Technology

Business

Health

Finance

Investing

Market Analysis

Investment

manufacturing

Chemicals

Crop Protection

(1/17)

SCIL is a wholly owned subsidiary of Japanese chemical major, Sumitomo Chemical Company Limited Japan (SCCL), engaged in the manufacturing & marketing of crop protection formulations based on the active ingredients procured from SCCL and third parties.

SCIL is a wholly owned subsidiary of Japanese chemical major, Sumitomo Chemical Company Limited Japan (SCCL), engaged in the manufacturing & marketing of crop protection formulations based on the active ingredients procured from SCCL and third parties.

(2/17)

About SCCL:

SCCL is a leading Japanese research driven diversified chemical company listed on the Tokyo Stock Exchange with consolidated sales revenue of more than US$ 22.5 bn.

It holds 12,600+ Patents of which ~34% are in Health & Crop Science

About SCCL:

SCCL is a leading Japanese research driven diversified chemical company listed on the Tokyo Stock Exchange with consolidated sales revenue of more than US$ 22.5 bn.

It holds 12,600+ Patents of which ~34% are in Health & Crop Science

(3/17)

SCIL journey so far:

• 2000: SCIL incorporated in India

• 2001: Manufacturing JV with New

Chemi

• 2005: Acquired EHD (HHI)

unit from Bayer Vapi

• 2010: Started Animal Nutrition

• 2012: Acquisition of New Chemi

• 2016: Acquisition of Excel

Crop Care

SCIL journey so far:

• 2000: SCIL incorporated in India

• 2001: Manufacturing JV with New

Chemi

• 2005: Acquired EHD (HHI)

unit from Bayer Vapi

• 2010: Started Animal Nutrition

• 2012: Acquisition of New Chemi

• 2016: Acquisition of Excel

Crop Care

(4/17)

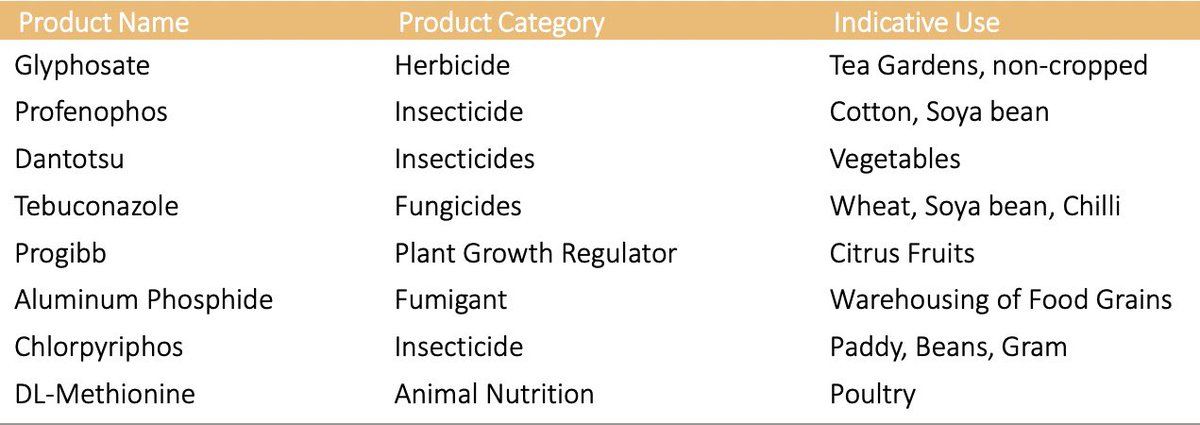

Company Overview:

• 5 manufacturing facility

• 200+ Brands, 700+ SKUs

• 25+ Patents

• 200+ Registrations

• 16000+ Direct Distributors

• Key Product list given below:

Company Overview:

• 5 manufacturing facility

• 200+ Brands, 700+ SKUs

• 25+ Patents

• 200+ Registrations

• 16000+ Direct Distributors

• Key Product list given below:

(5/17)

• Company is focusing more on Herbicides, PGR, Bio-rational products as they are more, stable and high profitable segments

• Top 10 products contributes less than 45% of Total Revenue

• No product / molecule contributes more than 16% of Total Revenue

• Company is focusing more on Herbicides, PGR, Bio-rational products as they are more, stable and high profitable segments

• Top 10 products contributes less than 45% of Total Revenue

• No product / molecule contributes more than 16% of Total Revenue

(6/17)

Capex Plans:

• Additional Capex ₹120 crore

over 2 years for 5 products

• Revenue potential of these 5 products on the above capex is ₹200 crore to ₹250 crore p.a.

• Signed and registered agreements to buy 2 additional land parcels

Capex Plans:

• Additional Capex ₹120 crore

over 2 years for 5 products

• Revenue potential of these 5 products on the above capex is ₹200 crore to ₹250 crore p.a.

• Signed and registered agreements to buy 2 additional land parcels

(7/17)

Growth Strategies:

• Focus on R&D to improve production processes,

enhancing yields and efficiency

• Capacity Expansion: • Invest ~15% of consolidated EBITDA every year for upgradation of

manufacturing facilities

• Expand Export Business

Growth Strategies:

• Focus on R&D to improve production processes,

enhancing yields and efficiency

• Capacity Expansion: • Invest ~15% of consolidated EBITDA every year for upgradation of

manufacturing facilities

• Expand Export Business

(8/17)

Key strengths :

• Established presence in the crop protection segment:

A diversified product portfolio & well-balanced technical and formulations manufacturing capabilities & access to SCCL’s products has helped SCIL establish itself as one of major players.

Key strengths :

• Established presence in the crop protection segment:

A diversified product portfolio & well-balanced technical and formulations manufacturing capabilities & access to SCCL’s products has helped SCIL establish itself as one of major players.

(9/17)

• Product portfolio is well diversified with company’s agro chemical products covering multiple crop segments in both Kharif and Rabi season. With over 13,000 distributors, SCIL’s distribution network covers close to 85% of mainland India, providing geographic diversity.

• Product portfolio is well diversified with company’s agro chemical products covering multiple crop segments in both Kharif and Rabi season. With over 13,000 distributors, SCIL’s distribution network covers close to 85% of mainland India, providing geographic diversity.

(10/17)

• Financial risk profile:

Financial risk profile is healthy, marked by comfortable gearing. Tangible networth was healthy at ₹2,217 crore, & debt has been ~nil. Company’s focus on healthy cash generation, should lead to further improvement in financial risk profile.

• Financial risk profile:

Financial risk profile is healthy, marked by comfortable gearing. Tangible networth was healthy at ₹2,217 crore, & debt has been ~nil. Company’s focus on healthy cash generation, should lead to further improvement in financial risk profile.

(11/17)

Liquidity:

SCIL enjoys strong liquidity. Expected annual cash accruals of ~₹400 cr in FY23 & cash and cash equivalents of ~₹599 crore as on Mar 31, 2022 should comfortably cover moderate capex plan of Rs. 40-50 crore per annum for regular maintenance & up gradation.

Liquidity:

SCIL enjoys strong liquidity. Expected annual cash accruals of ~₹400 cr in FY23 & cash and cash equivalents of ~₹599 crore as on Mar 31, 2022 should comfortably cover moderate capex plan of Rs. 40-50 crore per annum for regular maintenance & up gradation.

(12/17)

Weaknesses:

Large working capital requirement:

The agrochemical industry is characterised by working capital-intensive operations, due to large inventory requirement, seasonality in demand, and payment is realised post-harvest, thus resulting in large receivables.

Weaknesses:

Large working capital requirement:

The agrochemical industry is characterised by working capital-intensive operations, due to large inventory requirement, seasonality in demand, and payment is realised post-harvest, thus resulting in large receivables.

(13/17)

• Susceptibility to risks inherent in the agrochemicals sector:

Change in regulatory requirements, such as export and import policies, and environmental and safety requirements in countries where the company has significant exposure, could weaken growth prospects.

• Susceptibility to risks inherent in the agrochemicals sector:

Change in regulatory requirements, such as export and import policies, and environmental and safety requirements in countries where the company has significant exposure, could weaken growth prospects.

(14/17)

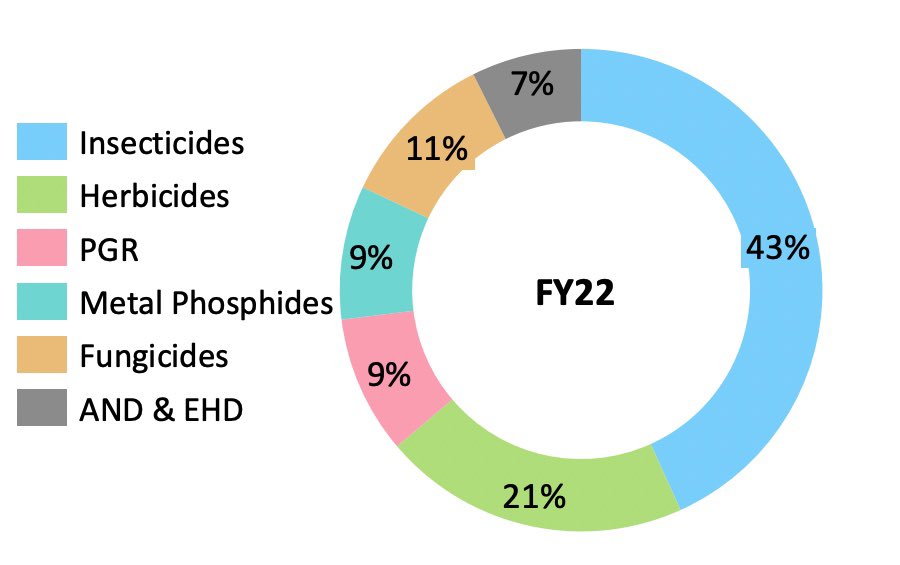

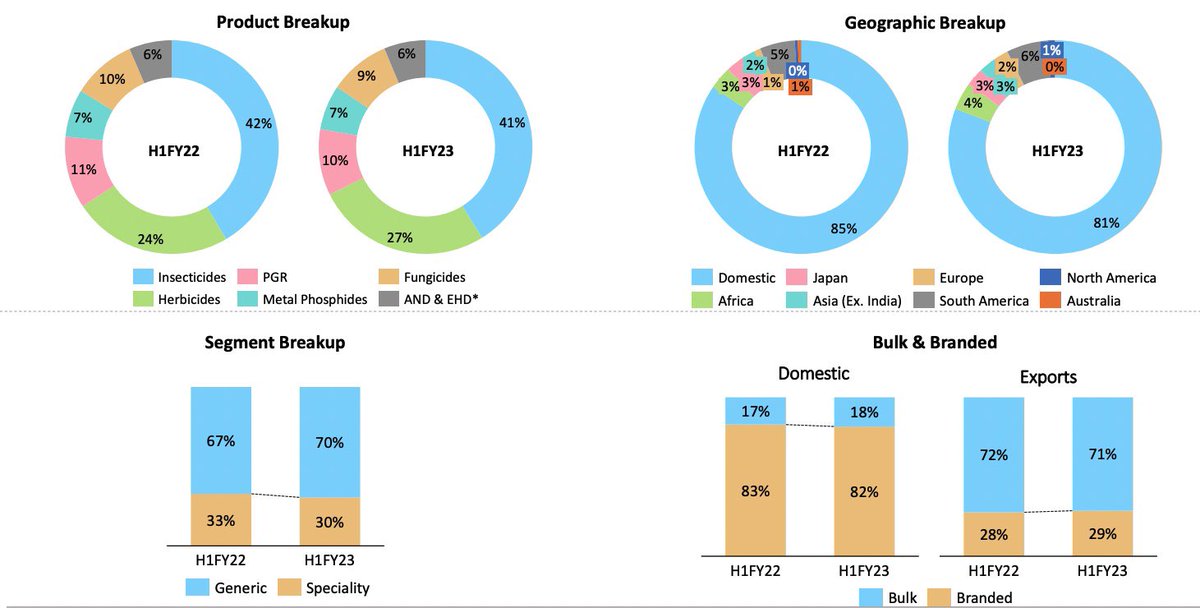

Revenue Breakup:

Revenue Breakup:

(15/17)

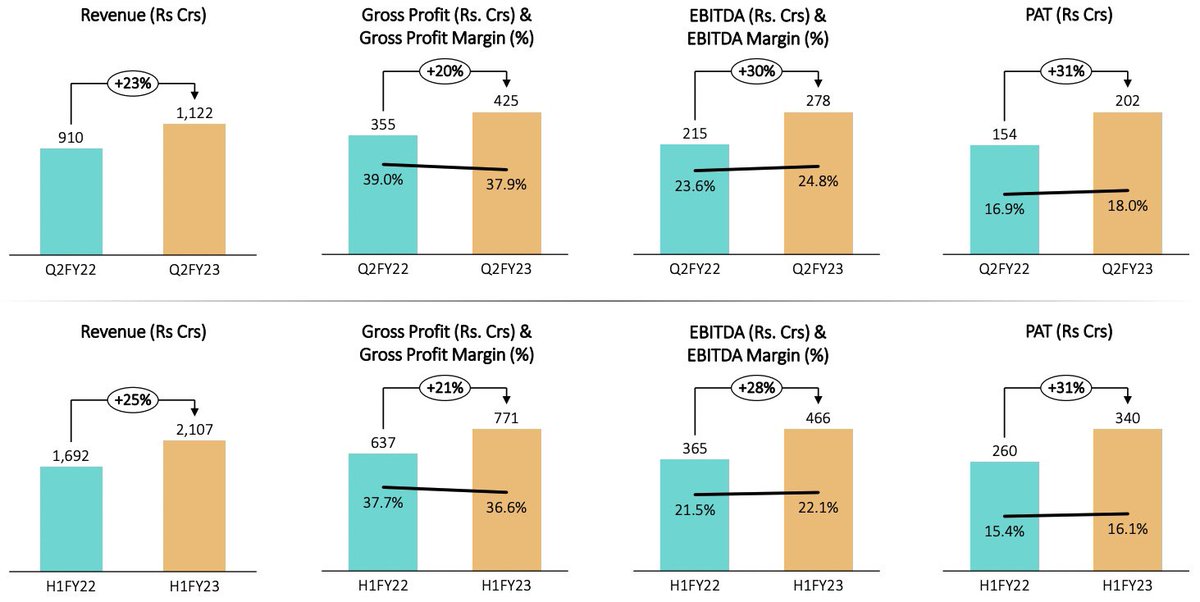

Key Highlights of Q2:

• 3 insecticide, 1 fungicide, 1 metal phosphide and 3 PGR products launched during H1FY23

• There has been an uptick in exports, & recent capacity expansion investments should help

sustain this trend

• Company expects a good Rabi season

Key Highlights of Q2:

• 3 insecticide, 1 fungicide, 1 metal phosphide and 3 PGR products launched during H1FY23

• There has been an uptick in exports, & recent capacity expansion investments should help

sustain this trend

• Company expects a good Rabi season

(16/17)

Key Numbers and Ratios:

• Market Cap: ₹23,949cr

• Stock P/E: 46.7 vs Ind P/E: 24.77

• RoCE: 33.7%

• RoE: 25.1%

• PEG: 0.98

• Sales 3 year CAGR: 11.3%

• Price to Sales: 6.88

• NPM Last year: 14.2%

• OPM Q2FY23: 25%

• D/E: 0.01

Key Numbers and Ratios:

• Market Cap: ₹23,949cr

• Stock P/E: 46.7 vs Ind P/E: 24.77

• RoCE: 33.7%

• RoE: 25.1%

• PEG: 0.98

• Sales 3 year CAGR: 11.3%

• Price to Sales: 6.88

• NPM Last year: 14.2%

• OPM Q2FY23: 25%

• D/E: 0.01

(17/17)

SCIL’s business should see improvement over the medium term, supported by the healthy demand for crop-protection products, and Optimistic Rabi Season prospect with improving exports.

Which is your favourite stock in this sector?

@caniravkaria @kuttrapali26 @chartmojo

SCIL’s business should see improvement over the medium term, supported by the healthy demand for crop-protection products, and Optimistic Rabi Season prospect with improving exports.

Which is your favourite stock in this sector?

@caniravkaria @kuttrapali26 @chartmojo

Loading suggestions...