“ROIC is one way to measure whether a company’s earnings are sufficient relative to the capital it has invested.”

Key takeaways from ROIC and Intangible Assets by M. Mauboussin (@mjmauboussin)and D. Callahan

Key takeaways from ROIC and Intangible Assets by M. Mauboussin (@mjmauboussin)and D. Callahan

Accounting doesn’t treat tangible and intangible investments the same. Tangible investments are recorded on the balance sheet and are depreciated over their useful lives. Intangible investments on the other hand are expensed on the income statements.

In order for us to put companies on the same footing, we need to treat tangible and intangible investments the same . This thus requires us to capitalize intangible investments.

This involves us dissecting SG&A into maintenance SG&A and investment SG&A. We take the investment SG&A and capitalize it.

This reclassification results in NOPAT and Invested Capital both increasing, thus thus affects and changes ROIC.

This reclassification results in NOPAT and Invested Capital both increasing, thus thus affects and changes ROIC.

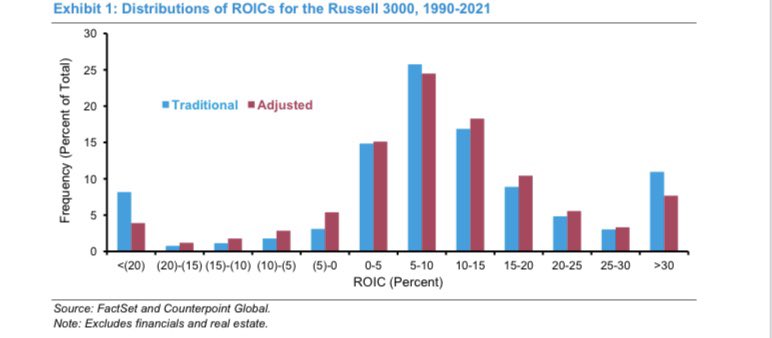

Extremely high and low ROIC regress to the mean.

It is noticeable that after adjustments, the bins with the lowest ROIC( far left) and highest ROIC(far right) will have fewer companies in them.

It is noticeable that after adjustments, the bins with the lowest ROIC( far left) and highest ROIC(far right) will have fewer companies in them.

This reclassification however doesn’t affect Free Cash Flow, it only provides a more accurate view of profits and investments

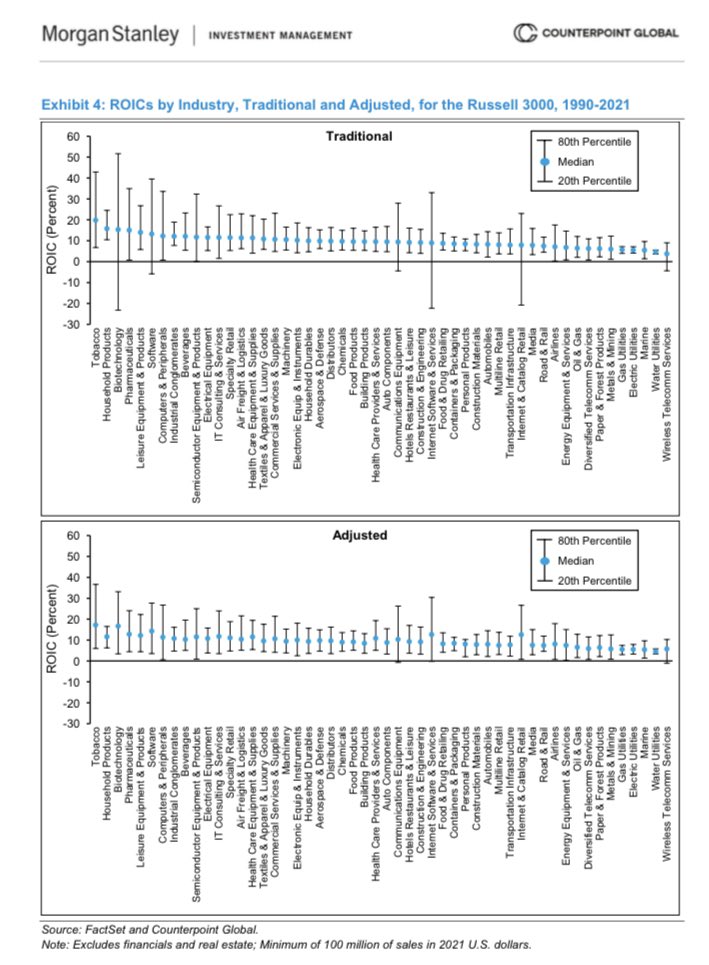

Adjusting for intangible investments has greater effect in certain industries, typically in those that rely heavily on intangible investments ( eg. biotech, software).

The capitalizing of intangibles in such companies results in an increase in ROIC.

The capitalizing of intangibles in such companies results in an increase in ROIC.

How we adjust for Intangible Investment

We need to acknowledge that part of SG&A is investments and the rest is for maintenance.

So we need to determine how much of SG&A is investments and the appropriate asset life.

This will allow us to place the intangible investments on

We need to acknowledge that part of SG&A is investments and the rest is for maintenance.

So we need to determine how much of SG&A is investments and the appropriate asset life.

This will allow us to place the intangible investments on

the balance sheet and capitalize them.

Prof. Peters and Taylor suggest that we treat all of R&D expense and 30% of non- R&D SG&A expense as intangible investments.

This approach has clear limitations as some R&D can actually be for maintaining current operations and

Prof. Peters and Taylor suggest that we treat all of R&D expense and 30% of non- R&D SG&A expense as intangible investments.

This approach has clear limitations as some R&D can actually be for maintaining current operations and

the portion of R&D expense and non-R&D SG&A expense that is an intangible investment varies with industries.

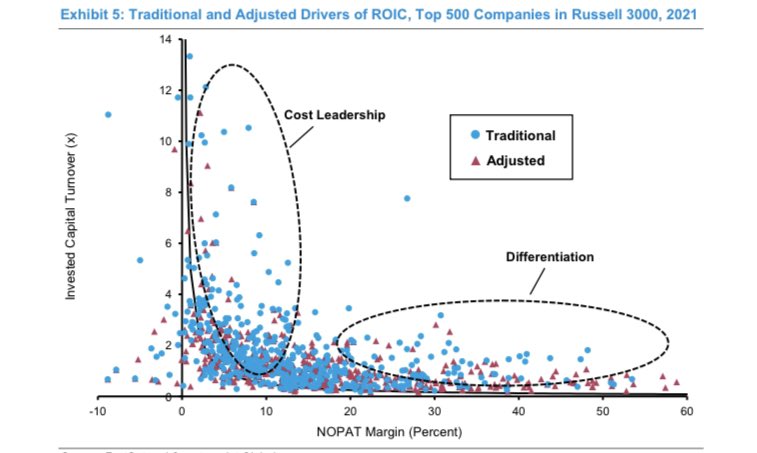

ROIC and Competitive Advantage

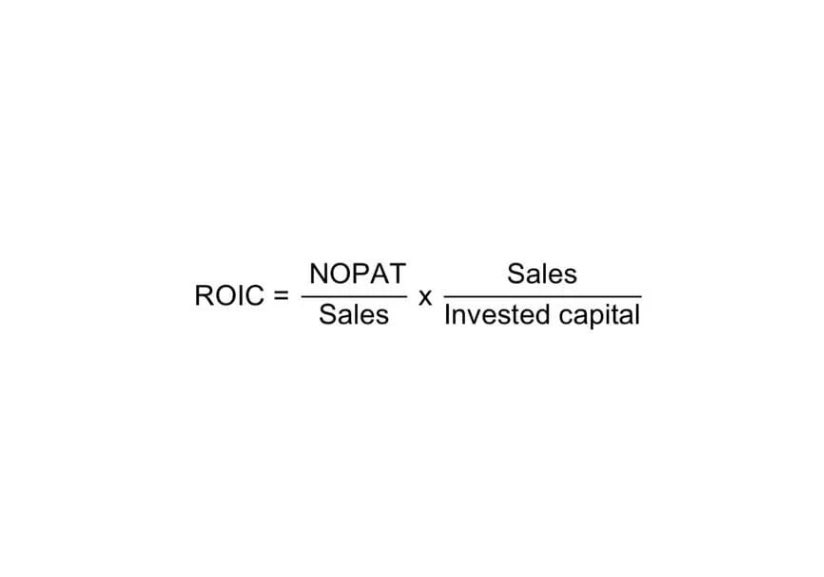

Breaking down ROIC can help us know the source of a company’s competitive advantage.

If a company achieves its high ROIC via a high NOPAT margin you should focus your analysis on differentiation.

If a company earns its high ROIC via a

Breaking down ROIC can help us know the source of a company’s competitive advantage.

If a company achieves its high ROIC via a high NOPAT margin you should focus your analysis on differentiation.

If a company earns its high ROIC via a

high invested capital turnover ratio, focus your analysis on cost leadership.

That’s all. Please like, follow and retweet .

Link: morganstanley.com

Link: morganstanley.com

Loading suggestions...