The 3 basic needs have changed today from Food, Clothing & Shelter to Fast Food, Clothing & Shelter!

Jokes aside - today we are going to talk about the Quick Service Restaurant (Fast food) space and a company called Devyani International!

Do Retweet for wider reach :)

Jokes aside - today we are going to talk about the Quick Service Restaurant (Fast food) space and a company called Devyani International!

Do Retweet for wider reach :)

1/n

- In 1991 when India opened to the rest of the world, QSR was unknown.

- 1991 reforms paved the way for the rise of QSR in India.

- QSR comes under the organized food services market. It serves food that is cooked quickly and cheaper as compared to fine dining restaurants

- In 1991 when India opened to the rest of the world, QSR was unknown.

- 1991 reforms paved the way for the rise of QSR in India.

- QSR comes under the organized food services market. It serves food that is cooked quickly and cheaper as compared to fine dining restaurants

2/n

- International brands have dominated the QSR market with a 50%+ market share because of investment in increasing geographical presence, brand equity, value focus, menu localization, etc.

- Burger King, McD, KFC, etc have been aggressively investing in opening more stores.

- International brands have dominated the QSR market with a 50%+ market share because of investment in increasing geographical presence, brand equity, value focus, menu localization, etc.

- Burger King, McD, KFC, etc have been aggressively investing in opening more stores.

3/n

- From FY14-FY20, the QSR market grew at a CAGR of 19.1%. It has bounced back well post the covid-19 period. They have also started focusing on high growth and high margins

- With rise of food delivery, takeaway is projected to grow faster and bigger as compared to dine-in

- From FY14-FY20, the QSR market grew at a CAGR of 19.1%. It has bounced back well post the covid-19 period. They have also started focusing on high growth and high margins

- With rise of food delivery, takeaway is projected to grow faster and bigger as compared to dine-in

4/n

- With the ongoing FIFA World Cup and Cricket season, sales are expected to boom in the ongoing quarter

- With price hikes at around high single digits, high inflation won’t have a significant impact on margins

- With the ongoing FIFA World Cup and Cricket season, sales are expected to boom in the ongoing quarter

- With price hikes at around high single digits, high inflation won’t have a significant impact on margins

5/n

- A Return to Office continues and IT companies targeting tier 2 and 3 cities, young people would want to try more fast food from QSR

- Over the past 2-3 years Zomato and Swiggy have expanded to tier 1,2, and 3 cities.

- A Return to Office continues and IT companies targeting tier 2 and 3 cities, young people would want to try more fast food from QSR

- Over the past 2-3 years Zomato and Swiggy have expanded to tier 1,2, and 3 cities.

6/n

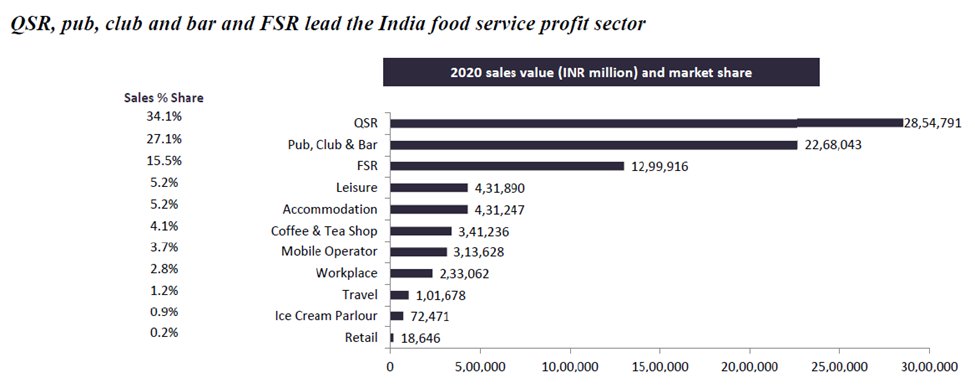

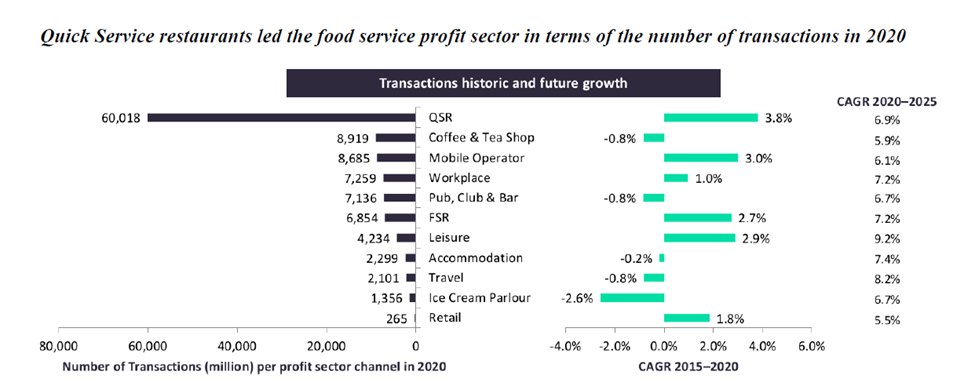

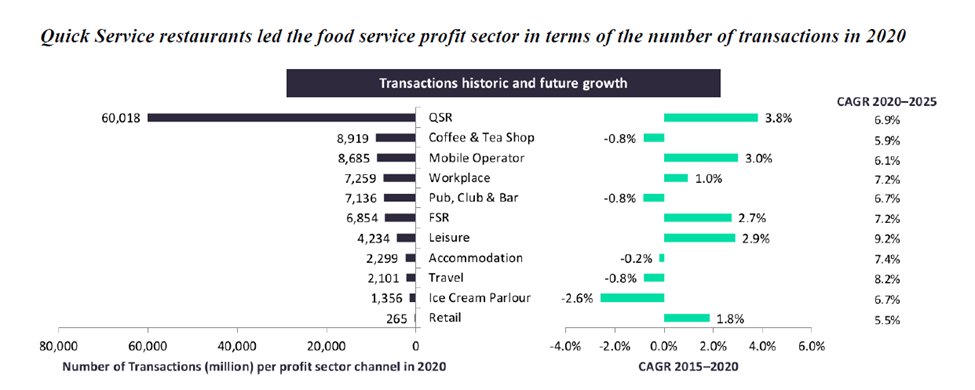

- They are now individually present in over 700+ cities. Due to this, QSR chains have been aggressive in store openings in tier 2 and 3 cities

- In terms of no. of transactions, QSR leads the food service industry.

- They are now individually present in over 700+ cities. Due to this, QSR chains have been aggressive in store openings in tier 2 and 3 cities

- In terms of no. of transactions, QSR leads the food service industry.

7/n

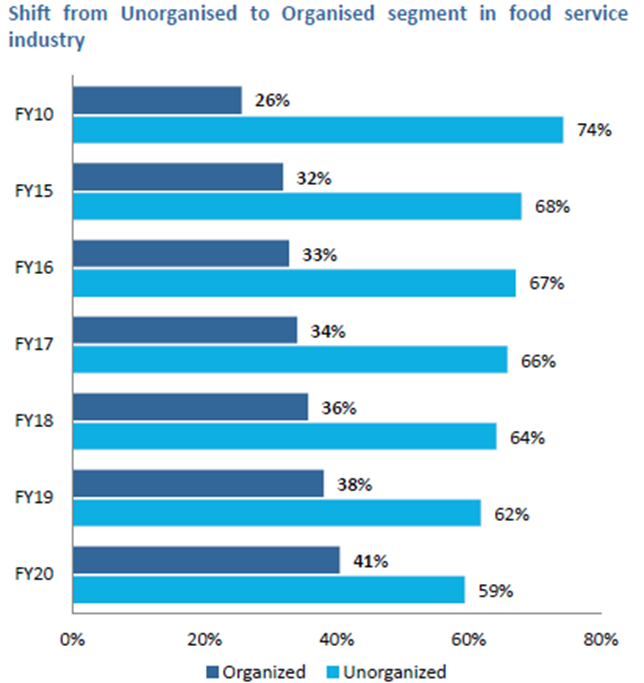

- This is because of short service time, wide availability, and affordability.

- The food service market has steadily shifted from an unorganized to an organized market

- This is because of short service time, wide availability, and affordability.

- The food service market has steadily shifted from an unorganized to an organized market

8/n

Trends -

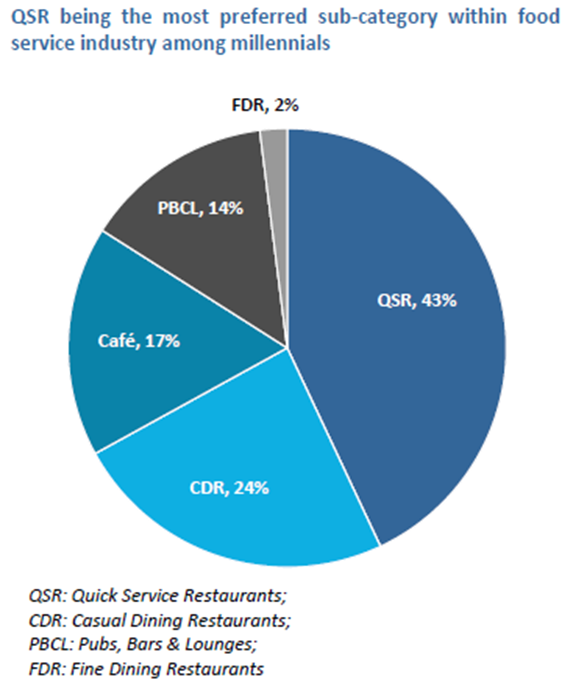

- Millennials prefer global western brands

- As the middle class has expanded over the last decade with a rise in per capita income, it has led to high disposable income and a rise in spending in QSR

Trends -

- Millennials prefer global western brands

- As the middle class has expanded over the last decade with a rise in per capita income, it has led to high disposable income and a rise in spending in QSR

9/n

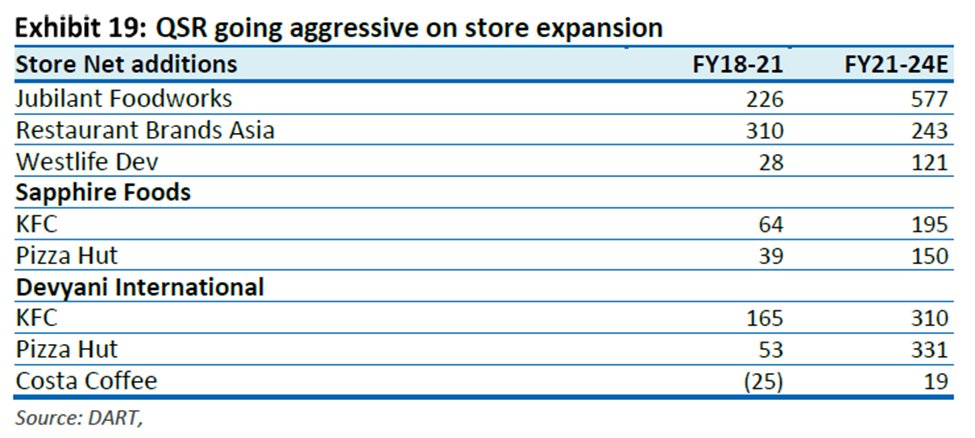

- Due to the large and rising millennial population, most international brands have started expanding their store count aggressively in recent years

- Due to the large and rising millennial population, most international brands have started expanding their store count aggressively in recent years

10/n

The Scope is huge!

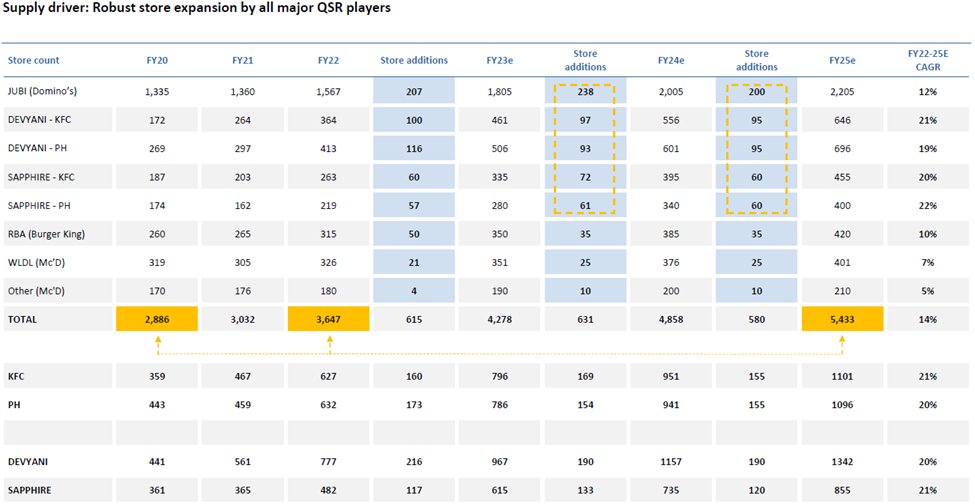

- When it comes to penetration, India still has enough space to be filled for QSR chains to open more stores. - 1 McD store addresses 205000 people in China while 1 McD store addresses 925000 people in India

The Scope is huge!

- When it comes to penetration, India still has enough space to be filled for QSR chains to open more stores. - 1 McD store addresses 205000 people in China while 1 McD store addresses 925000 people in India

11/n

Devyani International Ltd.

-One of India’s largest operators of QSR chain

- It is promoted by RJ Corporation which also owns Varun Beverages.

- In FY22 the company recorded its highest revenues and profits numbers

Devyani International Ltd.

-One of India’s largest operators of QSR chain

- It is promoted by RJ Corporation which also owns Varun Beverages.

- In FY22 the company recorded its highest revenues and profits numbers

12/n

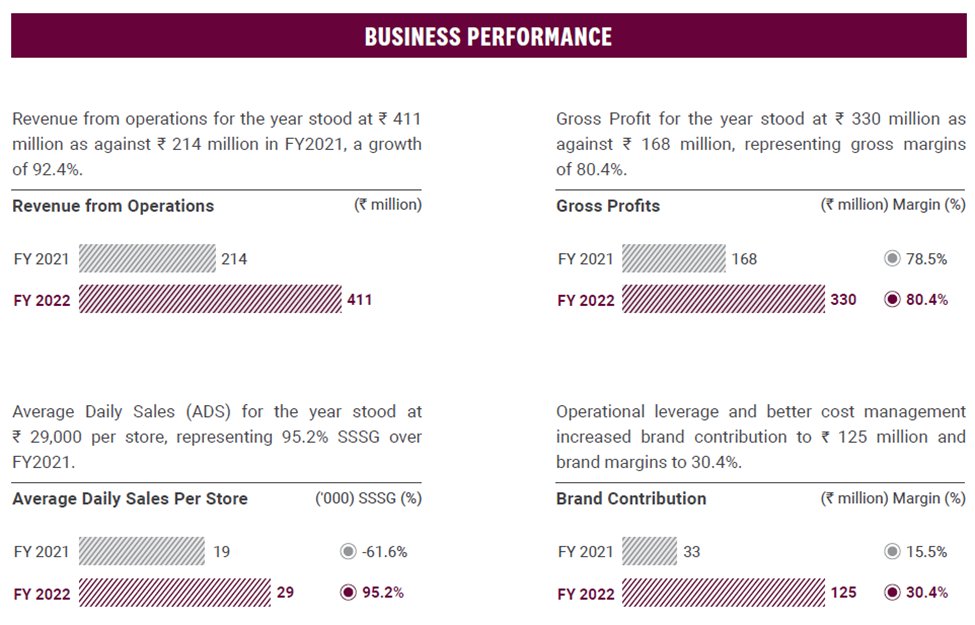

- The YoY revenue growth stood at 84%. The EBITDA increased by 3x. The company is now net debt free on an external basis.

- It is the largest franchisee of Yum Brands in India that owns Pizza Hut, KFC worldwide

- It operates Pizza Hut, KFC in India, Nepal, Nigeria

- The YoY revenue growth stood at 84%. The EBITDA increased by 3x. The company is now net debt free on an external basis.

- It is the largest franchisee of Yum Brands in India that owns Pizza Hut, KFC worldwide

- It operates Pizza Hut, KFC in India, Nepal, Nigeria

13/n

- They also operate Costa Coffee. They also have in-house brands like Vaango and Food Street.

- With increasing internet penetration, a growing middle class, and a millennial population, the company has witnessed good growth

- 5 Year data given below -

- They also operate Costa Coffee. They also have in-house brands like Vaango and Food Street.

- With increasing internet penetration, a growing middle class, and a millennial population, the company has witnessed good growth

- 5 Year data given below -

14/n

KFC business performance -

- Launched new products

- Expanded to 133 cities in 2022 as compared to 97 in 2021.

- The company added 100 new stores.

- outside restaurant sales expanded to 44% from 33% thanks to tech and deliveries

KFC business performance -

- Launched new products

- Expanded to 133 cities in 2022 as compared to 97 in 2021.

- The company added 100 new stores.

- outside restaurant sales expanded to 44% from 33% thanks to tech and deliveries

15/n

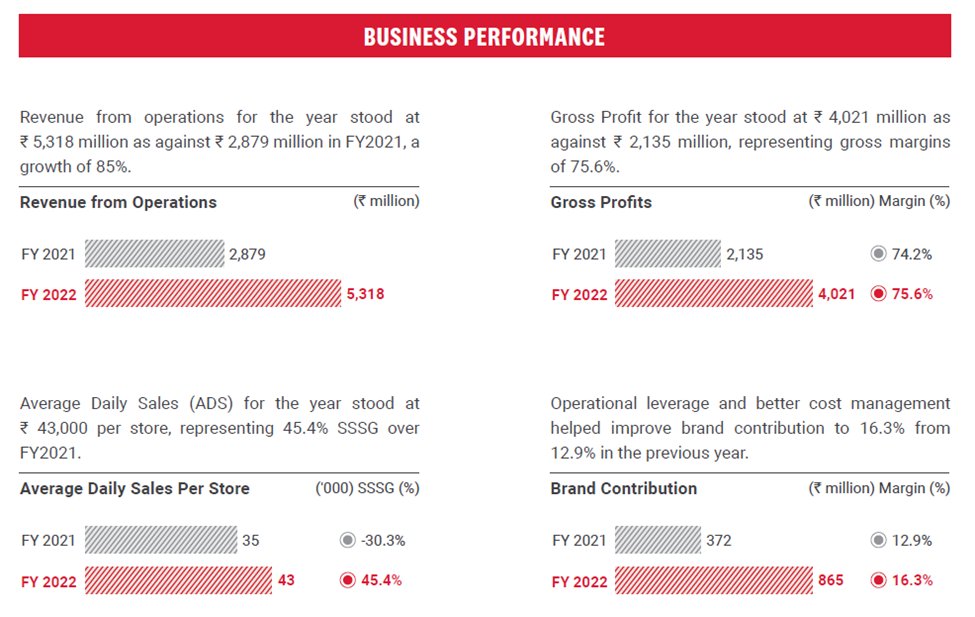

Pizza Hut Business -

- Crossed Rs. 500 crores of sales, 85% YoY growth

- New Variants Launched

- stores count at 413 from 297 in FY21

- 136 cities v/s 100 cities in FY21

- 63% of Pizza Hut sales were off-premise as v/s 57% in FY21.

Pizza Hut Business -

- Crossed Rs. 500 crores of sales, 85% YoY growth

- New Variants Launched

- stores count at 413 from 297 in FY21

- 136 cities v/s 100 cities in FY21

- 63% of Pizza Hut sales were off-premise as v/s 57% in FY21.

16/n

Costa Coffee Business -

- They will grow the brand aggressively

- Gross profit Rs. 33 cr v/s 17 cr in FY21

- Granted development rights for pan-India in a phased manner for the Costa coffee brand.

- 11 new stores, 55 total stores

- Now in 21 cities v/s 17 in FY21

Costa Coffee Business -

- They will grow the brand aggressively

- Gross profit Rs. 33 cr v/s 17 cr in FY21

- Granted development rights for pan-India in a phased manner for the Costa coffee brand.

- 11 new stores, 55 total stores

- Now in 21 cities v/s 17 in FY21

17/n

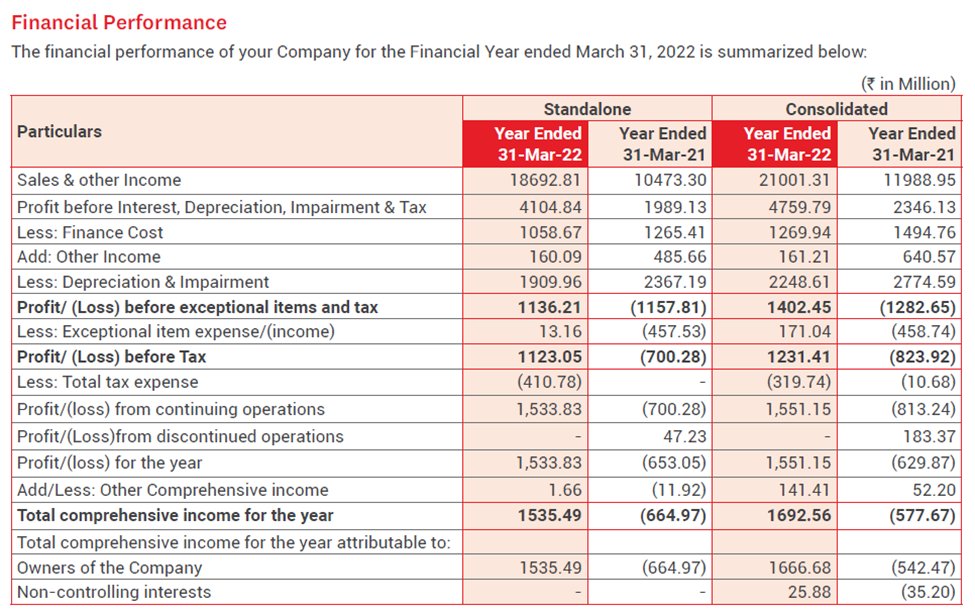

Financials FY22 v/s FY21 -

Strengths of the business -

- Ravi Jaipura, the promoter has 30+ years of experience in managing, establishing, and growing food, beverage, and dairy businesses in South Asia and Africa

- The company has well-diversified portfolio of brands

Financials FY22 v/s FY21 -

Strengths of the business -

- Ravi Jaipura, the promoter has 30+ years of experience in managing, establishing, and growing food, beverage, and dairy businesses in South Asia and Africa

- The company has well-diversified portfolio of brands

18/n

- For healthy operating performance, the company has enhanced store economics and cost efficiency.

- Close ties with Yum along with marketing, technological, and operational skills have enabled it to position itself as a strong player in the QSR space

- For healthy operating performance, the company has enhanced store economics and cost efficiency.

- Close ties with Yum along with marketing, technological, and operational skills have enabled it to position itself as a strong player in the QSR space

19/n

- The company has been aggressive in-store expansion over the past 2-3 years to get into tier 2 and 3 cities to address the growing urban and middle-class population and also address the millennials

- They expanded to nearly 50 cities in India in FY22.

- The company has been aggressive in-store expansion over the past 2-3 years to get into tier 2 and 3 cities to address the growing urban and middle-class population and also address the millennials

- They expanded to nearly 50 cities in India in FY22.

20/n

- Brand contribution margin which is a key metric in QSR improved to 19.9% in FY22 vs 14.4% YoY.

- Due to this, pre-INDAS EBITDA jumped to Rs. 299.5 crores which are their highest ever

- Net Profit stood at Rs. 155.1 Cr v/s a loss in the previous year

- Brand contribution margin which is a key metric in QSR improved to 19.9% in FY22 vs 14.4% YoY.

- Due to this, pre-INDAS EBITDA jumped to Rs. 299.5 crores which are their highest ever

- Net Profit stood at Rs. 155.1 Cr v/s a loss in the previous year

21/n

Outlook -

- Festive demand this year would have driven sales.

- There surely has been a lot of revenge buying across sectors.

- Inflation has cooled down input costs and will positively contribute to margins

- The company has plans to further increase prices as well

Outlook -

- Festive demand this year would have driven sales.

- There surely has been a lot of revenge buying across sectors.

- Inflation has cooled down input costs and will positively contribute to margins

- The company has plans to further increase prices as well

22/n

- In Q2FY23, EBITDA (Pre IndAS) stood at 112.5 crores and margins stood at 15.1%. (42% growth YoY)

- Devyani will benefit from the growing young population in urban cities + return to office + shift to tier 1 or 2 cities

- In Q2FY23, EBITDA (Pre IndAS) stood at 112.5 crores and margins stood at 15.1%. (42% growth YoY)

- Devyani will benefit from the growing young population in urban cities + return to office + shift to tier 1 or 2 cities

23/n

- Due to fast serving, and cheap prices as compared to fine dining, QSR is preferred for food.

- With low availability, there is room for more store expansion in both existing cities and the addition of new cities

References -

- Due to fast serving, and cheap prices as compared to fine dining, QSR is preferred for food.

- With low availability, there is room for more store expansion in both existing cities and the addition of new cities

References -

24/n

End of thread! Thanks for reading :)

Please follow us at @compcircle to make sure you never miss a thread.

Stay tuned for more.

End of thread! Thanks for reading :)

Please follow us at @compcircle to make sure you never miss a thread.

Stay tuned for more.

25/n

Please note this thread is not a recommendation for the sector or the stock.

It is purely education, please do your own due diligence before acting upon any of the information contained here.

Thank you.

Please note this thread is not a recommendation for the sector or the stock.

It is purely education, please do your own due diligence before acting upon any of the information contained here.

Thank you.

Loading suggestions...