(1/20)

About:

Incorporated in Jan 2001, AWHCL is one of the leading players in the field of Municipal Solid Waste (MSW) management

services in India. It is a part of Antony Group having diversified business interests mainly in automotive body building and

ancillary industries.

About:

Incorporated in Jan 2001, AWHCL is one of the leading players in the field of Municipal Solid Waste (MSW) management

services in India. It is a part of Antony Group having diversified business interests mainly in automotive body building and

ancillary industries.

(2/20)

India’s waste management industry:

The size of the global waste management industry is ₹23Lakh Cr whereas the size of India’s waste management industry is mere ₹5,000 cr

India also practices higher open dumping (77%) than the global average (52%)

India’s waste management industry:

The size of the global waste management industry is ₹23Lakh Cr whereas the size of India’s waste management industry is mere ₹5,000 cr

India also practices higher open dumping (77%) than the global average (52%)

(3/20)

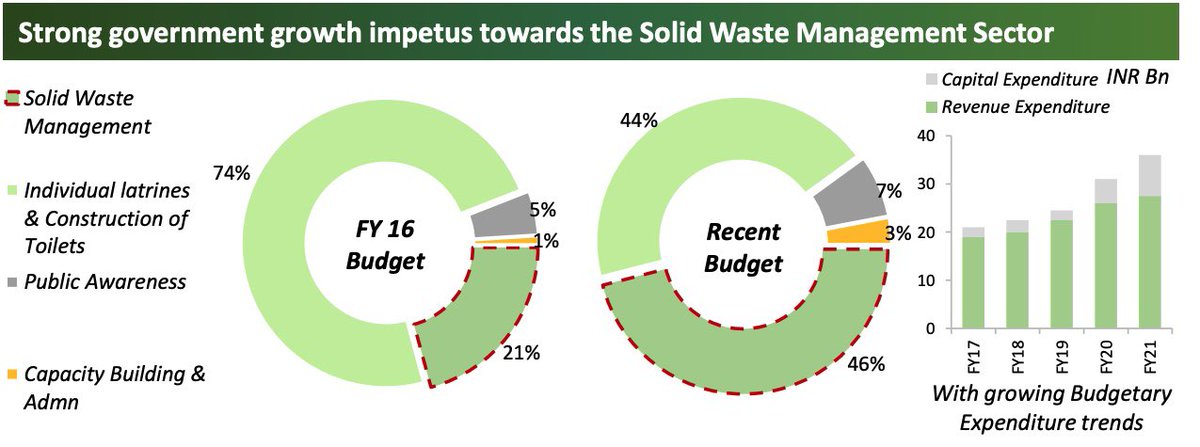

GOIs push towards Solid waste Management:

If you look at the chart below, you will understand how the govt has gradually shifted the resources from creating new Toilets in FY16 to utilising the same for solid waste management. This bodes well for a company like AWHCL

GOIs push towards Solid waste Management:

If you look at the chart below, you will understand how the govt has gradually shifted the resources from creating new Toilets in FY16 to utilising the same for solid waste management. This bodes well for a company like AWHCL

(4/20)

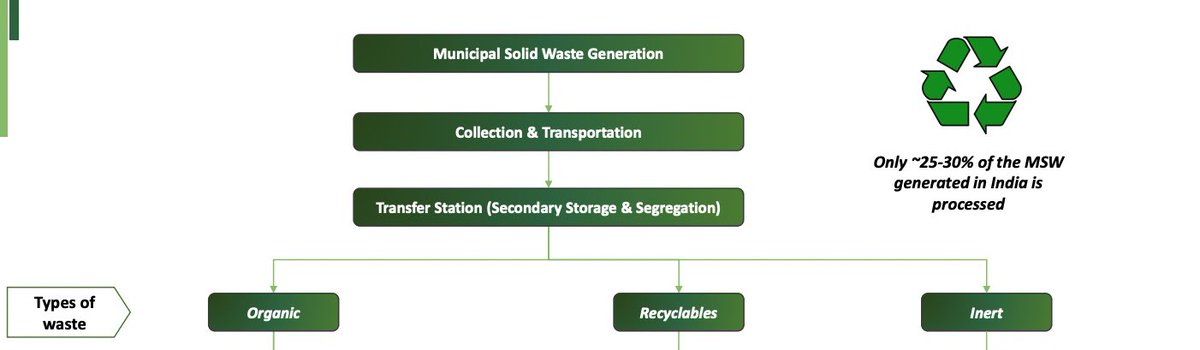

Processing Technologies used by AWHCL:

The company deals in Organic, Recyclables and Inert waste. Here’s how they process it:

• Composting

• Bio-Methanation

• Incineration

• Reuse/Recycling

• Landfilling ➡️ Bio-mining

Processing Technologies used by AWHCL:

The company deals in Organic, Recyclables and Inert waste. Here’s how they process it:

• Composting

• Bio-Methanation

• Incineration

• Reuse/Recycling

• Landfilling ➡️ Bio-mining

(5/20)

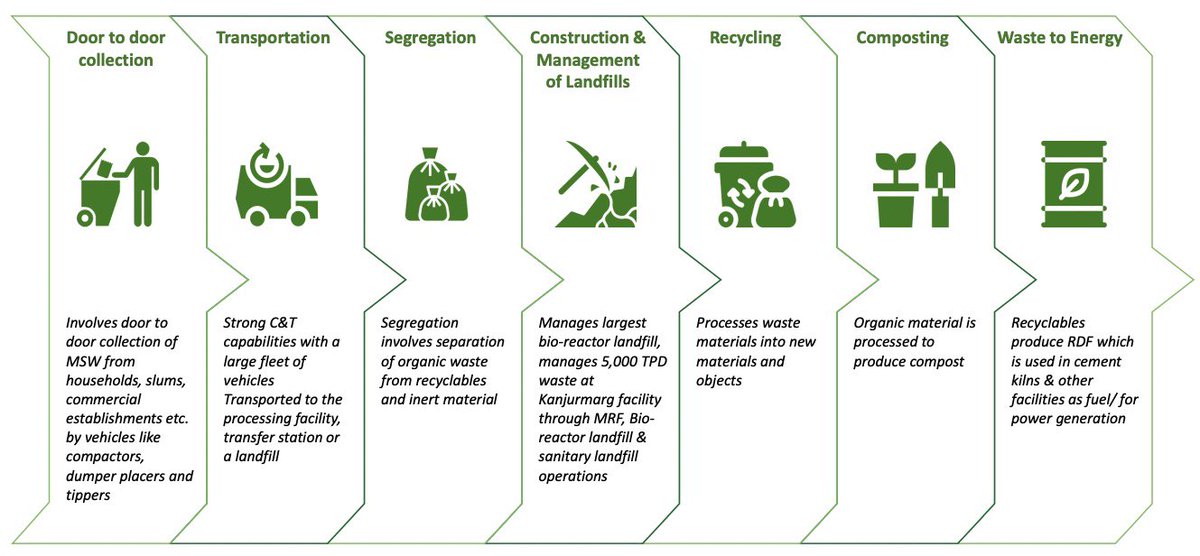

It’s Process:

It’s Process:

(6/20)

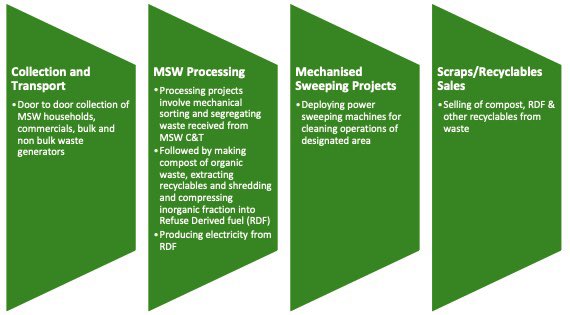

Revenue classification:

• MSW C&T: 62% of total revenue

Door to door collection through primary collection vehicles

• MSW Processing: 23%

Involves sorting & segregating waste received from MSW C&T, followed by composting, recycling, shredding & compressing into RDF

Revenue classification:

• MSW C&T: 62% of total revenue

Door to door collection through primary collection vehicles

• MSW Processing: 23%

Involves sorting & segregating waste received from MSW C&T, followed by composting, recycling, shredding & compressing into RDF

(7/20)

• Contract & Others: 15%

Integrated mechanical and manual

sweeping of streets, sale of goods,

Revenue from sale of scrap.

• Contract & Others: 15%

Integrated mechanical and manual

sweeping of streets, sale of goods,

Revenue from sale of scrap.

(8/20)

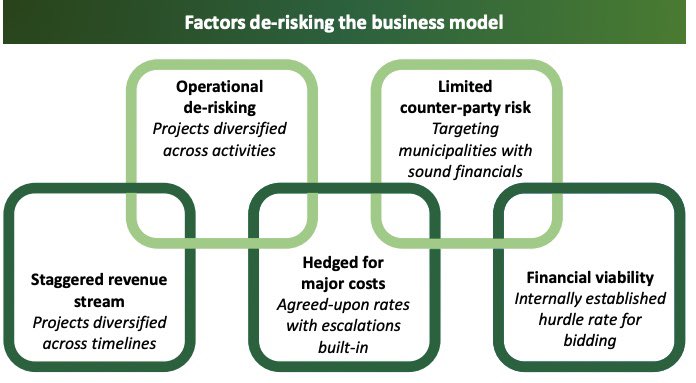

AWHCL has 23 ongoing projects, comprising 14 C&T projects, 3 MSW processing projects and 6 mechanized sweeping projects.

By diversifying the ongoing project portfolio across multiple municipalities with favorable dynamics, the company has limited the counterparty risk.

AWHCL has 23 ongoing projects, comprising 14 C&T projects, 3 MSW processing projects and 6 mechanized sweeping projects.

By diversifying the ongoing project portfolio across multiple municipalities with favorable dynamics, the company has limited the counterparty risk.

(9/20)

Vehicle and Equipment Pool:

AWHCL had a total of 1,754 collection trucks across the country out of which 1,619 are fitted with GPS trackers. These are procured from leading international

suppliers including the likes of Compost Systems GMBH.

Vehicle and Equipment Pool:

AWHCL had a total of 1,754 collection trucks across the country out of which 1,619 are fitted with GPS trackers. These are procured from leading international

suppliers including the likes of Compost Systems GMBH.

(10/20)

Areas of growth:

• Biomenthanation

Generates methane rich bio-gas,

fuel and sludge for making compost

• Refuse Derived Fuel:

Used as a substitute for coal in energy

• Bio-Mining:

World’s largest Biomining project was started in 2018 at Mulund dumping ground

Areas of growth:

• Biomenthanation

Generates methane rich bio-gas,

fuel and sludge for making compost

• Refuse Derived Fuel:

Used as a substitute for coal in energy

• Bio-Mining:

World’s largest Biomining project was started in 2018 at Mulund dumping ground

(11/20)

Strengths:

• Experienced Management:

AWHCL is promoted by Mr.Jose Jacob, Mr. Shiju Jacob, and Mr.Shiju Antony. They have vast experience in waste management industry with an established track record for undertaking waste management services for more than 2 decades.

Strengths:

• Experienced Management:

AWHCL is promoted by Mr.Jose Jacob, Mr. Shiju Jacob, and Mr.Shiju Antony. They have vast experience in waste management industry with an established track record for undertaking waste management services for more than 2 decades.

(12/20)

• Revenue visibility:

AWHCL through its subsidiaries has entered into multi-year concession agreement with various Municipal bodies across India.

C&T projects are generally awarded for a period of 7-10 years, while waste processing contracts for over 20 years.

• Revenue visibility:

AWHCL through its subsidiaries has entered into multi-year concession agreement with various Municipal bodies across India.

C&T projects are generally awarded for a period of 7-10 years, while waste processing contracts for over 20 years.

(13/20)

• Healthy operating margins:

Antony Waste group is earning healthy operational margins in in C&T and mechanical sweeping segment. It also earns high operational margins in case of waste processing, segregation and bio-reactor landfilling activities.

• Healthy operating margins:

Antony Waste group is earning healthy operational margins in in C&T and mechanical sweeping segment. It also earns high operational margins in case of waste processing, segregation and bio-reactor landfilling activities.

(14/20)

Weaknesses:

• Small scale of operations:

Out of total 205 municipal Corporations (Excluding Municipalities & ULBs) in India, currently the group is catering to largely 15 Municipal Corporations. Hence, the small scale of operation restricts it’s financial flexibility.

Weaknesses:

• Small scale of operations:

Out of total 205 municipal Corporations (Excluding Municipalities & ULBs) in India, currently the group is catering to largely 15 Municipal Corporations. Hence, the small scale of operation restricts it’s financial flexibility.

(15/20)

• Delayed Payments:

The Debtors days of the company is ~72 days. And it’s Trade receivables amounts to ₹128cr as on March 31, 2022.

There are long pending dues whose contracts have already been concluded 5-6 years back

~85% of total projects make timely payments.

• Delayed Payments:

The Debtors days of the company is ~72 days. And it’s Trade receivables amounts to ₹128cr as on March 31, 2022.

There are long pending dues whose contracts have already been concluded 5-6 years back

~85% of total projects make timely payments.

(16/20)

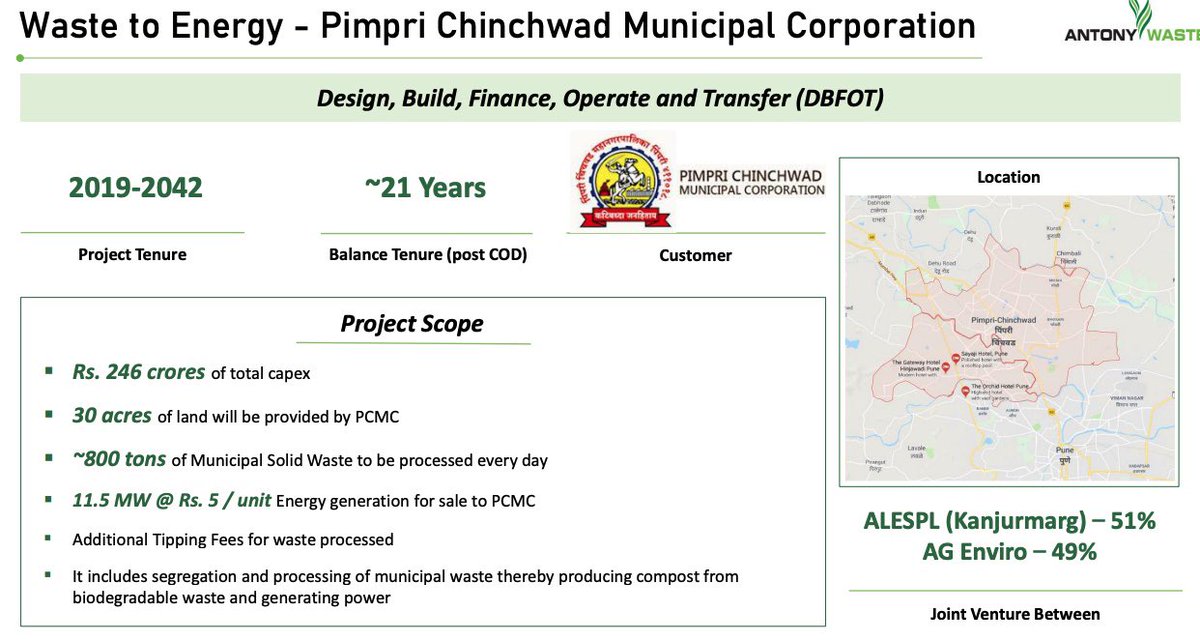

• Waste to Energy Plant setup:

• Plant is scheduled to be commissioned by the end of FY23.

• Total Cost - ₹246cr

• Debt component - ₹172cr

• Project is a new venture with no prior experience, thus the company is exposed with project risk.

• Waste to Energy Plant setup:

• Plant is scheduled to be commissioned by the end of FY23.

• Total Cost - ₹246cr

• Debt component - ₹172cr

• Project is a new venture with no prior experience, thus the company is exposed with project risk.

(17/20)

• Susceptible to Policy change:

Any downward revision in the Tipping Fee or C&T fees will

impact the revenues of the company

Many Municipalities are highly dependent on state/central/budget allocation to fund various projects, hence delay in payment is an issue.

• Susceptible to Policy change:

Any downward revision in the Tipping Fee or C&T fees will

impact the revenues of the company

Many Municipalities are highly dependent on state/central/budget allocation to fund various projects, hence delay in payment is an issue.

(18/20)

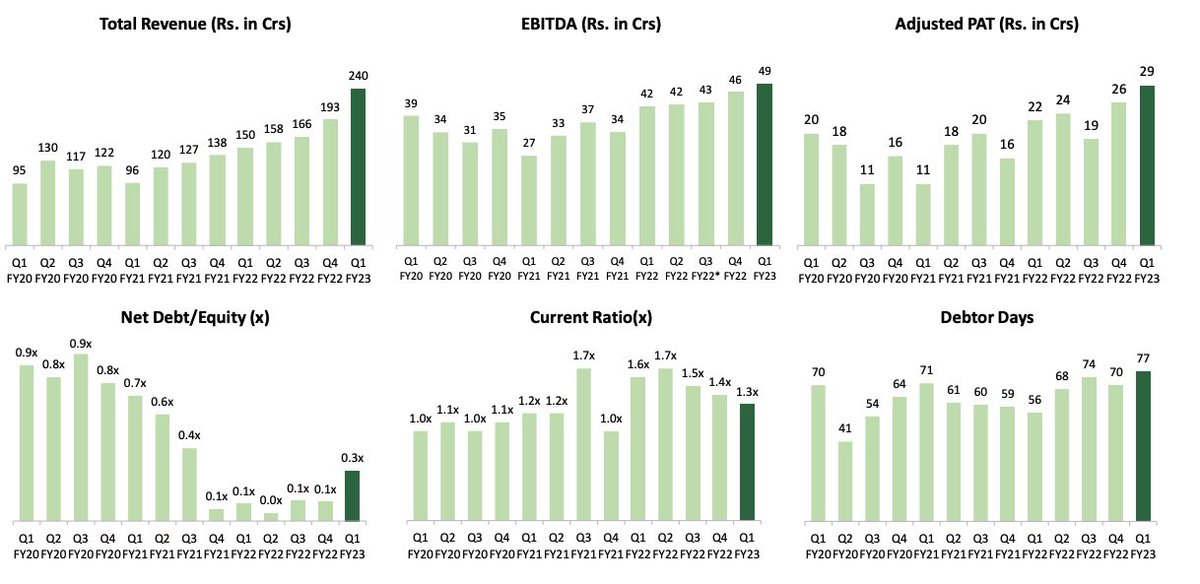

Financials:

• Revenue and Margin looks solid

• Debtor days is showing stability, although it should ideally be in a downward trend

• D/E went up owing to the new WTE plant in Pune.

Financials:

• Revenue and Margin looks solid

• Debtor days is showing stability, although it should ideally be in a downward trend

• D/E went up owing to the new WTE plant in Pune.

(19/20)

Shareholding Pattern:

• Promoters : 46.23%

• FIIs: 13.16%

• DIIs : 6.48%

• Public: 34.13%

Shareholding Pattern:

• Promoters : 46.23%

• FIIs: 13.16%

• DIIs : 6.48%

• Public: 34.13%

(20/20)

Though the nos of AWHCL looks good, but it’s very nature of dealing with municipal corporation which are infamous for their payment delays creates a doubt in investors mind and hence we see this company trading at a fairly cheaper valuation.

@caniravkaria @kuttrapali26

Though the nos of AWHCL looks good, but it’s very nature of dealing with municipal corporation which are infamous for their payment delays creates a doubt in investors mind and hence we see this company trading at a fairly cheaper valuation.

@caniravkaria @kuttrapali26

Loading suggestions...