Returns are not normally distributed.

Why do your metrics assume they are?

The Omega ratio considers the full distribution.

Here’s how in Python:

Why do your metrics assume they are?

The Omega ratio considers the full distribution.

Here’s how in Python:

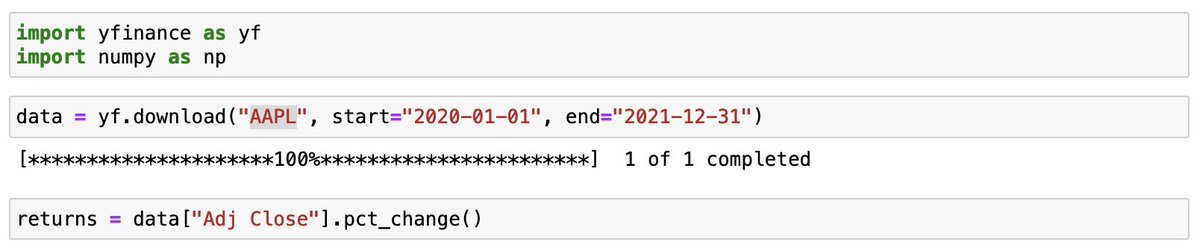

1/Get data

I use yfinance to get stock data in 1 line of code.

I use yfinance to get stock data in 1 line of code.

2/Build the Omega ratio

It’s calculus made easy. With Python.

It’s calculus made easy. With Python.

3/Analyze return the distribution

Asset returns are not normally distributed.

Asset returns are not normally distributed.

4/Compute the Omega ratio

Taking into consideration skew and kurtosis, AAPL’s gains outperformed the losses by a factor of 1.2.

Taking into consideration skew and kurtosis, AAPL’s gains outperformed the losses by a factor of 1.2.

I cover the details of the Omega ratio in a recent newsletter:

1. Get data

2. Compute Omega

3. Analyze distributions

You can read it here for free:

pyquantnews.com

1. Get data

2. Compute Omega

3. Analyze distributions

You can read it here for free:

pyquantnews.com

Loading suggestions...