(1/16)

About:

Incorporated in 1984, SBCL is promoted by Mr S S Sandhu and Mr N S Ghumman.

The company manufactures thermostatic bimetal/trimetal strips, components, shunt resistors and clad metals.

Its units are in Chambaghat, Himachal Pradesh.

About:

Incorporated in 1984, SBCL is promoted by Mr S S Sandhu and Mr N S Ghumman.

The company manufactures thermostatic bimetal/trimetal strips, components, shunt resistors and clad metals.

Its units are in Chambaghat, Himachal Pradesh.

(2/16)

Product Portfolio:

• Thermostatic Bimetal Parts/Strips

• Thermostatic Bimetal Coils & Spring

• SMDs / Shunt Resistors

• Snap Action Disc

• Continuous Electron Beam Welded Strip

• Battery Management Shunts

Product Portfolio:

• Thermostatic Bimetal Parts/Strips

• Thermostatic Bimetal Coils & Spring

• SMDs / Shunt Resistors

• Snap Action Disc

• Continuous Electron Beam Welded Strip

• Battery Management Shunts

(3/16)

Industry Overview:

SHIVALIK caters to a broad spectrum of applications which include Switchgears, Energy Meters, Industrial, Electrical

applications, Automotive & Electronic Devices.

Their growth is directly connected with the Electrical, Electronics &

Automotive Ind.

Industry Overview:

SHIVALIK caters to a broad spectrum of applications which include Switchgears, Energy Meters, Industrial, Electrical

applications, Automotive & Electronic Devices.

Their growth is directly connected with the Electrical, Electronics &

Automotive Ind.

(4/16)

Electrical Industry:

Domestic electrical equipment market is expected to grow at an annual rate of 12 per cent to reach

USD 72 billion by 2025

Automotive Industries:

The global electric vehicle market size is projected to grow at a CAGR of 26.8% till 2030

Electrical Industry:

Domestic electrical equipment market is expected to grow at an annual rate of 12 per cent to reach

USD 72 billion by 2025

Automotive Industries:

The global electric vehicle market size is projected to grow at a CAGR of 26.8% till 2030

(5/16)

The Company is a single vendor to many prestigious OEMs since 1986 . It’s products are exported to about 40 industrialized countries around the world.

It offers precision manufactured components specific to the

application requirements of its customers.

The Company is a single vendor to many prestigious OEMs since 1986 . It’s products are exported to about 40 industrialized countries around the world.

It offers precision manufactured components specific to the

application requirements of its customers.

(6/16)

Opportunities:

1) Introduction of new ELECTRIC vehicle models in the Global market.

2) Affordable housing projects of the government and government stress on infrastructure building will stimulate further

demand for switchgear

Opportunities:

1) Introduction of new ELECTRIC vehicle models in the Global market.

2) Affordable housing projects of the government and government stress on infrastructure building will stimulate further

demand for switchgear

(7/16)

3) Continuing Government’s plan to convert traditional meters into smart meters and replace them with retrofitting programmes.

4) Continuing Favourable Government Schemes and Programmes

6) Mandatory requirements for battery management systems even in ICE Vehicles.

3) Continuing Government’s plan to convert traditional meters into smart meters and replace them with retrofitting programmes.

4) Continuing Favourable Government Schemes and Programmes

6) Mandatory requirements for battery management systems even in ICE Vehicles.

(8/16)

Threats

• Supply disruptions of nickel & copper due to Geo-political effects of the UKRAINE conflict

• General inflation: Sharp increase in prices could lead to lower purchasing power which could impact on demand in due course

• Continued Supply chain Disruptions

Threats

• Supply disruptions of nickel & copper due to Geo-political effects of the UKRAINE conflict

• General inflation: Sharp increase in prices could lead to lower purchasing power which could impact on demand in due course

• Continued Supply chain Disruptions

(9/16)

Strengths:

Strong market position in the niche linear bimetals segment:

Being one of the few manufacturers of bimetal parts & shunt resistors in India, SBCL faces limited competition.

It growth is linked with the very strong Auto, electrical & electronics industry

Strengths:

Strong market position in the niche linear bimetals segment:

Being one of the few manufacturers of bimetal parts & shunt resistors in India, SBCL faces limited competition.

It growth is linked with the very strong Auto, electrical & electronics industry

(10/16)

Strong track record of key management:

Presence of over three decades in the niche and highly specialised bimetal industry, has enabled the promoters to ensure sustained revenue growth, despite industry downturns.

Strong track record of key management:

Presence of over three decades in the niche and highly specialised bimetal industry, has enabled the promoters to ensure sustained revenue growth, despite industry downturns.

(11/16)

Weakness:

Working capital-intensive operations: Inventory stood at 260 days as on March 31, 2022, and is expected to remain along similar lines going forward.

Raw materials inventory of around 120 days is maintained as procurement is imported

Weakness:

Working capital-intensive operations: Inventory stood at 260 days as on March 31, 2022, and is expected to remain along similar lines going forward.

Raw materials inventory of around 120 days is maintained as procurement is imported

(12/16)

Key Ratios:

• Market Cap: ₹2,715 cr

• Stock P/E: 46.9

• RoCE: 35.1%

• RoE: 31.9%

• PEG: 1.09

• 3 years Sales CAGR: 18.8%

• Int Coverage: 21.2

• Debt: ₹57.9cr

• D/E: 0.31

• NPM last year: 16%

• OPM last quarter: 25%

• FY22 EPS: 9.02 vs 4.19 YoY

Key Ratios:

• Market Cap: ₹2,715 cr

• Stock P/E: 46.9

• RoCE: 35.1%

• RoE: 31.9%

• PEG: 1.09

• 3 years Sales CAGR: 18.8%

• Int Coverage: 21.2

• Debt: ₹57.9cr

• D/E: 0.31

• NPM last year: 16%

• OPM last quarter: 25%

• FY22 EPS: 9.02 vs 4.19 YoY

(13/16)

Shareholding Pattern:

• Promoters : 60.61%

• FIIs : 0.06%

• DII : 0.17%

• Public : 39.17%

Shareholding Pattern:

• Promoters : 60.61%

• FIIs : 0.06%

• DII : 0.17%

• Public : 39.17%

(14/16)

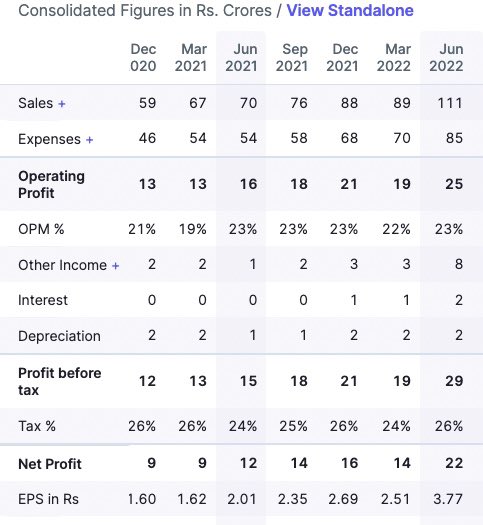

Latest Numbers:

• Healthy increase in revenue and Stable OPM

• Incrwase of EPS from 2.01 to 3.77 YoY

• Last year dividend payout was 7%

Latest Numbers:

• Healthy increase in revenue and Stable OPM

• Incrwase of EPS from 2.01 to 3.77 YoY

• Last year dividend payout was 7%

(15/16)

Focus of the Management going forward:

• Innovation via development of new products

• Continuous Engineering for Cost Optimization

• Automation and digitalization

• Enhancing Global Presence

• Control on Operating expenditure

• Competency enhancement

Focus of the Management going forward:

• Innovation via development of new products

• Continuous Engineering for Cost Optimization

• Automation and digitalization

• Enhancing Global Presence

• Control on Operating expenditure

• Competency enhancement

(16/16)

If you like our content kindly, Like and Hit Retweet for better reach!

@caniravkaria @kuttrapali26 @chartmojo

If you like our content kindly, Like and Hit Retweet for better reach!

@caniravkaria @kuttrapali26 @chartmojo

Loading suggestions...