From an overzealous hurry to raise fast to a soft signal of "not" cutting. This is how fast CBs turn.

Some will keep waiting for a Fed pivot.

With a 2000 point rally on Nifty from recent lows, this is probably moving to Small & Midcap outperformance and Largecap consolidation

Some will keep waiting for a Fed pivot.

With a 2000 point rally on Nifty from recent lows, this is probably moving to Small & Midcap outperformance and Largecap consolidation

Few people care to actaully read the statement and most just read the headlines. Here is the link to the actual transcript if you haven't watched it live: federalreserve.gov

Key excerpts from yesterday's speech in following tweets:

Key excerpts from yesterday's speech in following tweets:

Starts by acknowleding that inflation is high

"The report must begin by acknowledging the reality that inflation remains far too high. My colleagues and I are acutely aware that high inflation is imposing significant hardship..."

"The report must begin by acknowledging the reality that inflation remains far too high. My colleagues and I are acutely aware that high inflation is imposing significant hardship..."

"We currently estimate that 12M PCE inflation through Oct ran at 6.0%...Oct inflation data received so far showed a welcome surprise to the downside, these are a single month's data...It will take substantially more evidence to give comfort that inflation is actually declining"

"...core inflation often gives a more accurate indicator of where overall inflation is headed. Twelve-month core PCE inflation stands at 5.0 percent in our October estimate, approximately where it stood last December when policy tightening was in its early stages."

"we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent...It seems to me likely that the ultimate level of rates will need to be somewhat higher than thought at the time of the September meeting...we have more ground to cover"

"We are tightening the stance of policy in order to slow growth in aggregate demand...should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth"

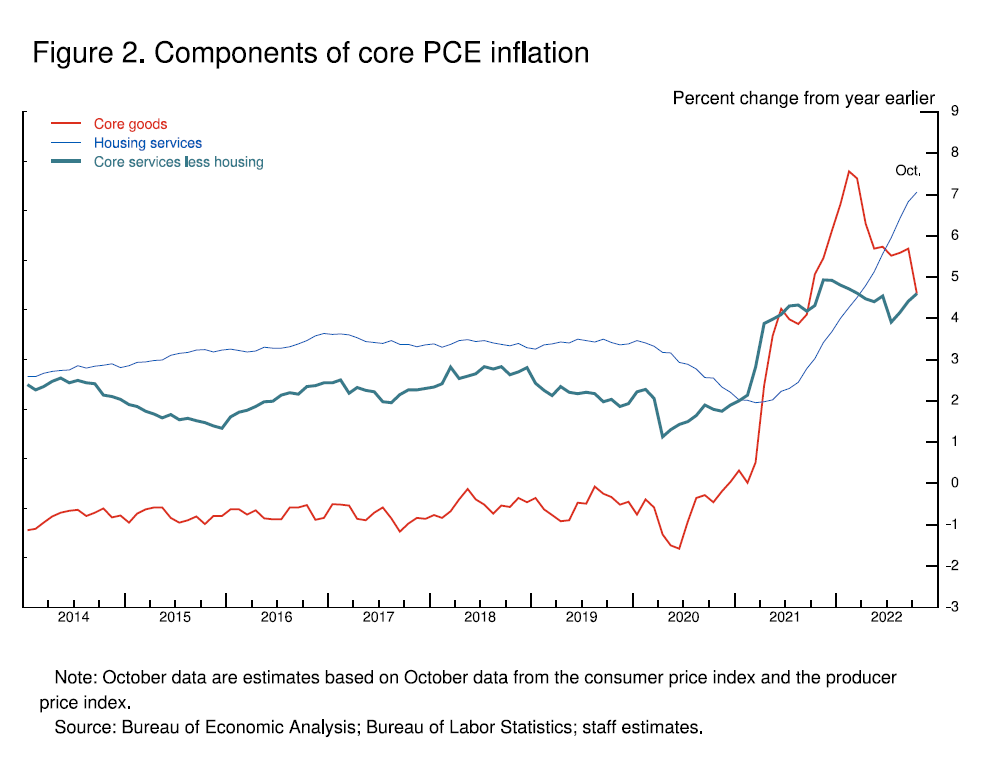

"To assess what it will take to get inflation down, it is useful to break core inflation into three component categories: core goods inflation, housing services inflation, and inflation in core services other than housing"

"Early in the pandemic, goods prices began rising rapidly, as abnormally strong demand was met by pandemic-hampered supply...12m core goods inflation remains elevated at 4.6%, it has fallen nearly 3% from earlier..goods prices should begin to exert downward pressure on inflation"

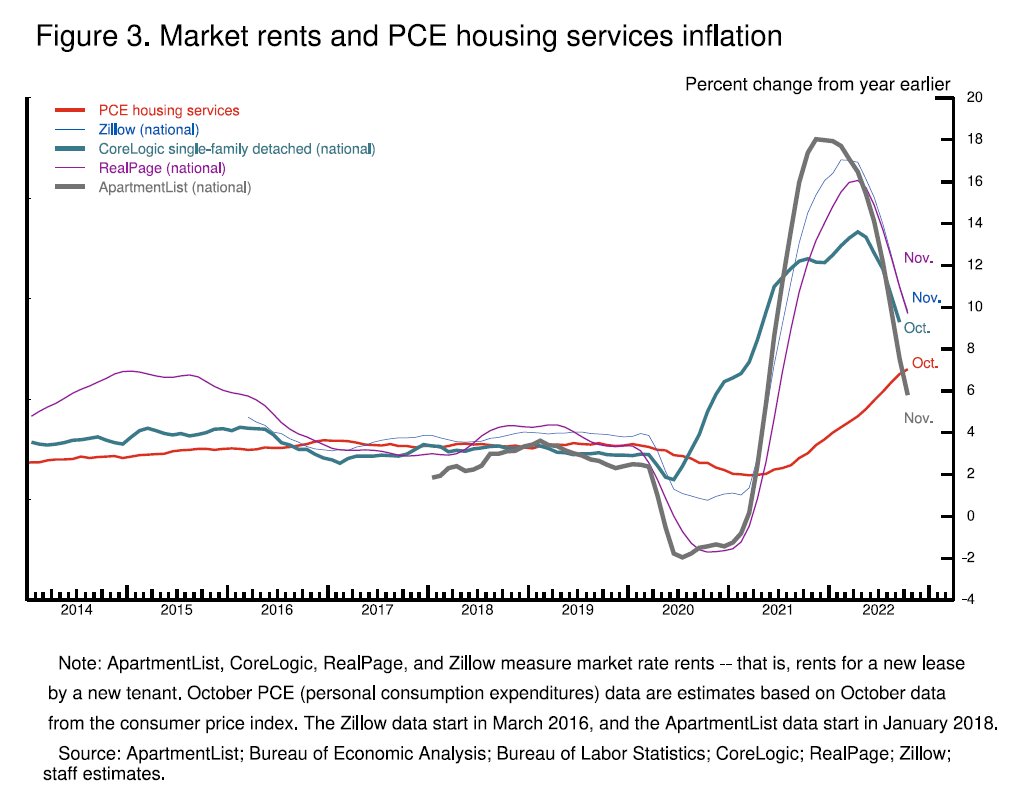

"Housing inflation tends to lag other prices around inflation turning points, however, because of the slow rate at which the stock of rental leases turns over. The market rate on new leases is a timelier indicator of where overall housing inflation will go over the next year..."

"Measures of 12m inflation in new leases rose to nearly 20% during the pandemic but have been falling sharply ...overall housing services inflation has continued to rise as existing leases turn over and jump in price to catch up with the higher level of rents for new leases."

"This is likely to continue well into next year. But as long as new lease inflation keeps falling, we would expect housing services inflation to begin falling sometime next year..."

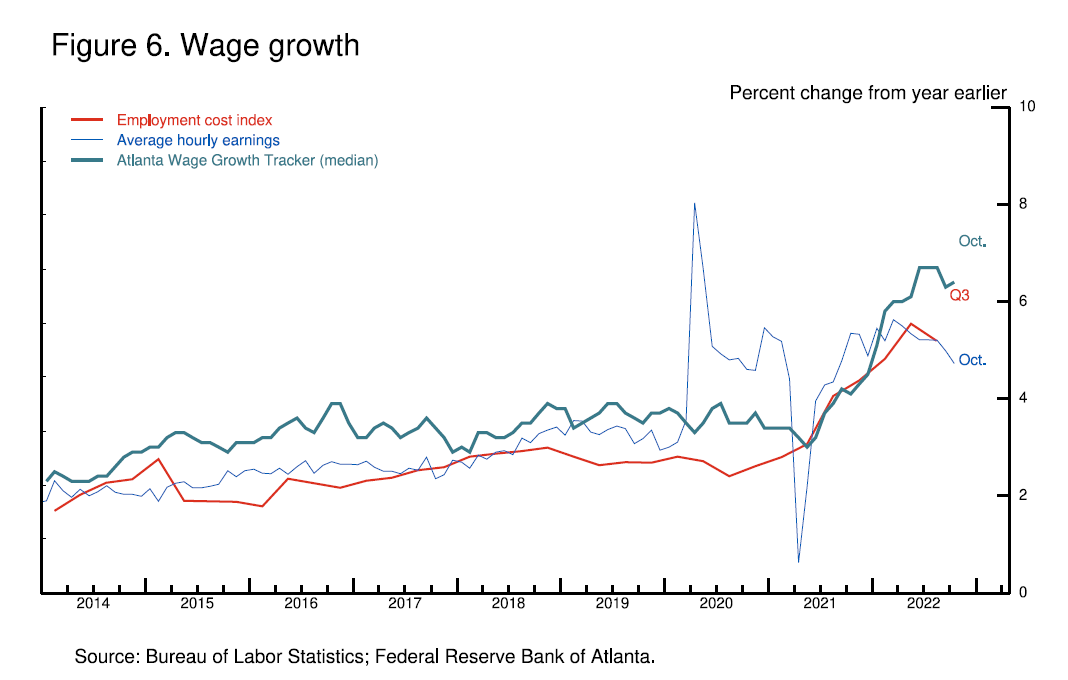

"Core services other than housing...is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation."

"another condition we are looking for is the restoration of balance between supply and demand in the labor market... job growth remains far in excess of the pace needed to accommodate population growth... Job openings have fallen by about 1.5mn this year but remain higher..."

"Wage growth, too, shows only tentative signs of returning to balance...strong wage growth is a good thing. But for wage growth to be sustainable, it needs to be consistent with 2 percent inflation."

My conclusion:

1. Core goods inflation is moderating

2. Housing inflation is peaking, gradaully. Will fall in 2023.

3. Core services inflation is dependent on employment and wages, thats why Fed wants to slowdown the economy.

Means - worst part of inflation is over.

1. Core goods inflation is moderating

2. Housing inflation is peaking, gradaully. Will fall in 2023.

3. Core services inflation is dependent on employment and wages, thats why Fed wants to slowdown the economy.

Means - worst part of inflation is over.

What did Powell say about policy:

" it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting."

" it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting."

Loading suggestions...