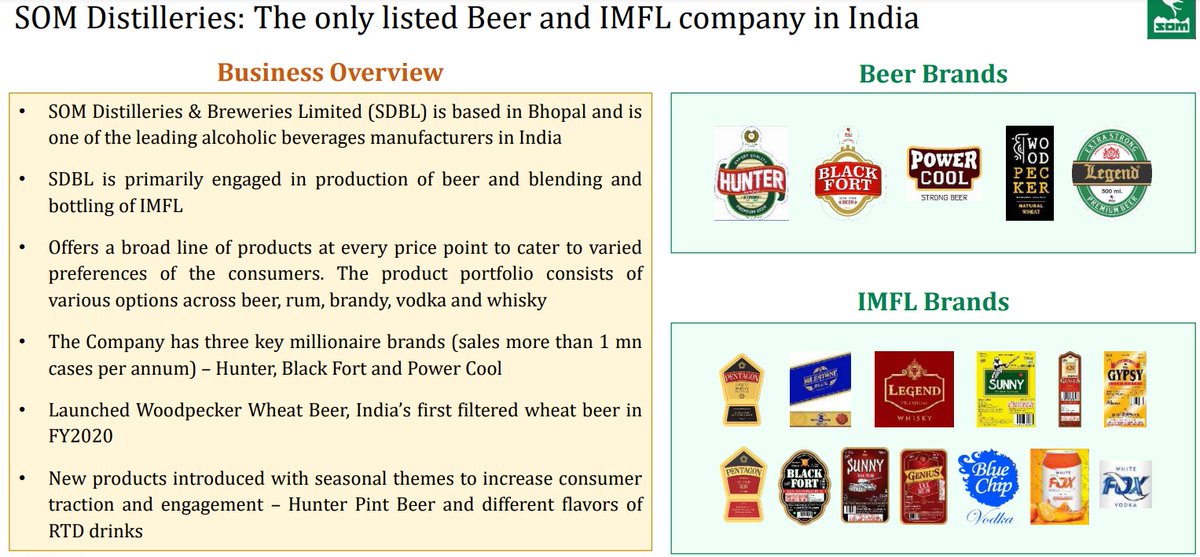

Som Distilleries: A small cap beer co, based out of Bhopal, has 3 millionaire brands (sells million cases p.a.) – Hunter, Power Cool & Black Fort. Currently has presence in MP (55% rev), Karnataka (25% Rev), Odisha (15% Rev), UP, Kerala, Delhi. A quick thread 👇

1/10

1/10

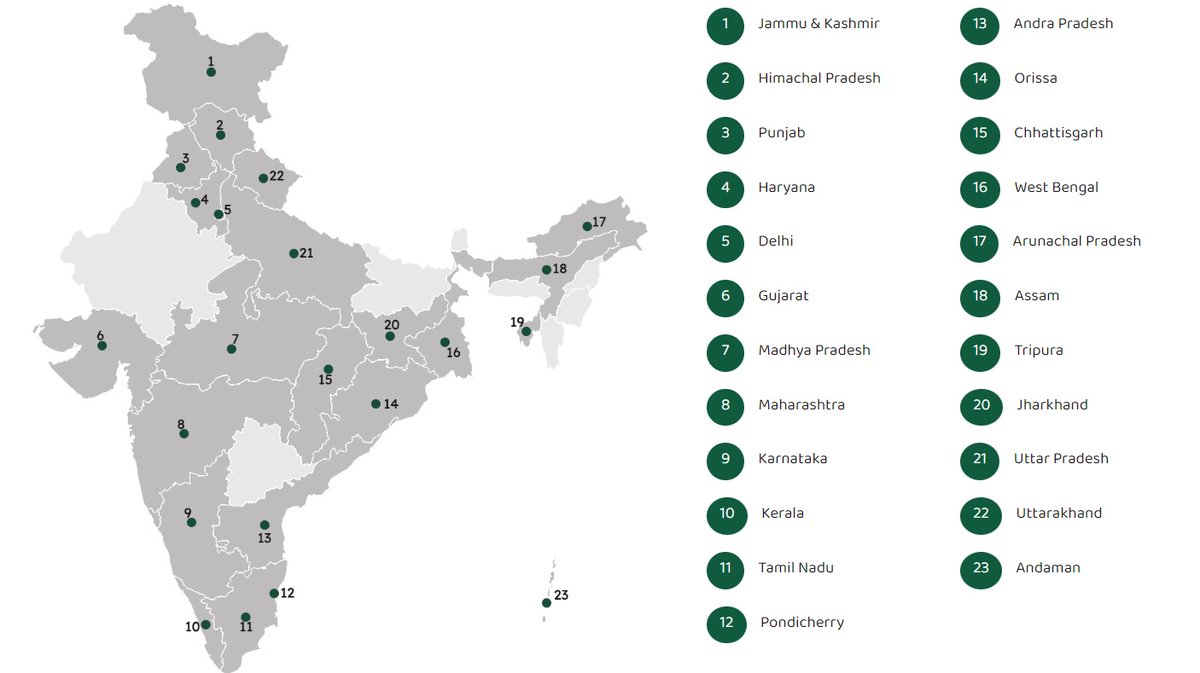

Co currently has 3 plants – Bhopal (state-of-the-art), Karnataka & Orissa. While Karnataka facility is running at 100% capacity utilization, Bhopal & Orissa are running at 65% utilization. Co is in the midst of significant capacity expansion.

2/10

2/10

Increasing canning capacity in Bhopal from 15k cases/day to 65k cases/day. This additional capacity is expected to be operational by Feb end & be ready for the upcoming season - can expect it to run at 100%. Post this, Som will have India’s largest canning facility.

3/10

3/10

Co is also doubling its wheat beer (Woodpecker) capacity in Karnataka from 4.5mn cases to 8.5mn cases. In Orissa expansion will take capacity from 3.5lac cases/month to 8lac cases/month. The total capex stands at 150cr of which 70cr has already been expended.

4/10

4/10

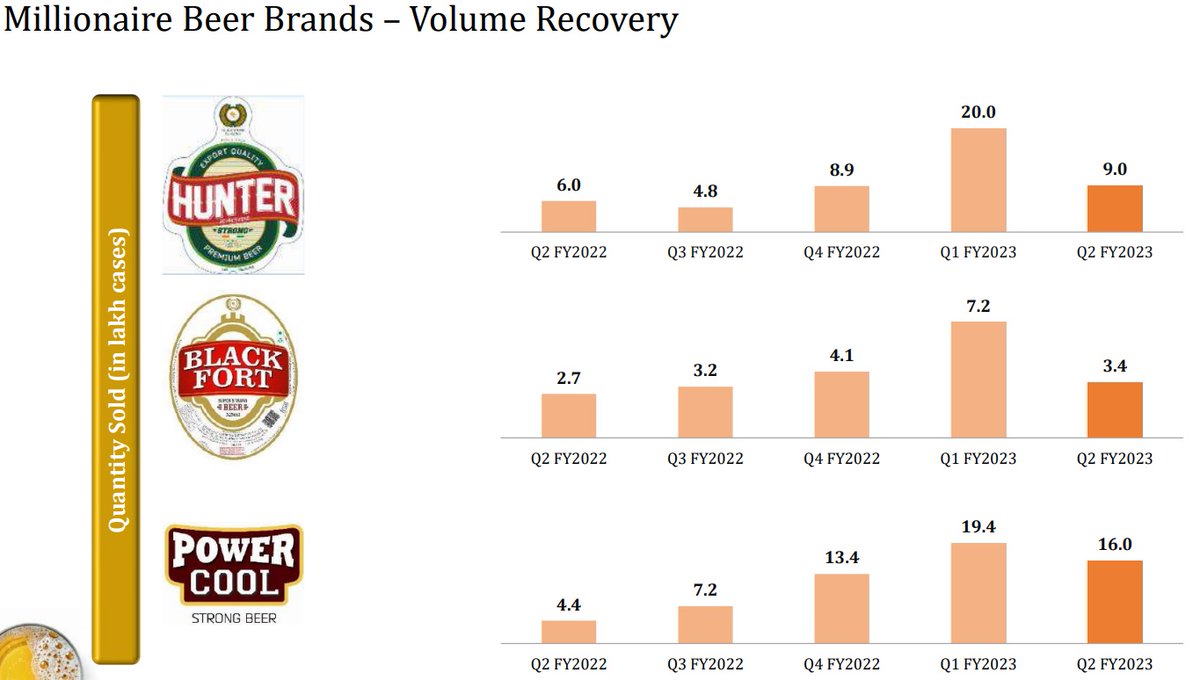

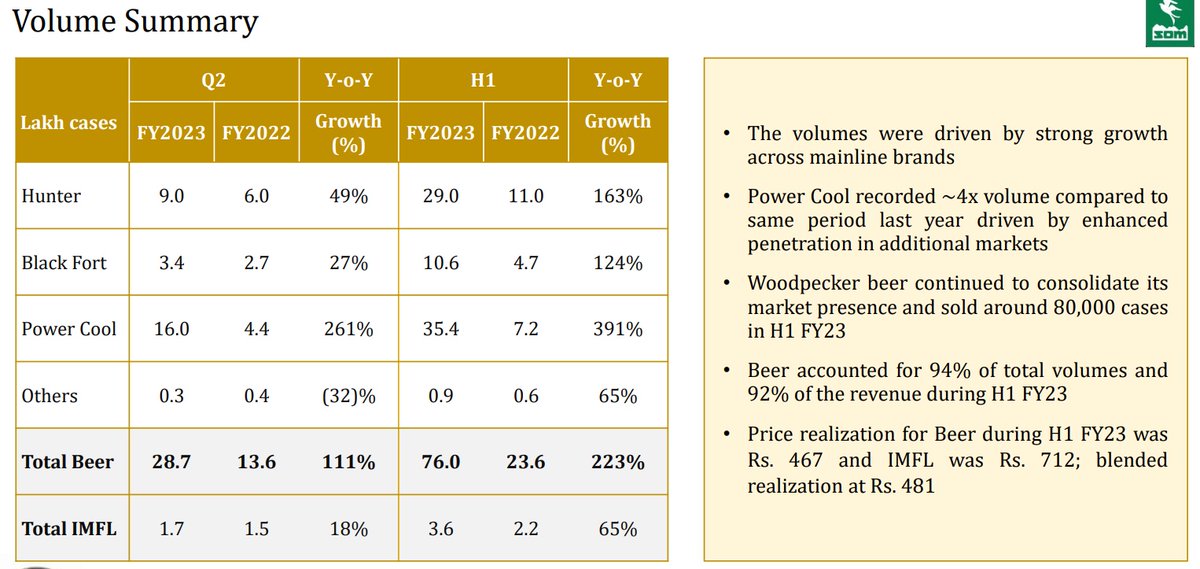

While co plans to sell 12.5mn cases in FY23, post expansion co can potentially sell 20mn cases p.a.

Current Market Standing:

MP – 1 (45% mkt share)

Karnataka – 3 (aims to be no 2 in this season)

Odisha – 2

Kerala – 3

Delhi – 3

5/10

Current Market Standing:

MP – 1 (45% mkt share)

Karnataka – 3 (aims to be no 2 in this season)

Odisha – 2

Kerala – 3

Delhi – 3

5/10

Apart from going deeper in existing mkts like Bhopal, Karnataka & Orissa; co is expanding aggressively (potential to grow 200-300% in this season) in UP where its products have received very good response. Other new mkts are Maharashtra, Jharkhand, WB

6/10

6/10

Company’s major sales happen via government canteens (CDS) & has majorly targeted states where distribution happens via this channel. States like Maharashtra where distribution is private, company has been wary of expanding at a rapid pace.

7/10

7/10

With 2x expansion, strong entry barriers, millionaire brands, favorable govt policies & powerful consumption tailwinds, co has the potential to grow profitability at 50-60% CAGR over FY23-FY25. Single digit valuation on FY25 earnings: 7-8x PE makes risk reward favorable.

8/10

8/10

While promoter holding is low currently, they have been increasing their stake over the past few qtrs: 24.5% in Dec '21 to 33.3% currently. Promoters keen to take this to 51% over the next 3yrs. New gen has been instrumental & should be a key driver for re rating

9/10

9/10

Risks:

Government policies (if state govt decides to ban alcohol)

Distribution (no advertisements allowed + govt controlled)

Promoter legacy (arrest warrant issued in GST case, given a clean chit, low holding but now moving up)

10/10

Government policies (if state govt decides to ban alcohol)

Distribution (no advertisements allowed + govt controlled)

Promoter legacy (arrest warrant issued in GST case, given a clean chit, low holding but now moving up)

10/10

Loading suggestions...