Kitty’s Semi thread!

Semiconductor thread focusing on CPUs/GPUs from NVDA, AMD and INTC. Some alpha but mainly about what the future will bring.

Part 1: Current Market outlook

Part 2: companies competetive adv.

Part 3: Why this is the apex of NVDAs graphics/compute dominance

Semiconductor thread focusing on CPUs/GPUs from NVDA, AMD and INTC. Some alpha but mainly about what the future will bring.

Part 1: Current Market outlook

Part 2: companies competetive adv.

Part 3: Why this is the apex of NVDAs graphics/compute dominance

TLDR: Wouldn’t touch NVDA, INTC for quite a while, AMD on the other hand might be a good buy in the coming months/year (after another significant drop). Reason being current/upcoming margin suppression. (1/n)

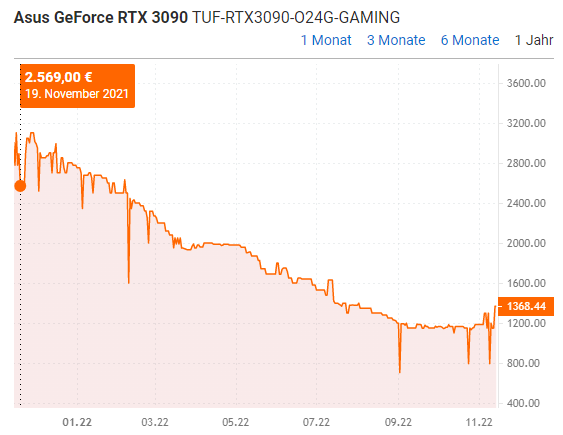

GPU price declines have been quiete insane this year. Rtx 3090 going for 1100$ (800 used) since September. Thats more than 1/2 decline from 2800$ (2400 used) in early January. Tho Prices have recently somewhat stabilized, prices in the used market will likly drop further. (2/N)

Primary reason are ofc crypto miners, rumors surgest that many miners are still sitting on lots of cards and waiting for prices to go back up again. That could backfire with the release of AMDs new 7900 xtx. (3/N)

Because of this competition from the used market, as well as new competition from intel and even China. I highly doubt that they will be able to achieve margin from 20-40% anytime soon. (4/N)

Now part 2 ------------------------------------

Summary and moat of the 3 cos:

Might be nothing new for some,

for juicy alpha skip to part 3! (14/N)

(5/N)

Summary and moat of the 3 cos:

Might be nothing new for some,

for juicy alpha skip to part 3! (14/N)

(5/N)

First thing to say is that there is still rapid development ongoing in semis, and I am quite excited that more innovation and performance leaps are likely to come.

Moores law might not be that dead after all.

(6/N)

Moores law might not be that dead after all.

(6/N)

NVDAs competitive advantage:

Right now they do have the most powerful chips, but their real advantage is their software integration and advancements in AI.

(7/N)

Right now they do have the most powerful chips, but their real advantage is their software integration and advancements in AI.

(7/N)

NVDA working very closely with the most popular Machine learning libraries (i.e pytorch, Tensorflow. Xgboost) and their achievents in that field have been quite impressive. For hardware accelerated ai they are and will be the biggest player.

(8/N)

(8/N)

AMD:

Incredible progress over the past couple of years, from being close to bankrupt in 2015 too having the most powerful cpus and taking large market share for intel (especially DIY and consumer mindshare). What they where able to achieve with a tiny budget was remarkable.

(9/N)

Incredible progress over the past couple of years, from being close to bankrupt in 2015 too having the most powerful cpus and taking large market share for intel (especially DIY and consumer mindshare). What they where able to achieve with a tiny budget was remarkable.

(9/N)

Competitive advantage:

They not only produce the most powerful CPUs but are also very close to NVDA regarding GPU performance. That’s makes them the only company that is competitive in both segments. Their infinity fabric/chiplet architecture makes scaling super easy.

(10/N)

They not only produce the most powerful CPUs but are also very close to NVDA regarding GPU performance. That’s makes them the only company that is competitive in both segments. Their infinity fabric/chiplet architecture makes scaling super easy.

(10/N)

INTC:

They are spending an unholy amount of $ for r&d, and aiming to get the performance crown back form AMD ( they aim for 2025). INTC is also planning to enter the GPU market and taking market share. CEO Pat Gelsinger as huge aspirations.

(11/N)

They are spending an unholy amount of $ for r&d, and aiming to get the performance crown back form AMD ( they aim for 2025). INTC is also planning to enter the GPU market and taking market share. CEO Pat Gelsinger as huge aspirations.

(11/N)

Competitive advantage:

Intel is the one semiconductor that not only designs their own chips, but can also produce them in own foundries. For that AMD and NVDA are dependent on TSMC, and in case China does anything stupid, INTC will benefit.

(12/N)

Intel is the one semiconductor that not only designs their own chips, but can also produce them in own foundries. For that AMD and NVDA are dependent on TSMC, and in case China does anything stupid, INTC will benefit.

(12/N)

Also, withith the amount of R&D they spend in the last years they for sure have some interesting products in their pipeline and might be competitive again in the coming years.

(13/N)

(13/N)

Part 3 ------------------------------------

Now getting in the more technical stuff:

(14/N)

Now getting in the more technical stuff:

(14/N)

AMD Chiplets:

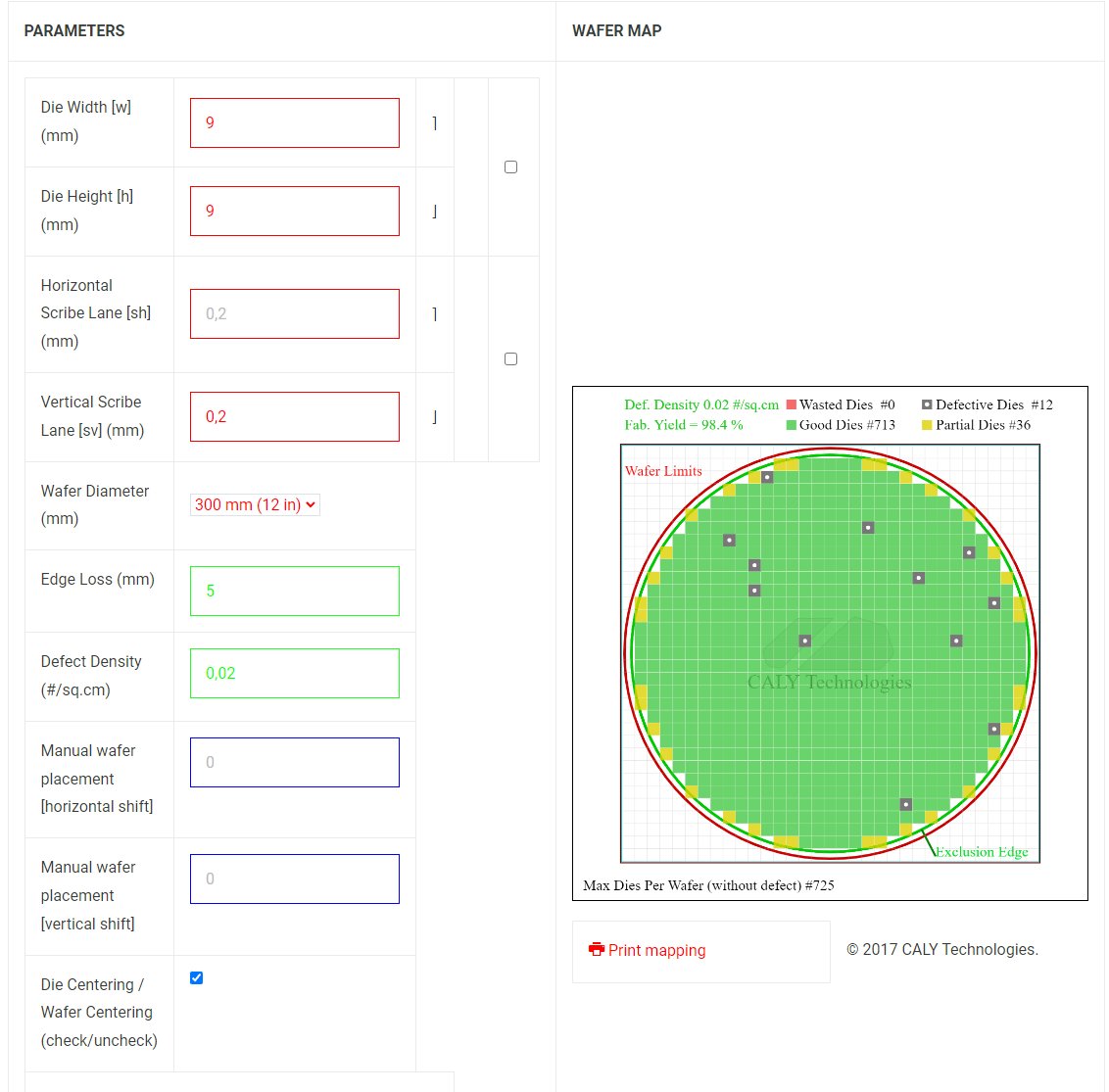

Every New processor gets printed (in case of TSMC 5nm) with EUV light on a silicone waver. Every wave can be used to produce multiple chips, and often some of these chips have defects because of particles that’s disrupt the light projected on the waver.

(15/N)

Every New processor gets printed (in case of TSMC 5nm) with EUV light on a silicone waver. Every wave can be used to produce multiple chips, and often some of these chips have defects because of particles that’s disrupt the light projected on the waver.

(15/N)

Because Silicon wavers are expensive to produce, (TSMC 5nm waver is expected to cost 9000$) using every inch of waver space is essential for achieving high profit margins. You can see how a smaller die (left) increase the fab yield by quite a lot.

(16/N)

(16/N)

AMDs chiplet technology makes this possible by using multiple dies for a single processor (gpu in the future). This is not easy to achieve and will took AMD years to implement properly.

And now, why right now might be the apex of NVDAs graphics/compute dominance:

(17/N)

And now, why right now might be the apex of NVDAs graphics/compute dominance:

(17/N)

First of all, the maximum die size reachable with the tsmc 4nm node is 858mm^2. NVDAs new 4090 is 608mm^2 with 16,384 Shading Cores, so there have about 40% more shaders (23k) left in the tank on the 4nm process node.

(18/N)

(18/N)

AMDs new 7900 xtx (5nm node) has a shader count of 12,288, but that’s on a die size of 300mm^2. That means unlike NVDA, AMD is not limited by die size and they have lots of headroom regarding shader counts for the future (35k shaders on a single 5nm die).

(19/N)

(19/N)

So NVDA limiting factor for future performance will be die size and they can only increase performance with a better process Node from TSMC. Or ofc they have a chiplet architecture already in the making, which is unlikely and takes alot of time.

(20/N)

(20/N)

Thus, we will probably see AMD take the performance crown for GPUs in the coming years. Which most people /analysts dont think is possible.

(21/N)

Fin.

(21/N)

Fin.

@kittysquiddy first thread ever, done :)

Loading suggestions...