarely search any further once purchase has been made."

"Once they have the goods, the ‘endowment’ effect normally reduces their desire to make a return.”

BNPL, like any credit product, is a tool.

But with no consumer protections in place, that tool can also harm people who misuse it.

That's why ~43% of BNPL users have made a late payment at some point.

But there's good news, too!

But with no consumer protections in place, that tool can also harm people who misuse it.

That's why ~43% of BNPL users have made a late payment at some point.

But there's good news, too!

Like I said, you can be nudged in either direction.

By using these tools differently, BNPL can complement credit cards.

Another study found that "repayment by purchase" (like BNPL) increased the chance that purchases are paid off instead of sitting for months on a credit card.

By using these tools differently, BNPL can complement credit cards.

Another study found that "repayment by purchase" (like BNPL) increased the chance that purchases are paid off instead of sitting for months on a credit card.

So while BNPL can be an effective tool to help people manage their personal credit and cash flow, it can also be harmful.

But if you know about the triggers and "nudges" that BNPL companies put in place, it's easier to avoid their pitfalls.

But if you know about the triggers and "nudges" that BNPL companies put in place, it's easier to avoid their pitfalls.

Want to learn more about how Fintech companies operate?

Sign up for my 2x weekly newsletter!

workweek.com

Sign up for my 2x weekly newsletter!

workweek.com

Loading suggestions...