1) What’s next for tech, FAANG, and Silicon Valley?

Revisit the spectacular shale boom-bust cycle. There are more similarities than you think.

Both were profitless technological revolutions funded by cheap capital and carrying enormous benefits to society.

Pay attention 🧵

Revisit the spectacular shale boom-bust cycle. There are more similarities than you think.

Both were profitless technological revolutions funded by cheap capital and carrying enormous benefits to society.

Pay attention 🧵

2) The innovations of horizontal drilling and hydraulic fracturing made it possible to extract shale oil.

Neither technology was entirely new, but they were both improved upon and combined to increase the commercial viability of shale gas.

Neither technology was entirely new, but they were both improved upon and combined to increase the commercial viability of shale gas.

3) The Bakken and Permian were transformed into the Silicon Valley of the energy sector: hubs of creative activity where engineers collaborated and competed to advance the frontiers of technology.

4) Between 2010 and 2015, US oil production increased from 5.4 million barrels per day to 9.4 million, closing on the all-time peak of just over 10 million set in 1970.

Texas produced more oil than Brazil, Venezuela, Nigeria, Mexico and Kuwait.

Texas produced more oil than Brazil, Venezuela, Nigeria, Mexico and Kuwait.

5) Two factors drove the US shale boom.

First, oil prices averaged above $90 a barrel from 2011 to 2014, which was enough to support the high infrastructure and drilling costs.

Second, low interest rates gave banks and private equity investors a strong incentive to lend.

First, oil prices averaged above $90 a barrel from 2011 to 2014, which was enough to support the high infrastructure and drilling costs.

Second, low interest rates gave banks and private equity investors a strong incentive to lend.

6) Shale producers blew through every penny they made and took out further loans to drill new wells.

The revolution was profitless. The only thing keeping them afloat was a steady inflow of capital.

The revolution was profitless. The only thing keeping them afloat was a steady inflow of capital.

7) When oil prices crashed in mid-2014 shale producers defied expectations and kept drilling.

Lenders and stock investors rewarded companies for high volumes.

Executive pay that was linked to oil production rather than profits led to a drill-at-any-cost mentality.

Lenders and stock investors rewarded companies for high volumes.

Executive pay that was linked to oil production rather than profits led to a drill-at-any-cost mentality.

8) The shale industry was pumping more oil than anyone needed.

Consumers won, with the retail price of gasoline plummeting.

Consumers won, with the retail price of gasoline plummeting.

9) Eventually, low prices caught up with the industry.

Banks used oil reserves as collateral, and as oil prices fell, so did the value of the collateral.

Many teams stopped drilling. Nearly half of new wells were sitting idle.

Banks used oil reserves as collateral, and as oil prices fell, so did the value of the collateral.

Many teams stopped drilling. Nearly half of new wells were sitting idle.

10) In February 2016, the price of crude oil dropped to $26 a barrel. Shale companies laid off workers and cut spending.

About 30 percent of the oil and gas industry’s debt was trading at distressed levels. Some seventy companies with $56 billion in debt declared bankruptcy.

About 30 percent of the oil and gas industry’s debt was trading at distressed levels. Some seventy companies with $56 billion in debt declared bankruptcy.

11) By nearly all accounts, the shale boom had gone bust.

US oil production was down a million barrels a day by mid-2016.

All told, more than 170,000 oil and gas jobs disappeared during the downturn.

US oil production was down a million barrels a day by mid-2016.

All told, more than 170,000 oil and gas jobs disappeared during the downturn.

12) After growing at the fastest pace for years, North Dakota’s growth fell to 0.15 percent in 2015—16.

In large segments of the US economy, by contrast, it was business as usual.

Anyone who didn’t work in the energy industry could be forgiven for not noticing it at all.

In large segments of the US economy, by contrast, it was business as usual.

Anyone who didn’t work in the energy industry could be forgiven for not noticing it at all.

13) From 2010 to 2020, large publicly traded US oil producers poured a total of $1.2 trillion into drilling, mostly in fracking.

But they made only $819 billion in cash from their oil operations, a combined loss of $361 billion.

But they made only $819 billion in cash from their oil operations, a combined loss of $361 billion.

14) The total return to shareholders in large-cap energy stocks from 2010 to 2020 was effectively zero!

15) Now onto tech.

According to Crunchbase, nearly $2.5 trillion was invested in venture capital deals worldwide between 2010 and 2021, with much of that coming just in the past few years.

According to Crunchbase, nearly $2.5 trillion was invested in venture capital deals worldwide between 2010 and 2021, with much of that coming just in the past few years.

16) A decade-long run of low interest rates enabled investors to extend their horizons and take bigger risks on high-growth start-ups.

Blitzscaling promised cash-guzzling startups with flimsy business models a “lightning-fast path to building massively valuable companies.”

Blitzscaling promised cash-guzzling startups with flimsy business models a “lightning-fast path to building massively valuable companies.”

17) The VC industry was willing to subsidize years of massive losses in pursuit of market dominance.

A focus on making money would entail sacrificing too much market share.

A constant supply of new money at ever-higher valuations kept the Silicon Valley boom chugging along.

A focus on making money would entail sacrificing too much market share.

A constant supply of new money at ever-higher valuations kept the Silicon Valley boom chugging along.

18) There are more than six hundred unicorns in the US today, private startups valued at more than $1 billion, up from just thirty a decade ago.

More unicorns were minted in 2021 than the previous five years combined.

But now the game is up.

More unicorns were minted in 2021 than the previous five years combined.

But now the game is up.

19) Investors are reconsidering the wisdom of funding business models that weaponize capital to subsidize customer acquisition.

Founders are realizing that they can’t continue to operate with negative unit economics.

Founders are realizing that they can’t continue to operate with negative unit economics.

20) According to @bgurley, “the unlearning process could be painful, surprising and unsettling to many.”

Amazon enjoyed positive free cash flow in its first quarter as a public company in 1997. Conversely many startups aren’t there yet—and won’t be for many years.

Amazon enjoyed positive free cash flow in its first quarter as a public company in 1997. Conversely many startups aren’t there yet—and won’t be for many years.

21) Sequencing matters when boom turns to bust.

I identify three stages—stocks down (the crash), stocks up (capital discipline), stocks down (still struggling to generate FCF).

We are now entering stage 2.

I identify three stages—stocks down (the crash), stocks up (capital discipline), stocks down (still struggling to generate FCF).

We are now entering stage 2.

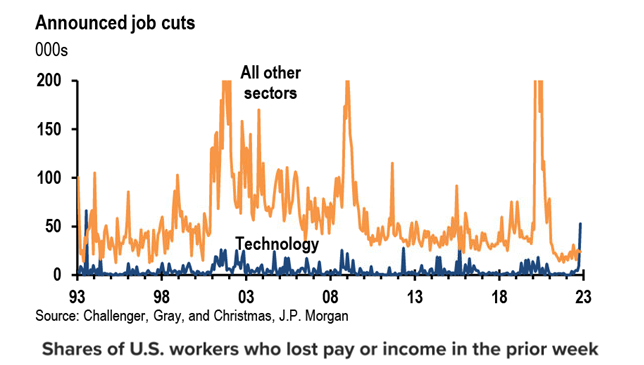

22) @altcap put it best: “It is a poorly kept secret in Silicon Valley that companies ranging from Google to Meta to Twitter to Uber could achieve similar levels of revenue with far fewer people."

23) @elonmusk is showing how to combat corporate bloat. He emailed an ultimatum: commit to “working long hours at high intensity” or resign.

For all the controversy he has caused, he is illuminating the way forward.

For all the controversy he has caused, he is illuminating the way forward.

25) We predicted a localized downturn in Silicon Valley. Much like the Texas shale bust in 2015/16.

San Francisco will see layoffs, falling salaries, worthless stock options, declining housing prices, and despair that lasts up to five years.

Rest of America keeps booming.

San Francisco will see layoffs, falling salaries, worthless stock options, declining housing prices, and despair that lasts up to five years.

Rest of America keeps booming.

25) How do stocks perform through the stages?

The S&P 500 Energy Sector ETF ($XLE) peaked in June 2014 and fell 51 percent by January 2016; rallied 60 percent by October 2018 as companies laid off workers and cut spending; before dropping another 71 percent through March 2020.

The S&P 500 Energy Sector ETF ($XLE) peaked in June 2014 and fell 51 percent by January 2016; rallied 60 percent by October 2018 as companies laid off workers and cut spending; before dropping another 71 percent through March 2020.

26) FANG stocks—$META, $AMZN, $NFLX, and $GOOG—are down 54 percent from the peak, on average.

While they will rally now in the second phase (capital discipline), I suspect the total return for FANG stocks will be zero from 2018 to 2028, much like it was for the energy sector.

While they will rally now in the second phase (capital discipline), I suspect the total return for FANG stocks will be zero from 2018 to 2028, much like it was for the energy sector.

27) The more speculative S&P 500 Oil & Gas Exploration and Production ETF ($XOP) plunged 73% from mid-2014 to early-2016; followed by a 10% gain in twelve months; and another 83% decline to the March 2020 low.

The road to generating meaningful FCF is a long and difficult one.

The road to generating meaningful FCF is a long and difficult one.

28) The analogy I draw is with Cathie Wood's Ark Innovation Fund ($ARKK). Since February 2021 it has declined 79 percent. In this second stage, I anticipate ARKK will double in value to around $70 a share before declining 75 percent to its final low later in the decade.

29) Do you understand what this means?

Only in an environment where the $SPY is up at least 25 percent can ARKK be up 100 percent. That would put the S&P 500 at a new record high above 5,000.

Are you ready?

Only in an environment where the $SPY is up at least 25 percent can ARKK be up 100 percent. That would put the S&P 500 at a new record high above 5,000.

Are you ready?

30) You can follow me @jsmian to meaningfully inform your investing (and maybe even your inner life).

You can learn more about our community stray-reflections.com

As Rumi said: “Be with those who help your being.”

You can learn more about our community stray-reflections.com

As Rumi said: “Be with those who help your being.”

Loading suggestions...