Piramal Pharma:-

The stock has been volatile ever since listing

The business has reported a slowdown!

A thread🧵on the business performance of Piramal Pharma and the future outlook

Lets go👇

(1/18)

The stock has been volatile ever since listing

The business has reported a slowdown!

A thread🧵on the business performance of Piramal Pharma and the future outlook

Lets go👇

(1/18)

What has happened?

Piramal Pharma listed at about 200.

Ever since the stock has lost nearly 25% value.

Lets find out why?

(2/18)

Piramal Pharma listed at about 200.

Ever since the stock has lost nearly 25% value.

Lets find out why?

(2/18)

Business:-

PPL has 3 verticles:-

🧪CDMO Business is a major chunk of the business.

🧪Complex hospital generics

🧪 Indian Consumer's healthcare

(3/18)

PPL has 3 verticles:-

🧪CDMO Business is a major chunk of the business.

🧪Complex hospital generics

🧪 Indian Consumer's healthcare

(3/18)

CDMO business remains strong:-

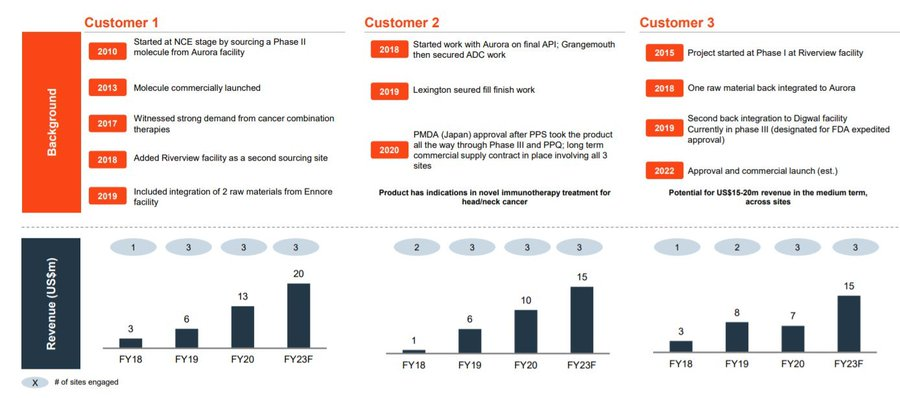

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

(4/18)

CDMO: 3x increase in phase III molecules from 10 in FY17 to 30 in FY21 & Significant growth in commercial products under patent from 11 in FY19 to 19 in FY21 with 500+ customers

The potential scale-up 💥👇

(4/18)

Expertise in niche, complex, and high margin areas like HPAPI, sterile injectables, hormones & peptide API

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example,even Syngene isn't till now, it is trying to enter manufacturing)

(5/18)

13th largest CDMO in the world & present across all phases of the drug lifecycle (for example,even Syngene isn't till now, it is trying to enter manufacturing)

(5/18)

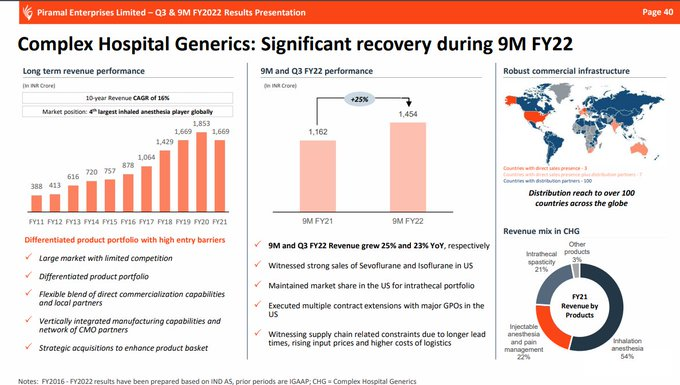

Complex hospital business continues to recover after a slump due to COVID-19

(6/18)

(6/18)

So How were the Q2FY23 results?

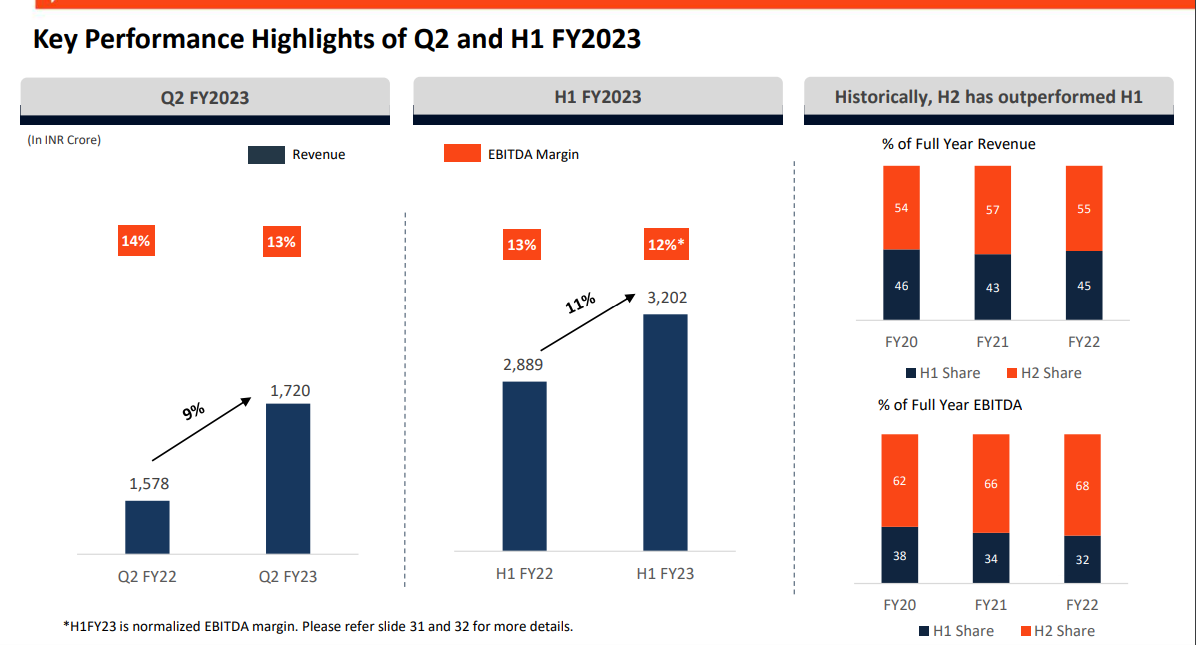

🧪Revenue grew by 13%

🧪Margins slowed down to 12%

🧪CDMO business reported a slowdown

🧪The company reported only 45% of the revenue of the full year

(7/18)

🧪Revenue grew by 13%

🧪Margins slowed down to 12%

🧪CDMO business reported a slowdown

🧪The company reported only 45% of the revenue of the full year

(7/18)

CDMO Business slowdown:-

🧪The CDMO business did report a slowdown to a growth of just 6%.

🧪This was led by a weakness in the API business.

(8/18)

🧪The CDMO business did report a slowdown to a growth of just 6%.

🧪This was led by a weakness in the API business.

(8/18)

🧪60% of CDMO business is API and 40% is formulation

🧪It has diversified mix of big pharma and

generics

🧪Peptide,high quality injectables continue to attract customers.

🧪Company is witnessing attrition and is taking measures to control it

(9/18)

🧪It has diversified mix of big pharma and

generics

🧪Peptide,high quality injectables continue to attract customers.

🧪Company is witnessing attrition and is taking measures to control it

(9/18)

🧪The company expects growth in API generic business as it continues to file DMFs with help of Hemmo Pharma. It also expects API services to grow well.

(10/18)

(10/18)

Strong guidance on the CDMO Business:-

Despite the weakness in the CDMO Business.

The company expects a recovery and has guided for

Doubling of the revenue in the next 5 years.

(11/18)

Despite the weakness in the CDMO Business.

The company expects a recovery and has guided for

Doubling of the revenue in the next 5 years.

(11/18)

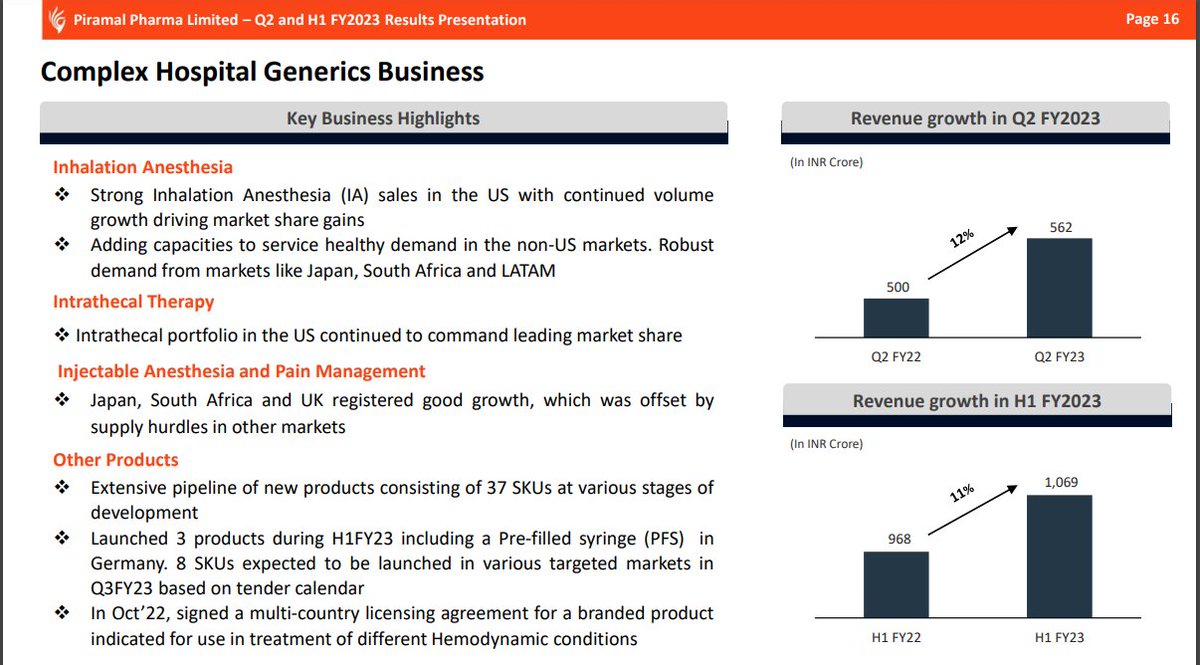

Complex Hospital Generics:-

🧪Strong sales with continued volume growth driving market share gains in Inhalation Anesthesia (IA) in the US market

🧪In Inhalation Anesthesia, the company

has less competition and expects high growth as it is gaining more supply chain.

(12/18)

🧪Strong sales with continued volume growth driving market share gains in Inhalation Anesthesia (IA) in the US market

🧪In Inhalation Anesthesia, the company

has less competition and expects high growth as it is gaining more supply chain.

(12/18)

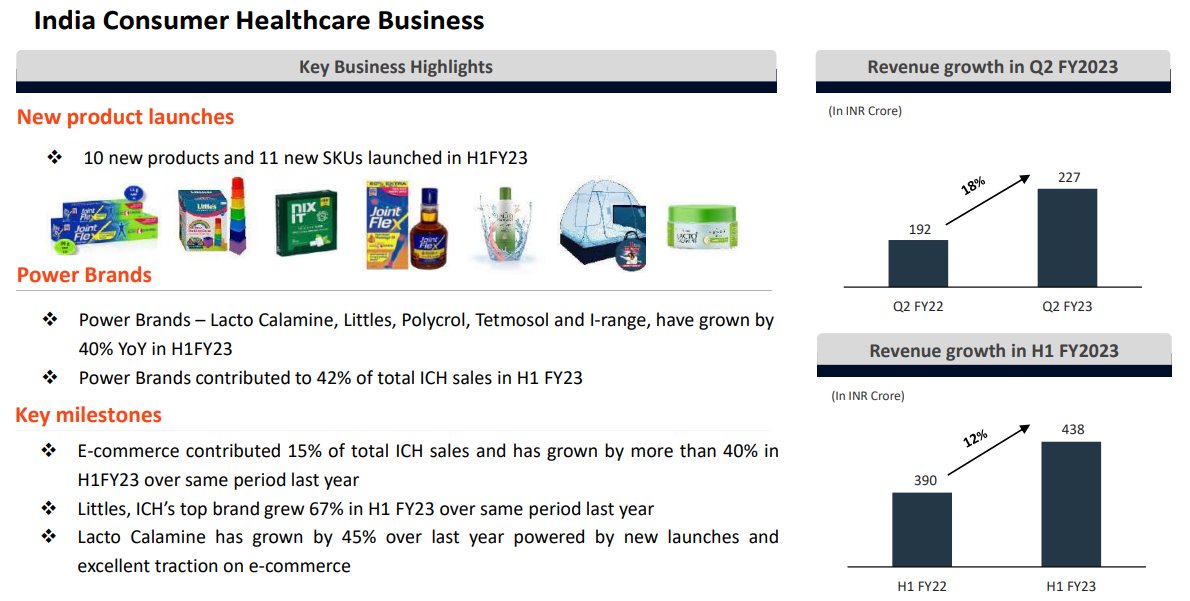

Indian Consumer Healthcare:-

🧪Power Brands constitute 42% of total ICH sales in H1FY23 (+40% YoY).The company launched 10 new products and 11 SKUs

🧪New products contribute 20% to sales

(13/18)

🧪Power Brands constitute 42% of total ICH sales in H1FY23 (+40% YoY).The company launched 10 new products and 11 SKUs

🧪New products contribute 20% to sales

(13/18)

Strong Compliance:-

In the first half of the year:-

We cleared more than 20 regulatory inspections at various plants

-Nandini Piramal,Piramal Pharma

(14/18)

In the first half of the year:-

We cleared more than 20 regulatory inspections at various plants

-Nandini Piramal,Piramal Pharma

(14/18)

Capex Plans:

🧪Through customer-led Brownfield expansions, the company is expanding capacities at our major sites

including Aurora, Pithampur, Riverview, Grangemouth and Mahad.

(15/18)

🧪Through customer-led Brownfield expansions, the company is expanding capacities at our major sites

including Aurora, Pithampur, Riverview, Grangemouth and Mahad.

(15/18)

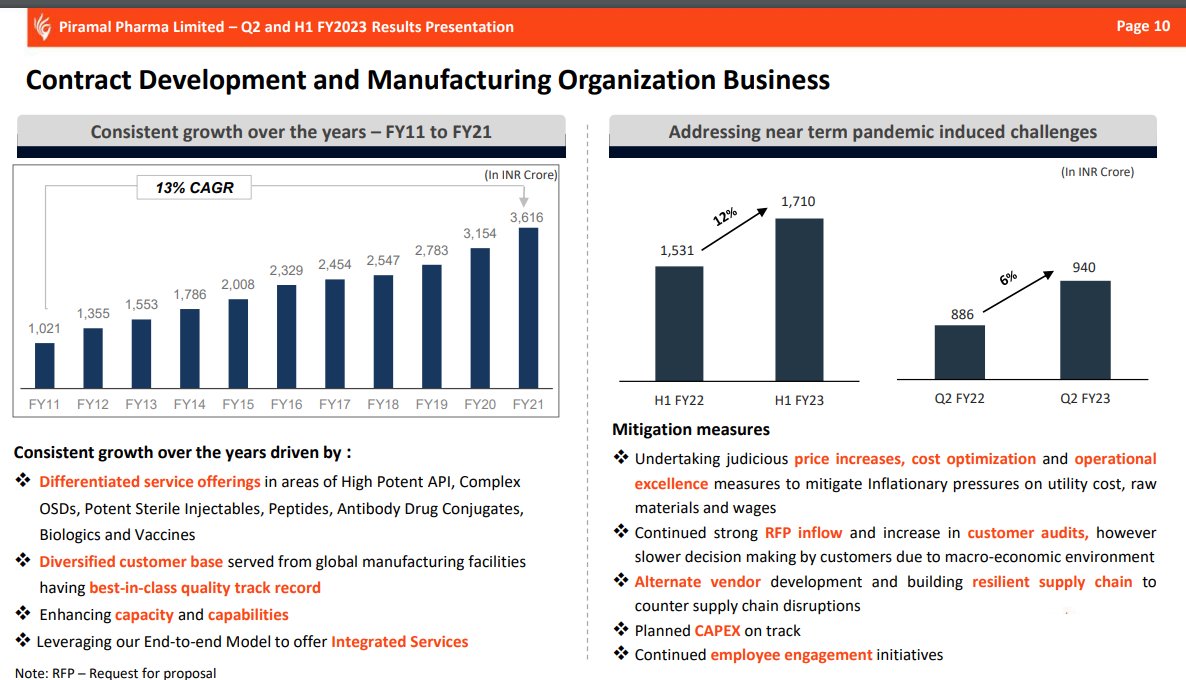

🧪In all, the company committed about $157 million of growth-oriented CAPEX investments across the various sites, which is expected to be completed over the next 18 to 24 months

(16/18)

(16/18)

Valuation:-

Given the slowdown in the CDMO business and the lower margins at which the business operates

Piramal Pharma traddes at 18x EV/EBIDTA

This is certainly not cheap

(17/18)

Given the slowdown in the CDMO business and the lower margins at which the business operates

Piramal Pharma traddes at 18x EV/EBIDTA

This is certainly not cheap

(17/18)

Conclusion:-

Piramal Pharma is a class company with a good compliance record.

The company faced near-term challenges-

1. Slowdown in CDMO Business

2. Increase in raw material prices

These challenges are short-term in nature.

One must keep this company on the radar.

(18/18)

Piramal Pharma is a class company with a good compliance record.

The company faced near-term challenges-

1. Slowdown in CDMO Business

2. Increase in raw material prices

These challenges are short-term in nature.

One must keep this company on the radar.

(18/18)

Disclaimer:-

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

Loading suggestions...