Lumax Auto Technologies Ltd. Analysis!!

#LumaxAutoTechnologies

A detailed thread 🪡🧵

#StockMarket #Investing

#LumaxAutoTechnologies

A detailed thread 🪡🧵

#StockMarket #Investing

About -

Founded in the year 1981, Lumax Auto Technologies is a part of D.K Jain Group. The company commenced its operations with manufacture of 2-wheeler lighting.

Under the continuous leadership & vision of the group, it has carved a niche for itself in the auto products

Founded in the year 1981, Lumax Auto Technologies is a part of D.K Jain Group. The company commenced its operations with manufacture of 2-wheeler lighting.

Under the continuous leadership & vision of the group, it has carved a niche for itself in the auto products

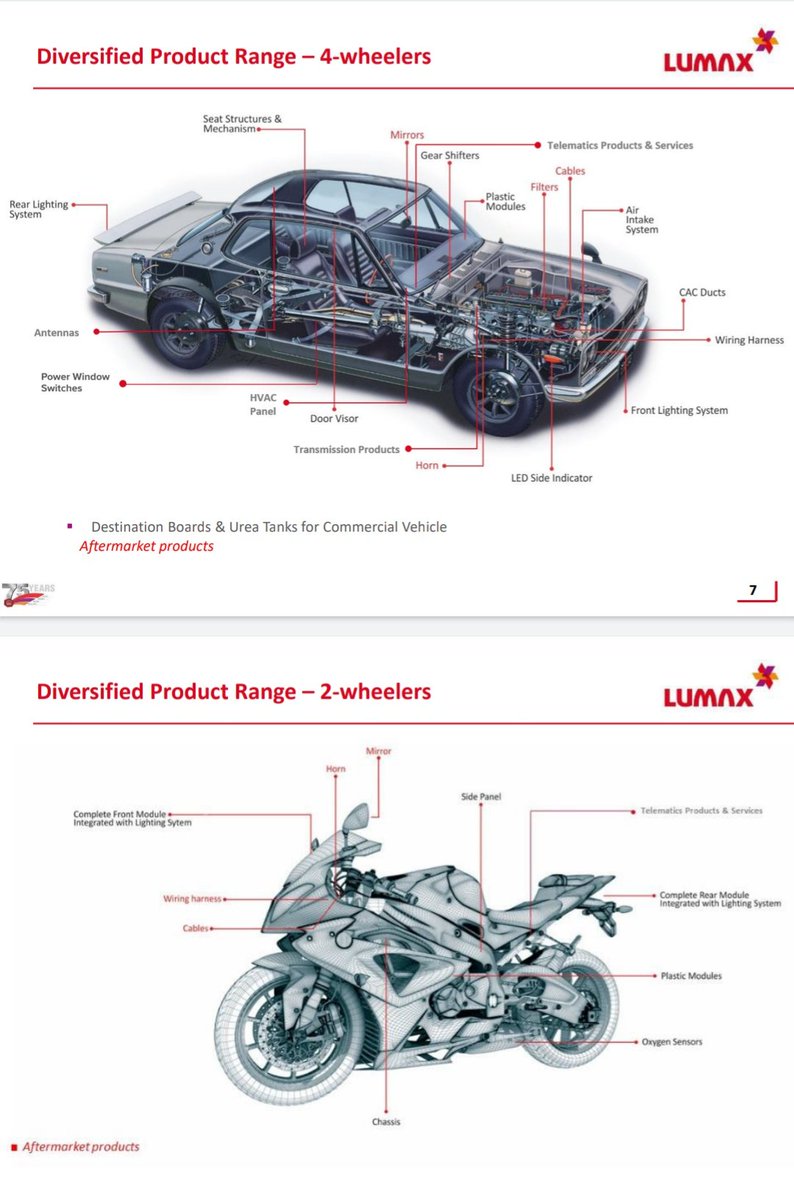

like intake systems, integrated plastic modules, 2-wheeler chassis & lighting, gear shifters, seat structures & mechanisms, electrical & electronics components, etc. for two, three and four wheeler segments with an experience of over three decades.

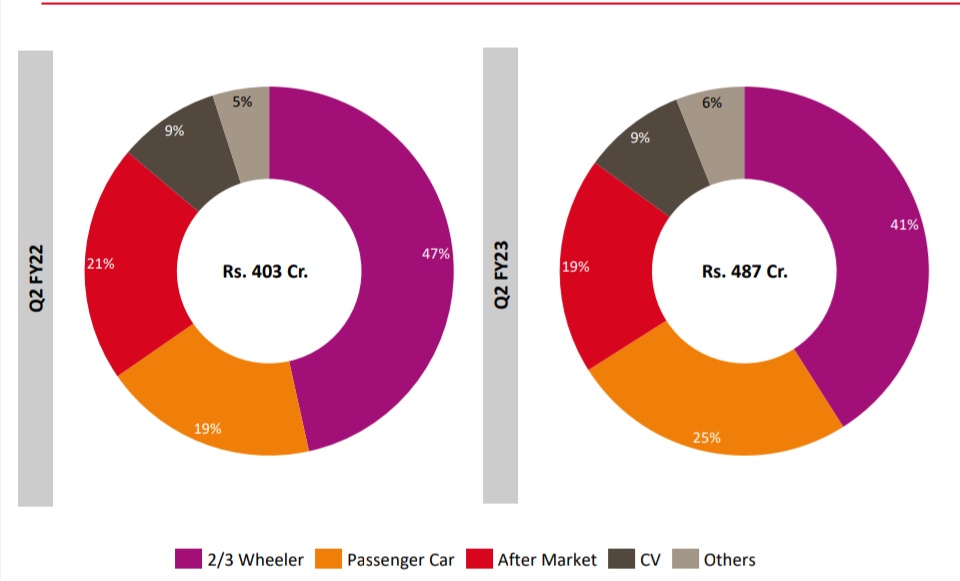

Segmental Revenue Break‐Up -

LATL earns 41% from 2/3 Wheelers,

25% from Passenger Car,

19% from After Market,

9% CV &

6% Others.

LATL earns 41% from 2/3 Wheelers,

25% from Passenger Car,

19% from After Market,

9% CV &

6% Others.

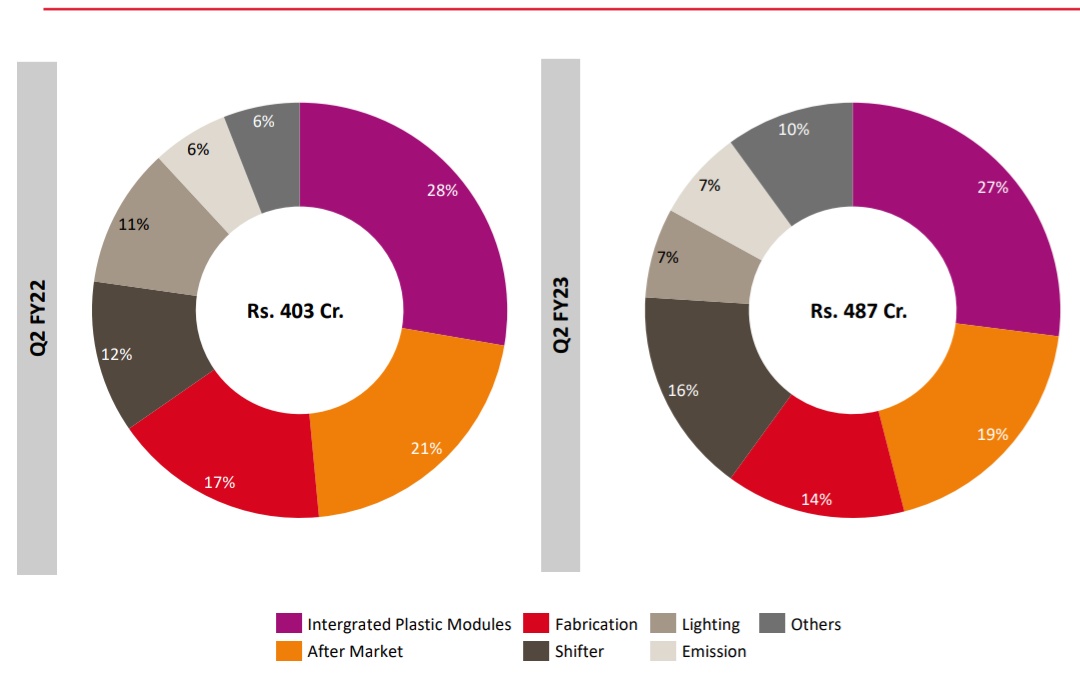

Product Wise Break-Up -

Lumax earns (27%) of it's revenue form Integrated Plastic Modules, (19%) from After Market , (14%) from Fabrication, (16%) Shifters, (7%) Lighting, (7%) Emission & (10%) Others.

Lumax earns (27%) of it's revenue form Integrated Plastic Modules, (19%) from After Market , (14%) from Fabrication, (16%) Shifters, (7%) Lighting, (7%) Emission & (10%) Others.

Financial Summary -

Q2 FY23 (YoY)

Revenue at ₹487 Cr vs ₹403 Cr ⬆️20.9%

EBITDA at ₹59.6 vs ₹47.8 ⬆️25%

PAT at ₹29.1 Cr vs ₹ 23.4 Cr ⬆️24%

LATL has recorded its highest ever quarterly & six monthly revenues at Rs.487 Cr and Rs.909 Cr

Q2 FY23 (YoY)

Revenue at ₹487 Cr vs ₹403 Cr ⬆️20.9%

EBITDA at ₹59.6 vs ₹47.8 ⬆️25%

PAT at ₹29.1 Cr vs ₹ 23.4 Cr ⬆️24%

LATL has recorded its highest ever quarterly & six monthly revenues at Rs.487 Cr and Rs.909 Cr

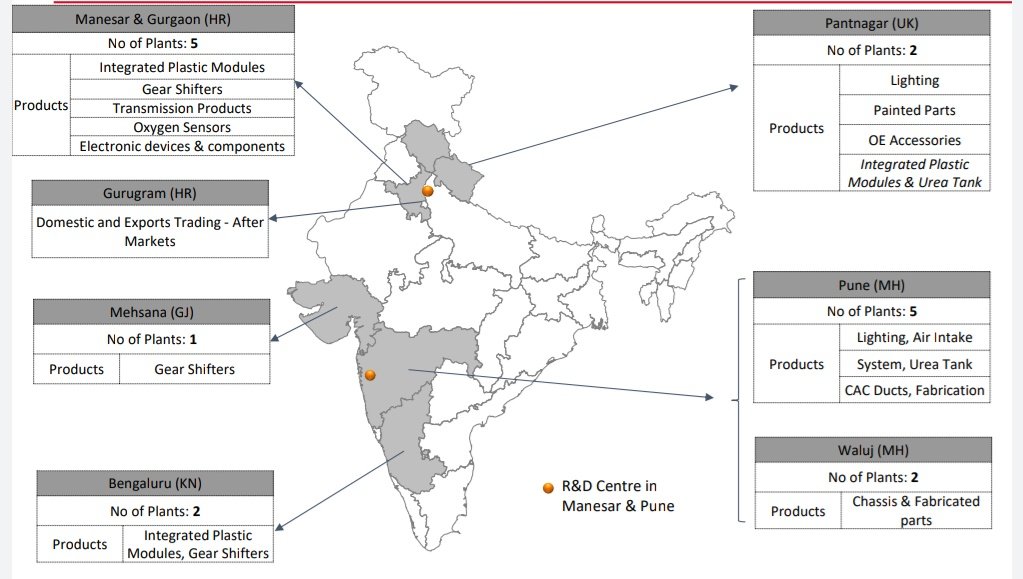

Manufacturing Facilities -

Lumax has 17 manufacturing facility spread across 5 states in India

&

2 R&D Centres in Manesar and Pune.

Lumax has 17 manufacturing facility spread across 5 states in India

&

2 R&D Centres in Manesar and Pune.

Fostering Partnerships to Deliver Excellence -

LATL has entered into JVs with global leaders to get technological advantage and launch better quality products.

LATL has entered into JVs with global leaders to get technological advantage and launch better quality products.

Key Triggers -

• Chosen under PLI scheme:

LATL & its JV subsidiaries, chosen for govt sops under the (PLI) scheme, is hopeful of investing a min. of ₹250Cr during 2022-27 even as the aim remains to generate 3x in terms of revenues from the proposed production capabilities.

• Chosen under PLI scheme:

LATL & its JV subsidiaries, chosen for govt sops under the (PLI) scheme, is hopeful of investing a min. of ₹250Cr during 2022-27 even as the aim remains to generate 3x in terms of revenues from the proposed production capabilities.

• Growing vehicle sales:

According to Crisil, CV & PV volume could grow 18% & 12%.

PV industry is witnessing strong improvement in sales. According to the data released by the Federation of Automobile Dealers Associations (FADA), passenger vehicle retail sales increased by 40%

According to Crisil, CV & PV volume could grow 18% & 12%.

PV industry is witnessing strong improvement in sales. According to the data released by the Federation of Automobile Dealers Associations (FADA), passenger vehicle retail sales increased by 40%

in October'22, compared to the same period last year. While CV segment

witnessed 25% YoY growth.

Two-wheelers sales recovered by 51% driven by the opening up of educational institutes & improved mobility.

witnessed 25% YoY growth.

Two-wheelers sales recovered by 51% driven by the opening up of educational institutes & improved mobility.

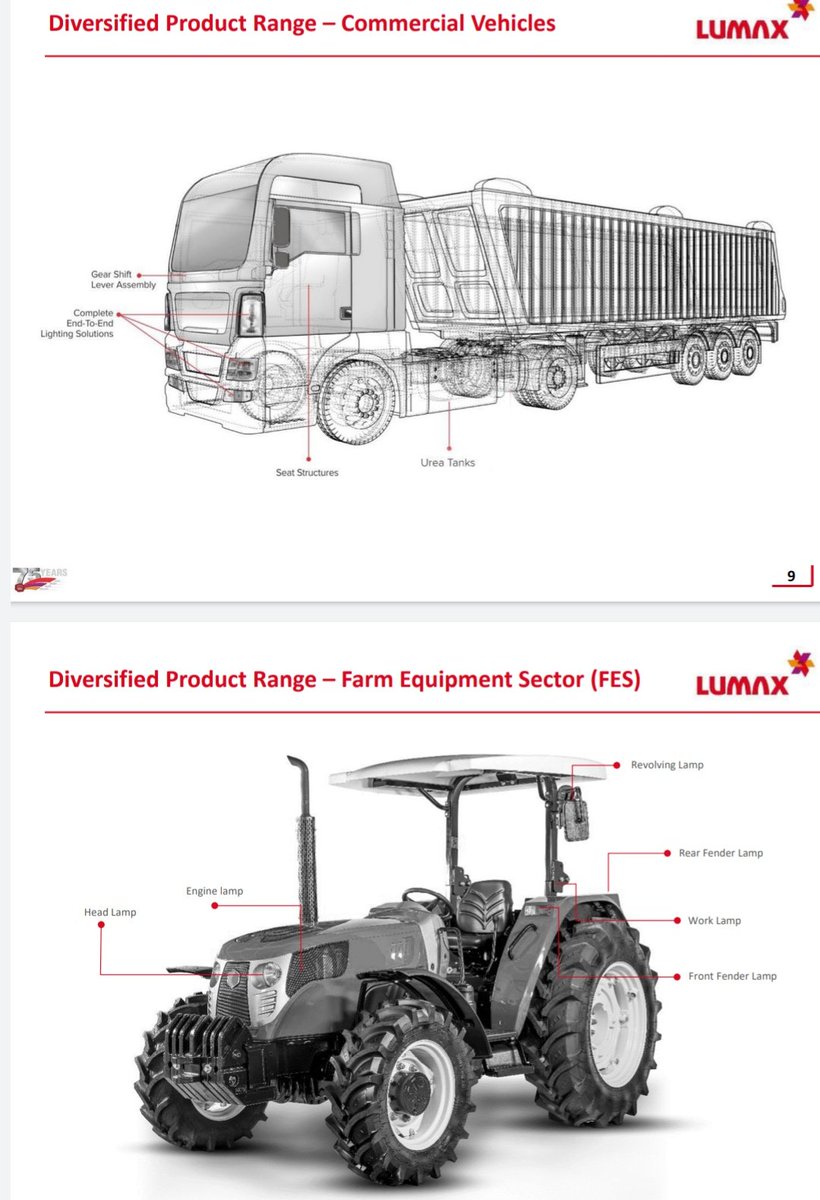

• Diversified product portfolio with strong growth potential:

LATL caters to 2W, 4W as well as CV segments of the automobile industry. This diversification helps the company to overcome downturn/cyclicality in any segment of automobile industry.

LATL caters to 2W, 4W as well as CV segments of the automobile industry. This diversification helps the company to overcome downturn/cyclicality in any segment of automobile industry.

Marquee OEM Customer Base -

LATL is one of the largest players in the automobile component segment in 🇮🇳, with presence across OEMs & aftermarket. It has been gaining market share with existing customers indicating quality & reliable products.

LATL is one of the largest players in the automobile component segment in 🇮🇳, with presence across OEMs & aftermarket. It has been gaining market share with existing customers indicating quality & reliable products.

Risks -

• Slowdown in the automobile industry:

Since LATL manufactures products which are consumed by the automobile industry any slowdown in the industry will directly impact the revenues of the company.

• Slowdown in the automobile industry:

Since LATL manufactures products which are consumed by the automobile industry any slowdown in the industry will directly impact the revenues of the company.

• Raw material price volatility:

Another cause of concern for LATL could be fluctuations in raw material prices, which could in turn impact the selling prices and realizations.

The main raw material used is polypropylene (PP), which is a downstream petrochemical product.

Another cause of concern for LATL could be fluctuations in raw material prices, which could in turn impact the selling prices and realizations.

The main raw material used is polypropylene (PP), which is a downstream petrochemical product.

Hence, the price of PP is directly linked to

crude oil rates, which are highly volatile.

crude oil rates, which are highly volatile.

• Working capital deterioration:

LATL currently has a Cash Conversion Cycle of just around 21 days. In case there is pressure on receivables, there can be deterioration in Free Cash Flow generation.

LATL currently has a Cash Conversion Cycle of just around 21 days. In case there is pressure on receivables, there can be deterioration in Free Cash Flow generation.

Fundamentals -

Market Cap : ₹ 1,764 Cr

P/E (Stock): 18.6

P/E (Industry): 38.77

P/B : 3.24

Debt to equity : 0.31

ROE : 13%

ROCE : 18.4%

EV/EBITDA : 9.1

Market Cap : ₹ 1,764 Cr

P/E (Stock): 18.6

P/E (Industry): 38.77

P/B : 3.24

Debt to equity : 0.31

ROE : 13%

ROCE : 18.4%

EV/EBITDA : 9.1

Conclusion -

Outlook for automobile demand is improving & LATL is witnessing increased offtake for its products.

It has added new models to its portfolio. The company is in talks with various OEMs for producing & developing products for their future EV requirement.

Outlook for automobile demand is improving & LATL is witnessing increased offtake for its products.

It has added new models to its portfolio. The company is in talks with various OEMs for producing & developing products for their future EV requirement.

It is also looking for inorganic growth opportunities in the non-EV space.

Company is expected to deliver healthy growth & outperform on the back of diverse product & client portfolio.

Company is expected to deliver healthy growth & outperform on the back of diverse product & client portfolio.

Please 🙏 like 👍,comment, retweet ♻️ if you find this 🧵 useful.

And follow us on @LnprCapital for more information like this.

And follow us on @LnprCapital for more information like this.

Loading suggestions...