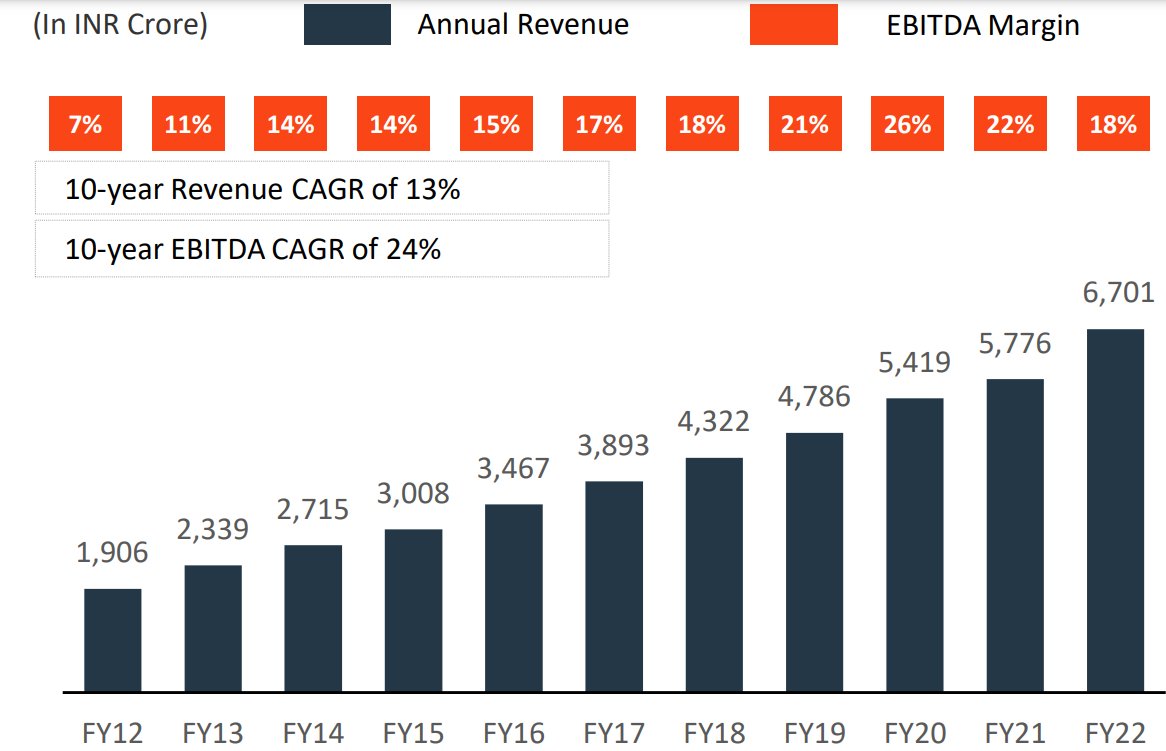

The business has 4 segments and will try to value each segment.

First is CDMO segment

Have sites across North America, Europe and India (2/17)

First is CDMO segment

Have sites across North America, Europe and India (2/17)

They offer integrated service (from discovery to commercial) in CDMO space across different areas of High Potent API, Complex OSDs, Potent Sterile Injectables, Peptides (via 100% subsidiary Hemmo Pharmaceuticals), Antibody Drug Conjugates etc.

(3/17)

(3/17)

33% stake in “Yapan Bio” gives access to Vaccines and Biologics space as well.

Facilities in developed market (unlike syngene or suven) and expertise across complex areas make Piramal CDMO in a unique place.

(4/17)

Facilities in developed market (unlike syngene or suven) and expertise across complex areas make Piramal CDMO in a unique place.

(4/17)

The margin of the business is currently impacted due to inflationary pressure in input cost.

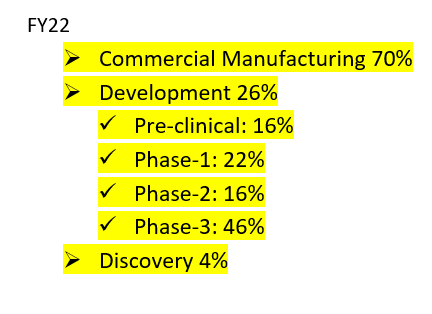

Let’s try to look at the growth areas.

34 molecules (vs 10 in FY17) are in phase-3 and given the track record a significant portion may become commercial in next 3-5 years.

(5/17)

Let’s try to look at the growth areas.

34 molecules (vs 10 in FY17) are in phase-3 and given the track record a significant portion may become commercial in next 3-5 years.

(5/17)

Management is also expecting demand and Rs 1250cr capex is announced across facilities.

This segment may become a 7000 cr business with 20% margin in next 5 years. Margin will be lower compared to Syngene (30%) as they have facilities outside India also.

(6/17)

This segment may become a 7000 cr business with 20% margin in next 5 years. Margin will be lower compared to Syngene (30%) as they have facilities outside India also.

(6/17)

Syngene trades at a price to sales of 8x (Overvalued though I love the business).

Considering P/S of 2.5 Piramal Pharma CDMO should be valued at 17.5k cr after 5 years.

(7/17)

Considering P/S of 2.5 Piramal Pharma CDMO should be valued at 17.5k cr after 5 years.

(7/17)

Second is Complex Hospital Generics.

Has 4 subsegments.

1. Inhalation Anaesthesia:

Largest Market Share in US for Sevoflurane and Isoflurane.

Vertically integrated with fluorochemicals (via 100% subsidiary Convergence Chemicals, 49% used to be owned by Navin Fluorine)

(8/17)

Has 4 subsegments.

1. Inhalation Anaesthesia:

Largest Market Share in US for Sevoflurane and Isoflurane.

Vertically integrated with fluorochemicals (via 100% subsidiary Convergence Chemicals, 49% used to be owned by Navin Fluorine)

(8/17)

4th largest global manufacturer.

2.Injectable Anaesthesia and pain management:

Portfolio: Fentanyl, Sufentanil, Alfentanil, Piritramide, Etomidate.

Marketed in 50+ countries (ex-US)

(9/17)

2.Injectable Anaesthesia and pain management:

Portfolio: Fentanyl, Sufentanil, Alfentanil, Piritramide, Etomidate.

Marketed in 50+ countries (ex-US)

(9/17)

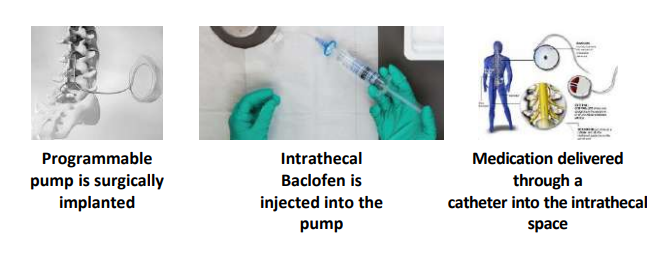

3. Intrathecal Therapy:

This is branded product portfolio and they have

largest market share in the US for Gablofen

(10/17)

This is branded product portfolio and they have

largest market share in the US for Gablofen

(10/17)

4.Other Injectables:

37 SKUs at various stages of development.

Product Portfolio: Ampicillin, Levothyroxine Sodium, Polygeline, Dexmedetomidine, Glycopyrolate, Rocuronium, Miglustat, Succinylcholine, Linezolid and Zinc Sulfate

(11/17)

37 SKUs at various stages of development.

Product Portfolio: Ampicillin, Levothyroxine Sodium, Polygeline, Dexmedetomidine, Glycopyrolate, Rocuronium, Miglustat, Succinylcholine, Linezolid and Zinc Sulfate

(11/17)

This can become a 3000cr business in next 5 years and should be valued at 6000cr (cosnidering 2x P/S)

(12/17)

(12/17)

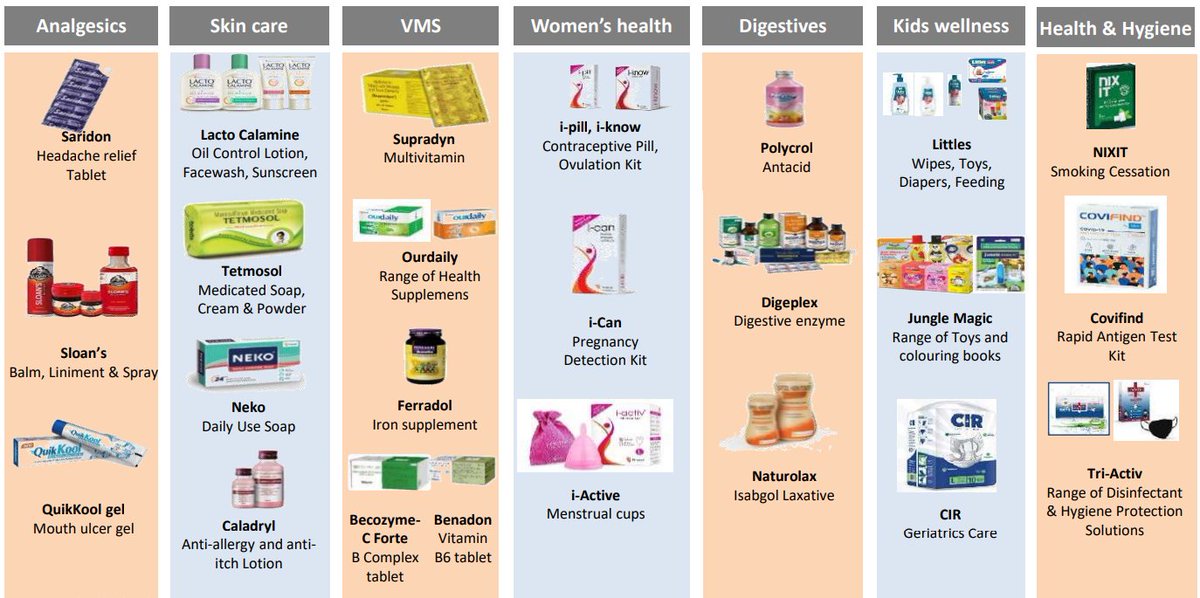

3rd segment India Consumer Healthcare:

This caters to few well know brands like

Lacto Calamine, Littles, Tetmosol, Polycrol, I-Pill etc.

This segment is currently EBITDA neutral as management is investing 15% topline in marketing.

(13/17)

This caters to few well know brands like

Lacto Calamine, Littles, Tetmosol, Polycrol, I-Pill etc.

This segment is currently EBITDA neutral as management is investing 15% topline in marketing.

(13/17)

Expecting this segment to grow fastest.

This can be a 1500cr business in 5 years. Should be valued at 3000cr considering 2x P/S.

(14/17)

This can be a 1500cr business in 5 years. Should be valued at 3000cr considering 2x P/S.

(14/17)

4th is Allergan India Pvt Limited.

It is a JV.

PPL has 49% stake and rest 51% held by Abbvie.

Leader in the eye care segment in India

#1 in Glaucoma (23% market share)

#1 in Tears segment (21% market share)

(15/17)

It is a JV.

PPL has 49% stake and rest 51% held by Abbvie.

Leader in the eye care segment in India

#1 in Glaucoma (23% market share)

#1 in Tears segment (21% market share)

(15/17)

This can be a 700cr business in 5years, this is the most profitable segment and should be valued at 2500cr.

Piramal stake would be 1250cr.

(16/17)

Piramal stake would be 1250cr.

(16/17)

Total valuation after 5 years.

CDMO: 17.5k cr

CHG: 6k cr

ICH: 3k cr

Allergan: 1.25k cr

Total: 27.75k cr, Market cap: 16k cr

This implies 11.6% CAGR over next 5 years.

Note: Valuations are carried out being very very very conservative.

(17/17)

CDMO: 17.5k cr

CHG: 6k cr

ICH: 3k cr

Allergan: 1.25k cr

Total: 27.75k cr, Market cap: 16k cr

This implies 11.6% CAGR over next 5 years.

Note: Valuations are carried out being very very very conservative.

(17/17)

Loading suggestions...