In this Detailed Thread 🧵 I'll Analyse Siyaram Silk Mills in Details. Each and every neeche information about Siyaram Silk will be covered in this Thread from this Business, to its Product Mix, to its Fundamentals & Financials, to its Management, to its Chart

#SiyaramSilk

#SiyaramSilk

Pattern📈📉Analysis, to its annual reports information. At last I'll give my final commentry👨💻about this stock

🎖️About the Company

✅Siyaram Silk Mills Ltd is a Textile manufacturing company.

✅It is engaged in manufacturing fabrics and readymade garments, especially in the

🎖️About the Company

✅Siyaram Silk Mills Ltd is a Textile manufacturing company.

✅It is engaged in manufacturing fabrics and readymade garments, especially in the

men’s wear section.

✅The Company exports to countries like Abu Dhabi, Australia, Bahrain, Bangladesh, Cambodia, Canada, etc.

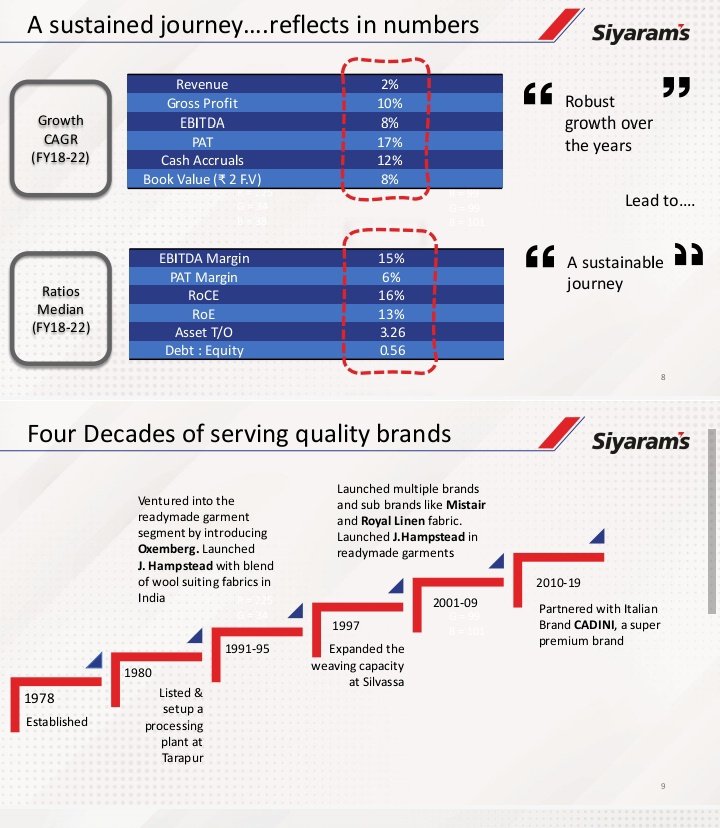

🎖️Company History

✅The Company was established in 1978 and promoted by Late Shri Dhara Prasad Poddar.

✅The Company exports to countries like Abu Dhabi, Australia, Bahrain, Bangladesh, Cambodia, Canada, etc.

🎖️Company History

✅The Company was established in 1978 and promoted by Late Shri Dhara Prasad Poddar.

✅Currently, the business is managed by his son Mr Ramesh D. Poddar as Chairman and MD.

✅In 1984, As a part of backward integration it set up a manufacturing plant for textured yarn at Patalganga, In 1991 it entered into the readymade garment segment by introducing

✅In 1984, As a part of backward integration it set up a manufacturing plant for textured yarn at Patalganga, In 1991 it entered into the readymade garment segment by introducing

Oxemberg and in 2015 Partnered with Italian Brand CADINI.

🎖️Products

🪙Fabrics - Fabrics includes Suiting & shirting fabrics, Cotton Linen, Wool Linen, garments etc.

🪙Apparel - This segment includes Ready Made clothes.

🪙Home Furnishing - It includes Home furnishing fabric

🎖️Products

🪙Fabrics - Fabrics includes Suiting & shirting fabrics, Cotton Linen, Wool Linen, garments etc.

🪙Apparel - This segment includes Ready Made clothes.

🪙Home Furnishing - It includes Home furnishing fabric

with designs including international, Regional, Ethnic, Retro.

🪙Institutional - Under this segment there is a varied range of garments, including formal wear, casual attire, corporate uniforms and home furnishing fabrics.

🪙Yarns - Poly/Viscose/Cotton Fabrics, Poly/Wool

🪙Institutional - Under this segment there is a varied range of garments, including formal wear, casual attire, corporate uniforms and home furnishing fabrics.

🪙Yarns - Poly/Viscose/Cotton Fabrics, Poly/Wool

and Poly/Viscose/Wool Fabrics, etc.

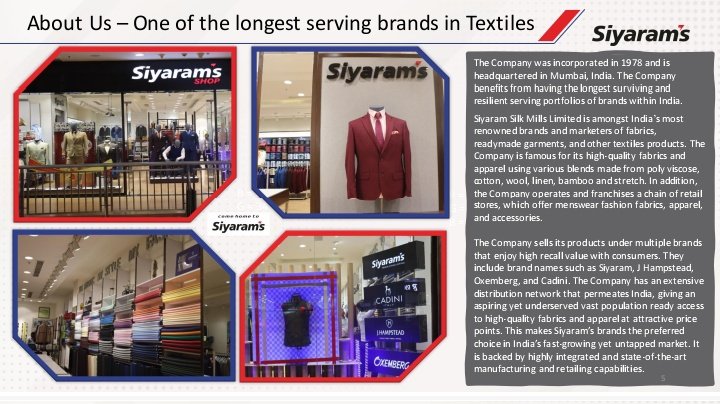

🎖️Brands

Some of the major brands under company name are Siyaram’s, J Hampstead, Cadini, Oxemberg, Casa Moda, Mozzo

🎖️Revenue Mix

🪙Fabrics: 73%

🪙Readymade Garments: 20%

🎖️Brands

Some of the major brands under company name are Siyaram’s, J Hampstead, Cadini, Oxemberg, Casa Moda, Mozzo

🎖️Revenue Mix

🪙Fabrics: 73%

🪙Readymade Garments: 20%

🎖️Manufacturing Facilities

✅Weaving Unit - 3 plants in Tarapur, Maharashtra and 1 in Silvassa.

✅Yarn Unit - 1 in Tarapur, Maharashtra

✅Readymade Garments Unit - 2 Plants in Daman & Diu.

Dyeing Unit - Tarapur, Maharashtra

Indigo Yarn Dyeing - Amravati, Maharashtra.

✅Weaving Unit - 3 plants in Tarapur, Maharashtra and 1 in Silvassa.

✅Yarn Unit - 1 in Tarapur, Maharashtra

✅Readymade Garments Unit - 2 Plants in Daman & Diu.

Dyeing Unit - Tarapur, Maharashtra

Indigo Yarn Dyeing - Amravati, Maharashtra.

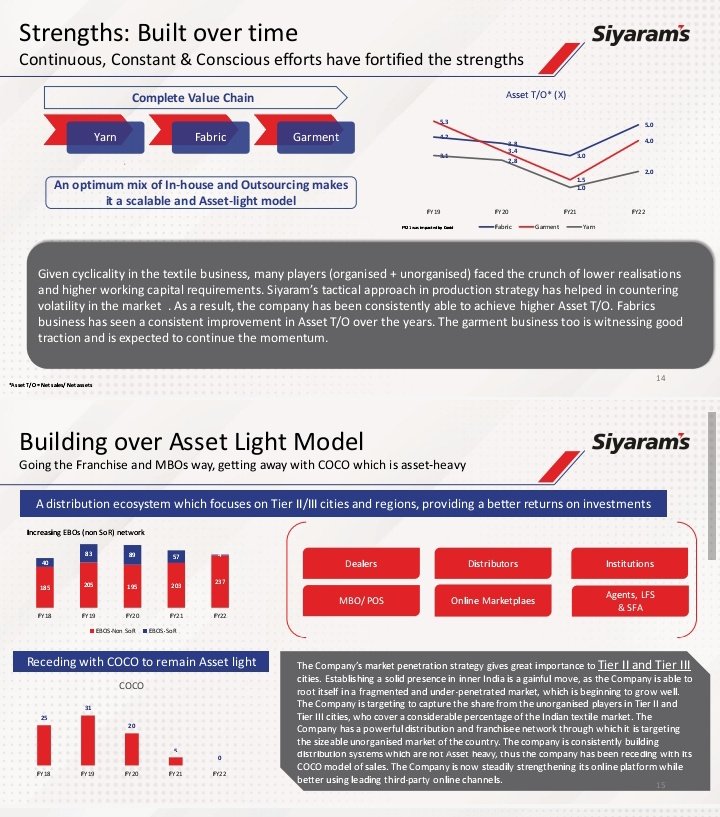

🎖️Fundamental Analysis

✅Market Cap:- Rs 2427 Cr

✅Stock PE:- 9.27(Undervalued)

✅Industry PE:- 15

✅Book Value:- Rs 221

✅Intrinsic Value:- Rs 437

✅Graham No:- Rs 523

✅ROCE:- 29.2%

✅ROE:- 24.7%

✅Dividend Yield:- 1.78%

✅Debt to Equity:- 0.24

✅Reserves:- Rs 1025 Cr

✅Market Cap:- Rs 2427 Cr

✅Stock PE:- 9.27(Undervalued)

✅Industry PE:- 15

✅Book Value:- Rs 221

✅Intrinsic Value:- Rs 437

✅Graham No:- Rs 523

✅ROCE:- 29.2%

✅ROE:- 24.7%

✅Dividend Yield:- 1.78%

✅Debt to Equity:- 0.24

✅Reserves:- Rs 1025 Cr

✅Debt:- Rs 252 Cr

✅Fixed Assets:- Rs 468 Cr

✅CWIP:- 20 Cr

✅Investments:- 70 Cr

✅Promoters Holding:- 67.18%

✅FII Holding:- 2.66%

✅DII Holding:- 6.11%

✅Public Holding:- 24.4%

✅PEG Ratio:- 0.50

✅Piotroski Score:- 6

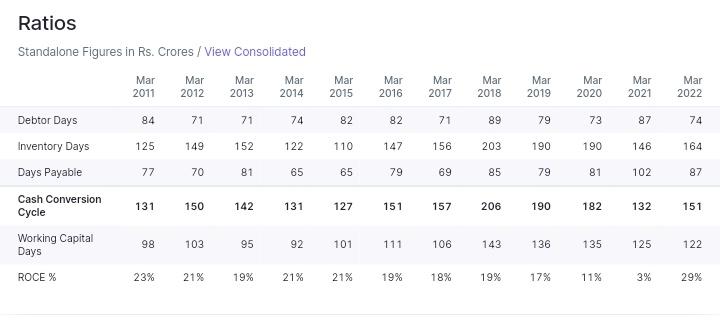

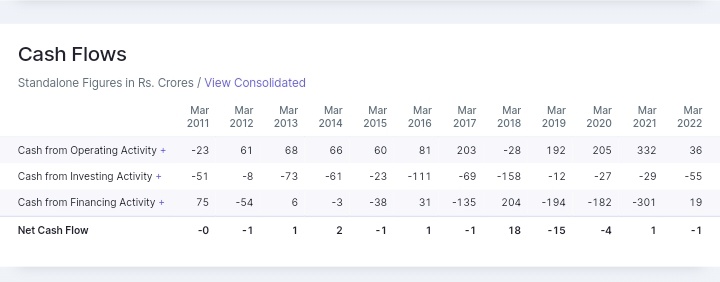

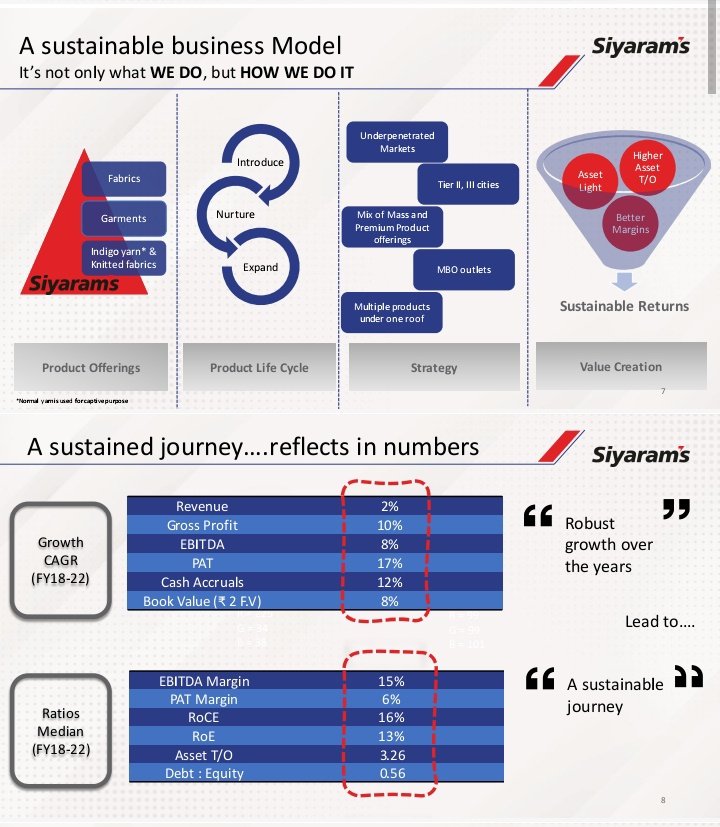

Last 3,5,10 Years CAGR, Accounting Ratios🧾 Cash Flow⚖️

✅Fixed Assets:- Rs 468 Cr

✅CWIP:- 20 Cr

✅Investments:- 70 Cr

✅Promoters Holding:- 67.18%

✅FII Holding:- 2.66%

✅DII Holding:- 6.11%

✅Public Holding:- 24.4%

✅PEG Ratio:- 0.50

✅Piotroski Score:- 6

Last 3,5,10 Years CAGR, Accounting Ratios🧾 Cash Flow⚖️

Statement above.

🎖️Annual Reports Layouts

🎖️Annual Reports Layouts

🎖️Concalls(Part 1)

🎖️Part 2

🎖️Chart Pattern Analysis📉📈 Financial Results Analysis and My Commentry👨💻👨💻

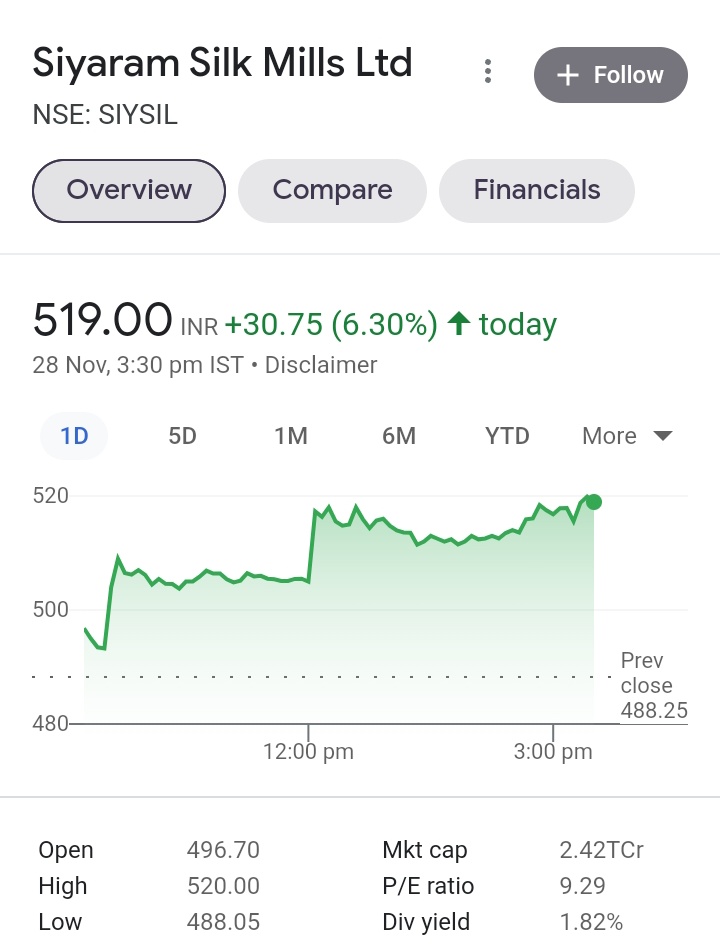

✅CMP of the Stock is at Rs 517.80

✅Currently the stock is trading above all the EMAs and DMAs

✅ Recent highs of the stock was at Rs 568+ levels after that Retest happened in this stock st Rs 486

✅CMP of the Stock is at Rs 517.80

✅Currently the stock is trading above all the EMAs and DMAs

✅ Recent highs of the stock was at Rs 568+ levels after that Retest happened in this stock st Rs 486

✅Stock will show a good Momentum above Rs 532+ but it will be weak if it goes below Rs 470+ on the downside.

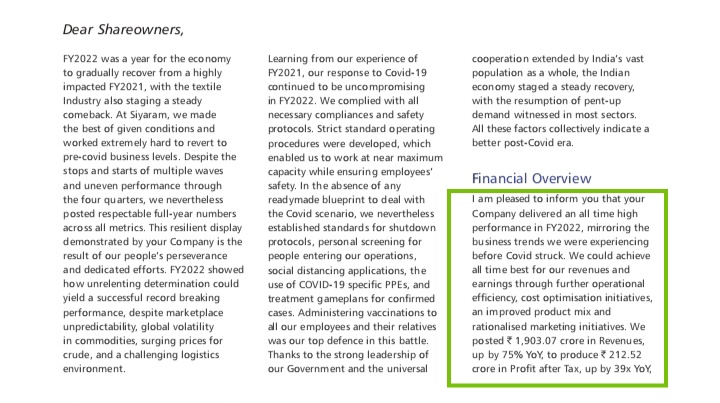

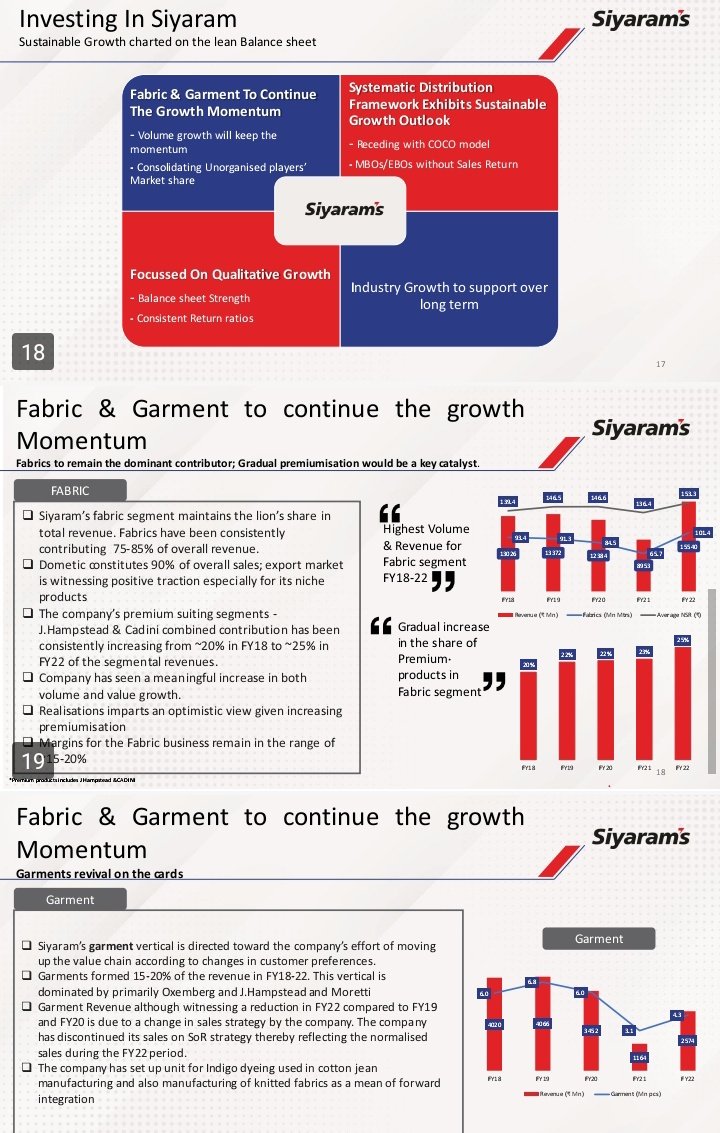

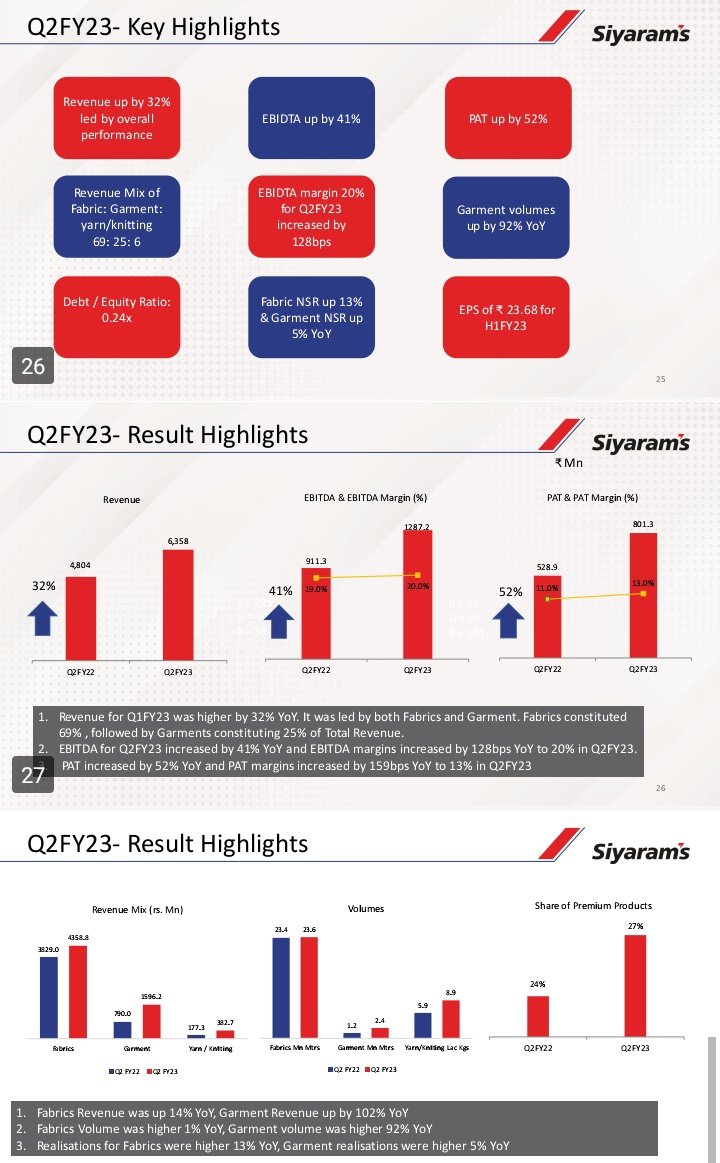

🎖️Financial Results

✅In the present Quarter Siyaram Silk saw its Highest ever Sales in History and also highest ever Net Profits.

✅Sales of Q1+Q2 has been at Rs

🎖️Financial Results

✅In the present Quarter Siyaram Silk saw its Highest ever Sales in History and also highest ever Net Profits.

✅Sales of Q1+Q2 has been at Rs

Rs 1033 Cr(Rs 308 Cr+ Rs 635 Cr). Lets assume that company does maintains Rs 600+ Cr Sales for Q3+Q4 too then on expected lines Siyaram Silk Sales can be at Rs 2233 Cr for FY23

✅Net Profits of Q1+Q2 has been at Rs 112 Cr. Lets assume that Siyaram Silk does pull offs

✅Net Profits of Q1+Q2 has been at Rs 112 Cr. Lets assume that Siyaram Silk does pull offs

Rs 75 Cr Net Profits for Q3 and Q4 too. So, NP of FY23 can be at Rs 262 Cr. As a investor we've to be optimistic with the company in which we're investing and we've to assume that company can do this much amount of Sales and Net Profits.

✅So, if Siyaram Silk is able to do

✅So, if Siyaram Silk is able to do

Rs 2200 Cr Sales and Rs 260+ Cr Net Profits for FY23 it means that it means that Siyaram Silk Forward EPS will be at 56 and it is currently available at a forward PE Ratio of 9.25

✅If Siyaram Silk acheives said Sales and Net Profits target 🎯🎯 then it will be its highest ever

✅If Siyaram Silk acheives said Sales and Net Profits target 🎯🎯 then it will be its highest ever

Sales and Net Profits in a Financial Year.

✅Siyaram Silk was Trading at Rs 799+ levels. This peak came in Q3-Q4 of FY18

✅Mentioning one thing Siyaram Silk Sales of FY18 was only at Rs 1733 Cr and Net Profits was at Rs 112 Cr. It means that at that point of time it was trading

✅Siyaram Silk was Trading at Rs 799+ levels. This peak came in Q3-Q4 of FY18

✅Mentioning one thing Siyaram Silk Sales of FY18 was only at Rs 1733 Cr and Net Profits was at Rs 112 Cr. It means that at that point of time it was trading

at 24-25 PE Ratio.

✅If Siyaram Silk does Business for next quarters efficiently and effectively and acheives the said Revenue Target of Rs 2200 Cr then it means that its Rev will increase by 27%💹💹 from 2018 Levels

✅If Siyaram Silk acheives said Net Profits target

✅If Siyaram Silk does Business for next quarters efficiently and effectively and acheives the said Revenue Target of Rs 2200 Cr then it means that its Rev will increase by 27%💹💹 from 2018 Levels

✅If Siyaram Silk acheives said Net Profits target

Then its Net Profits will increase by 132%💹💹 from 2018 levels and its EPS will increase from Rs 23.81 to Rs 55-56

✅There's a clear valuations Gap in this stock if market rewards it with 15-16 PE Ratio then it can break its ATH. At 15 PE Ratio its price will reach at Rs 825

✅There's a clear valuations Gap in this stock if market rewards it with 15-16 PE Ratio then it can break its ATH. At 15 PE Ratio its price will reach at Rs 825

and at 16 PE Ratio its price will reach at Rs 900+.

So, here my analysis ends about Siyaram Silks👔👔👕👕 I've presented all the facts about this company. Don't jump and Buy due your own analysis properly. I'll not responsible for your profits or loss. If you liked this analysis

So, here my analysis ends about Siyaram Silks👔👔👕👕 I've presented all the facts about this company. Don't jump and Buy due your own analysis properly. I'll not responsible for your profits or loss. If you liked this analysis

Please try to retweet♻️♻️ it. It took me 6 Hours to make this report in details.

Loading suggestions...