Ammo Inc $POWW released earnings last night and the stock is down 25%+ today.

The company is an excellent case study on why you should change your mind in the face of disconfirming evidence.

Some thoughts on the biz, ER, and how I'm thinking about the situation from here ...🧵

The company is an excellent case study on why you should change your mind in the face of disconfirming evidence.

Some thoughts on the biz, ER, and how I'm thinking about the situation from here ...🧵

1/ Backstory

I used to be a $POWW bull. I found them around $1.75/share and thought they had a chance to really ramp revenue and reach profitability.

They even bought Gunbroker, which I thought was a terrific acquisition.

I wrote about it below.

macro-ops.com

I used to be a $POWW bull. I found them around $1.75/share and thought they had a chance to really ramp revenue and reach profitability.

They even bought Gunbroker, which I thought was a terrific acquisition.

I wrote about it below.

macro-ops.com

2/ GunBroker

GunBroker made sense to me. It was a differentiated asset with high (50%+) profit margins.

It required very little capex to maintain. They also had some low hanging fruit to improve the product (UI/UX, purchase flow, etc.).

Plus, they paid 4x EBIT for It.

GunBroker made sense to me. It was a differentiated asset with high (50%+) profit margins.

It required very little capex to maintain. They also had some low hanging fruit to improve the product (UI/UX, purchase flow, etc.).

Plus, they paid 4x EBIT for It.

3/ When Things Changed

June's earnings revealed a few things:

- The ammunition business was deteriorating

- Growth slowing at GunBroker

- Bad capital allocation

- Balance sheet discrepancies

- Wild EBITDA add-backs

No bueno.

I went deeper here: macro-ops.com

June's earnings revealed a few things:

- The ammunition business was deteriorating

- Growth slowing at GunBroker

- Bad capital allocation

- Balance sheet discrepancies

- Wild EBITDA add-backs

No bueno.

I went deeper here: macro-ops.com

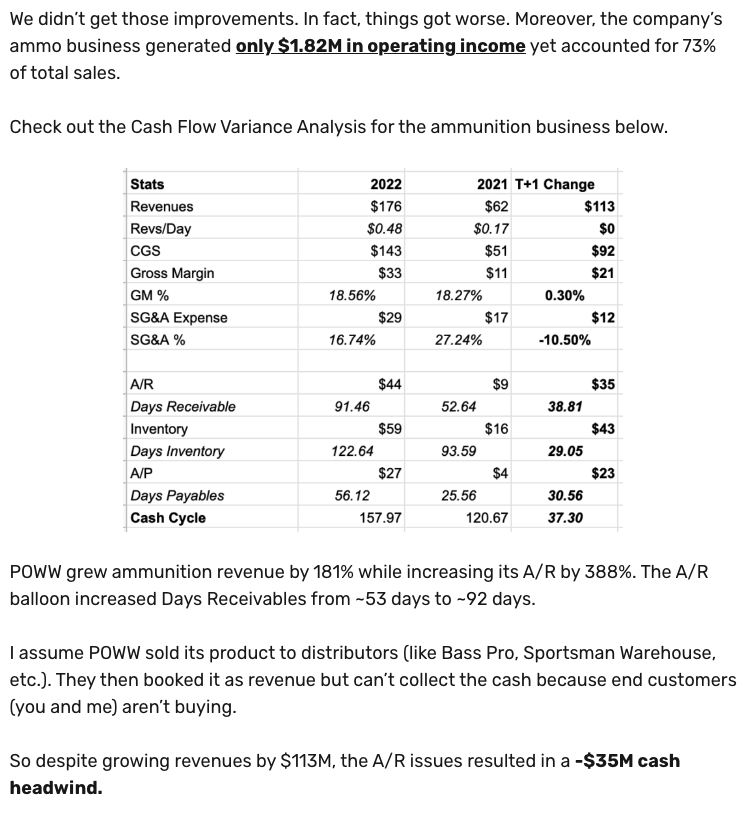

4/ Canary in Coal Mine: Failing Ammo Biz

$POWW's ammo biz had serious issues. The segment lost money as it grew.

More importantly, I didn't see a way the company could leverage its Inv + A/R to change that fact.

Sales grew by 181%. But A/R grew by 388%. Major red flag.

$POWW's ammo biz had serious issues. The segment lost money as it grew.

More importantly, I didn't see a way the company could leverage its Inv + A/R to change that fact.

Sales grew by 181%. But A/R grew by 388%. Major red flag.

5/ Canary in the Coal Mine Cont ...

Then there was Inventory. Which last quarter increased from 93 Days to 123 Days.

In other words, $POWW was struggling to sell its product through its channels.

At that rate, $POWW was losing $0.72 for every $1 in ammo manufacturing growth

Then there was Inventory. Which last quarter increased from 93 Days to 123 Days.

In other words, $POWW was struggling to sell its product through its channels.

At that rate, $POWW was losing $0.72 for every $1 in ammo manufacturing growth

6/ Steve Urvan Goes Activist

It wasn't surprising that former GunBroker CEO, Steve Urvan, went activist.

He highlighted many of the issues I explained a month or so prior.

What did $POWW do? Fire him and kick him off the board.

Hard to argue with those numbers, right?

It wasn't surprising that former GunBroker CEO, Steve Urvan, went activist.

He highlighted many of the issues I explained a month or so prior.

What did $POWW do? Fire him and kick him off the board.

Hard to argue with those numbers, right?

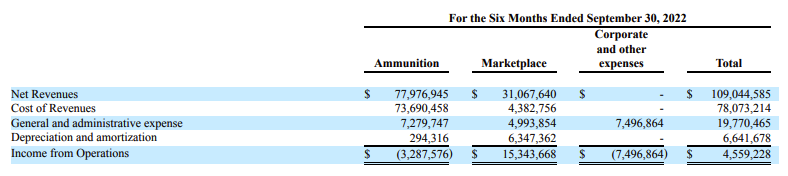

7/ Where Are We Now: Latest Earnings

How is $POWW doing today?

The ammo manufacturing biz is losing money at a ~$6M annualized run rate. Which you could've seen had you read the balance sheet tea leaves (A/R & Inventory!).

GunBroker is on pace to generate $30M in profits.

How is $POWW doing today?

The ammo manufacturing biz is losing money at a ~$6M annualized run rate. Which you could've seen had you read the balance sheet tea leaves (A/R & Inventory!).

GunBroker is on pace to generate $30M in profits.

8/ Where Do We Go From Here?

It's obvious that $POWW's manufacturing business is worth more dead than alive.

So what should they do?

Close the manufacturing plant, sell any relevant assets.

And focus 100% on GunBroker.

But you need an entirely new management team.

It's obvious that $POWW's manufacturing business is worth more dead than alive.

So what should they do?

Close the manufacturing plant, sell any relevant assets.

And focus 100% on GunBroker.

But you need an entirely new management team.

9/ Is There Even A Mispricing?

$POWW currently trades at a $230M Enterprise Value ($29M in cash, 75% of existing receivables less $10M LT debt).

In other words, you're paying ~8x run-rate GunBroker profits for the biz.

What would GB be worth to someone like $RGR or $SWBI?

$POWW currently trades at a $230M Enterprise Value ($29M in cash, 75% of existing receivables less $10M LT debt).

In other words, you're paying ~8x run-rate GunBroker profits for the biz.

What would GB be worth to someone like $RGR or $SWBI?

10/ Takeaway: Follow The Cash Flow

I changed my mind on $POWW because the facts changed.

The company was determined to invest in a commodity product that (IMO) couldn't reach terminal profitability.

I got out in time.

Remember, Follow The Cash Flow. macro-ops.com

I changed my mind on $POWW because the facts changed.

The company was determined to invest in a commodity product that (IMO) couldn't reach terminal profitability.

I got out in time.

Remember, Follow The Cash Flow. macro-ops.com

Loading suggestions...