(1/16)

About:

UML is one of the leading global manufacturers of steel wire & wire ropes. Its manufacturing plants are located in Ranchi and Hoshiarpur in India, and in Thailand, Dubai and the UK overseas.

About:

UML is one of the leading global manufacturers of steel wire & wire ropes. Its manufacturing plants are located in Ranchi and Hoshiarpur in India, and in Thailand, Dubai and the UK overseas.

(2/16)

It’s Products:

• Anchor Mooring Rope

• Crane Rope

• Mooring Rope

• Locked Coil Rope

• LRPC

• Wire

• Cables

• Welding Wire

• Fishing Rope

• Jelly Filled Telephone Copper Cables

It’s Products:

• Anchor Mooring Rope

• Crane Rope

• Mooring Rope

• Locked Coil Rope

• LRPC

• Wire

• Cables

• Welding Wire

• Fishing Rope

• Jelly Filled Telephone Copper Cables

(3/16)

Key Focus Area Going forward:

• Reducing low contributory items

and focusing more on high value-added products

• Focus on areas like enlarging

product basket

• The Company aims to increase its global footprint in the mining segment

Key Focus Area Going forward:

• Reducing low contributory items

and focusing more on high value-added products

• Focus on areas like enlarging

product basket

• The Company aims to increase its global footprint in the mining segment

(4/16)

Opportunities:

• Leveraging higher plant productivity resulting from

refurbishment of machines to increase market share in products with supply constraints.

• Increasing activity in Oil and Offshore markets globally to boost demand for specialty products.

Opportunities:

• Leveraging higher plant productivity resulting from

refurbishment of machines to increase market share in products with supply constraints.

• Increasing activity in Oil and Offshore markets globally to boost demand for specialty products.

(5/16)

Industries UML Caters to:

• Construction/ Infrastructure

• Elevator

• Crane

• Mining

• Oil & Gas

• Automobile

• Fishing

• Steel Plants

• Power Plant

• Shipping

• Material/ Passenger Transportation

Industries UML Caters to:

• Construction/ Infrastructure

• Elevator

• Crane

• Mining

• Oil & Gas

• Automobile

• Fishing

• Steel Plants

• Power Plant

• Shipping

• Material/ Passenger Transportation

(6/16)

Key Q2 highlights:

• Capex program underway to increase capacity and capability across product segments

• Company faced many headwinds which were mostly macro economic like High inflation, monetary tightening, strengthening USD & Global demand slowdown

Key Q2 highlights:

• Capex program underway to increase capacity and capability across product segments

• Company faced many headwinds which were mostly macro economic like High inflation, monetary tightening, strengthening USD & Global demand slowdown

(7/16)

Update on Realisation from UML’s steel division to TSLPL in April 2019:

UML received ₹43.65 billion (96.5% of the total sum) in FY21.

42% of balance was realised in FY22. The remaining balance of ₹93.5cr is likely to be released in this fiscal.

Update on Realisation from UML’s steel division to TSLPL in April 2019:

UML received ₹43.65 billion (96.5% of the total sum) in FY21.

42% of balance was realised in FY22. The remaining balance of ₹93.5cr is likely to be released in this fiscal.

(8/16)

Key Strengths:

• Leading Player in the Wire and Wire Rope Business:

UML is the market leader in the Indian wire and wire rope space and is among the top five leading manufacturers globally. The company caters to various non-correlated end-user industries cited above.

Key Strengths:

• Leading Player in the Wire and Wire Rope Business:

UML is the market leader in the Indian wire and wire rope space and is among the top five leading manufacturers globally. The company caters to various non-correlated end-user industries cited above.

(9/16)

• Stable Revenue:

UML largely manufactures wire rope products which are customised based on the consumers’ requirements, thus commanding higher & more stable realisations than commodity products.

They have been successful so far to maintain its market share.

• Stable Revenue:

UML largely manufactures wire rope products which are customised based on the consumers’ requirements, thus commanding higher & more stable realisations than commodity products.

They have been successful so far to maintain its market share.

(10/16)

• Pricing Power with no supply glitches:

UML had entered into an agreement with TSLPL for the supply of 1LTPA of wire rods up to FY24; thus ensuring 50% RM availability.

Since production is order-based, UML has been able to pass on volatility in RM prices to clients.

• Pricing Power with no supply glitches:

UML had entered into an agreement with TSLPL for the supply of 1LTPA of wire rods up to FY24; thus ensuring 50% RM availability.

Since production is order-based, UML has been able to pass on volatility in RM prices to clients.

(11/16)

Liquidity:

The company’s average utilisation of fund-based facilities for the 12 months ended Q1FY23 was around 40%, indicating adequate liquidity.

Capex of ₹250cr will mostly make its CF negative in FY23.

Cash & CE fell from ₹154cr in April,23 to ₹86cr in Sep,23

Liquidity:

The company’s average utilisation of fund-based facilities for the 12 months ended Q1FY23 was around 40%, indicating adequate liquidity.

Capex of ₹250cr will mostly make its CF negative in FY23.

Cash & CE fell from ₹154cr in April,23 to ₹86cr in Sep,23

(12/16)

Large Self-funded Capex:

UML is undertaking debottlenecking & upgradation of the plant at Ranchi, which shall enhance its overall capacity by 25% by FYE25. The capacities will become operational in phases over FY23-25 & will be funded by internal accruals.

Large Self-funded Capex:

UML is undertaking debottlenecking & upgradation of the plant at Ranchi, which shall enhance its overall capacity by 25% by FYE25. The capacities will become operational in phases over FY23-25 & will be funded by internal accruals.

(13/16)

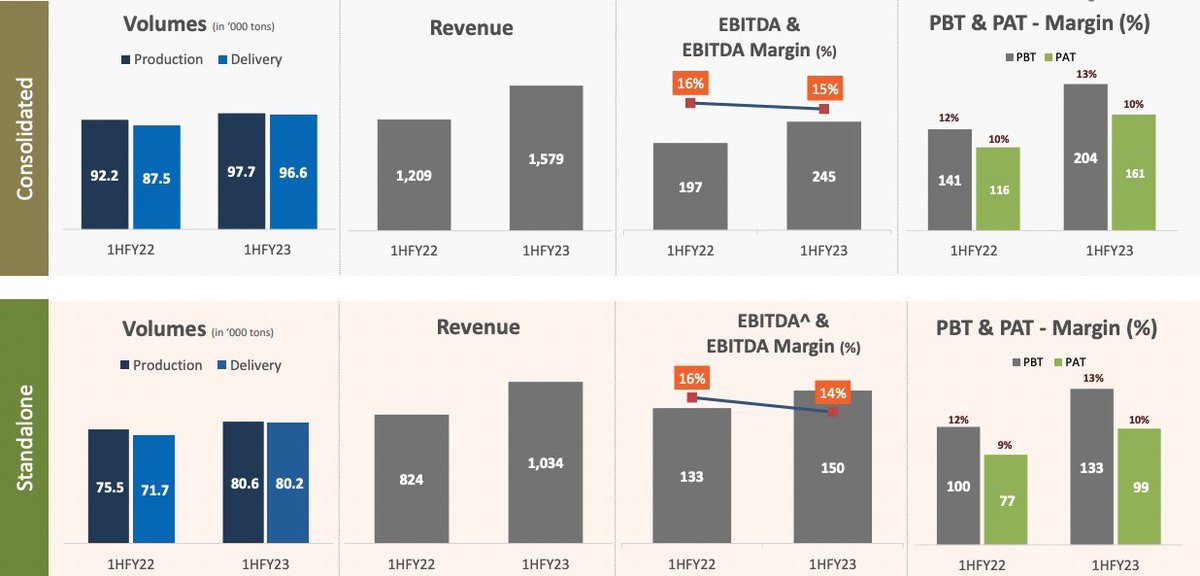

• The capacity expansion plan includes adding new high-value, high-margin products to it’s portfolio.

These high margin products will improve its EBITDA going forward which is currently range bound between 12-14%.

Keep an eye on its EBITDA trend.

• The capacity expansion plan includes adding new high-value, high-margin products to it’s portfolio.

These high margin products will improve its EBITDA going forward which is currently range bound between 12-14%.

Keep an eye on its EBITDA trend.

(14/16)

Contingent Liability:

UML had long-standing contingent liabilities, amounting to INR3.95 billion at FYE22.

It has an ongoing Central Bureau of Investigation’s (CBI) enquiry with respect to the sale of iron ore fines from its captive mines over FY06-FY10.

Contingent Liability:

UML had long-standing contingent liabilities, amounting to INR3.95 billion at FYE22.

It has an ongoing Central Bureau of Investigation’s (CBI) enquiry with respect to the sale of iron ore fines from its captive mines over FY06-FY10.

(15/16)

Key Numbers & Ratios:

• Market Cap: ₹ 4,056 Cr

• Stock P/E: 13.3 vs Ind P/E: 17.16

• RoCE: 17.2 %

• RoE: 17.1%

• PEG: 0.61

• Sales 3 year CAGR: 2.61%

• Price to Sales: 1.33

• NPM Last year: 9.84%

• OPM Q2FY23: 14%

• D/E: 0.24

Key Numbers & Ratios:

• Market Cap: ₹ 4,056 Cr

• Stock P/E: 13.3 vs Ind P/E: 17.16

• RoCE: 17.2 %

• RoE: 17.1%

• PEG: 0.61

• Sales 3 year CAGR: 2.61%

• Price to Sales: 1.33

• NPM Last year: 9.84%

• OPM Q2FY23: 14%

• D/E: 0.24

(16/16)

UML is primarily focusing on improving its product mix to derive strong CF generation.

All eyes will be on its new High value high margin products which will give its EBITDA a much needed growth.

What are your thoughts about Usha Martin?

@caniravkaria @kuttrapali26

UML is primarily focusing on improving its product mix to derive strong CF generation.

All eyes will be on its new High value high margin products which will give its EBITDA a much needed growth.

What are your thoughts about Usha Martin?

@caniravkaria @kuttrapali26

Loading suggestions...