How is GammaSwap innovating upon the current AMM model and as an LP how can I profit off IL? 🧠

A 🧵on impermanent gainzzz 💪👇

A 🧵on impermanent gainzzz 💪👇

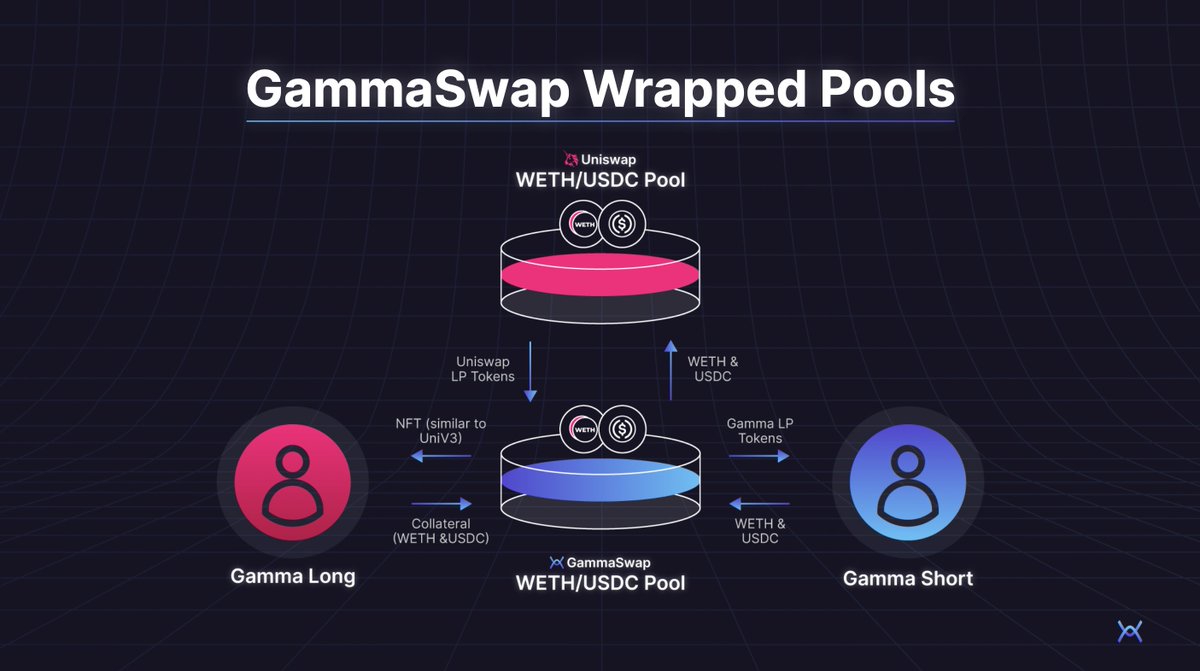

There are two participants in the GammaSwap model. LPs who are short gamma (short volatility) and borrowers who are long gamma.

In the case of a Uniswap ETH/USDC pool, the LP could create a position with the reserve tokens (ETH & USDC) or directly with the UniLP tokens.

1/n

In the case of a Uniswap ETH/USDC pool, the LP could create a position with the reserve tokens (ETH & USDC) or directly with the UniLP tokens.

1/n

Let’s say the LP deposited the reserve tokens in ETH / USDC. GammaSwap would deposit those underlying tokens into Uniswap, receive the UniLP tokens and hold on to the UniLP tokens in the smart contract.

GammaSwap would then issue the LP a GammaSwap (GS) ERC-20 LP token.

2/n

GammaSwap would then issue the LP a GammaSwap (GS) ERC-20 LP token.

2/n

The GS LP token is similar to a UniLP token except it earns the interest rate from those borrowing the liquidity (long gamma)

Uniswap P&L = fees(volume) - IL(volatility)

GammaSwap P&L = fees(volume) + Interest rate(long vol) - IL(short vol)

GS returns >= Uniswap returns

3/n

Uniswap P&L = fees(volume) - IL(volatility)

GammaSwap P&L = fees(volume) + Interest rate(long vol) - IL(short vol)

GS returns >= Uniswap returns

3/n

The yield in GammaSwap for an LP will always be greater than or equal to the underlying AMM. The extra yield is dependent on the demand for gamma.

The only additional risk as an LP is the smart contract risk which we will mitigate through an audit with @HalbornSecurity

4/n

The only additional risk as an LP is the smart contract risk which we will mitigate through an audit with @HalbornSecurity

4/n

Even if an LP isn’t hedging IL (borrowing liquidity or using vaults) they will still be better compensated for their risk they are taking.

In periods of higher IL, the demand for volatility will increase & the LP will earn more fees from the interest rate on borrowers.

5/n

In periods of higher IL, the demand for volatility will increase & the LP will earn more fees from the interest rate on borrowers.

5/n

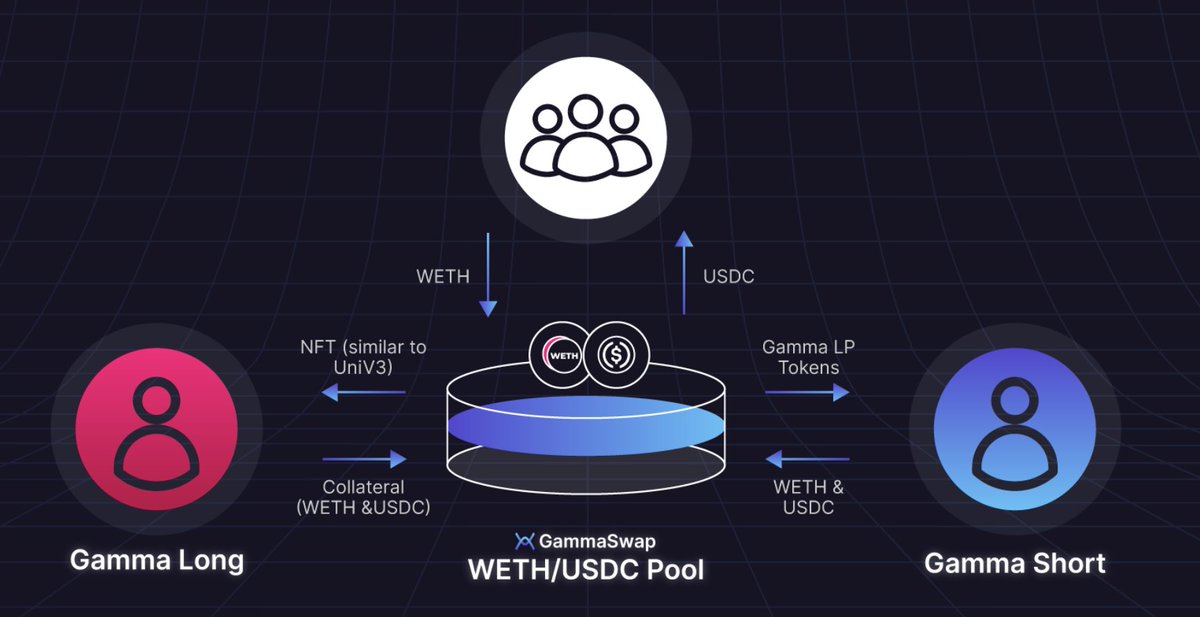

On the other side, you have those who are borrowing the liquidity or longing gamma.

To open a long gamma position, the user would deposit collateral in the form of the reserve tokens (ETH / USDC). They will receive an NFT similar to Uniswap V3 that manages their loan.

6/n

To open a long gamma position, the user would deposit collateral in the form of the reserve tokens (ETH / USDC). They will receive an NFT similar to Uniswap V3 that manages their loan.

6/n

When a user opens this position, GammaSwap redeems the UniLP token for the underlying tokens and creates a synthetic LP token. An index is used to track the fees earned had the LP position not been burned + the interest rate.

7/n

7/n

The loan must maintain a 90% LTV ratio to remain healthy. If the loan crosses this threshold, it will get liquidated.

As the underlying tokens move in either direction, the loan becomes over collateralized and the user is able to buy more LP tokens with the reserve tokens.

8/n

As the underlying tokens move in either direction, the loan becomes over collateralized and the user is able to buy more LP tokens with the reserve tokens.

8/n

Now anyone is able to take the exact opposite risk position of an LP turning their IL into impermanent gainz 💪

This service can be applied to any liquidity pool in any AMM and is not reliant on an oracle, unlike normal hedging solutions ex. perps or Aave shorts.

9/n

This service can be applied to any liquidity pool in any AMM and is not reliant on an oracle, unlike normal hedging solutions ex. perps or Aave shorts.

9/n

Opening a long gamma position could be leveraged for multiple strategies:

1. A leveraged bet on volatility on any token pair

2. Hedging IL

3. Protecting oneself against a rug pull in a new project

10/n

1. A leveraged bet on volatility on any token pair

2. Hedging IL

3. Protecting oneself against a rug pull in a new project

10/n

GammaSwap solves multiple issues with current DeFi options markets: fragmentation of liquidity, mispricing of IV, narrow range of asset exposure, etc. while maintaining the optionality of normal volatility trading.

11/n

11/n

For example, a long gamma trader can change the reserve ratio of the tokens he uses as collateral. Perhaps in this scenario he decides to deposit 80% ETH & 20% USDC instead of a 50/50 ratio.

12/n

12/n

This changes the Δ of the position enabling him to hedge his IL with a smaller position size or essentially take a leveraged bet on the price of ETH. More here: medium.com

13/n

13/n

In conclusion, GS enables vol trading on a wider range of assets and is a superior method for hedging an LP position.

Normal hedging strategies are limited by oracles and aren’t a perfect hedge (Δ of a perp is 1:1 while Δ of an AMM changes w price)

14/n

Normal hedging strategies are limited by oracles and aren’t a perfect hedge (Δ of a perp is 1:1 while Δ of an AMM changes w price)

14/n

Loading suggestions...