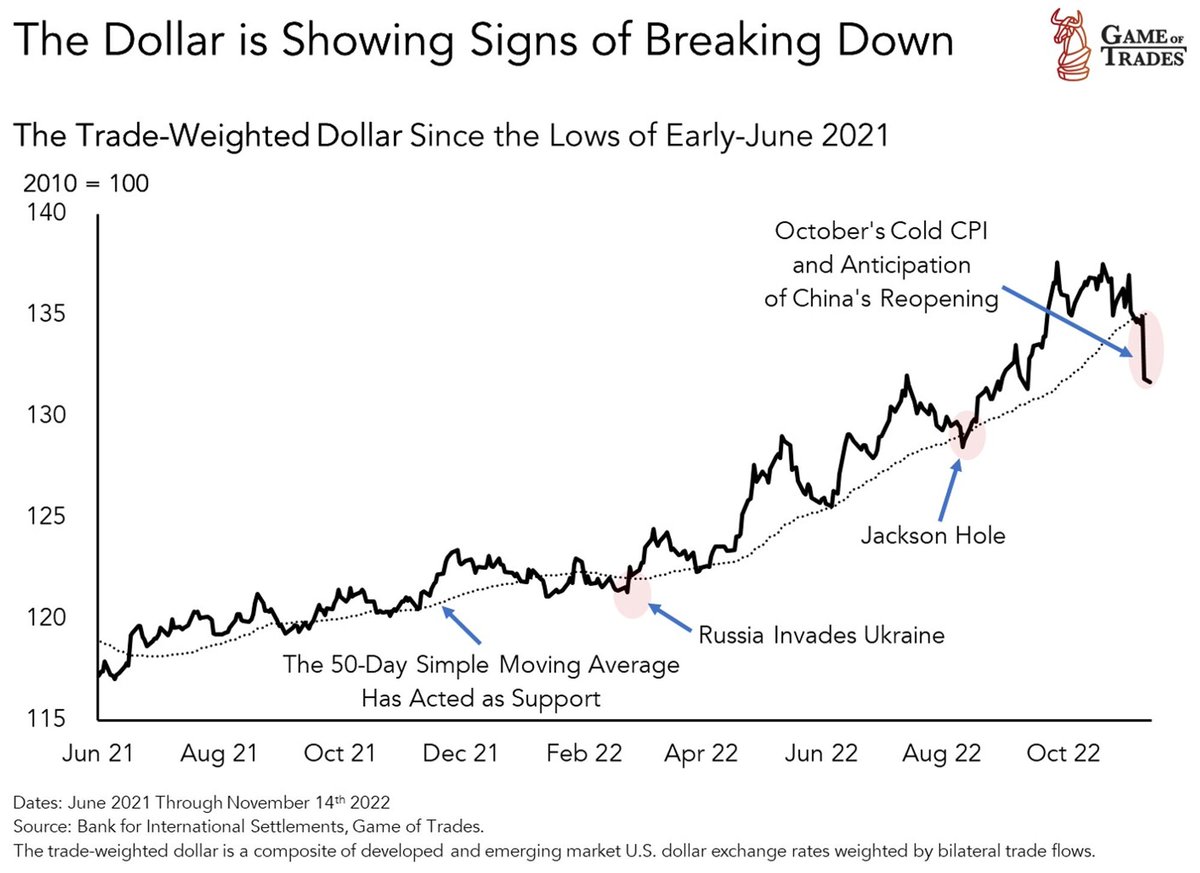

Following a relentless rise since June of 2021, the almighty USD has been struggling recently

Here is our framework for understanding what's been driving the USD and where it's headed

A thread 🧵👇

Here is our framework for understanding what's been driving the USD and where it's headed

A thread 🧵👇

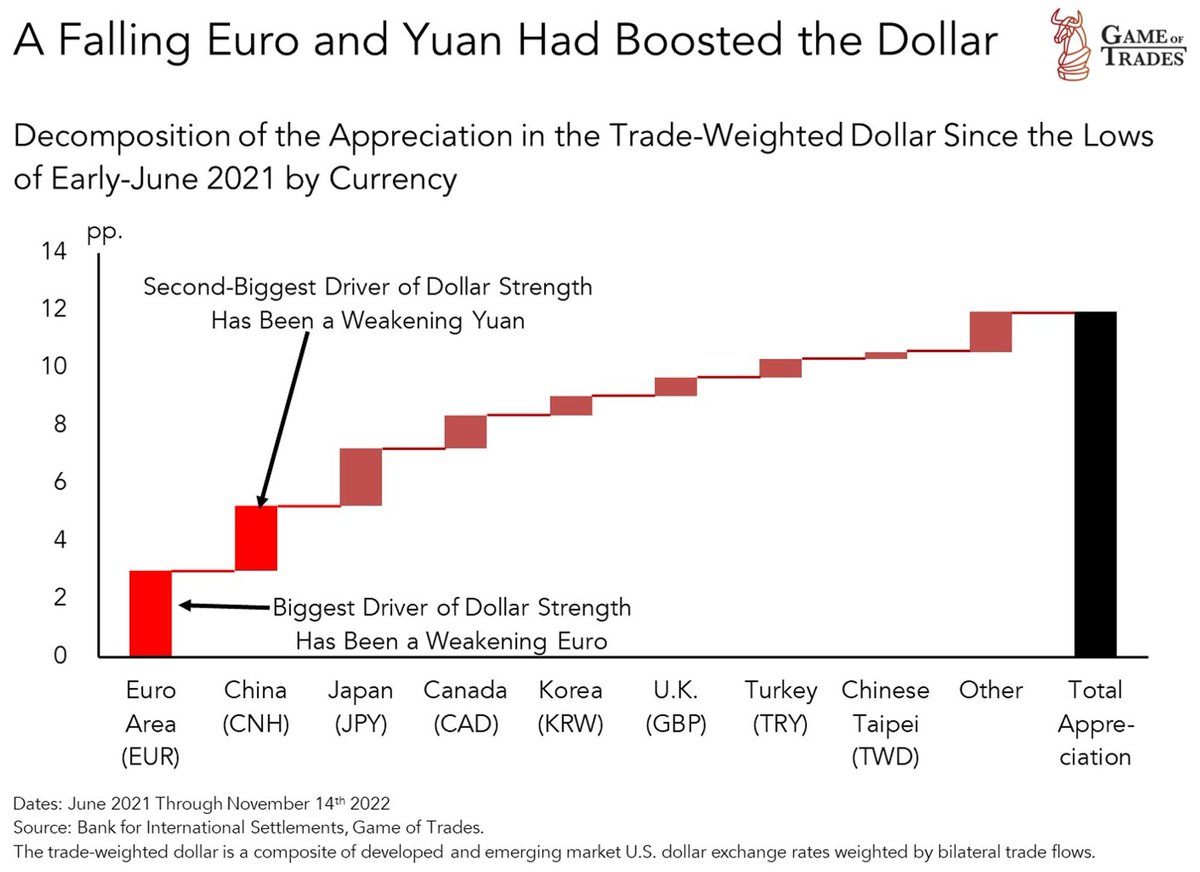

2/ The massive USD upcycle that began in June of last year has been mainly driven by weakness in the euro and the Chinese yuan

3/ Moves in the euro and the yuan make a big impact on the trade-weighted USD, given those economies trade a lot with the US

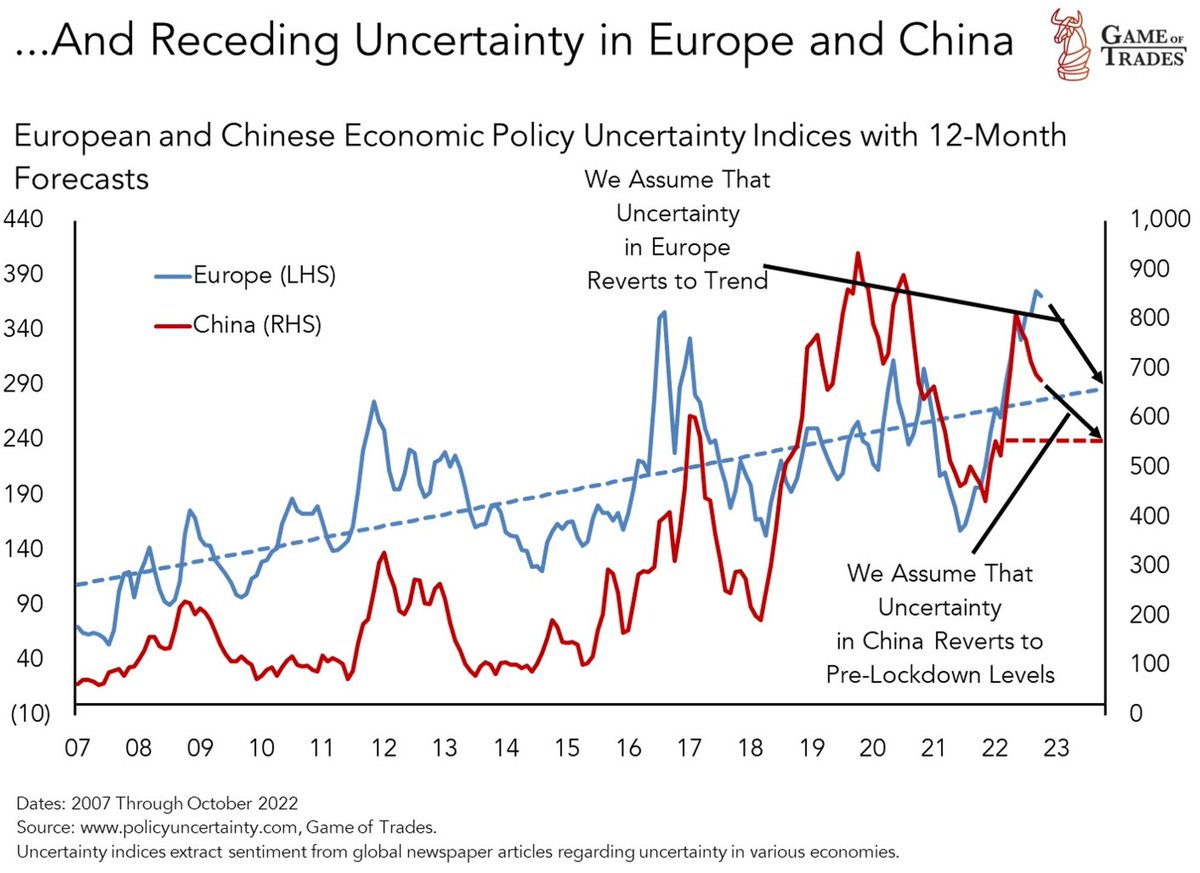

4/ Rising economic uncertainty in Europe resulting from a supply crunch in natural gas following a post-pandemic boom in demand drove the USD higher in early June last year.

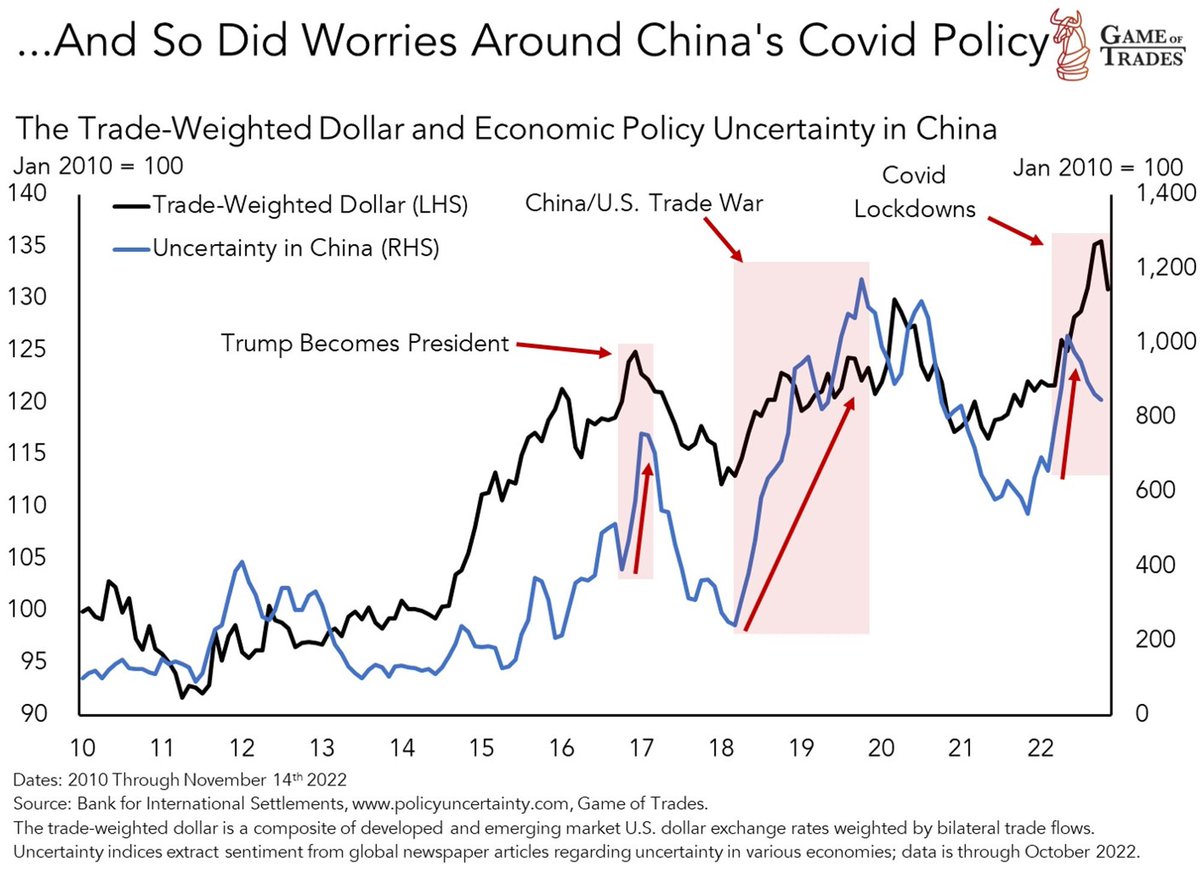

4/ China has been another important story driving the USD's strength this year.

Strict lockdowns in the spring drove economic uncertainty in China, triggering worries of a deep slowdown.

Ensuing weakness in the yuan drove the USD higher.

Strict lockdowns in the spring drove economic uncertainty in China, triggering worries of a deep slowdown.

Ensuing weakness in the yuan drove the USD higher.

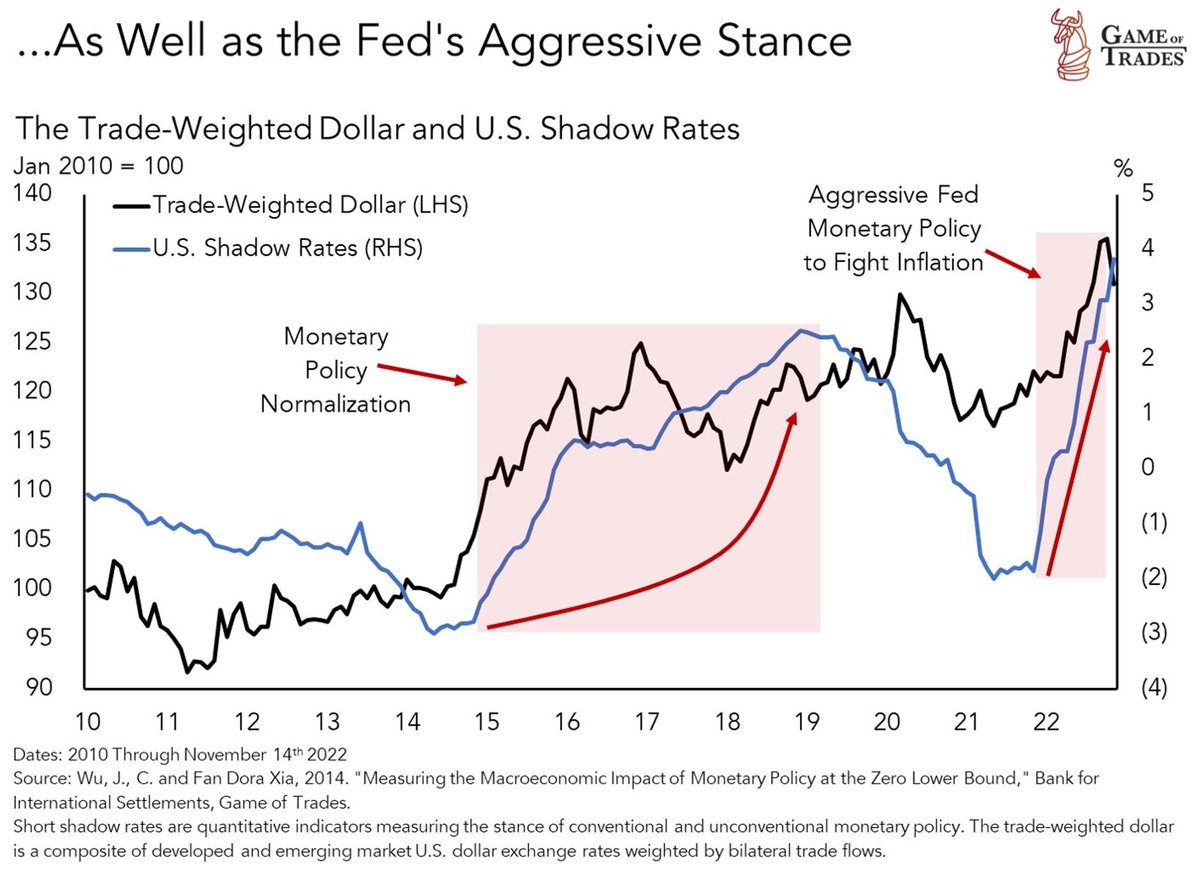

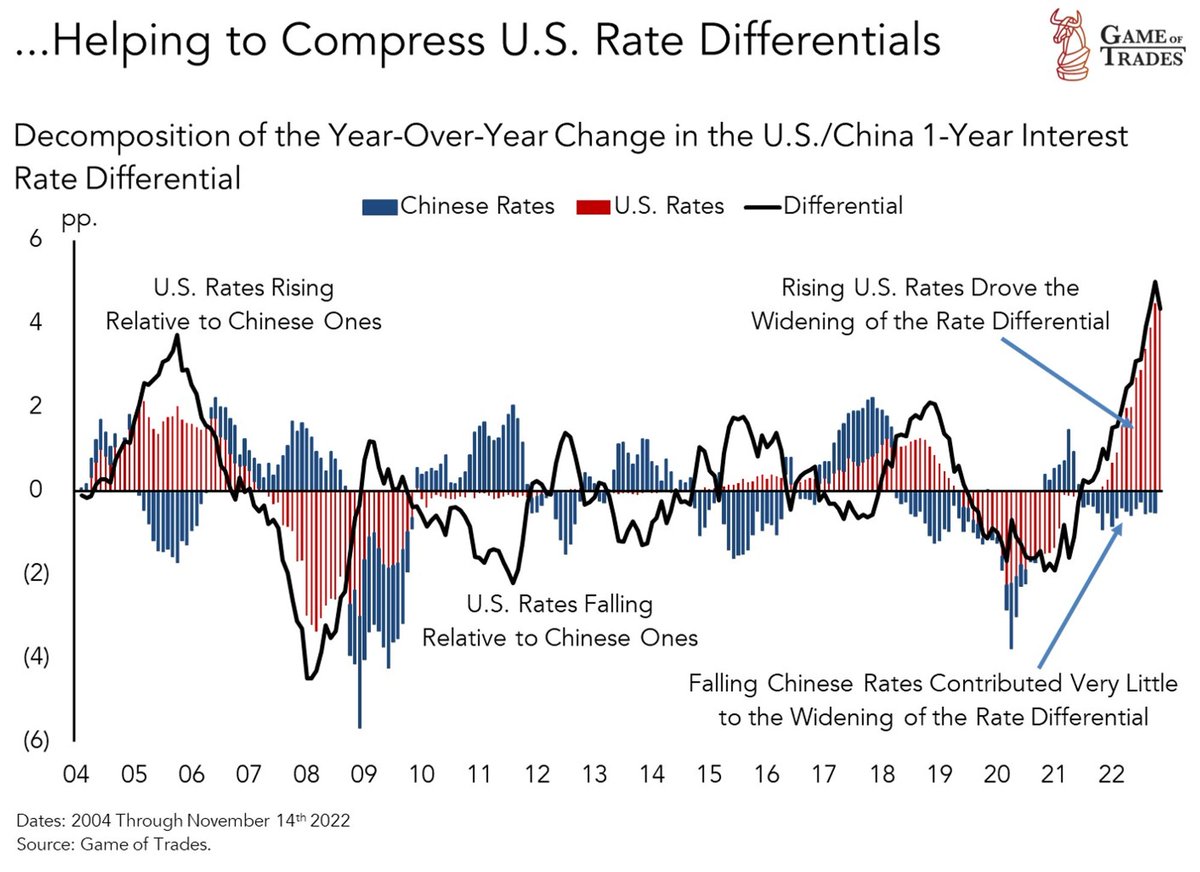

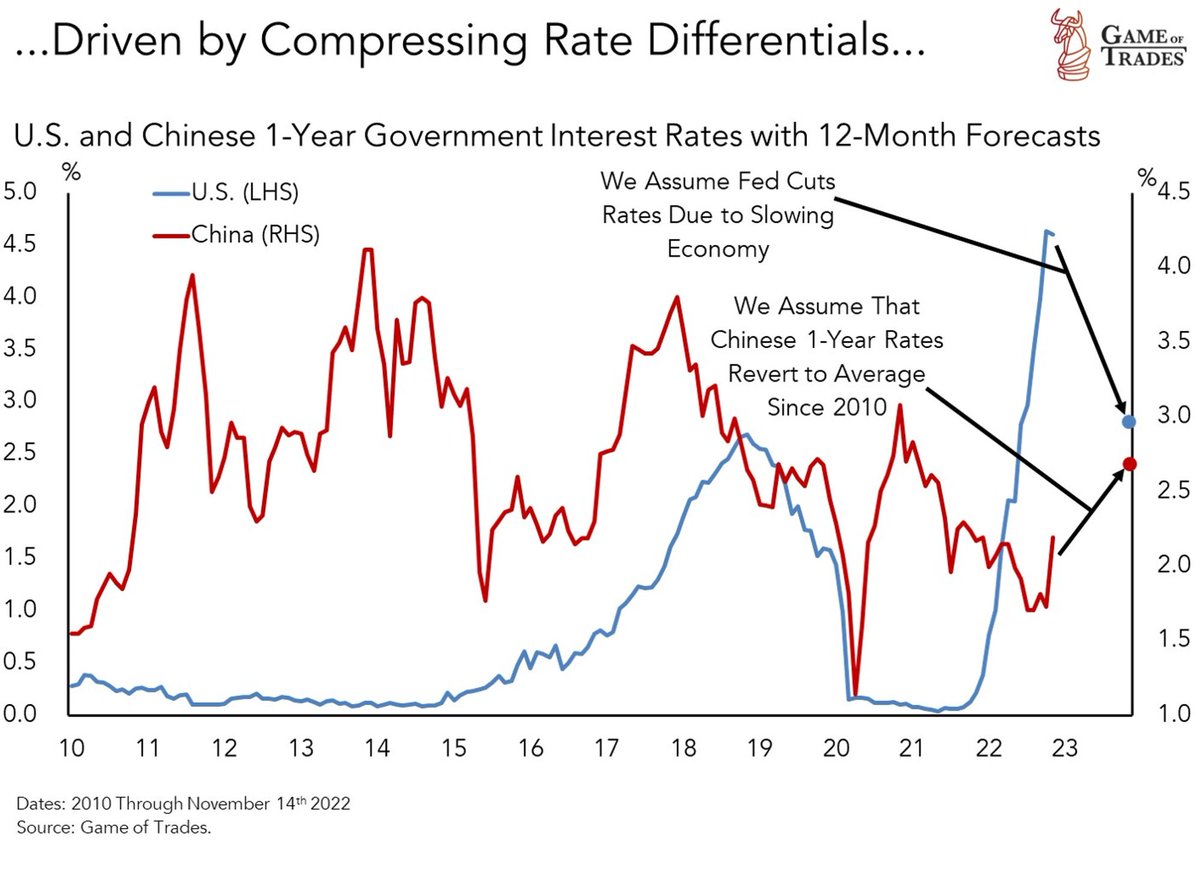

5/ Lastly, the Fed's aggressive stance has also played a large role in driving the USD higher

→ widening interest rate differentials between those in the US and the rest of the world

→ widening interest rate differentials between those in the US and the rest of the world

6/ With an understanding of what's driven the USD higher since June 2021

Let's focus on what's driven the weakness in the USD over the last few weeks.

Let's focus on what's driven the weakness in the USD over the last few weeks.

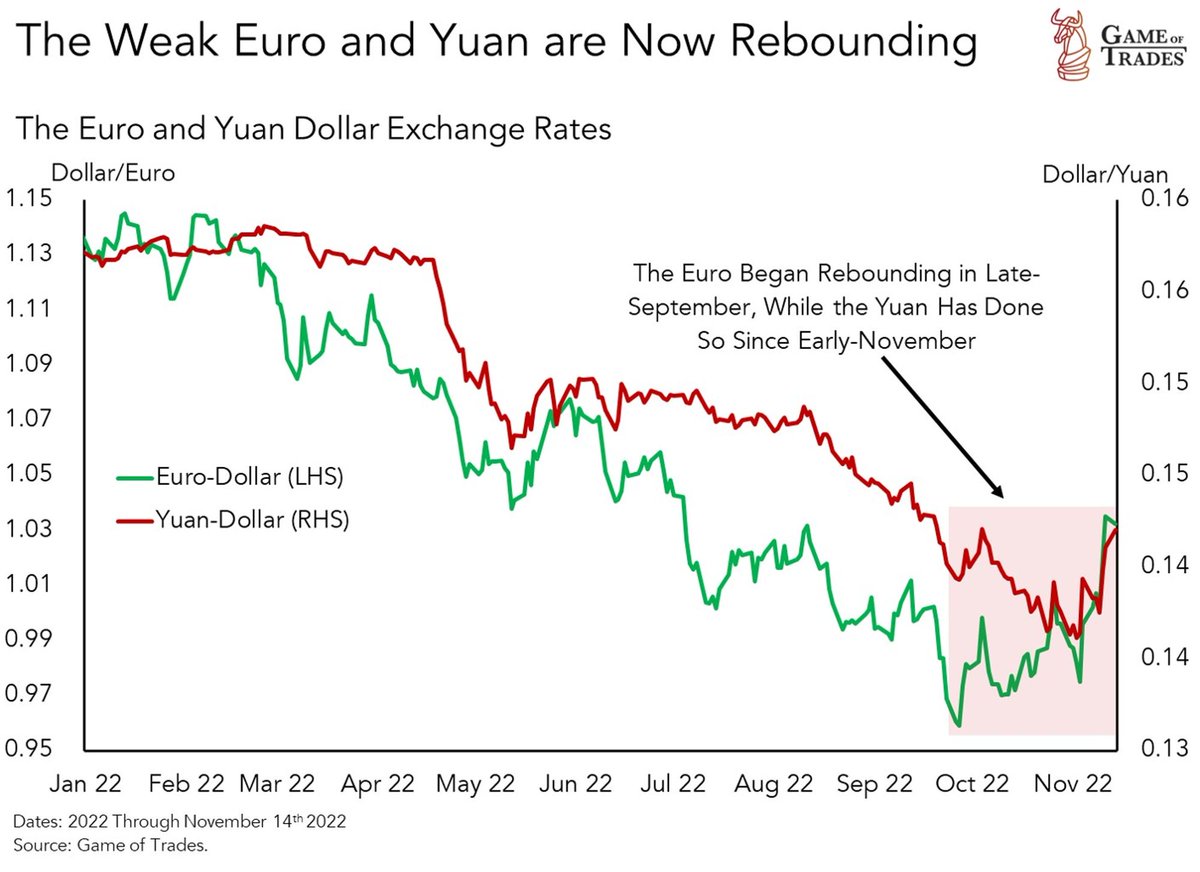

7/ Since September, the euro has seen a big rebound relative to the USD, with positive developments regarding the energy crisis in Europe

Meanwhile, the yuan has seen big appreciation with news that China will be loosening its strict Covid policies and providing stimulus

Meanwhile, the yuan has seen big appreciation with news that China will be loosening its strict Covid policies and providing stimulus

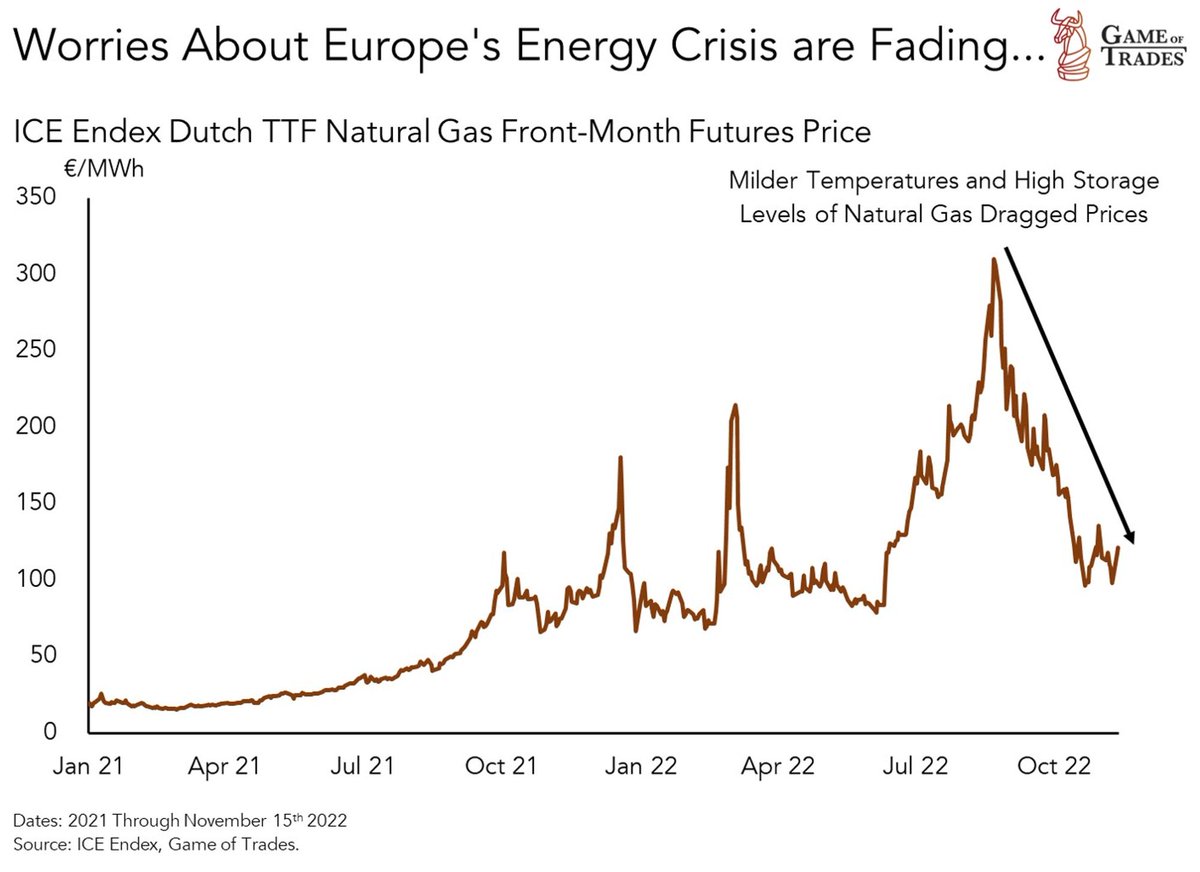

8/ Energy concerns in Europe have been dissipating

This is reflected in prices of natural gas in Europe, seeing a massive decline following their peak in late-August.

This is reflected in prices of natural gas in Europe, seeing a massive decline following their peak in late-August.

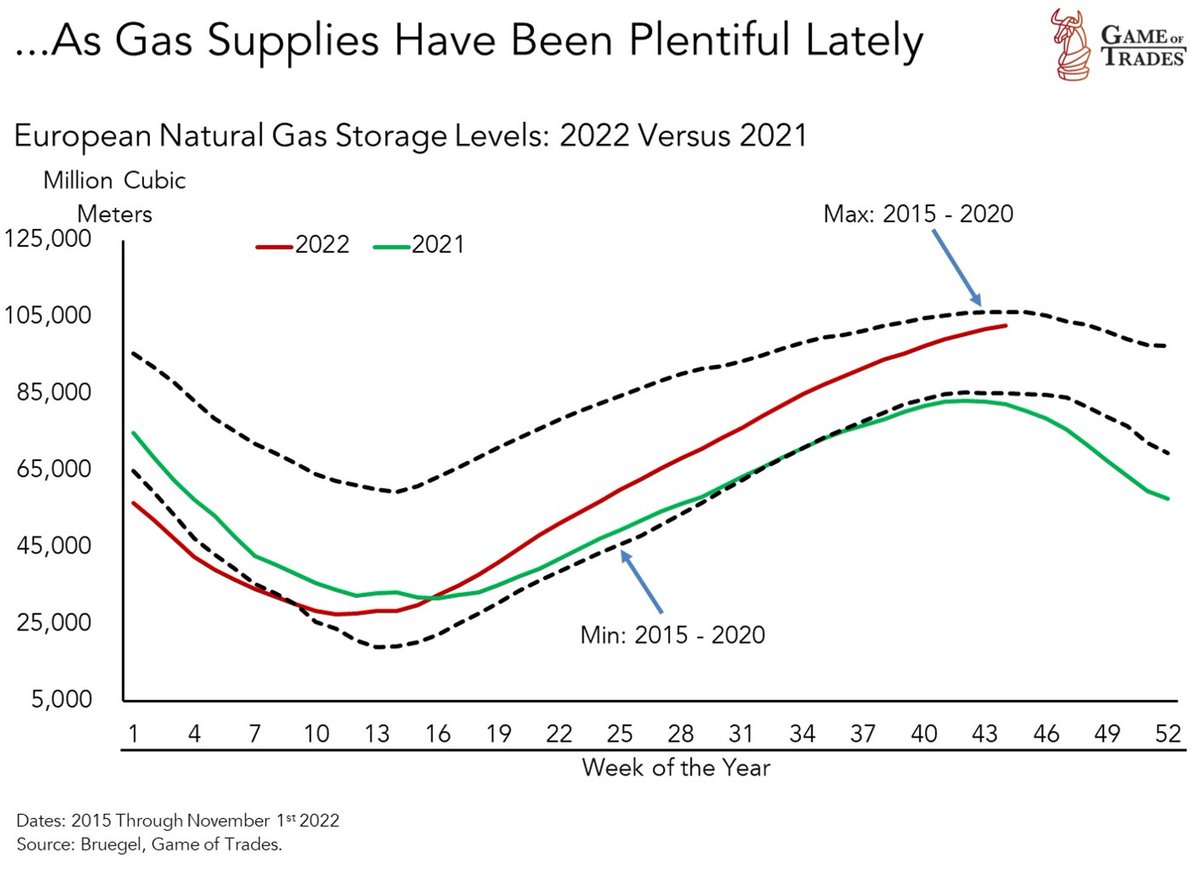

9/ One of the drivers has been the surge in natural gas supplies held in European storage.

Another driver has been milder temperatures, reducing demand.

These constructive developments have rekindled optimism on the euro.

Another driver has been milder temperatures, reducing demand.

These constructive developments have rekindled optimism on the euro.

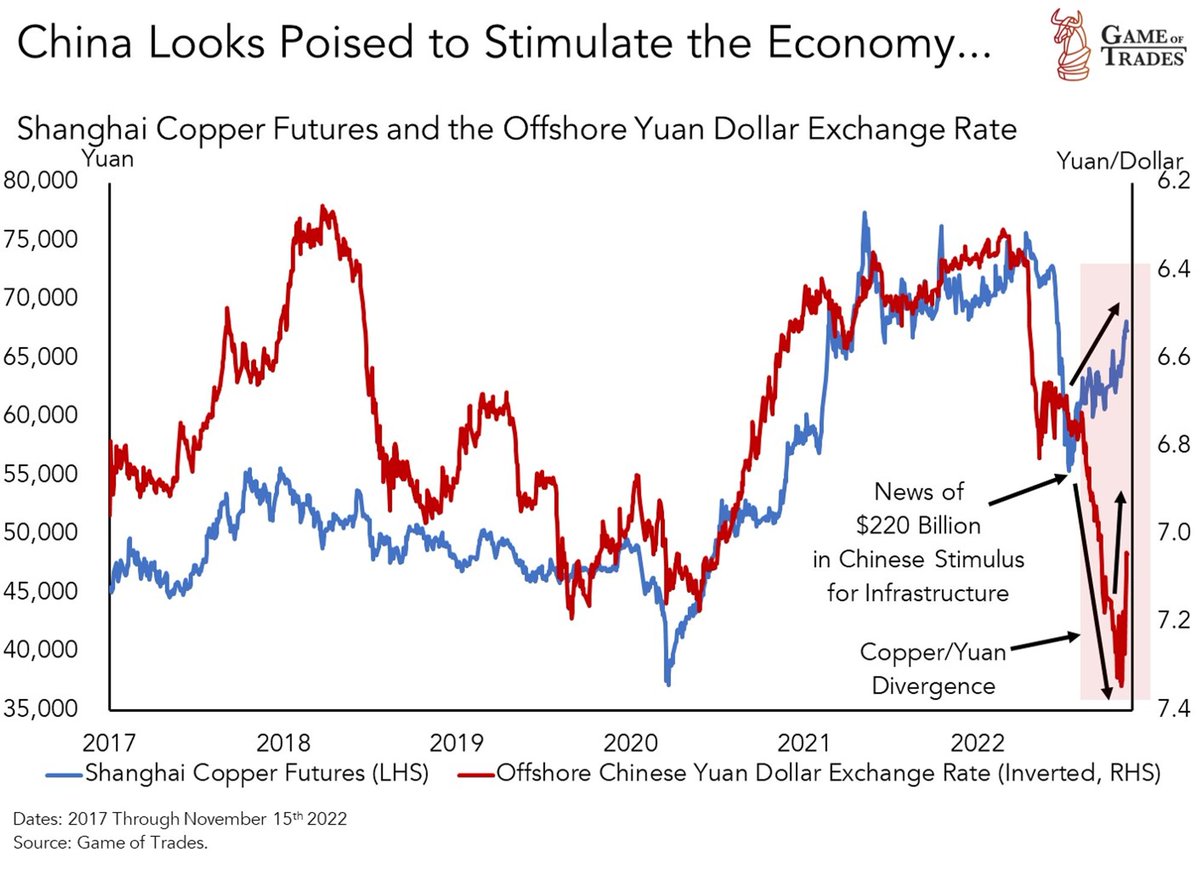

10/ Moving along to the yuan, the currency's rebound recently is a story of shifting government policy.

The Chinese government has hinted at loosening its Covid-zero policy and has also been guiding at providing stimulus for infrastructure spending.

The Chinese government has hinted at loosening its Covid-zero policy and has also been guiding at providing stimulus for infrastructure spending.

11/ Shanghai copper prices have been moving higher since mid-July following news of a potential $220 billion infrastructure spending stimulus package

The yuan now looks undervalued relative to copper and is poised to catch up to the industrial metal.

The yuan now looks undervalued relative to copper and is poised to catch up to the industrial metal.

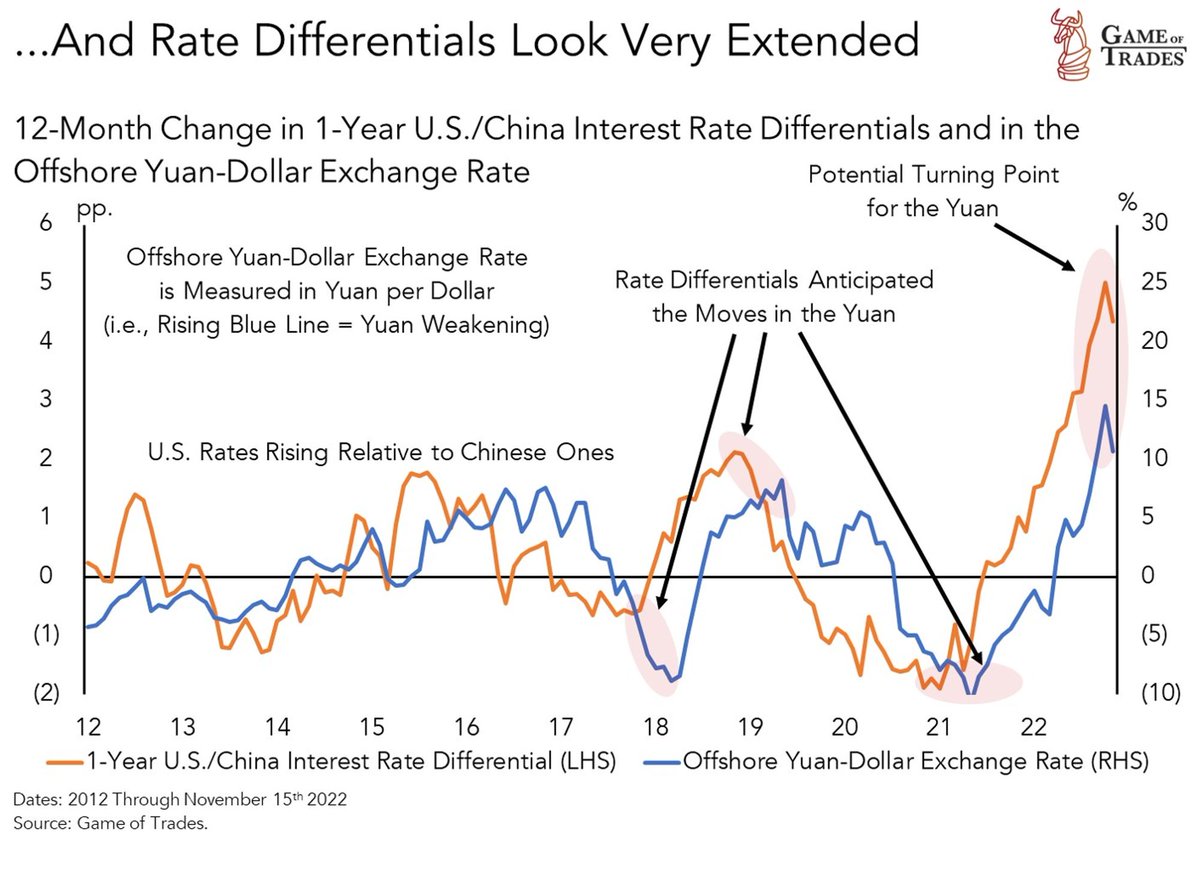

12/ Another recent driver of the yuan has been the narrowing differential in interest rates with the US

Inflation decelerating and a gradual reopening of China will lead US rates down and Chinese rates higher

→ compressing the differential and boosting the yuan

Inflation decelerating and a gradual reopening of China will lead US rates down and Chinese rates higher

→ compressing the differential and boosting the yuan

13/ Inflection points in the rate differential have anticipated big moves in the yuan in the last few years

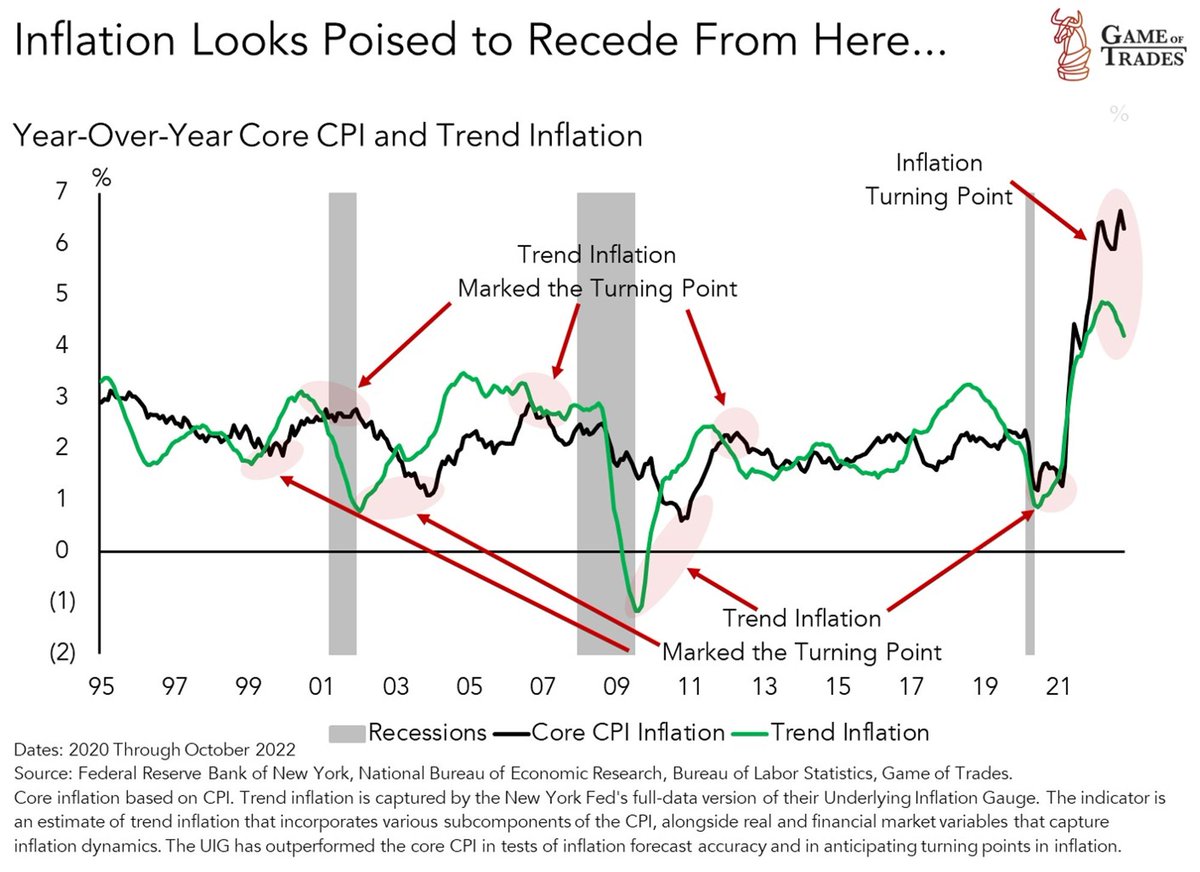

14/ Lastly, the weak CPI print of October has put downside pressure on US interest rates, narrowing rate differentials with Europe as well

Underlying trend in inflation peaked back in March

Historically it's proven a good leading indicator of headline and core inflation

Underlying trend in inflation peaked back in March

Historically it's proven a good leading indicator of headline and core inflation

15/ As inflation inflects downward, the US bond market will start pricing lower interest rates, weakening the appeal for holding USD-based assets and boosting the yuan.

It'll become a big source of downside pressure on the greenback.

It'll become a big source of downside pressure on the greenback.

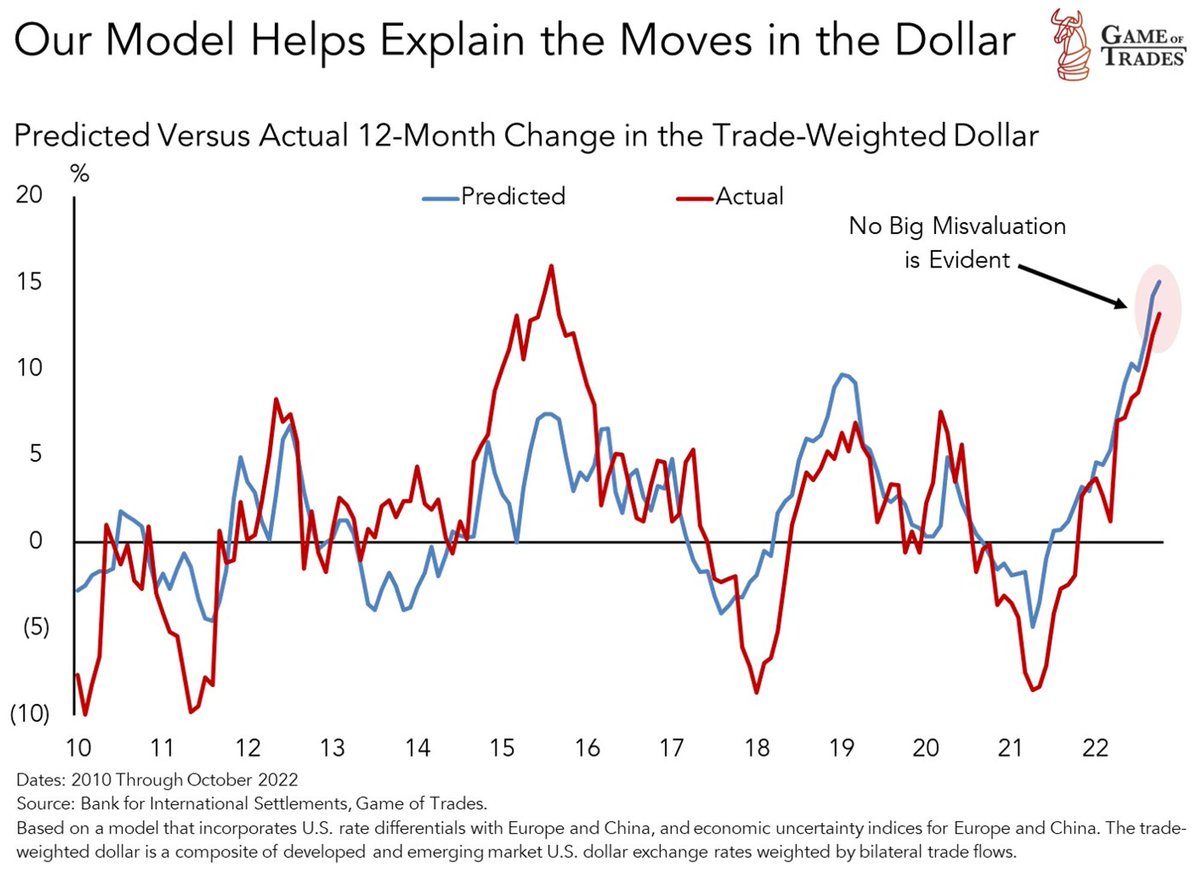

16/ Our framework for modeling the USD today involves an assessment of economic uncertainty as well as differentials in interest rates between the US, Europe, and China

17/ We built a model for explaining the moves in the USD based on the following variables:

- Economic uncertainty in Europe

- Economic uncertainty in China

- US/Europe interest rate differentials

- US/China interest rate differentials

- Economic uncertainty in Europe

- Economic uncertainty in China

- US/Europe interest rate differentials

- US/China interest rate differentials

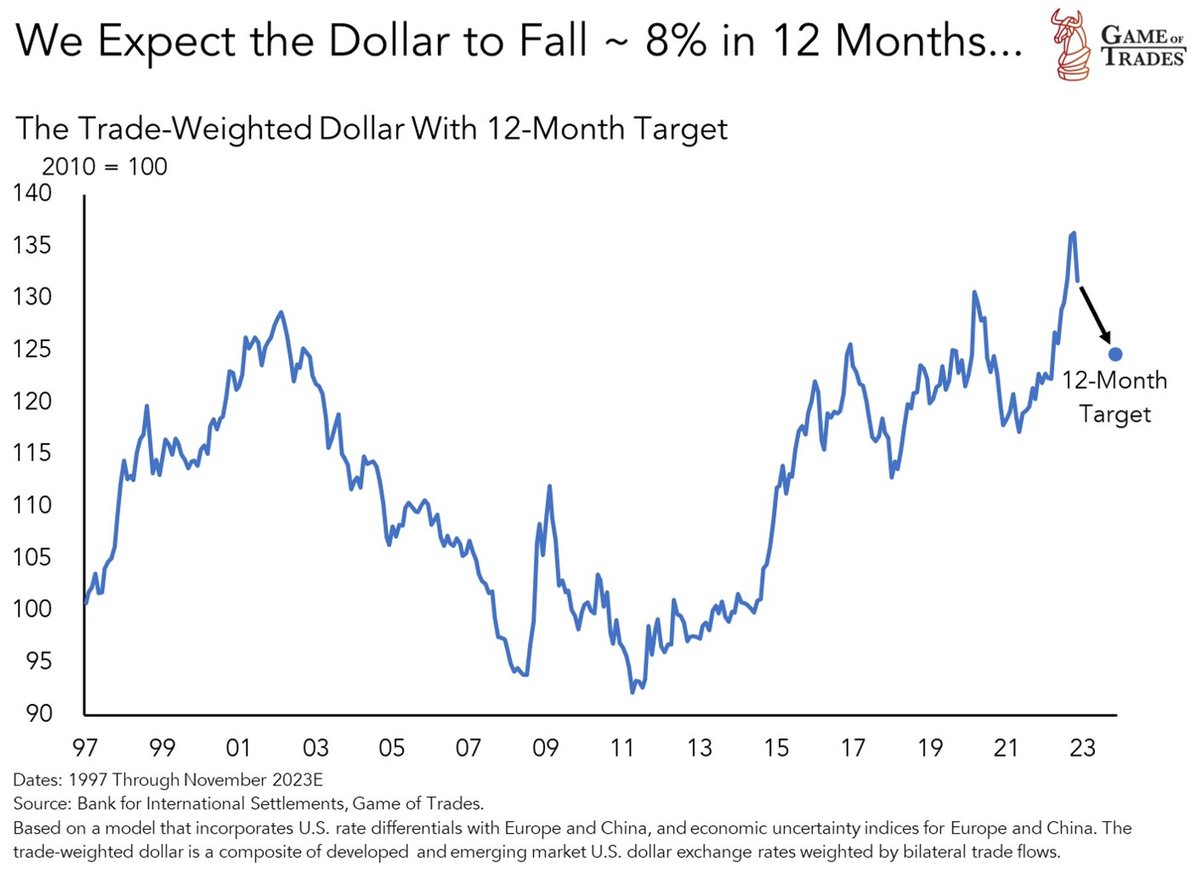

18/ We expect a decline in the USD of about 8% over the next 6-12 months

That's driven by our expectations for:

- Positive developments in Europe's energy crisis

- Loosening Covid restrictions + stimulus policies in China

- Receding inflation pressures in the US

That's driven by our expectations for:

- Positive developments in Europe's energy crisis

- Loosening Covid restrictions + stimulus policies in China

- Receding inflation pressures in the US

19/ We fed the following assumptions in our model to get our target:

20/

- Declining US inflation and the gradual reopening of China's economy eases interest rate pressures, reducing US-China rate differentials

- No change in European-US rate differentials: falling energy prices and weak economic growth will limit the ECB's ability to raise rates

- Declining US inflation and the gradual reopening of China's economy eases interest rate pressures, reducing US-China rate differentials

- No change in European-US rate differentials: falling energy prices and weak economic growth will limit the ECB's ability to raise rates

21/

- The worst of Europe's energy crisis is over for now, and uncertainty will revert to trend

- Economic uncertainty in China comes down to the level seen earlier this year before the lockdowns were implemented.

- The worst of Europe's energy crisis is over for now, and uncertainty will revert to trend

- Economic uncertainty in China comes down to the level seen earlier this year before the lockdowns were implemented.

22/ Our thesis on the USD could prove wrong if the reopening in China creates a big spike in Covid cases.

Moreover, hotter-than-expected CPI readings in the next few months could force the bond market to price in higher US rates, widening differentials.

Moreover, hotter-than-expected CPI readings in the next few months could force the bond market to price in higher US rates, widening differentials.

23/ Our call is mainly for a correction of the aggressive move in the USD that began last year.

Not calling for an end to the post-Covid USD bull run.

That's a question for another day.

Not calling for an end to the post-Covid USD bull run.

That's a question for another day.

24/ Thanks for reading!

If you liked this, please like and retweet the first tweet below.

And follow @gameoftrades_ for more market insights, finance, and investment strategy content.

[

If you liked this, please like and retweet the first tweet below.

And follow @gameoftrades_ for more market insights, finance, and investment strategy content.

[

25/ It's almost Black Friday, and we'll be launching some amazing offers this weekend!

Get Institutional-Grade Investment Research at gameoftrades.net !

Get Institutional-Grade Investment Research at gameoftrades.net !

Loading suggestions...