Monthly Macro Recap - October

Let's dive in🧵

Let's dive in🧵

US Equities outperformed, with the Dow Jones putting up one of its strongest months on record - driven primarily by UNH, GS, MCD, and AMGN. Meanwhile, Chinese tech equities were decimated following Xi's re-election.

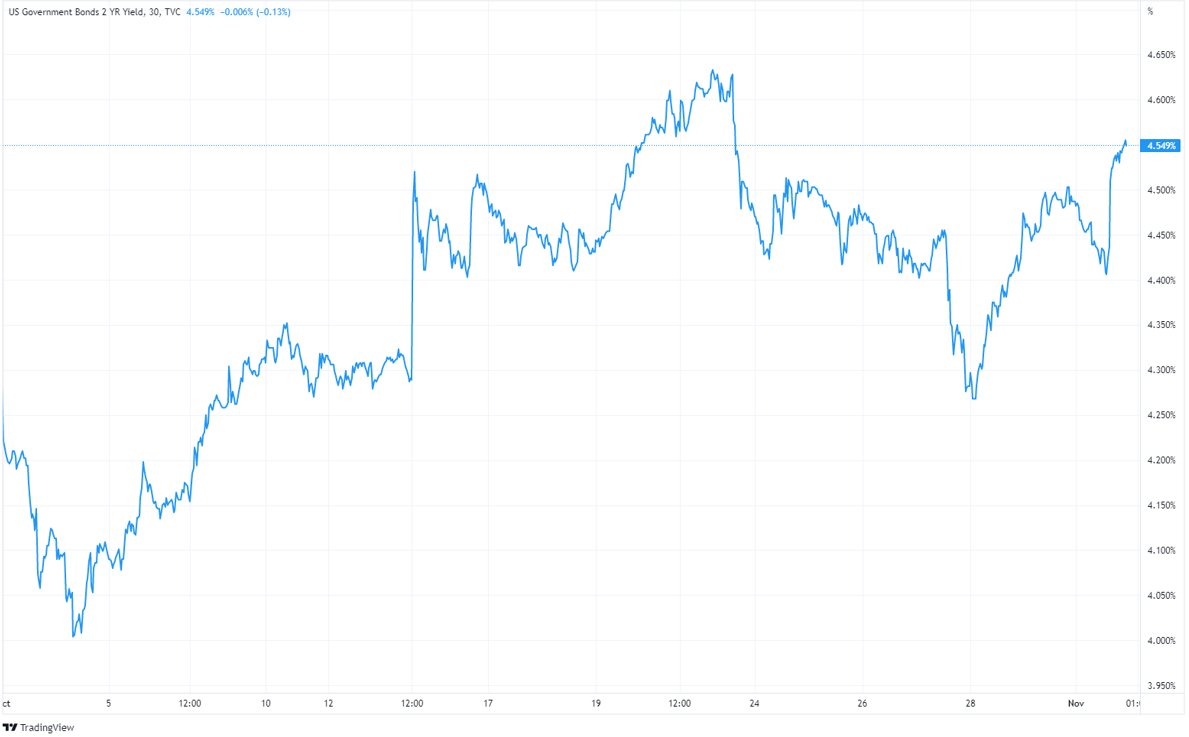

While the front end of the curve continued its push higher

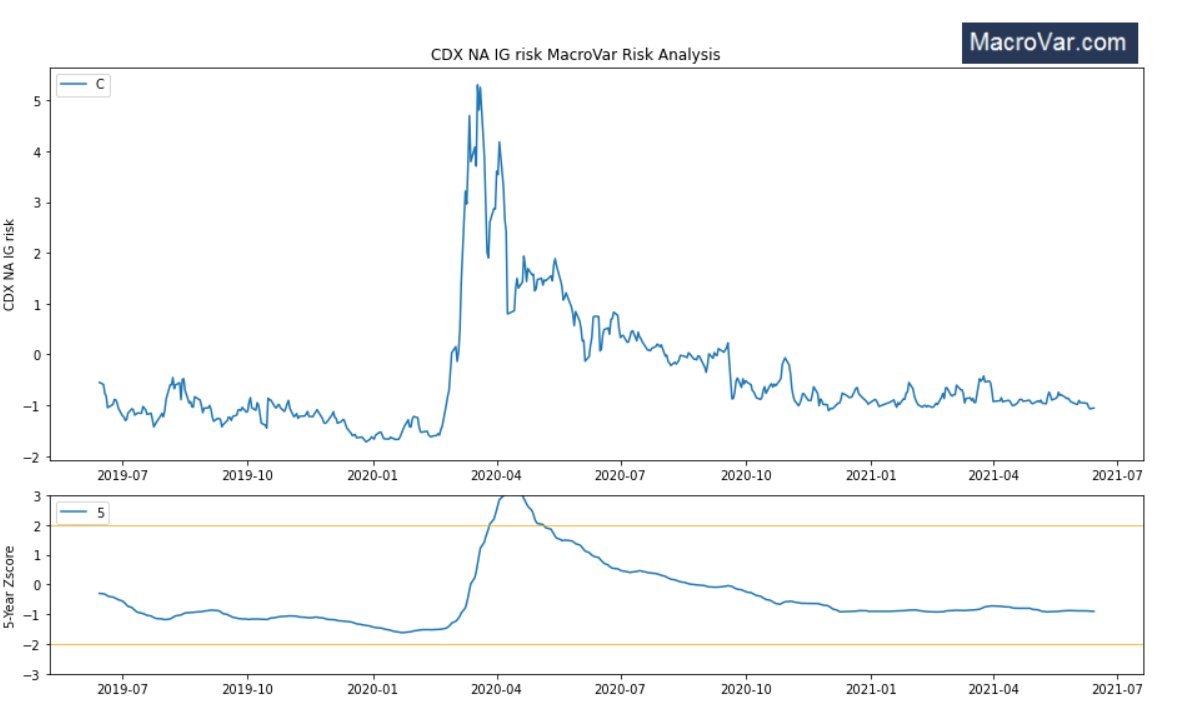

Despite rates moving higher, we have still not seen significant stress as a result of default risk with CDX still trading very low.

As the front-end rates move higher, the $ continues to be a wrecking ball against both the Yen and the Yuan, forcing the BoJ to (fruitlessly) intervene.

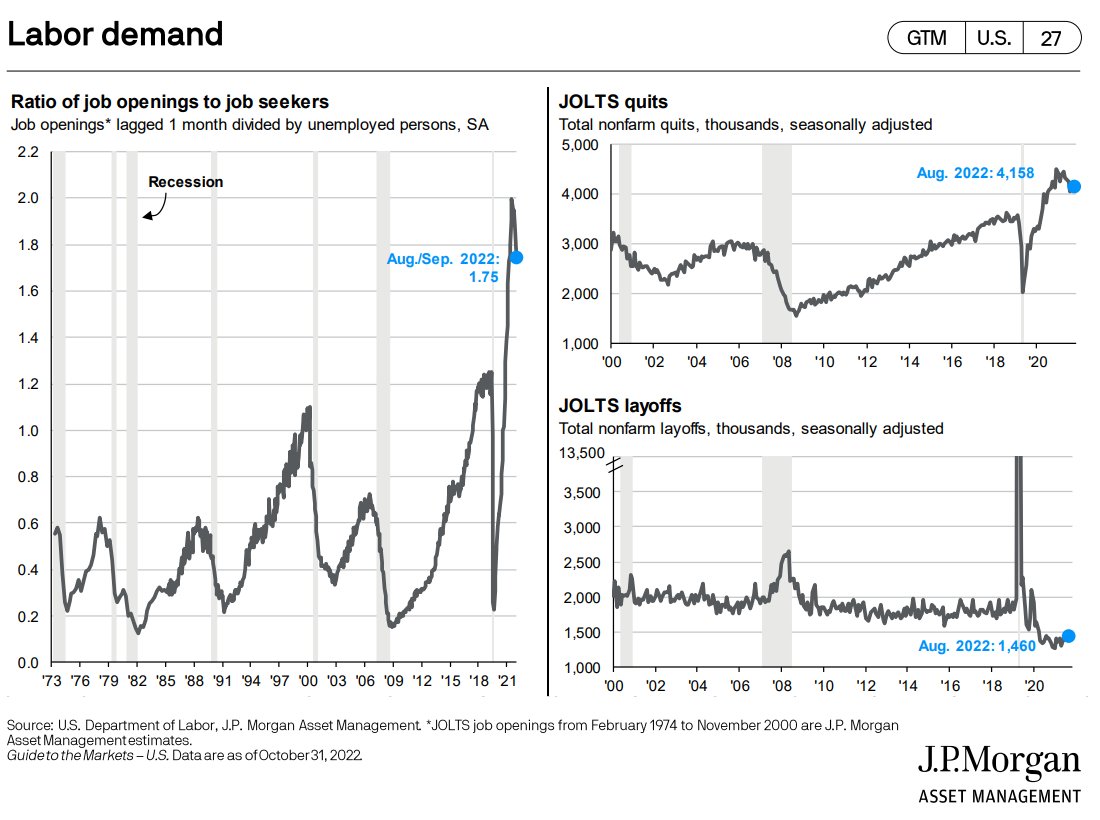

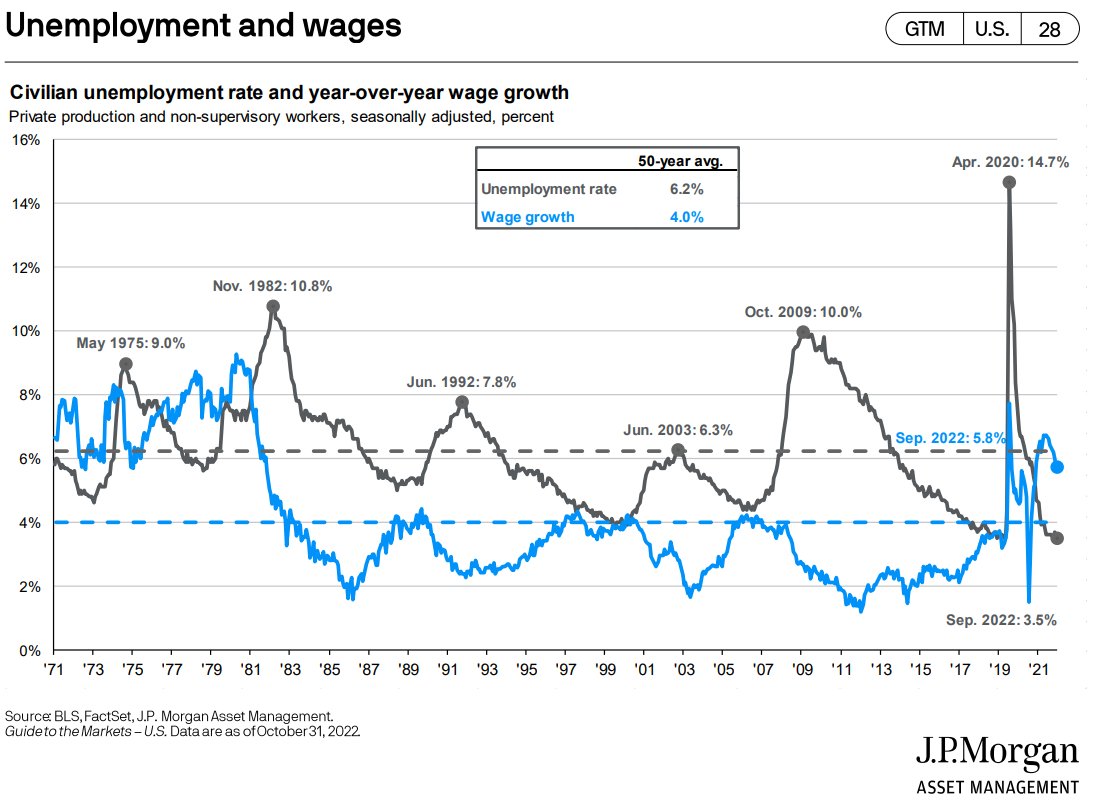

We have begun to see some moderation in both labor demand and wage growth. Both still remain quite elevated.

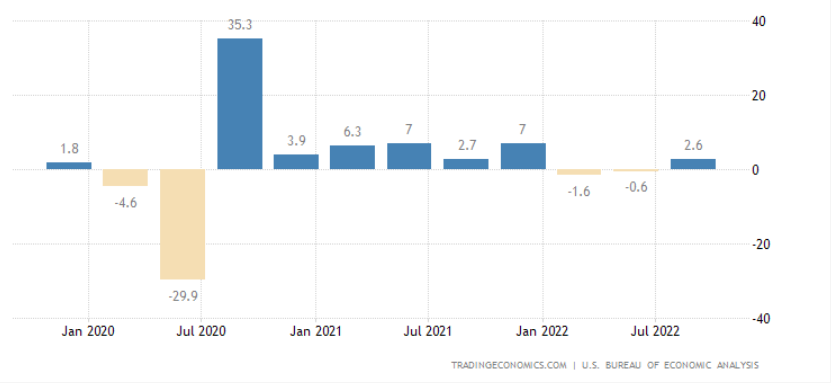

Meanwhile, US GDP returned positive at +2.6%, quelling the recession hysteria we have listened to all year

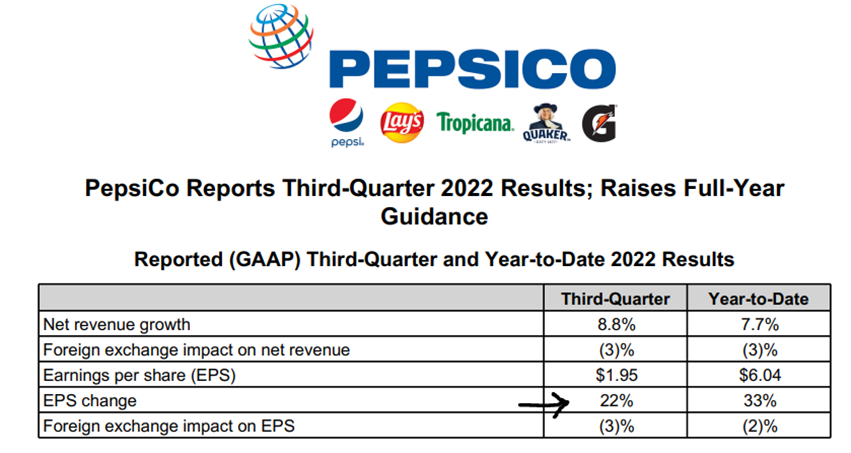

The strength of consumer staple earnings provided us with another data point that the US consumer has remained resilient, despite inflationary pressures.

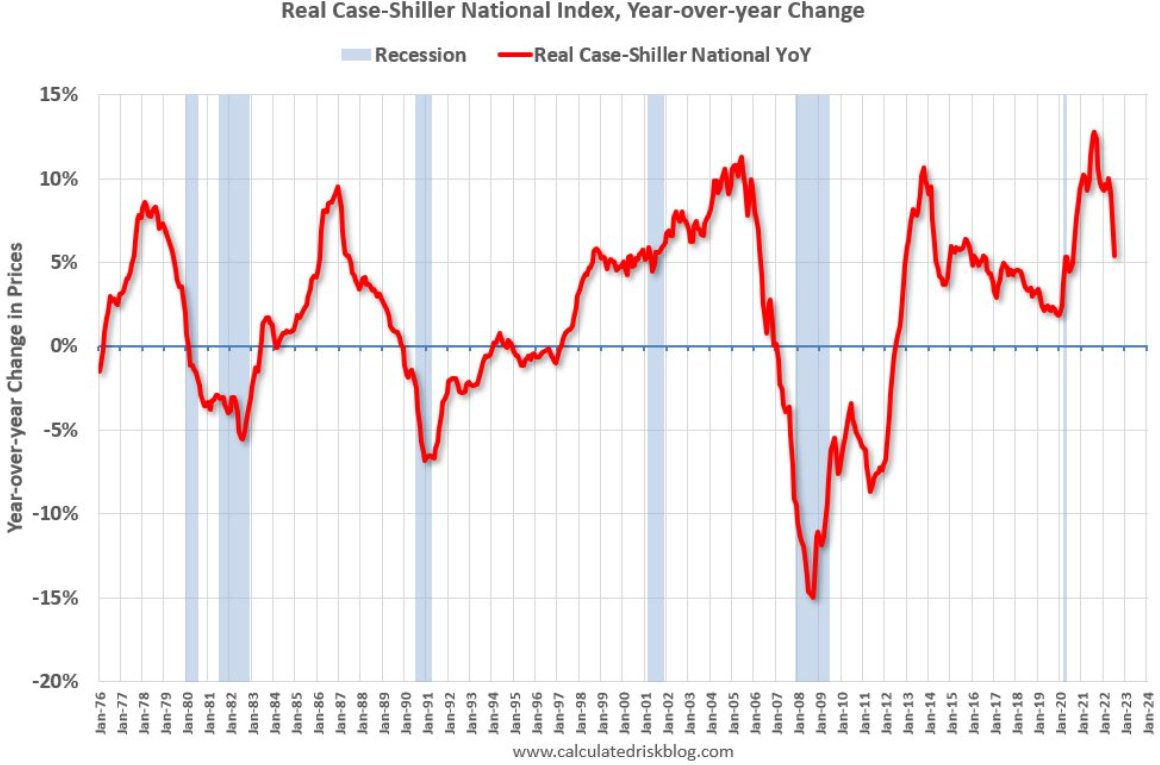

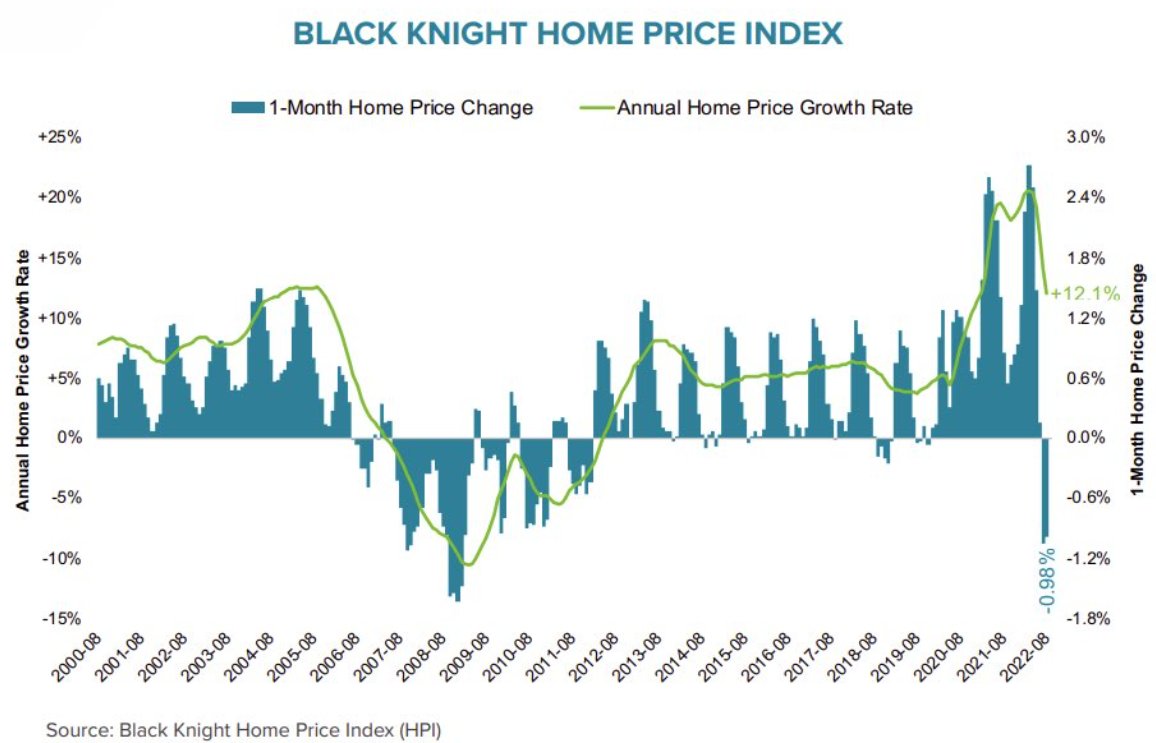

While consumers remain strong, we have seen rapid policy transmission across the housing complex.

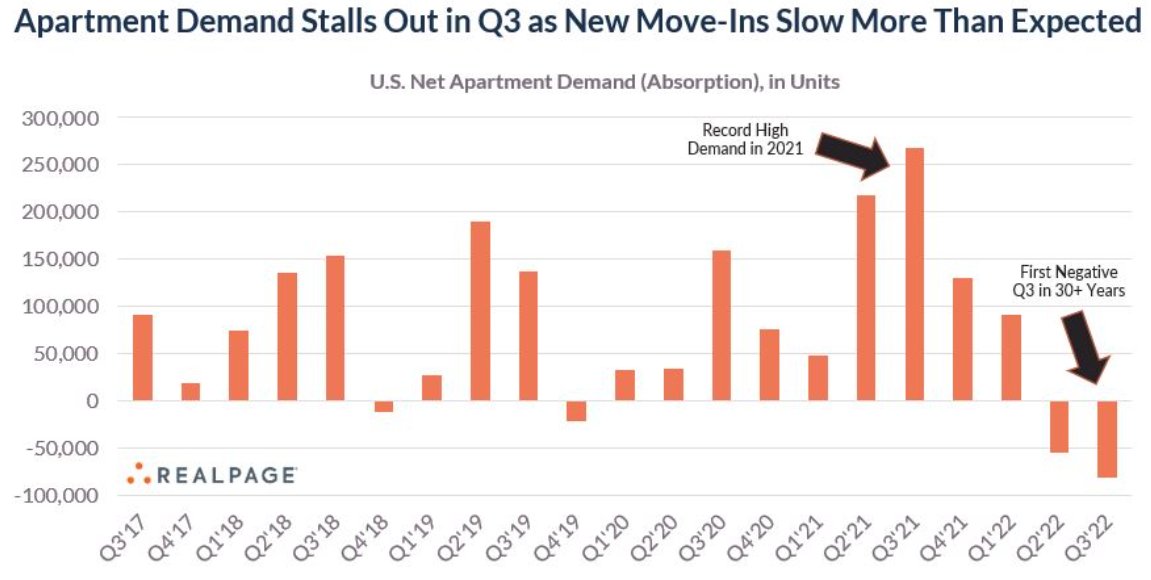

And we are beginning to see apartment demand fall in response to slowing household formation. Caveat: Seasonality plays a strong role in these numbers so don't read too much into it.

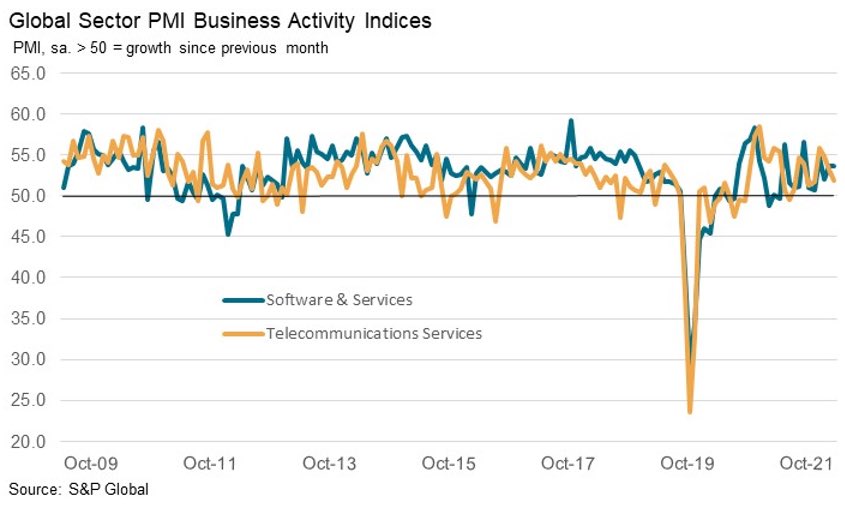

Slowing demand has begun to have a strong impact on global PMIs

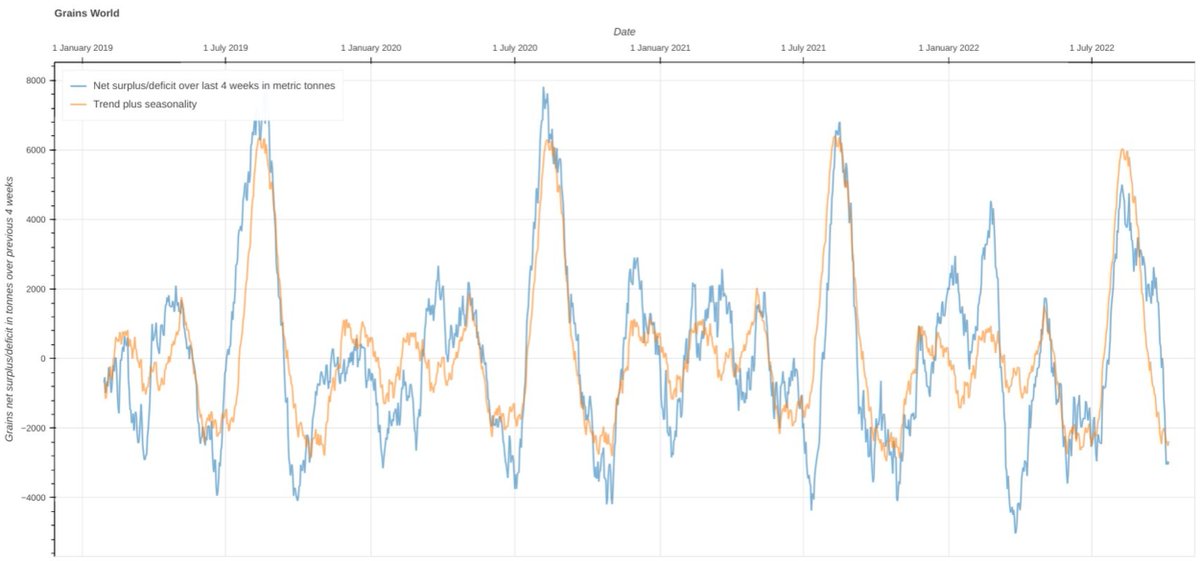

While we are seeing demand-side destruction, commodities remain a wild card for those in the "inflation has peaked" camp. Due to a host of policy mistakes and the Ukr/Rus war, we now find ourselves in a potential worst-case scenario for both oil and grains. H/t @BenniKim

Commodities were starting to drag on CPI and we now run the risk of them being a significant factor once again. As we have already established - we are not in a recession yet. Thus, the demand destruction argument for grains and energy will weaken - sending prices higher.

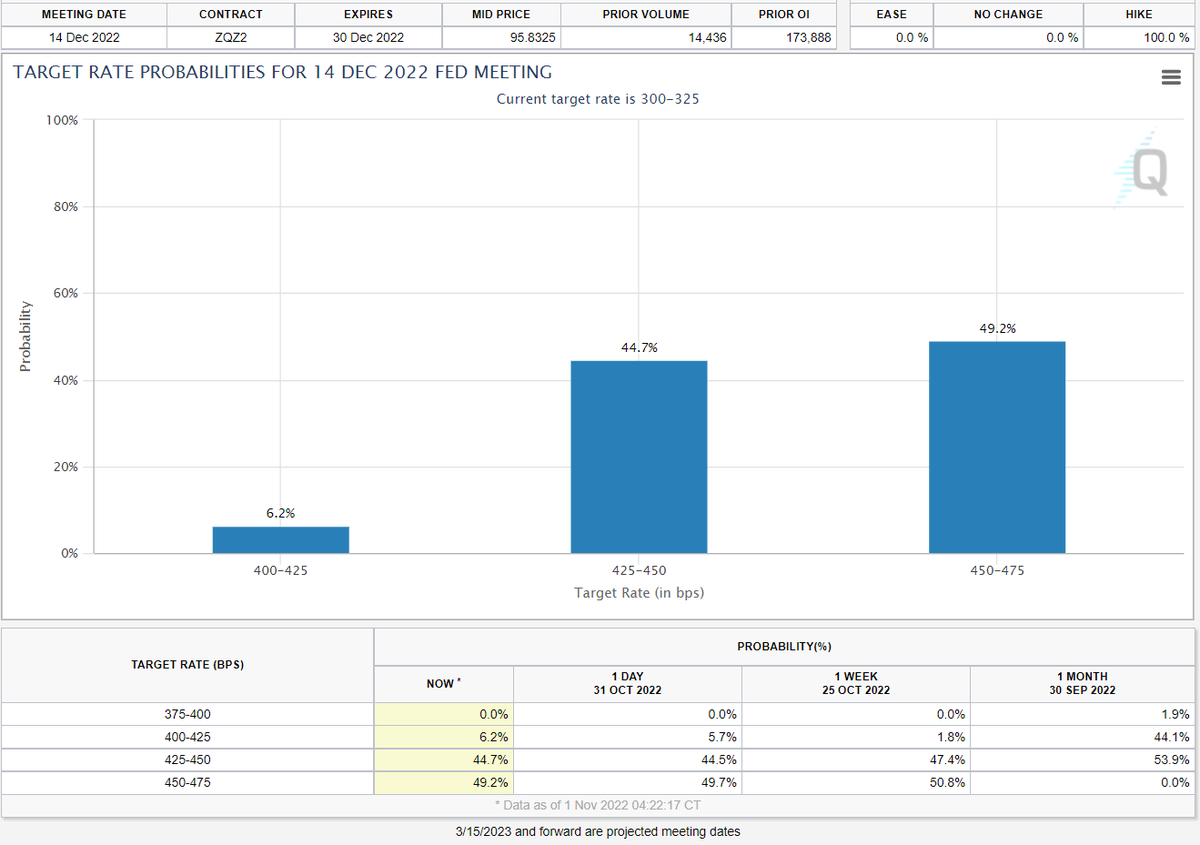

Investors are now wholly focused on what the Fed indicates for December. In our estimation, the most likely outcome is that they open the door to a *discussion* of 50bps. The market currently assigns a ~50% chance that they raise 50bps

In summary:

CBs are playing whack-a-mole with a big hammer while politicians continue to shove moles through the holes via poor policy. Meanwhile, the equity market is living on a hope and prayer that the Fed will ease rates and the party can go on.

CBs are playing whack-a-mole with a big hammer while politicians continue to shove moles through the holes via poor policy. Meanwhile, the equity market is living on a hope and prayer that the Fed will ease rates and the party can go on.

The reality is that the world is having to pay for years of excesses and that process is going to take time to play out with some highs and many lows along the way. Heavy cash and low cockiness as we move forward.

Loading suggestions...