While they typically beat the high end of their guidance, Q3 topline was near the low end of the guidance.

Moreover, guidance appears to be weak too as Q4 implied topline growth is HSD i.e. ~7-9%.

However, Autodesk did see modest deceleration in our new business, particularly in Europe during Q3, that does have a slight follow-on impact to revenue in Q4

However, Autodesk is seeing less demand for multiyear upfront billings and more demand for annual contracts than they expected.

Customers are likely being more conscious about their cashflows in a soft macro environment.

Labor shortage continues to be primary concern.

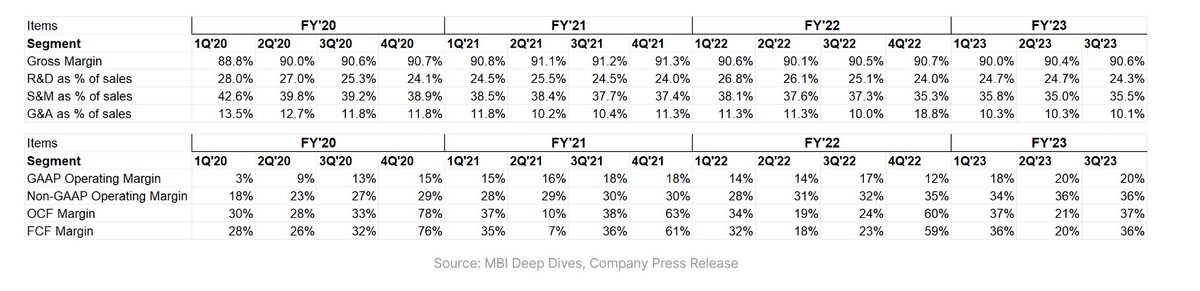

Management reiterated non-GAAP margin guidance to ~38-40% sometime in FY'23-26 window.

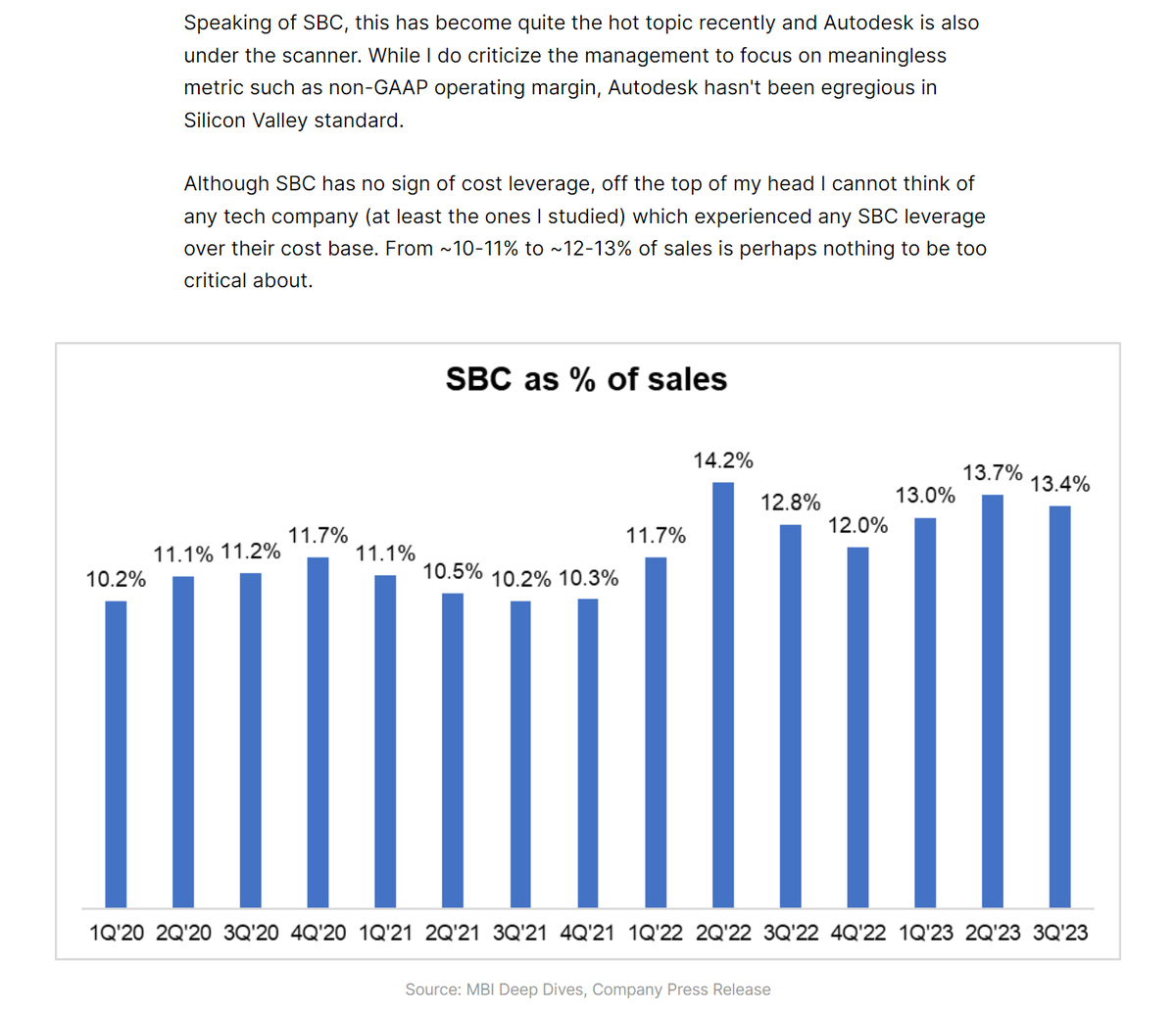

It is disappointing to see management focusing on such meaningless number. cc @andrew_anagnost

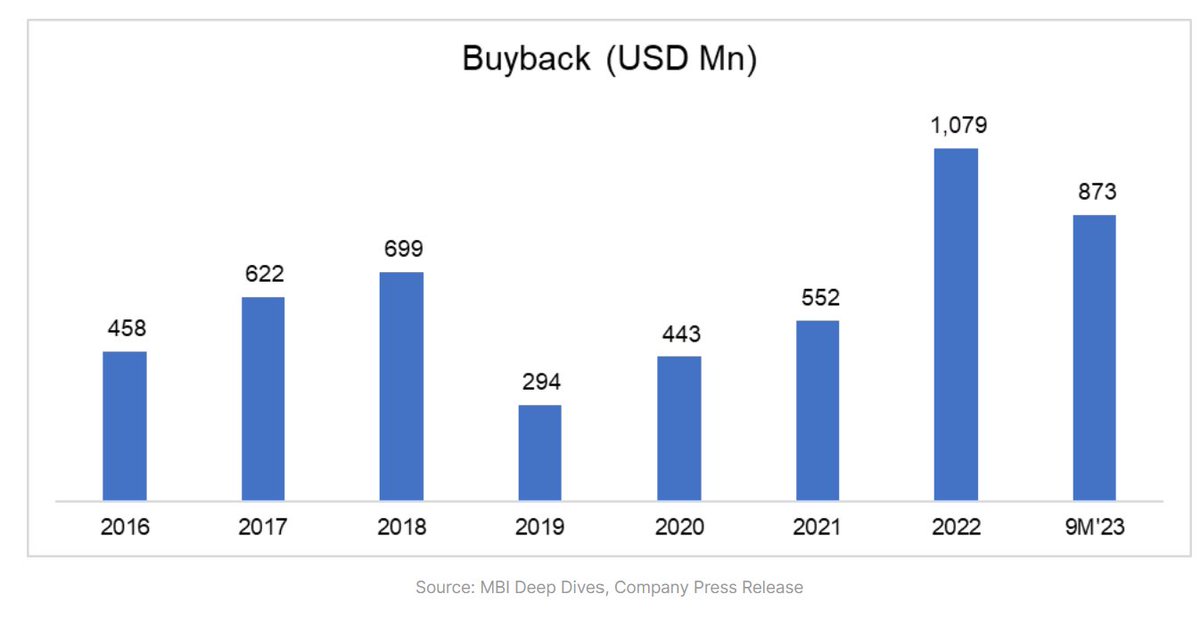

Frustratingly, they keep mentioning buying back stock primarily to offset dilution from SBC and don't think it as capital return strategy.

For my followers in the US, Happy Thanksgiving!

Recent Threads

I’ve recently seen a lot of people criticizing smaller indie projects for releasing merchandise or doing kickstarter funding to fund their projects. T...

I compiled all the specific references I noticed in May's moveset! #イニブ #g_bd #g_bdr #GBDR https://t.co/PvNHzH6yj6

taekook taguan ng anak au wherein jk received a surprising gift from their xmas party… [ christmas special 🎄] https://t.co/WY3C450KpV

@HitWithAHeart I hear him before I see him. The weight of his steps on the stairs. Slower than usual. Measured. Like he’s already bracing for whatev...

(1/7) I'm not going to do a full trailer breakdown for Zach Cregger's Resident Evil film, since we have an early form of the script you can place a lo...

Nikola Jokic is 0-6 against 50+ win teams in the playoffs. https://t.co/l5hCeVCoUj

Popular Threads

Winning the Chevening Scholarship + 12 Strong Samples of the Chevening Essay There are four important Essays on the Chevening Scholarship application...

The ICT Mentorship Core Content Month 1 Summarized: https://t.co/6tXJxPMDhm

Here's 40 TikTok hooks that could make you go viral. (Not in any particular order) //THREAD//

A thread: Pakistani newspaper Dawn's front pages from 4th december 1971 to 20 December to see how they kept their own people in the dark. This was on...

ICT’s 2022 Mentorship Summarized: https://t.co/zFJCgIfDAR

Ware County, Ga has broken the Dominion algorithm: Using sequestered Dominion Equipment, Ware County ran a equal number of Trump votes and Biden vote...