Survive To Thrive Part 3

Originally written in January 2021.

Reproducing again ~2 years later with some updates.

A Long thread 🧵

"Retweet" if you find value.🙏

Let's go!

Originally written in January 2021.

Reproducing again ~2 years later with some updates.

A Long thread 🧵

"Retweet" if you find value.🙏

Let's go!

At the time of the covid-induced market crash, we were reviewing clients’ performance over the last 3 yrs.

We noticed an interesting pattern.

Clients who committed to investing each month a fixed amount each did much better than the clients who gave us a lump sum.

We noticed an interesting pattern.

Clients who committed to investing each month a fixed amount each did much better than the clients who gave us a lump sum.

Three points to know before we move ahead:

1. It did not matter whether the fixed monthly committed amount was 5000, 50,000, or 5,00,000.

1. It did not matter whether the fixed monthly committed amount was 5000, 50,000, or 5,00,000.

2. While the choice of stocks and MF schemes did influence the magnitude, even an ordinary-looking portfolio of stocks or a bunch of MFs returned a decent CAGR if it was in an auto SIP mode.

3. A portfolio with even very good MF schemes or high-quality businesses did not provide as good a return as the SIP one as a substantial chunk of the invested amount was put into work as a lump sum.

We had the following 3 thoughts.

Remember it was April/May 2020.

1. Maybe, our sampling size is too small.

Remember it was April/May 2020.

1. Maybe, our sampling size is too small.

2. In the last four years, market has been very volatile (Nifty went from 8K to 11k and then back to 8K and currently above 14K. Midcap and small-cap indices have witnessed even more volatility.

3. Maybe, over the long term, this will not sustain.

So we started digging for some historical data.

Whatever narrative we may try to project or sell, there is only one benchmark to check whether your investment has done well or not over the long term.

And that is Returns.

So we started digging for some historical data.

Whatever narrative we may try to project or sell, there is only one benchmark to check whether your investment has done well or not over the long term.

And that is Returns.

We took Infosys as an example, to begin with.

We all know that Infosys was valued at an obscene P/E ratio of ~ 200 times during the dot-com bubble. If you had bought Infosys in 2000 at the height of the Y2K mania and held it until 2008, you would have made 0 returns.

We all know that Infosys was valued at an obscene P/E ratio of ~ 200 times during the dot-com bubble. If you had bought Infosys in 2000 at the height of the Y2K mania and held it until 2008, you would have made 0 returns.

However, suppose you had purchased 1 share of Infosys on the first day of each month starting from the month in which Infosys made a top in the year 2000. And you continued this process until 2008.

You would have earned a 13% XIRR on that investment.

You would have earned a 13% XIRR on that investment.

The XIRR would have been even higher if instead of buying 1 share, you invested a fixed amount in Infosys every month.

To know how to apply the XIRR function, check this

youtu.be

To know how to apply the XIRR function, check this

youtu.be

OK. You know that Infosys at the height of euphoria is probably an extreme example.

Let’s look at another extreme example.

You picked Titan, a not–so–hot stock at that time, and you followed the same SIP rule.

And here you get a mind-boggling 54% XIRR.

Let’s look at another extreme example.

You picked Titan, a not–so–hot stock at that time, and you followed the same SIP rule.

And here you get a mind-boggling 54% XIRR.

Both Infosys and Titan had only one thing in common, their business continued to grow and the revenues and profit growth were clear evidence for you to believe that the business directionally was doing well.

The thinking behind this whole exercise is to challenge the old belief that we have been holding on to for a decade that you'll have to have a strong grip on the valuation of a business before investing in it.

We at SSS are slowly trying to change our view on that.

Don’t get us wrong. We are not saying Valuation doesn’t matter.

Neither are we saying that buying and holding obscenely valued companies is the way to riches.

Certainly not.

Don’t get us wrong. We are not saying Valuation doesn’t matter.

Neither are we saying that buying and holding obscenely valued companies is the way to riches.

Certainly not.

We believe focusing on the long-term growth of the business (of course tracking its performance regularly) and getting into a system of buying good and growing businesses on a regular basis will help you counter the valuation problem effectively.

After all our education in finance and experience in the stock market investing for over a decade, we only surrender to the fact:

"Value indeed lies in the eye (read excel models) of the investor."

"Value indeed lies in the eye (read excel models) of the investor."

Nobody knows the real value. We can only guess. And even the best of the best investors make big horrible mistakes in valuation.

We, lesser mortals, are probably better off not participating in this contest and hence not trying to base our investment decision based on valuation.

We, lesser mortals, are probably better off not participating in this contest and hence not trying to base our investment decision based on valuation.

So valuation does matter but let’s not base our decision on it because we get tricked into selling winners early and holding on to losers.

There are many other stocks that do well even when they are highly priced, to begin with. The main thing to consider for you would be whether the business would continue to remain strong or not. If yes, you should continue your SIP in them.

And just like the NIFTY index balancing, you should remove the businesses which are not performing well.

A key difference is that NIFTY uses market valuation as a metric to decide, however, you will use the business growth and longevity to decide.

A key difference is that NIFTY uses market valuation as a metric to decide, however, you will use the business growth and longevity to decide.

You might ask why Infy & Titan.

I know no one can unearth and hold multi-baggers like Rakesh Jhunjhunwala.

There is a reason why we took two extreme examples.

"Every virtue is a mean between two extremes, each of which is a vice."

I know no one can unearth and hold multi-baggers like Rakesh Jhunjhunwala.

There is a reason why we took two extreme examples.

"Every virtue is a mean between two extremes, each of which is a vice."

Aristotle in the above quote says that moral virtue is to behave in the right manner and that is a mean between extremes of deficiency and excess, which are vices. We learn moral virtue primarily through habit and practice rather than through reasoning and instruction.

From an investing standpoint, we have to be aware that we cannot pick only the Infosys & Titans of 2000. We will be having a few others too. Some would show average performance. A few will fail miserably.

If you have luck &skills on your side, you may get a couple of 10-20x type stocks too. You will also have to replace the losers in your portfolio with new businesses. Businesses that come up in your watchlist and look better than some of the existing businesses in the portfolio.

So, “Survive to Thrive” is not just a thought to motivate yourself in investing and life in general.

“Survive to Thrive” is also a system and a pattern that investors must seek in businesses they want to own.

“Survive to Thrive” is also a system and a pattern that investors must seek in businesses they want to own.

After having done your due diligence and convinced about an investment idea, just before pulling the trigger to buy, it pays to ask this question:

Will it Survive to Thrive?

Will it Survive to Thrive?

You may not be right all the time in answering that question. However, it will embed a condition that will force you to think long-term.

However, let us put a caveat here.

At diff points like March 2020, 2012-2013, and 2008, your portfolio returns will look atrocious.

However, let us put a caveat here.

At diff points like March 2020, 2012-2013, and 2008, your portfolio returns will look atrocious.

The biggest mistake most of us do is panicking and selling the portfolio during those drawdowns. And this is the biggest risk you have to mitigate as an investor.

SIP in MF/stocks will yield a "-" result if you buy high & sell low or try to time the market.

You may take CM’s advice:

"It’s remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent."

You may take CM’s advice:

"It’s remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent."

The drawdown of your portfolio value during extreme pessimism makes you fearful. T

The only way to beat that successfully as a long-term investor is to systematically continue to invest during ups and downs.

The only way to beat that successfully as a long-term investor is to systematically continue to invest during ups and downs.

As individual investors, we start with very little capital and as we rise up the ladder, we earn more, save more, and have more money to invest in the market.

If you really want to do well, all you need is these 3 things:

If you really want to do well, all you need is these 3 things:

1.

Invest time and money in skill development in the early part of your carrier to earn well.

You may build a business or you may work for someone.

Don’t get into the ego battle of which one is better.

Trust us, both work well. Check what works well for you.

Invest time and money in skill development in the early part of your carrier to earn well.

You may build a business or you may work for someone.

Don’t get into the ego battle of which one is better.

Trust us, both work well. Check what works well for you.

2.

Save aggressively & invest systematically. Initially, in a few broad index funds or MFs. And gradually as your investible amount increases over time, shift to systematically investing directly into stocks if you can develop confidence in understanding businesses.

Save aggressively & invest systematically. Initially, in a few broad index funds or MFs. And gradually as your investible amount increases over time, shift to systematically investing directly into stocks if you can develop confidence in understanding businesses.

3.

Don’t interrupt compounding. Stay the course through the ups and downs.

Period!

Don’t interrupt compounding. Stay the course through the ups and downs.

Period!

That sounds too simple to believe. Right?

But there are success stories.

We admit. Not too much. But there are for sure.

They are the ones who took the pledge to stay put on the path of systematically investing through ups and downs and never stopped.

But there are success stories.

We admit. Not too much. But there are for sure.

They are the ones who took the pledge to stay put on the path of systematically investing through ups and downs and never stopped.

Morgan Housel, one of the finest writers and thinkers on investing today, says this in an interview with Safalniveshak’s founder, Vishal Khandelwal:

And let’s admit that most of us know this in theory but fail to follow it in practice.

You know that junk food is bad but dieticians earn their living by telling you to avoid it.

You know that doing physical exercise is good but you hire a physical trainer to be more disciplined.

You know that doing physical exercise is good but you hire a physical trainer to be more disciplined.

You know that eating well, sleeping well, low mental stress and physical exercise take care of 90% of your health problems, but you still seek advice from doctors and psychologists to keep you in order.

Similarly, an investment advisory firm like @SmartSyncServ earns its fees by just making sure you are keeping up with your financial health and staying invested for the long term.

Morgan Housel also says this:

"How long you stay invested for will likely be the single most important factor determining how well you do at investing."

"How long you stay invested for will likely be the single most important factor determining how well you do at investing."

If we had a chance to ask just one question to Morgan, we would definitely like to hear his views on adding just another factor and rephrase the above quote like this:

"How long you stay invested & how regularly you keep investing in your lifetime are the 2 most important factors determining how well you do at investing."

If you are reading this and are friends with Morgan, please ask him for his views.😃

If you are reading this and are friends with Morgan, please ask him for his views.😃

If you find reading a blog more convenient than reading a thread, here you go:

smartsyncservices.com

smartsyncservices.com

Just talking theory is of no use if you do not practice.

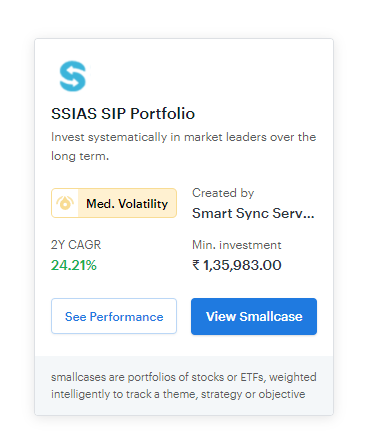

All the founders of SSS invest in the SSIAS SIP Portfolio which we started in August 2020.

2.5 years is too small a time frame for a long-term portfolio. But that's what we have now.

Details:smartsyncservices.com

All the founders of SSS invest in the SSIAS SIP Portfolio which we started in August 2020.

2.5 years is too small a time frame for a long-term portfolio. But that's what we have now.

Details:smartsyncservices.com

While most advisors only share their portfolio updates when their portfolio is doing good, we have a policy of sharing updates both in good and bad times. So that investors can take a much more informed decision.

Here's a glimpse of our communication

Here's a glimpse of our communication

If you find our research insightful, here are the 3 simple steps you need to follow:

1. Follow us @SmartSyncServ

2. Go to our Twitter bio & register for our free newsletter

3. "Retweet" the first tweet to help us educate maximum investors

Thank you for reading 🙏

1. Follow us @SmartSyncServ

2. Go to our Twitter bio & register for our free newsletter

3. "Retweet" the first tweet to help us educate maximum investors

Thank you for reading 🙏

Loading suggestions...