Technology

Crime

Finance

Cryptocurrency

Financial Fraud

Business Analysis

Investigative Journalism

Financial Crime

1/82

I'll be pinning this detailed timeline, as my final piece covering this topic, as now the case is closed in my mind.

This was a crime plain and simple and I'll put no more wind in this criminals sails:

FTX: Meltdown.

The definitive and chronological thread.

I'll be pinning this detailed timeline, as my final piece covering this topic, as now the case is closed in my mind.

This was a crime plain and simple and I'll put no more wind in this criminals sails:

FTX: Meltdown.

The definitive and chronological thread.

2/82

Sept 30th, 2022:

On September 30th, I noticed an odd behavior, that while other exchanges were declining in their Ethereum "open interest" (amount of futures contracts bought on leverage)

FTX was not.

It was at an all time high:

Sept 30th, 2022:

On September 30th, I noticed an odd behavior, that while other exchanges were declining in their Ethereum "open interest" (amount of futures contracts bought on leverage)

FTX was not.

It was at an all time high:

3/82

At the time, we didn't know why.

We'd later learn that the FTX<>Alameda relationship had for years misused customer funds illegally, and set up their systems in a way to maximize every dollar for their own benefit.

At the time, we didn't know why.

We'd later learn that the FTX<>Alameda relationship had for years misused customer funds illegally, and set up their systems in a way to maximize every dollar for their own benefit.

4/82

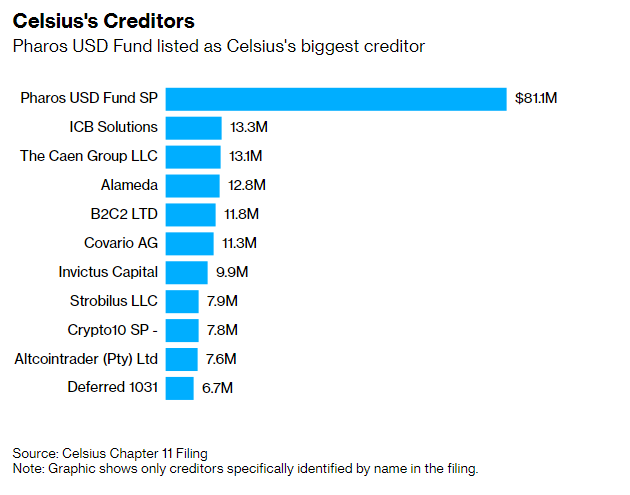

We had learned over the Summer that FTX had been using their $FTT and $SRM tokens to get large loans from centralized lenders like BlockFi and Celsius, often selling the assets they borrowed, distressing the markets and then buying out these distressed lenders.

We had learned over the Summer that FTX had been using their $FTT and $SRM tokens to get large loans from centralized lenders like BlockFi and Celsius, often selling the assets they borrowed, distressing the markets and then buying out these distressed lenders.

5/82

So what is the problem with these tokens?

They are primarily controlled by Alameda, with a low circulating supply.

It would be as if you sold one single strand of your hair for $100, and now claimed that the rest of all our hair was worth $1T in collateral.

So what is the problem with these tokens?

They are primarily controlled by Alameda, with a low circulating supply.

It would be as if you sold one single strand of your hair for $100, and now claimed that the rest of all our hair was worth $1T in collateral.

6/82

But, the market assumed that these games stopped with simply bad lenders making deals they shouldn't have.

We were wrong.

In early October SBF began to quietly lobby the US congress for the DCCPA bill:

But, the market assumed that these games stopped with simply bad lenders making deals they shouldn't have.

We were wrong.

In early October SBF began to quietly lobby the US congress for the DCCPA bill:

7/82

This bill would effectively ban decentralized finance, and force consumers to use centralized products like FTX.

There was a pattern emerging here that none of us saw at the time.

An obvious thread in hindsight, where everything was about putting more assets in FTX.

This bill would effectively ban decentralized finance, and force consumers to use centralized products like FTX.

There was a pattern emerging here that none of us saw at the time.

An obvious thread in hindsight, where everything was about putting more assets in FTX.

8/82

We later learned than whenever FTX/Alameda invested in an entity, they often told the projects to use the FTX exchange as their bank account/keep their assets on the exchange, as a part of the deal term.

This DCCPA bill was the same mantra, more assets on the exchange

We later learned than whenever FTX/Alameda invested in an entity, they often told the projects to use the FTX exchange as their bank account/keep their assets on the exchange, as a part of the deal term.

This DCCPA bill was the same mantra, more assets on the exchange

9/82

October 19th:

Near the end of October, lawyer @lex_node managed to get and release a copy of the DCCPA bill that had been floated around Washington as a draft.

The community, seeing that it would result in banning DeFi expressed their outrage towards Sam.

October 19th:

Near the end of October, lawyer @lex_node managed to get and release a copy of the DCCPA bill that had been floated around Washington as a draft.

The community, seeing that it would result in banning DeFi expressed their outrage towards Sam.

10/82

Over the coming days, Sam was erratic, aggressive and insulting to just about everyone.

It's also where he made his now infamous jab at Binance CEO CZ about not traveling to DC.

Over the coming days, Sam was erratic, aggressive and insulting to just about everyone.

It's also where he made his now infamous jab at Binance CEO CZ about not traveling to DC.

11/82

To this day, Sam wrongly claims that this led to CZ attacking the value of their token and collapsing their exchange. (But more on that soon)

The flippant tone of SBF struck the community as odd. It seemed like something was clearly wrong behind the scenes.

To this day, Sam wrongly claims that this led to CZ attacking the value of their token and collapsing their exchange. (But more on that soon)

The flippant tone of SBF struck the community as odd. It seemed like something was clearly wrong behind the scenes.

12/82

November 2nd:

On November 2nd, Coindesk then published an overview of Alameda's assets, which suggested that Alameda could be insolvent:

coindesk.com

November 2nd:

On November 2nd, Coindesk then published an overview of Alameda's assets, which suggested that Alameda could be insolvent:

coindesk.com

13/82

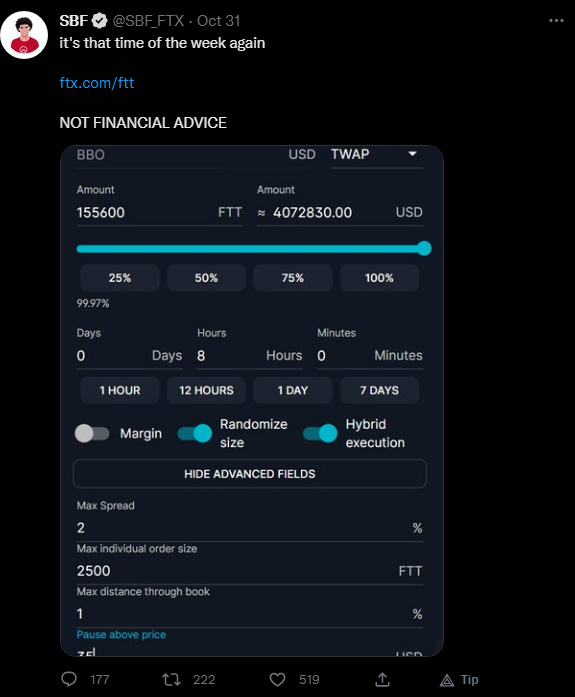

Rather than respond to these posts, Sam continued with business as usual, even his new and sudden tradition of posting a teaser of the weekly $FTT buy backs each week, trying to raise the value of the token:

Rather than respond to these posts, Sam continued with business as usual, even his new and sudden tradition of posting a teaser of the weekly $FTT buy backs each week, trying to raise the value of the token:

14/82

We learned then, that Alameda had over $8b of loans on their books, that was primarily backed by their $FTT token - something that no sophisticated lending desk (the type that would have $8b to spare) would ever allow.

Except perhaps FTX...

We learned then, that Alameda had over $8b of loans on their books, that was primarily backed by their $FTT token - something that no sophisticated lending desk (the type that would have $8b to spare) would ever allow.

Except perhaps FTX...

15/82

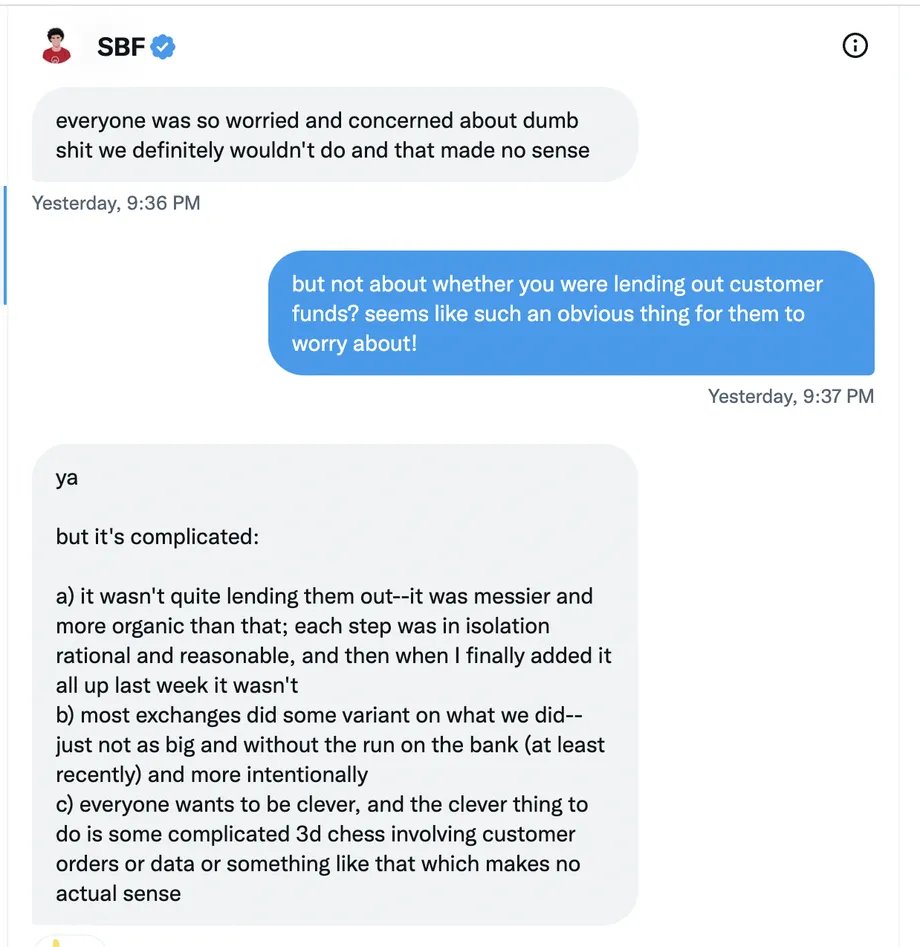

This is when we became alarmed.

You see unlike a bank, a crypto exchange isn't authorized to simply lend all your assets, unless its outlined in their terms of service, or unless you opt-in to a specific lending product.

This is when we became alarmed.

You see unlike a bank, a crypto exchange isn't authorized to simply lend all your assets, unless its outlined in their terms of service, or unless you opt-in to a specific lending product.

16/82

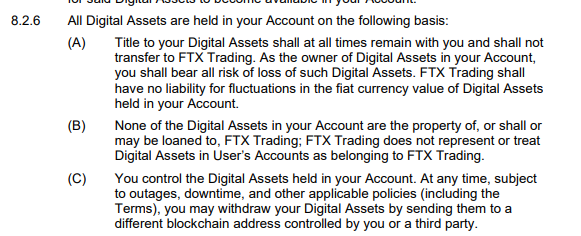

FTX's terms of service expressly require that you retain title to your assets, which means, if they use them for any purpose other than what you direct them to, it's legally theft.

FTX's terms of service expressly require that you retain title to your assets, which means, if they use them for any purpose other than what you direct them to, it's legally theft.

17/82

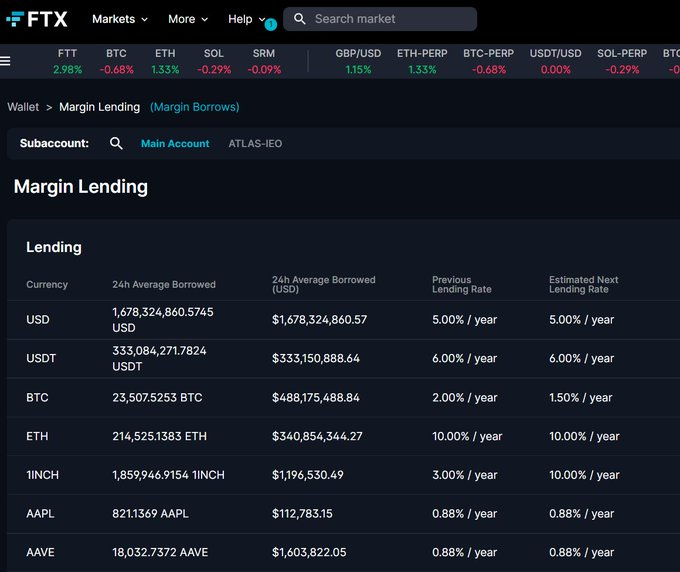

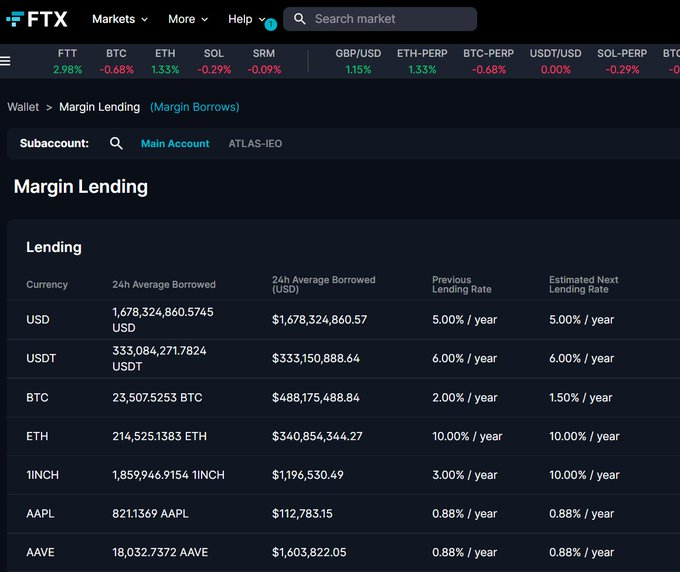

But, FTX's opt in lending market only showed around $2.8B in peer-to-peer authorized lending.

Something that wouldn't make up the total number required to lend to Alameda.

But, FTX's opt in lending market only showed around $2.8B in peer-to-peer authorized lending.

Something that wouldn't make up the total number required to lend to Alameda.

18/82

FTX also had an "Earn" program through the old Blockfolio app but it was later confirmed by head of sales @tackettzane that (at least as far as FTX employees were told) these funds came from marketing dollars and not lending.

FTX also had an "Earn" program through the old Blockfolio app but it was later confirmed by head of sales @tackettzane that (at least as far as FTX employees were told) these funds came from marketing dollars and not lending.

19/82

Since historical snapshots of FTX's balance on November 3rd showed only about $3B in assets, of which $1.4B was their own token, this suggested two possibilities:

-FTX had an undocumented "cold wallet" somewhere

-FTX was illegally lending (stealing) user assets.

Since historical snapshots of FTX's balance on November 3rd showed only about $3B in assets, of which $1.4B was their own token, this suggested two possibilities:

-FTX had an undocumented "cold wallet" somewhere

-FTX was illegally lending (stealing) user assets.

20/82

Given I had seen lots of large FTT transaction sold over the counter (peer to peer rather than on exchange) the past few weeks, I figured FTX was trying to cover up a hole:

Given I had seen lots of large FTT transaction sold over the counter (peer to peer rather than on exchange) the past few weeks, I figured FTX was trying to cover up a hole:

21/82

That was when Binance moved their $583M of FTT left over from their investment in FTX.

The next morning CZ made a rare announcement of their intent to sell their FTT:

That was when Binance moved their $583M of FTT left over from their investment in FTX.

The next morning CZ made a rare announcement of their intent to sell their FTT:

22/82

He noted irregularities among FTX.

While I had suspected a small gap in finances, this seemed like something much larger.

Which was suddenly confirmed when Alameda CEO Caroline broke he silence about finances, and offered to buy out the remaining FTT

He noted irregularities among FTX.

While I had suspected a small gap in finances, this seemed like something much larger.

Which was suddenly confirmed when Alameda CEO Caroline broke he silence about finances, and offered to buy out the remaining FTT

23/82

It was an odd choice for her to publicly name a price and odd for Alameda to care about the specific price.

It was this moment that set off tons of onchain sleuthing.

It was an odd choice for her to publicly name a price and odd for Alameda to care about the specific price.

It was this moment that set off tons of onchain sleuthing.

24/82

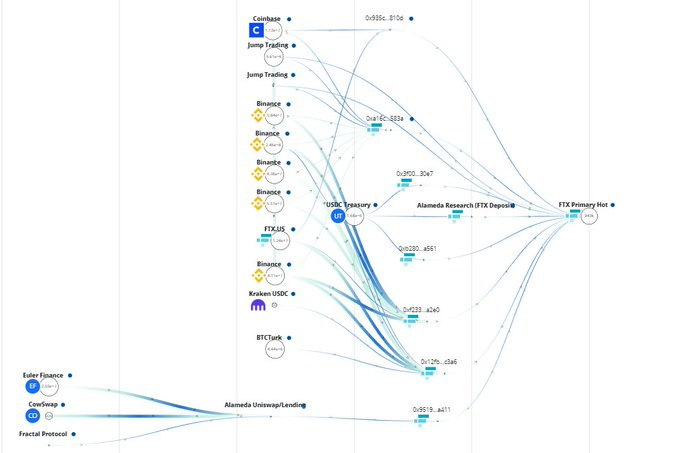

As withdrawals picked up on FTX's exchange - we noticed that Alameda's wallets started pulling stablecoins from everywhere to refill the FTX hot wallet:

As withdrawals picked up on FTX's exchange - we noticed that Alameda's wallets started pulling stablecoins from everywhere to refill the FTX hot wallet:

25/82

It's important to remember that this was November 6th, an entire day before the date that SBF claims the exchange was still fully solvent:

It's important to remember that this was November 6th, an entire day before the date that SBF claims the exchange was still fully solvent:

26/82

This meant there should have been no external funds needed in order to withdraw, as you retain title to your assets.

The balances that you see reported in FTX should remain in 1:1 in their possession at all times.

This meant there should have been no external funds needed in order to withdraw, as you retain title to your assets.

The balances that you see reported in FTX should remain in 1:1 in their possession at all times.

27/82

The one exception to that is USD, where they treat fiat (money in a bank account) and USDT, USDC, USDP and other stablecoins as one singular balance across all chains, meaning sometimes they have to trade them with market makers like Alameda to give you the one you request

The one exception to that is USD, where they treat fiat (money in a bank account) and USDT, USDC, USDP and other stablecoins as one singular balance across all chains, meaning sometimes they have to trade them with market makers like Alameda to give you the one you request

28/82

On the 6th, FTX claimed that was what was slowing their deposits, and why stablecoin balances were only being refilled by Alameda and not by a cold wallet used to store user assets.

But then the balances of ETH began to get low as well:

On the 6th, FTX claimed that was what was slowing their deposits, and why stablecoin balances were only being refilled by Alameda and not by a cold wallet used to store user assets.

But then the balances of ETH began to get low as well:

29/82

As that happened, people began to be concerned about their other balances and to withdraw their spot tokens from the exchange.

Which once again, should have always been 1:1 because users could only lose them if they opted-in to lending.

As that happened, people began to be concerned about their other balances and to withdraw their spot tokens from the exchange.

Which once again, should have always been 1:1 because users could only lose them if they opted-in to lending.

30/82

At this point the exchange began to run low on all it's assets:

Just the day prior Sam had noted that these were "unfounded rumors" from a competitor, trying to ruin them.

At this point the exchange began to run low on all it's assets:

Just the day prior Sam had noted that these were "unfounded rumors" from a competitor, trying to ruin them.

31/82

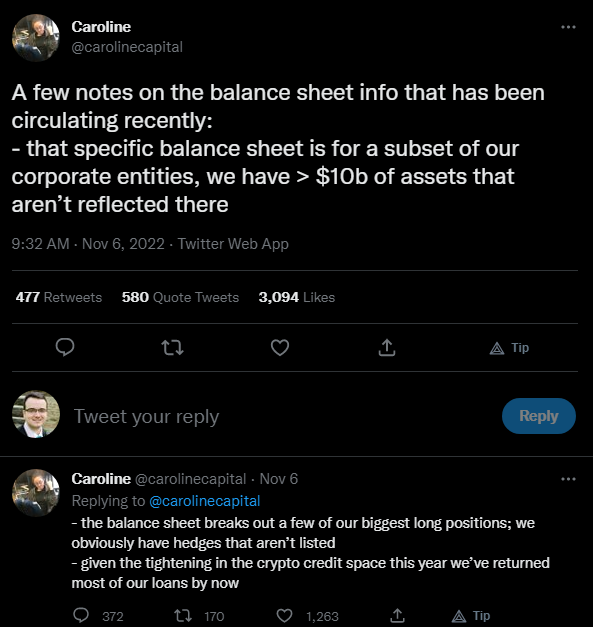

And Caroline had suggested that Alameda had an additional $10B assets not reflected in recent press leaks, bringing the total of Alameda's assets to $24B+

And Caroline had suggested that Alameda had an additional $10B assets not reflected in recent press leaks, bringing the total of Alameda's assets to $24B+

32/82

But as asset balances grew lower on the exchanges hot wallets, and users waited for an unidentified cold wallet to refill the balances - no such refill came.

But as asset balances grew lower on the exchanges hot wallets, and users waited for an unidentified cold wallet to refill the balances - no such refill came.

33/82

I then mapped out every wallet I could find of Alameda and FTX with transaction history going back multiple years

I then mapped out every wallet I could find of Alameda and FTX with transaction history going back multiple years

34/82

In their entire history, assets nearly always came in from Alameda wallets or other exchanges, and never any hidden cold wallet.

There was no legitimate reason for this to be the case.

It was clear now that there was fraud.

In their entire history, assets nearly always came in from Alameda wallets or other exchanges, and never any hidden cold wallet.

There was no legitimate reason for this to be the case.

It was clear now that there was fraud.

35/82

On the night of the 7th, the price of Solana, one of Alameda's other biggest holdings began to drop.

Someone was rapidly selling the Solana token in order to prop up the price of FTT at $22.

But then all at once, the price fell.

On the night of the 7th, the price of Solana, one of Alameda's other biggest holdings began to drop.

Someone was rapidly selling the Solana token in order to prop up the price of FTT at $22.

But then all at once, the price fell.

36/82

The $550M that Alameda claimed to have in order to be able to buyout the remaining Binance FTT had failed to hold the price.

How could a team who claimed to have $24B in assets, and an exchange with $10B+ in supposed user assets not complete their purchase?

The $550M that Alameda claimed to have in order to be able to buyout the remaining Binance FTT had failed to hold the price.

How could a team who claimed to have $24B in assets, and an exchange with $10B+ in supposed user assets not complete their purchase?

37/82

This is where the broader market began to become extremely concerned. It was clear something was wrong - and yet, still none of us realized how bad.

This is where the broader market began to become extremely concerned. It was clear something was wrong - and yet, still none of us realized how bad.

38/82

On an asset per asset basis, sometime on the night of November the 7th, FTX stopped processing withdrawals of many assets.

Users balances were entirely stuck.

On an asset per asset basis, sometime on the night of November the 7th, FTX stopped processing withdrawals of many assets.

Users balances were entirely stuck.

39/82

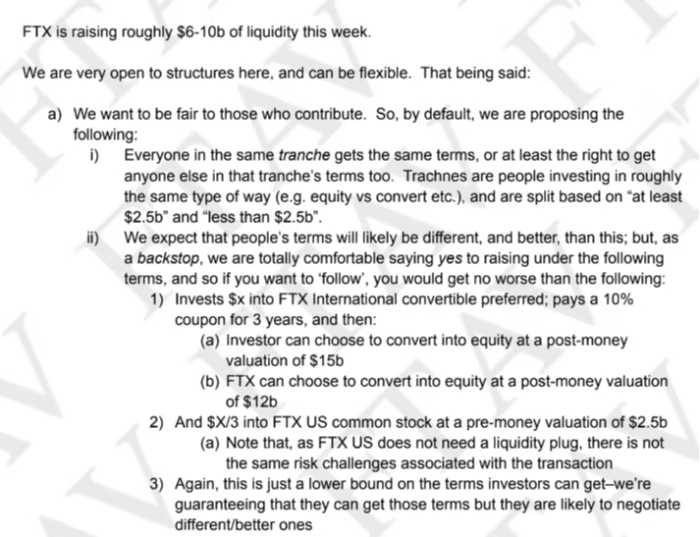

We now know, that at this time, SBF was trying to do an "emergency fundraise" of $6B-$10B with weird frantic terms.

The rumors of this raise began to spiral - but no one really believed the price tag.

We now know, that at this time, SBF was trying to do an "emergency fundraise" of $6B-$10B with weird frantic terms.

The rumors of this raise began to spiral - but no one really believed the price tag.

40/82

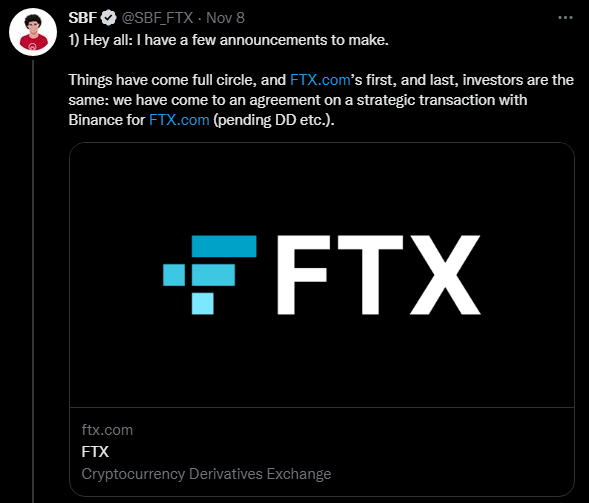

At the time, we thought FTX likely had lost some user funds and would likely fundraise a small amount to cover the balance and move on.

Instead, we awoke to the news that FTX was to be bought out entirely by Binance - subject to due diligence.

At the time, we thought FTX likely had lost some user funds and would likely fundraise a small amount to cover the balance and move on.

Instead, we awoke to the news that FTX was to be bought out entirely by Binance - subject to due diligence.

41/82

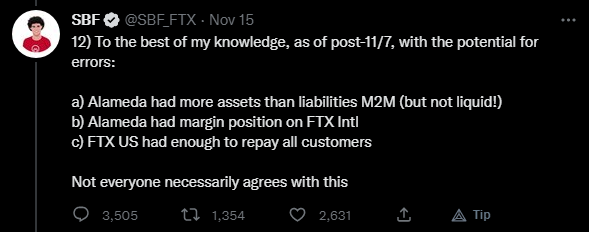

We were in shock.

Just the day prior, both FTX and Sam had claimed the exchange and Alameda to be entirely solvent; and yet there was a full buyout on the table.

It came to light that they did have a hole somewhere between $5b-$10b in missing assets.

We were in shock.

Just the day prior, both FTX and Sam had claimed the exchange and Alameda to be entirely solvent; and yet there was a full buyout on the table.

It came to light that they did have a hole somewhere between $5b-$10b in missing assets.

42/82

After not more than a day, Binance pulled out of the deal, citing too many issues with regulation and the misuse of user funds.

One of the first confirmations that something illegal had been done.

After not more than a day, Binance pulled out of the deal, citing too many issues with regulation and the misuse of user funds.

One of the first confirmations that something illegal had been done.

43/82

Something that both Reuters and TheBlock were able to confirm on November 12th.

That SBF had built a secret 'back door' to lend Alameda user funds without it appearing in the FTX logs.

theblock.co

Something that both Reuters and TheBlock were able to confirm on November 12th.

That SBF had built a secret 'back door' to lend Alameda user funds without it appearing in the FTX logs.

theblock.co

44/82

Meanwhile, during the silence, Alameda continued to make bizarre onchain trades and bets, using funds that they now knew would be clawed back in bankruptcy proceedings.

There was a rare silence from Sam.

Meanwhile, during the silence, Alameda continued to make bizarre onchain trades and bets, using funds that they now knew would be clawed back in bankruptcy proceedings.

There was a rare silence from Sam.

45/82

During this time, Sam spoke to media outlets, letting them know he was "putting together funding" and claimed commitments from sources like Tether.

Which Tether, and all other entities denied instantly, while Sam continued to lie.

During this time, Sam spoke to media outlets, letting them know he was "putting together funding" and claimed commitments from sources like Tether.

Which Tether, and all other entities denied instantly, while Sam continued to lie.

46/82

Alameda's trading efforts only came to an end after Tether was required to freeze Alameda and FTX's balances at the request of law enforcement agencies

Alameda's trading efforts only came to an end after Tether was required to freeze Alameda and FTX's balances at the request of law enforcement agencies

47/82

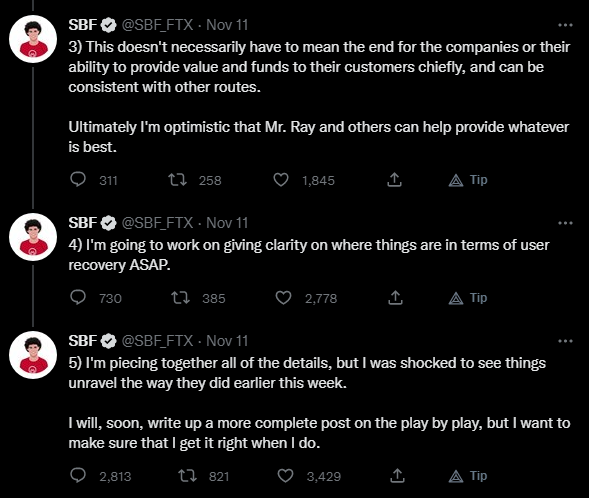

On the morning of the 11th, Sam then resurfaced, suddenly putting FTX and Alameda into Chapter 11 bankruptcy and stepping down as CEO.

Something that we now know took an extensive internal fight to achieve.

On the morning of the 11th, Sam then resurfaced, suddenly putting FTX and Alameda into Chapter 11 bankruptcy and stepping down as CEO.

Something that we now know took an extensive internal fight to achieve.

48/82

He claimed this didn't mean the end for Alameda and that he was "shocked" to see this happen - despite the fact that now know he specifically built the lending backdoor.

He claimed this didn't mean the end for Alameda and that he was "shocked" to see this happen - despite the fact that now know he specifically built the lending backdoor.

49/82

SBF claimed he was set to work with the team to help put things right for customers.

But, as confirmed by an insider - after stepping down Sam went and did his own thing leaving others to pick up the mess.

SBF claimed he was set to work with the team to help put things right for customers.

But, as confirmed by an insider - after stepping down Sam went and did his own thing leaving others to pick up the mess.

50/82

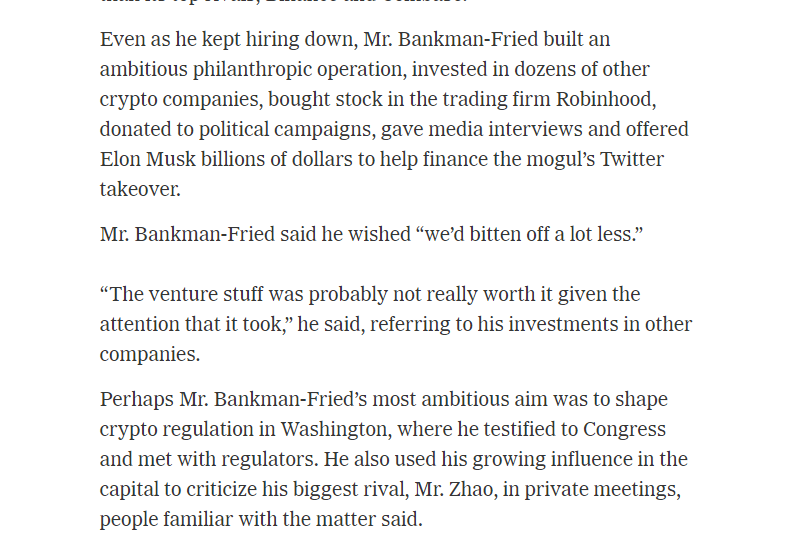

Over the next few days, Sam worked hard to get friendly media pieces written about him. Framing this blow up as "a mistake", that "they grew to big", that he was an "honest and humble" person and that this was the fault of "bad accounting" and a "rival"

Over the next few days, Sam worked hard to get friendly media pieces written about him. Framing this blow up as "a mistake", that "they grew to big", that he was an "honest and humble" person and that this was the fault of "bad accounting" and a "rival"

51/82

The NY Times wrote a piece on him outlining that he had simply "taken on too much" and that the "venture stuff" distracted them.

With no mention that whether distracted or not, they had stolen user funds to achieve their goals.

The NY Times wrote a piece on him outlining that he had simply "taken on too much" and that the "venture stuff" distracted them.

With no mention that whether distracted or not, they had stolen user funds to achieve their goals.

52/82

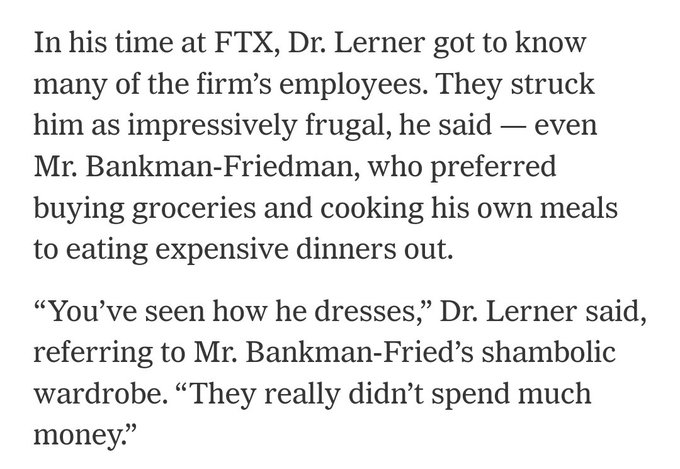

The also interviewed the teams in-house "coach" who talked about how humble and frugal Sam was.

Meanwhile SBF has said in previous posts that he can't really cook, and the team owns mulitple luxury apartments in Albany, a private Bahamas resort.

The also interviewed the teams in-house "coach" who talked about how humble and frugal Sam was.

Meanwhile SBF has said in previous posts that he can't really cook, and the team owns mulitple luxury apartments in Albany, a private Bahamas resort.

53/82

From putting their face on billboards, naming sports teams, buying up $30M luxury condos, building a giant office in the shape of their logo, and hiring 24/7 kitchen staff - the team was anything but frugal.

But that didn't stop this media ground game.

From putting their face on billboards, naming sports teams, buying up $30M luxury condos, building a giant office in the shape of their logo, and hiring 24/7 kitchen staff - the team was anything but frugal.

But that didn't stop this media ground game.

54/82

The goal was clear.

Paint SBF as a good kid, who fumbled a business that was growing too fast, when a rival attacked him.

Rather than a criminal who didn't care about taking risks with users money.

The goal was clear.

Paint SBF as a good kid, who fumbled a business that was growing too fast, when a rival attacked him.

Rather than a criminal who didn't care about taking risks with users money.

55/82

Then, that night, something odd happened at FTX.

The remaining wallets were hacked and user balances on the exchange were set to zero.

An update to the app was pushed containing possible spyware, but never confirmed.

Then, that night, something odd happened at FTX.

The remaining wallets were hacked and user balances on the exchange were set to zero.

An update to the app was pushed containing possible spyware, but never confirmed.

56/82

General Counsel Ryne Miller tweeted confirming that these withdrawals were unauthorized. That someone had walked away with more than $400M in remaining assets. Something you could only do if you had extensive system access at the highest levels.

General Counsel Ryne Miller tweeted confirming that these withdrawals were unauthorized. That someone had walked away with more than $400M in remaining assets. Something you could only do if you had extensive system access at the highest levels.

57/82

To this date (November 16th) FTX has not yet verified who is in possession of these assets or how they obtained access to them.

The hacker continues to access and swap these assets on chain.

To this date (November 16th) FTX has not yet verified who is in possession of these assets or how they obtained access to them.

The hacker continues to access and swap these assets on chain.

58/82

Then, things went quiet.

It wasn't until November 13th that we had real updates again.

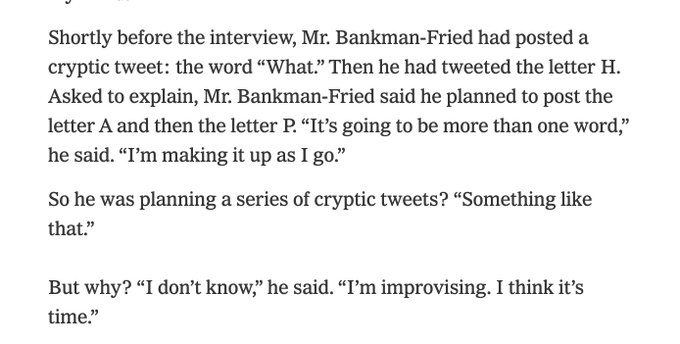

This time from SBF, simply tweeting "what"

Then, things went quiet.

It wasn't until November 13th that we had real updates again.

This time from SBF, simply tweeting "what"

59/82

Over the next 48 hours, he simply tweeted out letter by letter the word "happened" playing a game with followers - showing the lack of care and remorse for his actions.

Something that he admitted in an interview was just him improvising.

Over the next 48 hours, he simply tweeted out letter by letter the word "happened" playing a game with followers - showing the lack of care and remorse for his actions.

Something that he admitted in an interview was just him improvising.

60/82

After signifgant backlash from users and former teammates, he stopped this game and began what could only be described as a written apology tour.

First making the claim that everything was solvent as of November 7th.

After signifgant backlash from users and former teammates, he stopped this game and began what could only be described as a written apology tour.

First making the claim that everything was solvent as of November 7th.

61/82

This meant simply that he was claiming that the $10B hole was created between November 7th and the point of bankruptcy.

But unlike centralized exchanges, blockchains keep incredible records that allow us to go back and validate this.

This meant simply that he was claiming that the $10B hole was created between November 7th and the point of bankruptcy.

But unlike centralized exchanges, blockchains keep incredible records that allow us to go back and validate this.

62/82

The data in fact shows how much FTX held prior to the 'bank run' they claim - and it was insufficient amounts to cover user deposits.

The data in fact shows how much FTX held prior to the 'bank run' they claim - and it was insufficient amounts to cover user deposits.

63/82

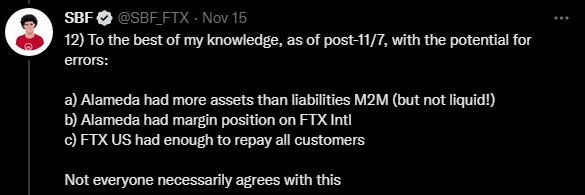

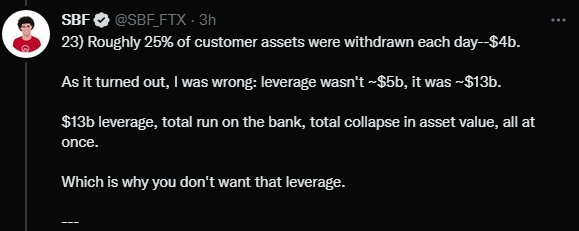

Sam then claims that the system simply took on too much leverage.

Around $13B - but that it was only reported as $5B in internal systems, and so this resulted in the exchange tumbling during the bankrun.

Sam then claims that the system simply took on too much leverage.

Around $13B - but that it was only reported as $5B in internal systems, and so this resulted in the exchange tumbling during the bankrun.

64/82

But, exchanges have coded rules in place.

Debt requires you to place collateral to take on leverage, and that leverage maxes out at 20x.

The debt also comes from somewhere, in the case of FTX it comes from their lending market, or Alameda backstopping.

But, exchanges have coded rules in place.

Debt requires you to place collateral to take on leverage, and that leverage maxes out at 20x.

The debt also comes from somewhere, in the case of FTX it comes from their lending market, or Alameda backstopping.

65/82

However, once again the FTX market had only $2.8B in lending taking place.

And with $3B in assets in the exchange, to be left with a $10B hole, Alameda would need to be borrowing $7B in USD.

However, once again the FTX market had only $2.8B in lending taking place.

And with $3B in assets in the exchange, to be left with a $10B hole, Alameda would need to be borrowing $7B in USD.

66/82

That $7B would also need around $1.4B in collateral to be borrowed against.

If that was the case, that also means that there was less than $1.5B in user assets in the exchange, despite them owing more than $10B in assets to users.

That $7B would also need around $1.4B in collateral to be borrowed against.

If that was the case, that also means that there was less than $1.5B in user assets in the exchange, despite them owing more than $10B in assets to users.

67/82

These numbers simply didn't add up.

But Sam continued to tweet that he was in it for his customers.

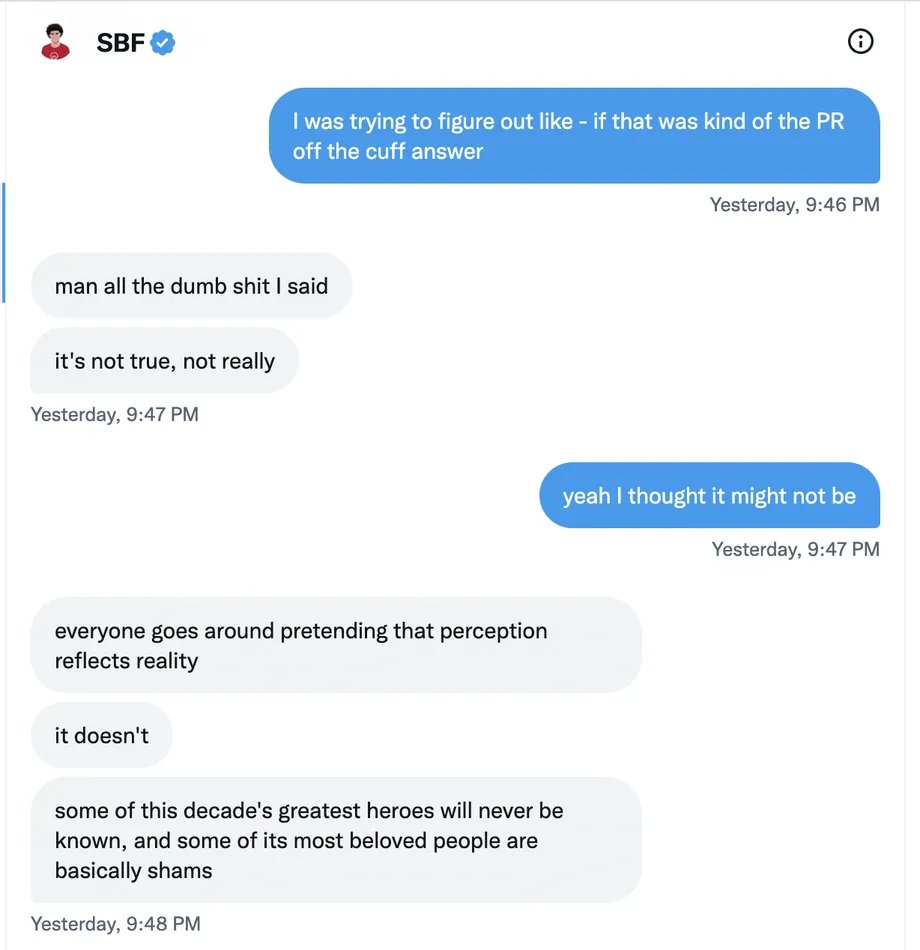

All the while giving an interview to Vox via message, saying that all his "ethics" and "altruism" was really just PR.

These numbers simply didn't add up.

But Sam continued to tweet that he was in it for his customers.

All the while giving an interview to Vox via message, saying that all his "ethics" and "altruism" was really just PR.

68/82

He also, in that same interview blatantly admits that he stole user funds, lending them to Alameda because "sometimes life creeps on you" - despite this being theft. He doesn't care.

He also, in that same interview blatantly admits that he stole user funds, lending them to Alameda because "sometimes life creeps on you" - despite this being theft. He doesn't care.

69/82

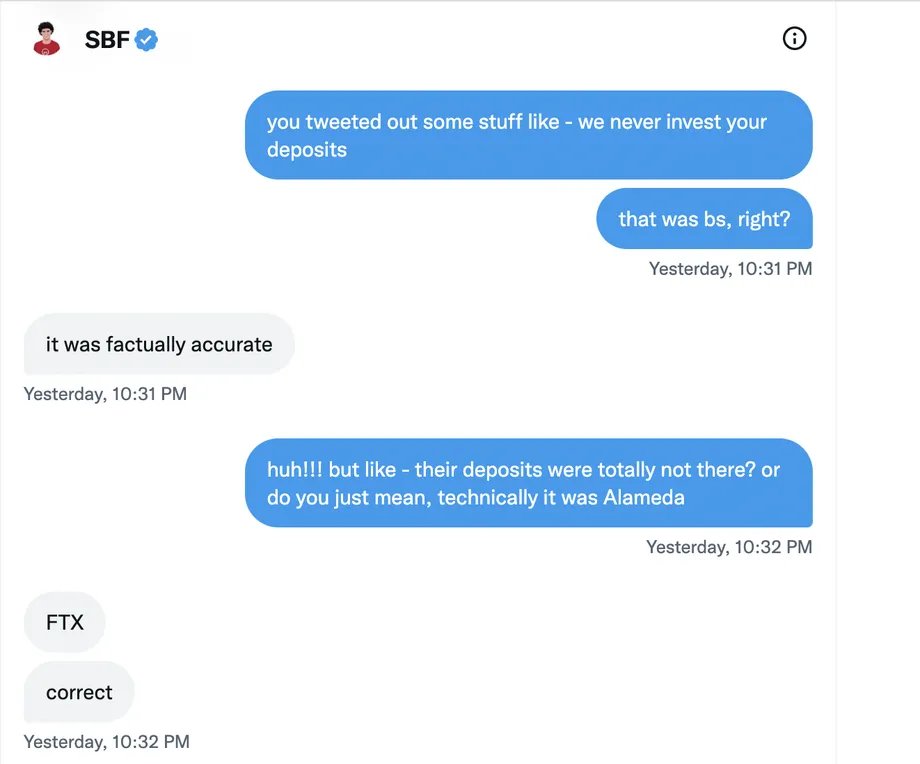

And he said it was "factually correct" when he said FTX doesn't invest your assets...because it was Alameda doing the investing.

And he said it was "factually correct" when he said FTX doesn't invest your assets...because it was Alameda doing the investing.

70/82

In his view, even though it was theft, and a violation of their own terms of service it was fine because "others do it" and he continues to claim that it was just "messy accounting" despite colleagues confirming he expressly programmed a backdoor.

In his view, even though it was theft, and a violation of their own terms of service it was fine because "others do it" and he continues to claim that it was just "messy accounting" despite colleagues confirming he expressly programmed a backdoor.

71/82

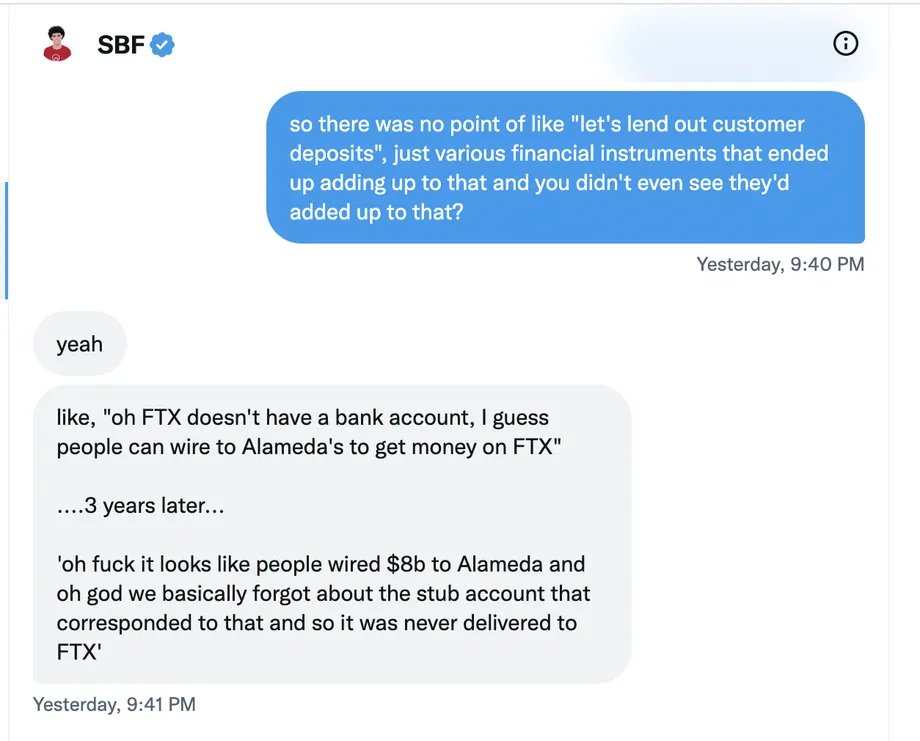

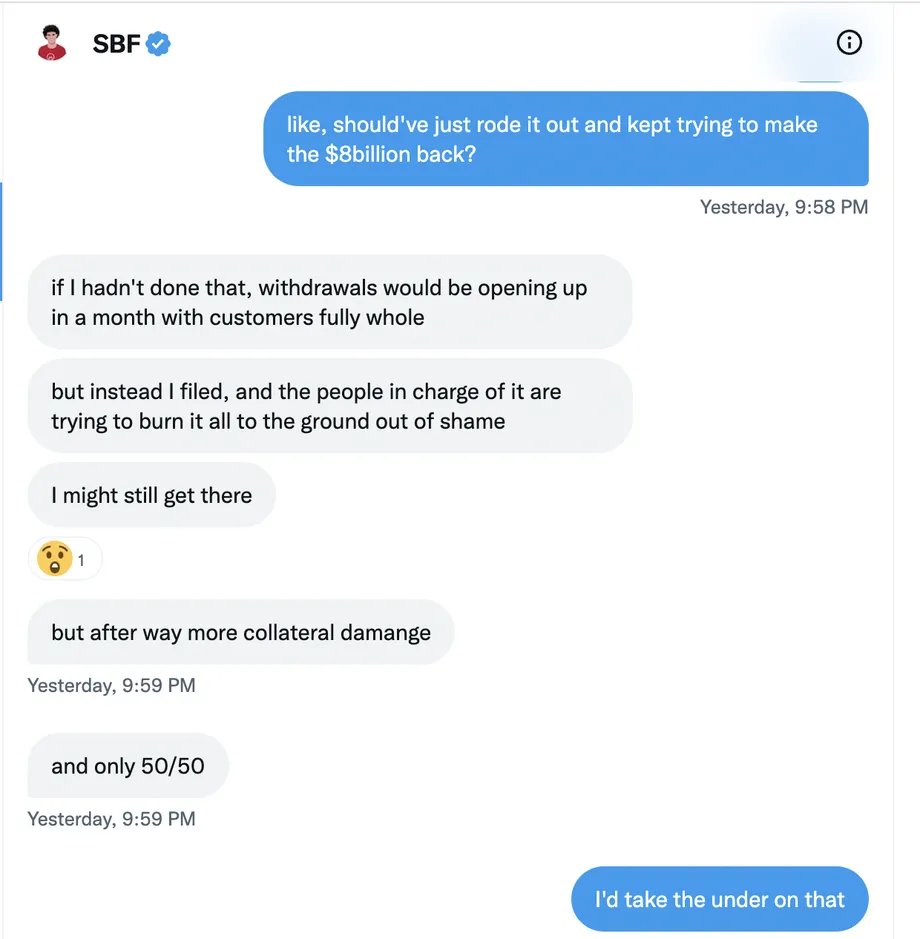

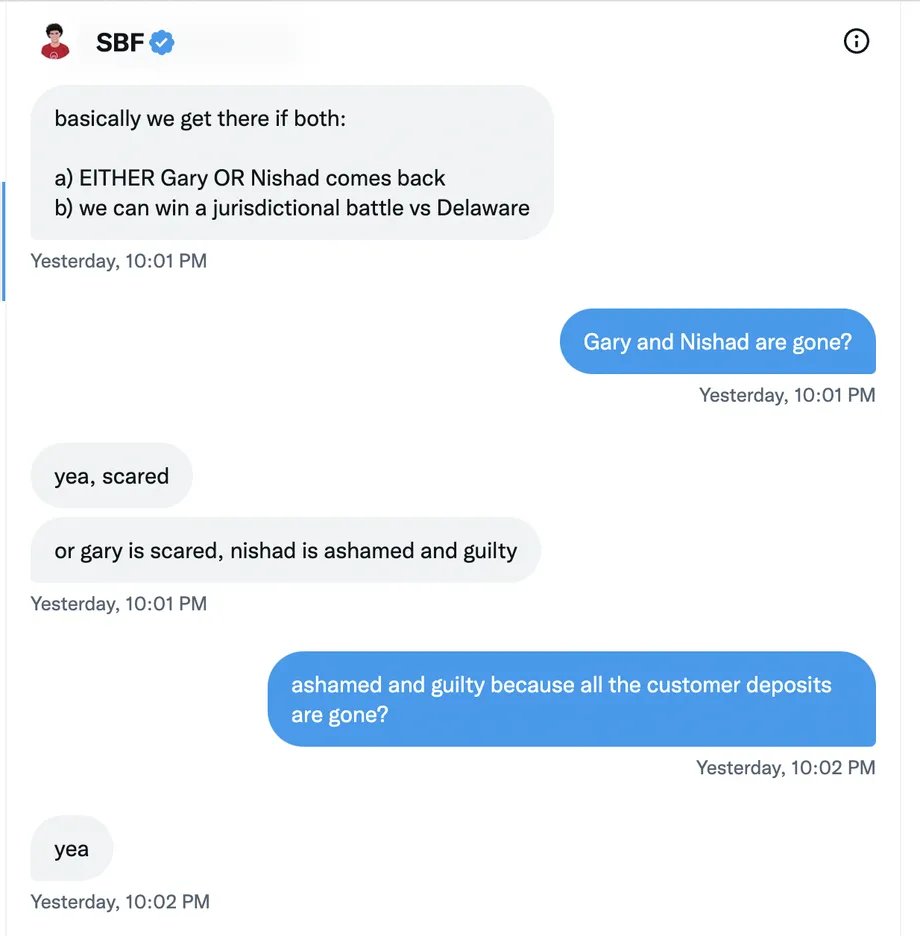

Sam continues to think that he will raise $8B to restore user deposits, and says that its the fault of the other founders being "ashamed" and "scared" that they've sided with the bankruptcy process.

Sam continues to think that he will raise $8B to restore user deposits, and says that its the fault of the other founders being "ashamed" and "scared" that they've sided with the bankruptcy process.

72/82

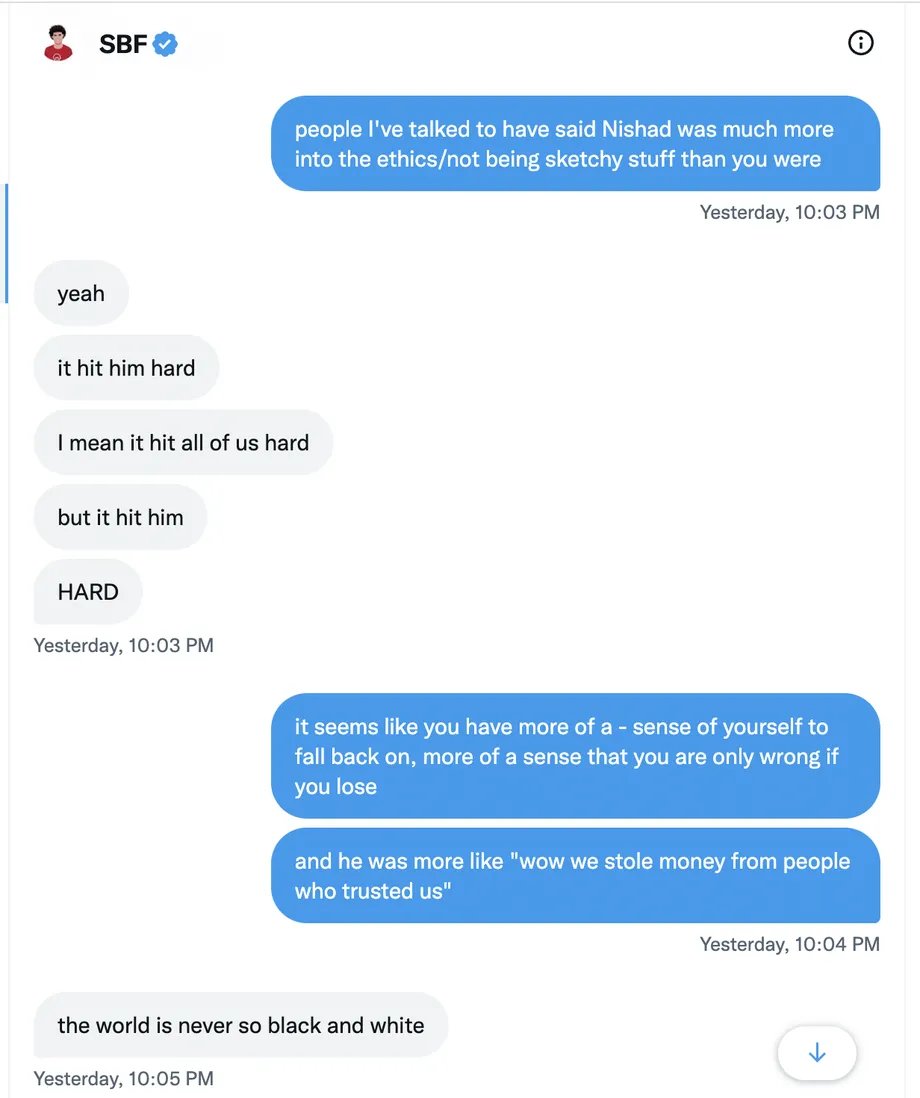

When confronted about why Nishad left, SBF specifically says it was because of ethics and Nishad feeling bad for stealing money.

Where as SBF says "the world is never so black and white"

When confronted about why Nishad left, SBF specifically says it was because of ethics and Nishad feeling bad for stealing money.

Where as SBF says "the world is never so black and white"

73/82

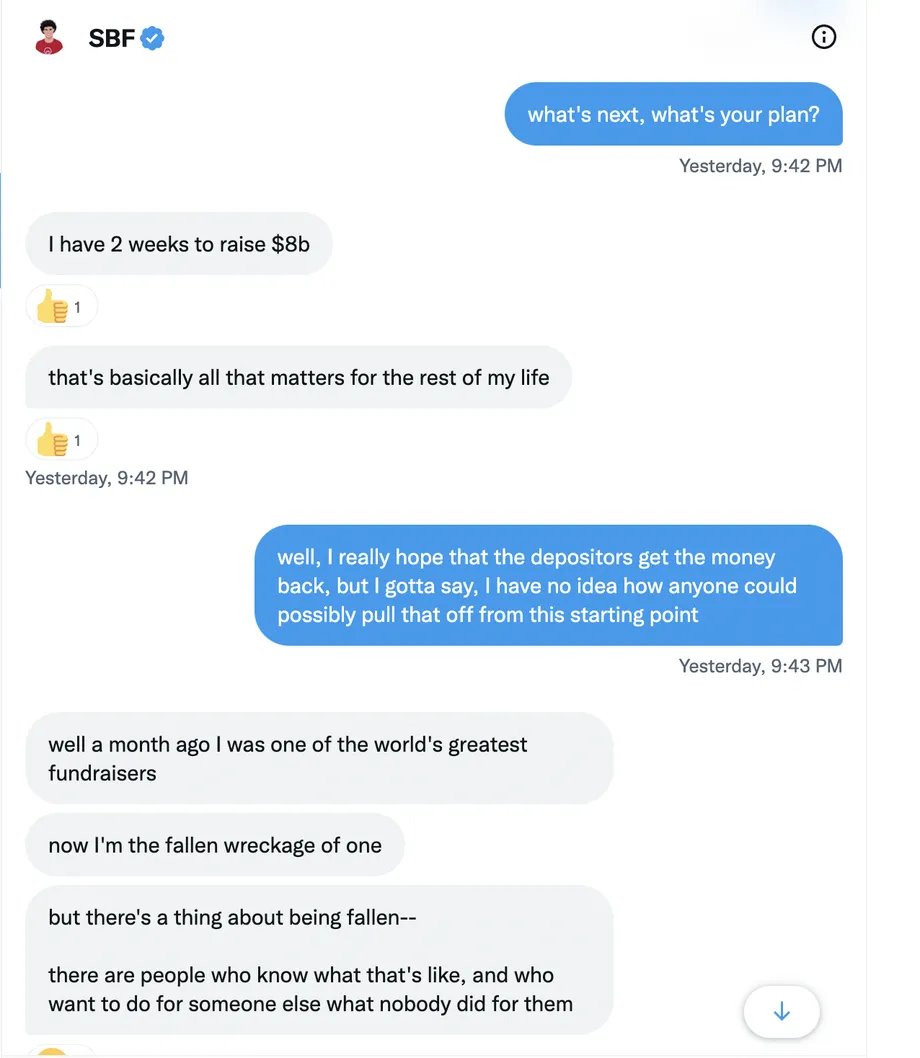

And despite all this, of stealing user funds, of blaming other founders, of coding a backdoor, of not caring about the ethics of it all, he still thinks he can raise $8B+ in two weeks, because "he was one of the world's greatest fundraisers"

And despite all this, of stealing user funds, of blaming other founders, of coding a backdoor, of not caring about the ethics of it all, he still thinks he can raise $8B+ in two weeks, because "he was one of the world's greatest fundraisers"

74/82

He doesn't care about users.

He flat out said, it isn't so black or white.

He doesn't care that he stole funds from people who trusted him.

He doesn't even care that he stole.

He doesn't care about users.

He flat out said, it isn't so black or white.

He doesn't care that he stole funds from people who trusted him.

He doesn't even care that he stole.

75/82

To him, this is some sort of perverse maximalist utilitarianism, where his actions are justified by the fact he was gambling big, and that others do similar things.

He'll just tell you out loud he stole.

To him, this is some sort of perverse maximalist utilitarianism, where his actions are justified by the fact he was gambling big, and that others do similar things.

He'll just tell you out loud he stole.

76/82

Meanwhile hundreds of people are hard at work, trying to guide the company through Chapter 11 and get as many dollars for the estate as possible to pay back creditors.

In the eyes of SBF, he blames his other founders.

It's their fault for caring.

Meanwhile hundreds of people are hard at work, trying to guide the company through Chapter 11 and get as many dollars for the estate as possible to pay back creditors.

In the eyes of SBF, he blames his other founders.

It's their fault for caring.

77/82

Meanwhile, he is focused on a media apology tour, to keep a clean enough brand to raise $8B.

Not for you.

For him.

So he can do it all again - and not go to jail.

Meanwhile, he is focused on a media apology tour, to keep a clean enough brand to raise $8B.

Not for you.

For him.

So he can do it all again - and not go to jail.

78/82

He lied to all of us, to our faces, right up until the bitter end of the exchange.

He tweeted lies and platitudes, and continued to change his story.

He slings arrows at "rivals" and cofounders, blaming them for his down fall.

He lied to all of us, to our faces, right up until the bitter end of the exchange.

He tweeted lies and platitudes, and continued to change his story.

He slings arrows at "rivals" and cofounders, blaming them for his down fall.

79/82

And I'm sure he will seek to discredit his critics, and continue to build a pristine image of himself along with the media to continue on the delusional quest of raising $8B.

We can't believe a single thing that he says at this point.

And I'm sure he will seek to discredit his critics, and continue to build a pristine image of himself along with the media to continue on the delusional quest of raising $8B.

We can't believe a single thing that he says at this point.

80/82

The scope of this illusion and fraud make the works of P. T. Barnum seem like an honest and ethical broker.

While I'm sure this story isn't over in its unraveling, I hope its over for him.

The scope of this illusion and fraud make the works of P. T. Barnum seem like an honest and ethical broker.

While I'm sure this story isn't over in its unraveling, I hope its over for him.

81/82

This is a man who lied to us, viewed it all as a game, thought of us as pieces on the chessboard, and continues to play the game, thinking he is above the ethics and the law.

This is a man who lied to us, viewed it all as a game, thought of us as pieces on the chessboard, and continues to play the game, thinking he is above the ethics and the law.

82/82

Make no mistake. This wasn't the actions of a caring altruist who messed up.

This was theft and fraud - with a bankruptcy that will scar this sector for a generation to come.

Decentralization and transparency matters.

That's what this industry is fighting for.

Make no mistake. This wasn't the actions of a caring altruist who messed up.

This was theft and fraud - with a bankruptcy that will scar this sector for a generation to come.

Decentralization and transparency matters.

That's what this industry is fighting for.

Loading suggestions...