@drjimmy2407 1. DNL is an import substitution play. Initially when I studied and made the video on this in 2020, Phenol spreads were low. Phenol spreads shooting up led to the outsized impact.

2. 1500 crore capex- out of which 700-1100 crore is for solvents like MIBK and MIBC

2. 1500 crore capex- out of which 700-1100 crore is for solvents like MIBK and MIBC

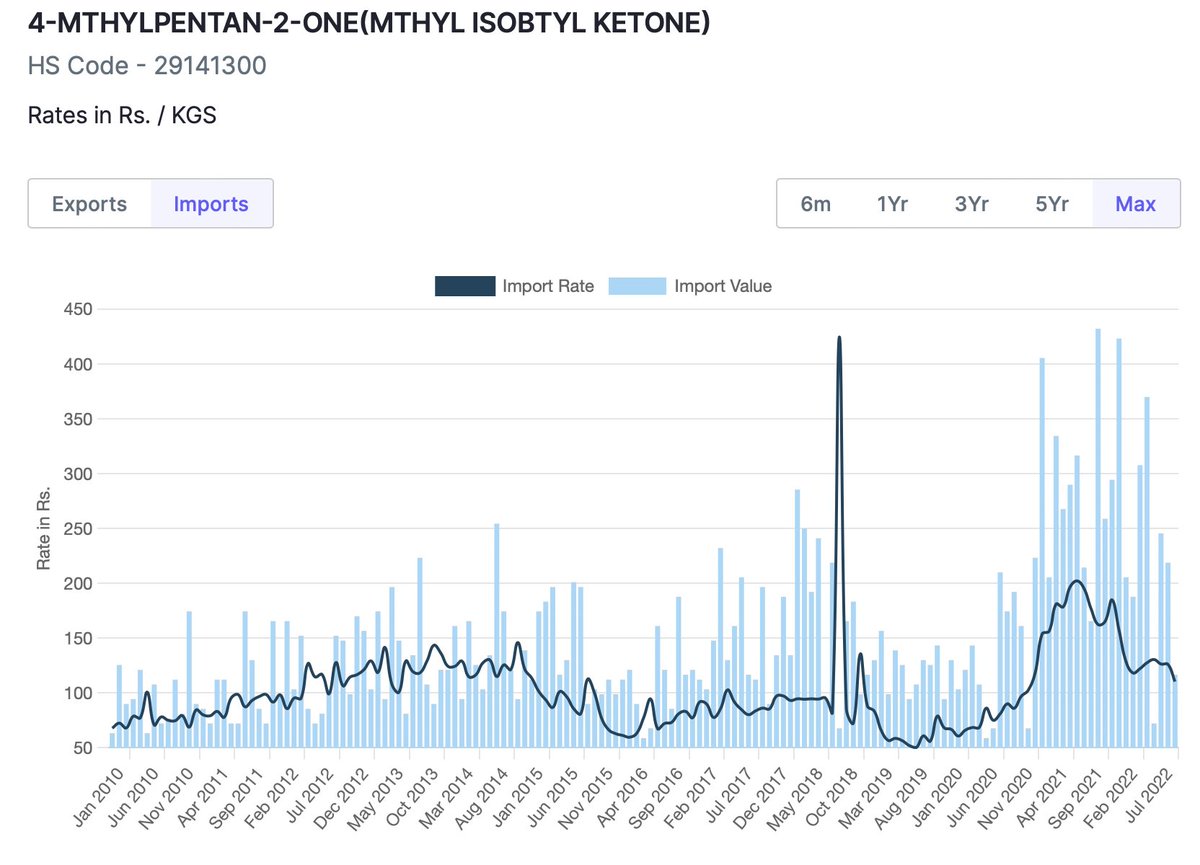

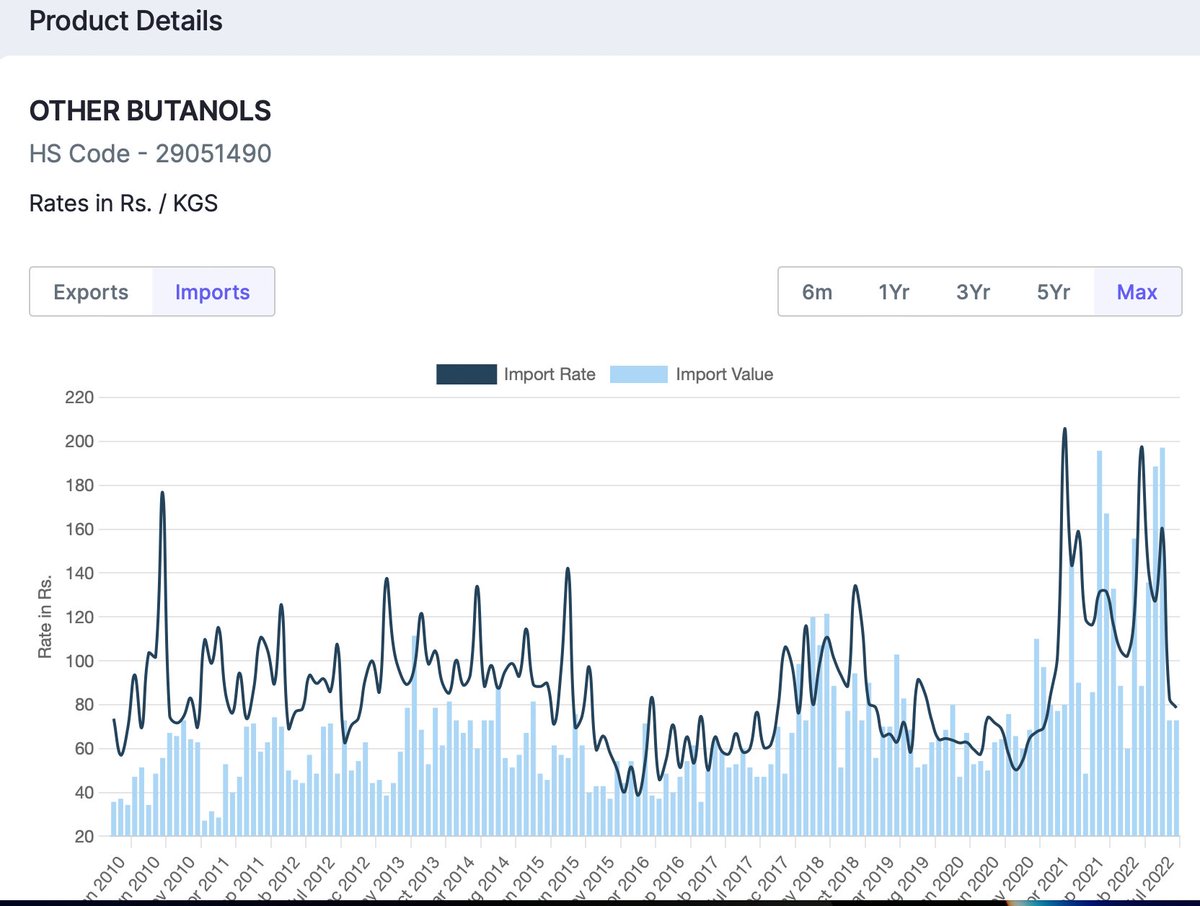

@drjimmy2407 This is the pricing of the downstream solvents of phenol

Again volatile (but margins might be 100-150 bps better)

Again volatile (but margins might be 100-150 bps better)

@drjimmy2407 Long run:-

1. Downstream phenol addition like- Polycarbonate (Bisphenol), and other solvents.

2. Base business being doubled with margins improving

3. More capacity for phenol (if polycarbonate plant is announced, my sense is they will need one more phenol plant)

1. Downstream phenol addition like- Polycarbonate (Bisphenol), and other solvents.

2. Base business being doubled with margins improving

3. More capacity for phenol (if polycarbonate plant is announced, my sense is they will need one more phenol plant)

@drjimmy2407 Just my sense on point 3.

Has to be the thesis,

However margins and spreads will be volatile as they are a price taker and not maker as covered in anti thesis here:-

youtube.com

Has to be the thesis,

However margins and spreads will be volatile as they are a price taker and not maker as covered in anti thesis here:-

youtube.com

@drjimmy2407 Such businesses have their cycle, and an active investor can do well by tracking the cycles closely :)

Long term guys can chill in sideways. Upto your game and what works for you

Long term guys can chill in sideways. Upto your game and what works for you

Loading suggestions...