(1/20)

About:

GMM Pfaudler manufactures GLE, heavy engineering & proprietary products.

It is a leading supplier of process equipments to the pharmaceutical and chemical industries

It has 14 manufacturing facilities globally. With 7 in Europe & 3 in India.

About:

GMM Pfaudler manufactures GLE, heavy engineering & proprietary products.

It is a leading supplier of process equipments to the pharmaceutical and chemical industries

It has 14 manufacturing facilities globally. With 7 in Europe & 3 in India.

(2/20)

Journey of GMM:

Journey of GMM:

(3/20)

Key Growth Drivers for Pharma Industry:

• Policy Support:

PLI scheme, an initiative by the

government has changed

the outlook and sentiment of

Indian market in the global

arena.

As of March 2022, govt has

approved 19 applications of

₹4,623 cr, under PLI scheme.

Key Growth Drivers for Pharma Industry:

• Policy Support:

PLI scheme, an initiative by the

government has changed

the outlook and sentiment of

Indian market in the global

arena.

As of March 2022, govt has

approved 19 applications of

₹4,623 cr, under PLI scheme.

(4/20)

• Cost-effectiveness:

Pharma companies

in India possess the ability

to produce high-quality

products at an economical

rate.

Low-cost manufacturing

will help them leverage the

opportunity of $5-6 bn

emerging from patent expiry

across the globe in the next

4-5 years.

• Cost-effectiveness:

Pharma companies

in India possess the ability

to produce high-quality

products at an economical

rate.

Low-cost manufacturing

will help them leverage the

opportunity of $5-6 bn

emerging from patent expiry

across the globe in the next

4-5 years.

(5/20)

Specialty Chemical

Industry:

• With an increase in domestic

production of specialty

chemicals, exports are

expected to rise too

• Improved compliance adherence with strong R&D culture, contract

manufacturing opportunity

and focus of nations on China +1

Specialty Chemical

Industry:

• With an increase in domestic

production of specialty

chemicals, exports are

expected to rise too

• Improved compliance adherence with strong R&D culture, contract

manufacturing opportunity

and focus of nations on China +1

(6/20)

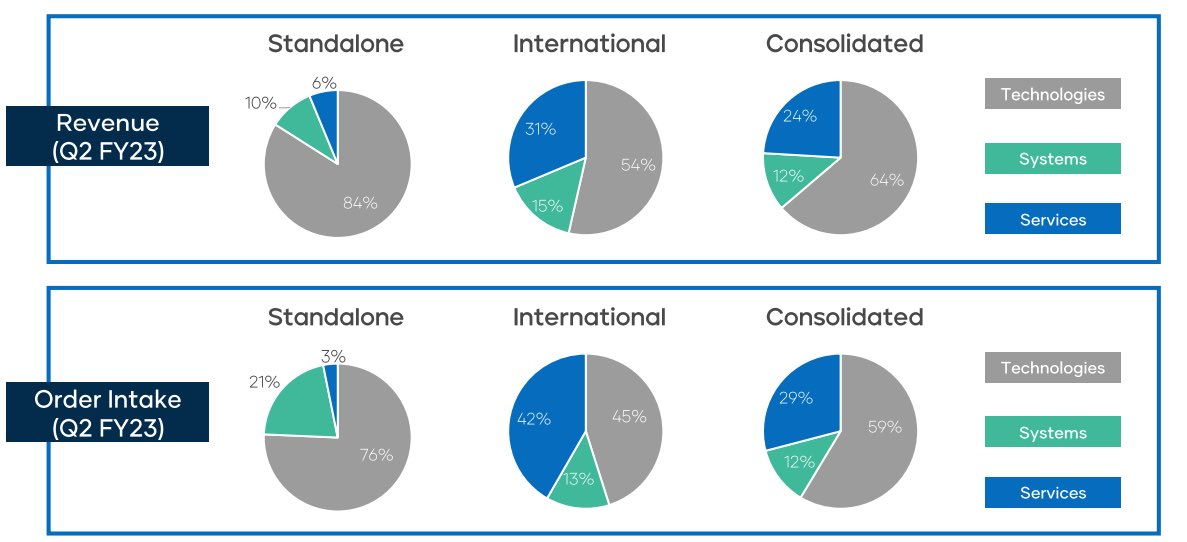

• Business Overview

GMM Pfaudler is present

across Americas, Europe and

Asia through its offerings in

technologies, systems and

services. The company

has sustained its business

relations with marquee

customer base & continues

to strengthen the same.

• Business Overview

GMM Pfaudler is present

across Americas, Europe and

Asia through its offerings in

technologies, systems and

services. The company

has sustained its business

relations with marquee

customer base & continues

to strengthen the same.

(7/20)

Business Highlights:

• Cross-selling of multiple products to customers globally resulting in increased customer spend

• Breakthrough in new markets such as Spain, SE Asia & Eastern Europe

• Gained market share in US & Europe by offering cost-effective solutions

Business Highlights:

• Cross-selling of multiple products to customers globally resulting in increased customer spend

• Breakthrough in new markets such as Spain, SE Asia & Eastern Europe

• Gained market share in US & Europe by offering cost-effective solutions

(8/20)

• Acid Recovery business continues to grow with new orders from South Korea, China and India

• Process know-how and green technologies being developed to target new high growth sectors

• Dedicated engineering and process teams to grow systems business

• Acid Recovery business continues to grow with new orders from South Korea, China and India

• Process know-how and green technologies being developed to target new high growth sectors

• Dedicated engineering and process teams to grow systems business

(9/20)

Acquisition:

The global acquisition has opened multiple growth levers for GMM Pfaudler Limited in terms of competitive sourcing, widening the customer base, broadening the products and solutions portfolio, and opening considerable cross-selling opportunities

Acquisition:

The global acquisition has opened multiple growth levers for GMM Pfaudler Limited in terms of competitive sourcing, widening the customer base, broadening the products and solutions portfolio, and opening considerable cross-selling opportunities

(10/20)

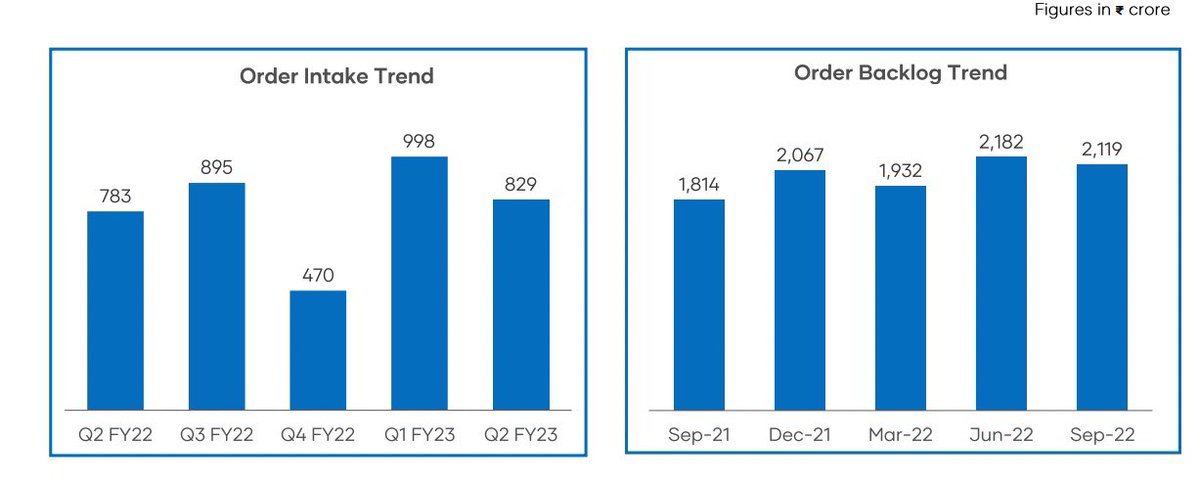

Order Intake & Backlog Trend:

The company is expecting India’s backlog in the glass lined business to range between 4-6 months.

And that the glass line in India is going to be a big driver for them in the next few quarters.

Order Intake & Backlog Trend:

The company is expecting India’s backlog in the glass lined business to range between 4-6 months.

And that the glass line in India is going to be a big driver for them in the next few quarters.

(11/20)

Increase in receivables:

The company’s receivable days is seeing an uptrend. And it is going up for both for India and International markets.

The company expects to get the collection going from this quarter onwards. So we can keep an eye on this number in the future.

Increase in receivables:

The company’s receivable days is seeing an uptrend. And it is going up for both for India and International markets.

The company expects to get the collection going from this quarter onwards. So we can keep an eye on this number in the future.

(12/20)

Company’s Europe Business:

The company is doing better than expected in Europe which is a positive. It is seeing demand as well as it is able to transfer rise in input prices to its customers.

It has added new small businesses,

through M&A which is seeing growth.

Company’s Europe Business:

The company is doing better than expected in Europe which is a positive. It is seeing demand as well as it is able to transfer rise in input prices to its customers.

It has added new small businesses,

through M&A which is seeing growth.

(13/20)

Key Strengths:

• Market leadership in the domestic GLE industry:

It is the market leader in the domestic GLE segment, with a share of around 55%.

The group has a near monopoly in large vessel segment. However, We should keep an eye on M&As taking place.

Key Strengths:

• Market leadership in the domestic GLE industry:

It is the market leader in the domestic GLE segment, with a share of around 55%.

The group has a near monopoly in large vessel segment. However, We should keep an eye on M&As taking place.

(14/20)

• Strong technological expertise and market presence of Pfaudler group in global markets

The company has acquired technology for manufacturing GLE from Pfaudler and has access to the diversified product mix and strong research and development capabilities of the group.

• Strong technological expertise and market presence of Pfaudler group in global markets

The company has acquired technology for manufacturing GLE from Pfaudler and has access to the diversified product mix and strong research and development capabilities of the group.

(15/20)

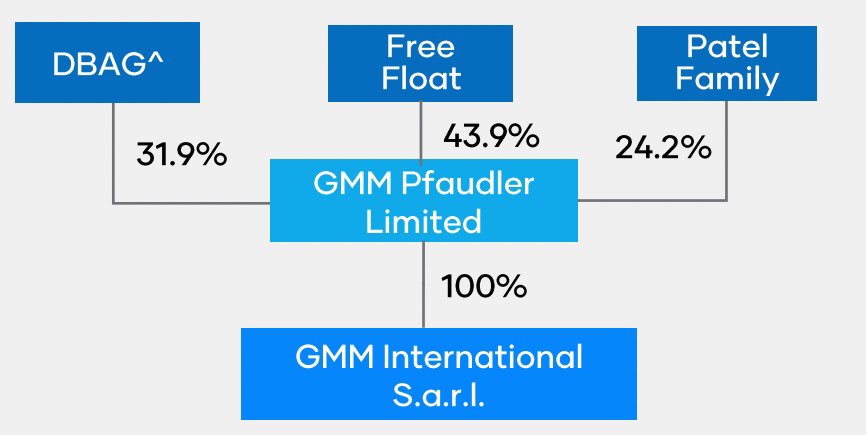

Post Acquisition Shareholding Pattern:

• GMMP is holding 100% stake in the 17 Pfaulder International entities through GMMI.

• Equity stake of Patel family in GMMP increased from 22.3% to 24.2%.

• DBAG continues to hold 31.9% in GMMP (currently 32.7%).

Post Acquisition Shareholding Pattern:

• GMMP is holding 100% stake in the 17 Pfaulder International entities through GMMI.

• Equity stake of Patel family in GMMP increased from 22.3% to 24.2%.

• DBAG continues to hold 31.9% in GMMP (currently 32.7%).

(16/20)

Weakness:

• Financial risk profile

GMMP has a total debt of ₹878 cr as on 31 March 2022, which includes pension liabilities worth ₹373 cr.

• Net gearing increased to 0.7 times (from 0.3 times) as on September 30, 2022

Weakness:

• Financial risk profile

GMMP has a total debt of ₹878 cr as on 31 March 2022, which includes pension liabilities worth ₹373 cr.

• Net gearing increased to 0.7 times (from 0.3 times) as on September 30, 2022

(17/20)

• Large working capital requirement

Typically inventory days range from 100-120 days while debtor days remain around 40-50 days.

Operations may remain susceptible to inventory pricing risk and potential delays by customers in taking deliveries.

• Large working capital requirement

Typically inventory days range from 100-120 days while debtor days remain around 40-50 days.

Operations may remain susceptible to inventory pricing risk and potential delays by customers in taking deliveries.

(18/20)

Key Ratios & Numbers:

• Market Cap: ₹8,308 cr

• Stock P/E: 52.8

• RoCE 3 Years: 17.3%

• RoE 3 Years: 20.2%

• Debt: ₹888cr

• PEG: 2.37

• Price to Sales: 2.90

• OPM 5 years: 13.4%

• Cash Conversion Cycle: 151

Key Ratios & Numbers:

• Market Cap: ₹8,308 cr

• Stock P/E: 52.8

• RoCE 3 Years: 17.3%

• RoE 3 Years: 20.2%

• Debt: ₹888cr

• PEG: 2.37

• Price to Sales: 2.90

• OPM 5 years: 13.4%

• Cash Conversion Cycle: 151

(19/20)

GMM Pfaudler should continue to benefit from its strong market position in the GLE segment & technological support from the Pfaudler group. The company is likely to maintain a healthy financial risk profile through steady cash accrual & benefits of synergies flowing in.

GMM Pfaudler should continue to benefit from its strong market position in the GLE segment & technological support from the Pfaudler group. The company is likely to maintain a healthy financial risk profile through steady cash accrual & benefits of synergies flowing in.

(20/20)

What’s your view about the company and it’s medium term performance?

@caniravkaria @kuttrapali26 @chartmojo

What’s your view about the company and it’s medium term performance?

@caniravkaria @kuttrapali26 @chartmojo

Loading suggestions...